Street Calls of the Week

Introduction & Market Context

Regency Centers Corporation (NYSE:NASDAQ:REG) presented its second quarter 2025 results on July 30, showing continued momentum in its retail-focused real estate portfolio. The shopping center REIT’s stock responded positively, trading up 2.11% to $73.28 following the presentation, approaching its 52-week high of $78.18.

The company’s presentation highlighted its strategic positioning as a leading owner, operator, and developer of open-air shopping centers, with 85% of its 480+ properties being grocery-anchored centers focused on necessity, service, convenience, and value retailers.

Quarterly Performance Highlights

