Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Regency Centers Corporation (NYSE:NASDAQ:REG), a leading owner, operator, and developer of open-air shopping centers, released its first quarter 2025 earnings presentation on April 30, 2025. The company’s stock is currently trading at $71.85, approaching its 52-week high of $78.18, reflecting investor confidence in its operational strategy and growth outlook.

Following a Q4 2024 performance that slightly missed analyst expectations with an EPS of $0.47 versus the forecasted $0.48, Regency is projecting stronger performance for 2025, underpinned by high occupancy rates and a substantial development pipeline.

Executive Summary

Regency Centers has positioned itself as a premier retail REIT with strategic advantages in portfolio quality, operational expertise, and financial strength. The company’s presentation highlights its focus on necessity-based retail, with over 80% of its portfolio being grocery-anchored properties in suburban trade areas.

The company is guiding for 3.2% to 4.0% same-property NOI growth in 2025, supported by peak occupancy levels of 96.5% and a significant pipeline of signed-but-not-occupied leases that will commence throughout the year. With approximately $500 million in development and redevelopment projects in process and a recent $119 million acquisition in Nashville, Regency continues to execute on its growth strategy while maintaining balance sheet discipline.

As shown in the following strategic advantages overview:

Financial Guidance & Performance Highlights

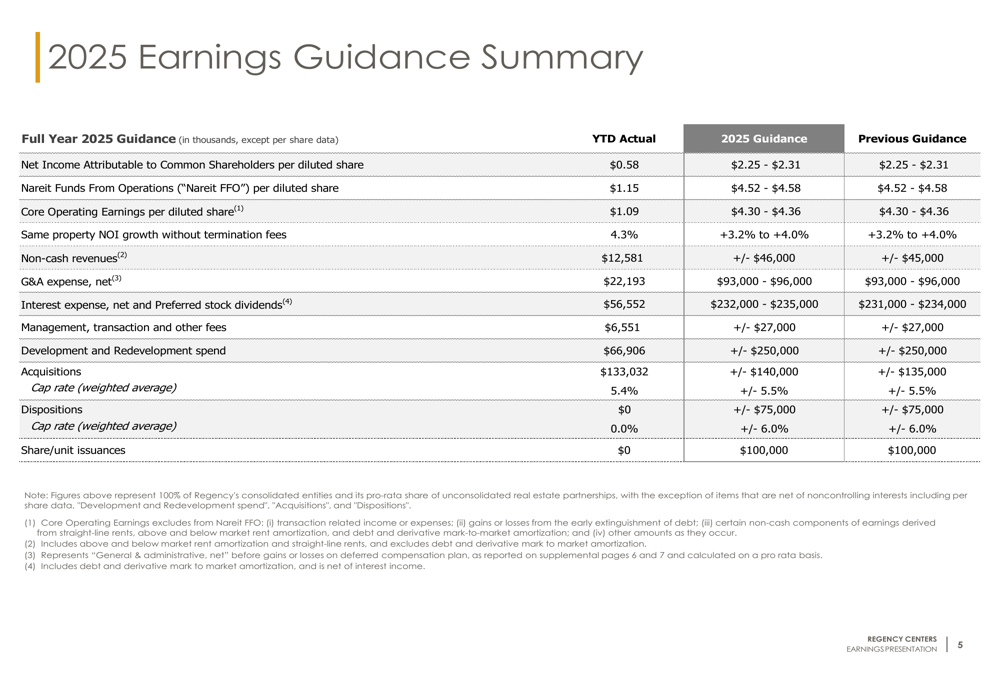

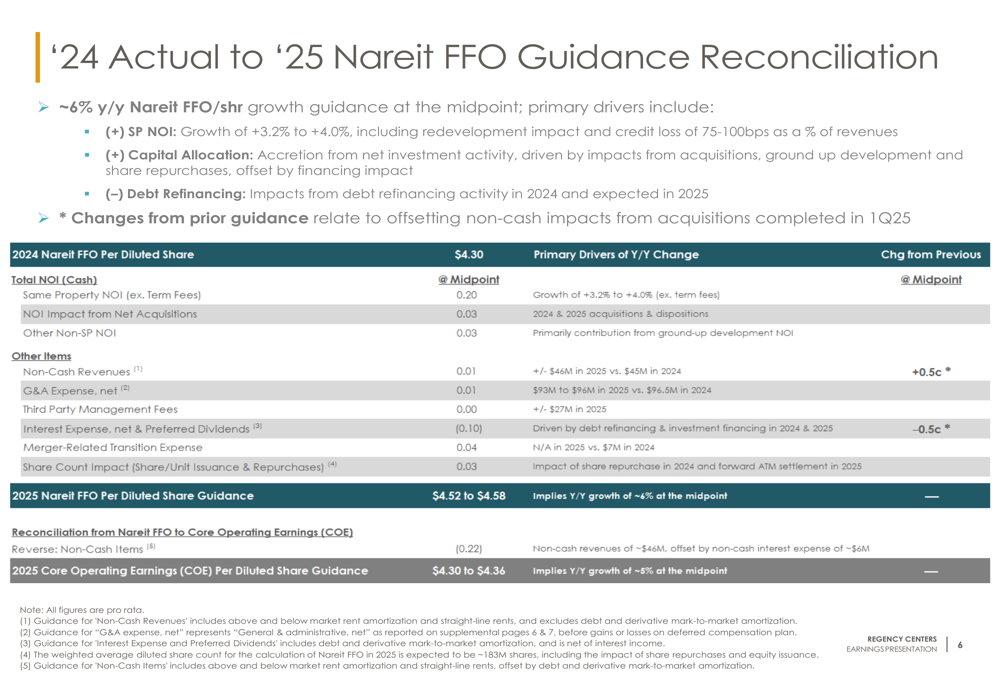

Regency’s 2025 financial guidance reflects confidence in continued operational strength. The company is projecting Net Income Attributable to Common Shareholders per diluted share of $2.25-$2.31 and Nareit Funds From Operations (FFO) per diluted share of $4.52-$4.58, representing nearly 6% year-over-year growth from 2024’s $4.30 per share.

The detailed financial guidance summary provides a comprehensive view of Regency’s expectations:

The company has clearly outlined the drivers behind its projected FFO growth, with same property NOI growth contributing approximately $0.20 per share to the year-over-year increase. Additional contributions come from NOI impact from net acquisitions ($0.03) and other non-same property NOI ($0.03).

The following reconciliation illustrates the bridge from 2024 actual results to 2025 guidance:

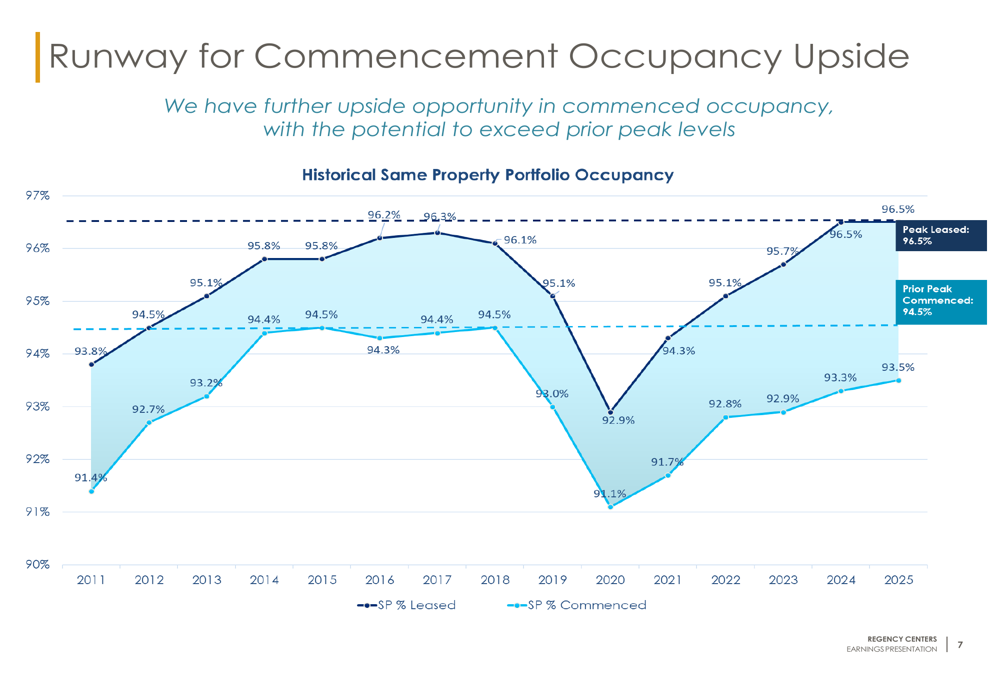

A key driver of Regency’s projected NOI growth is the spread between leased and commenced occupancy. The company’s same property portfolio is currently 96.5% leased, matching its historical peak, while commenced occupancy lags by approximately 300 basis points. This gap represents significant embedded growth potential as these leases commence operations and begin paying rent.

The historical occupancy trends demonstrate this opportunity:

Strategic Initiatives & Development Pipeline

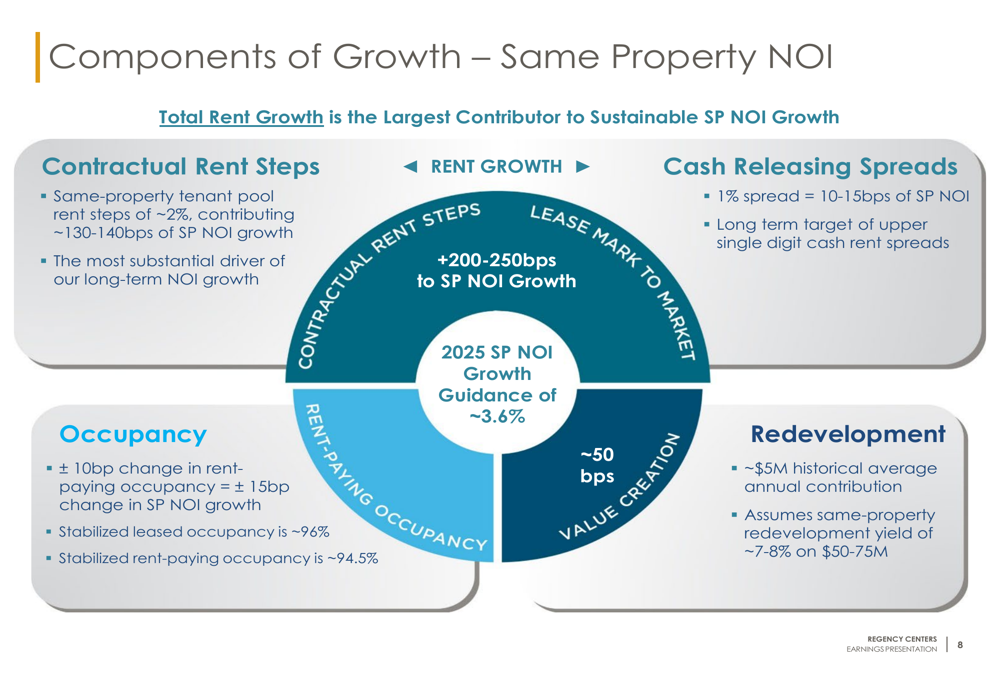

Regency’s same property NOI growth is supported by multiple components, with contractual rent steps contributing 200-250 basis points, strong releasing spreads, and contributions from redevelopment projects. The company targets upper single-digit cash rent spreads and notes that a 10 basis point change in rent-paying occupancy translates to approximately 15 basis points in same property NOI growth.

The components of growth are clearly illustrated in this breakdown:

A significant growth driver for Regency is its signed-not-occupied (SNO) pipeline, which represents approximately $46 million of incremental base rent. The company expects 80% of this ABR to commence by the end of fiscal year 2025, with full commencement by 2026. This pipeline is diversified across both shop space (58%) and anchor tenants (42%), with 37% tied to redevelopment projects.

Regency’s tenant mix remains focused on necessity, service, convenience, and value retail, with grocery anchors accounting for 20% of annualized base rent and restaurants comprising 19%. This focus on essential retail has proven resilient through various economic cycles.

The company’s development and redevelopment pipeline includes approximately $500 million of in-process projects expected to stabilize over the next three years. These projects are strategically phased to provide steady NOI contributions:

Balance Sheet Strength & Capital Allocation

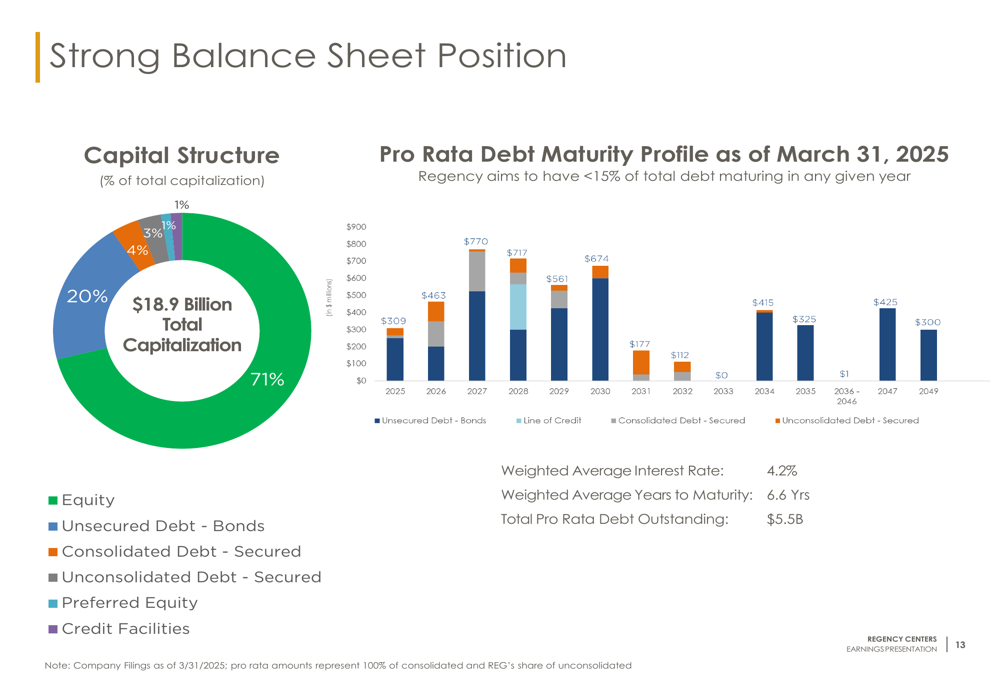

Regency continues to maintain one of the strongest balance sheets in the retail REIT sector, with sector-leading credit ratings (Moody’s A3 / S&P A-) and a trailing 12-month Debt & Preferred Stock-to-EBITDAre ratio of 5.3x. The company has approximately $1.2 billion in revolver availability, providing significant financial flexibility.

The capital structure is conservatively weighted toward equity (71%), with a well-laddered debt maturity profile. The weighted average interest rate on debt is 4.2% with a weighted average maturity of 6.6 years.

The following chart illustrates Regency’s strong balance sheet position:

In Q1 2025, Regency completed the acquisition of Brentwood Place, a 320,000 square foot community center in an affluent Nashville submarket. The $119 million acquisition is anchored by TJ Maxx/HomeGoods, Nordstrom (NYSE:JWN) Rack, Total (EPA:TTEF) Wine, and Golf Galaxy, and represents the company’s continued focus on high-quality retail assets in growing markets.

Forward-Looking Statements

Looking ahead, Regency Centers is well-positioned to deliver on its 2025 guidance, with multiple growth drivers in place. The company’s focus on necessity-based retail in suburban locations, combined with its development expertise and strong balance sheet, provides a solid foundation for continued performance.

Management has emphasized the importance of its development platform as a key differentiator, a sentiment echoed in previous earnings calls. The company plans to continue its approximately $250 million annual development program, focusing on strategic growth through both ground-up development and redevelopment projects.

While the retail environment continues to face challenges from tenant failures and move-outs, Regency’s diversified tenant mix and focus on necessity retail help mitigate these risks. The company’s guidance incorporates credit loss forecasts in line with historical averages.

As retail real estate supply remains constrained in many markets, Regency’s existing portfolio and development capabilities position it to capitalize on the demand for high-quality retail space, particularly in growing suburban markets where the company has established a strong presence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.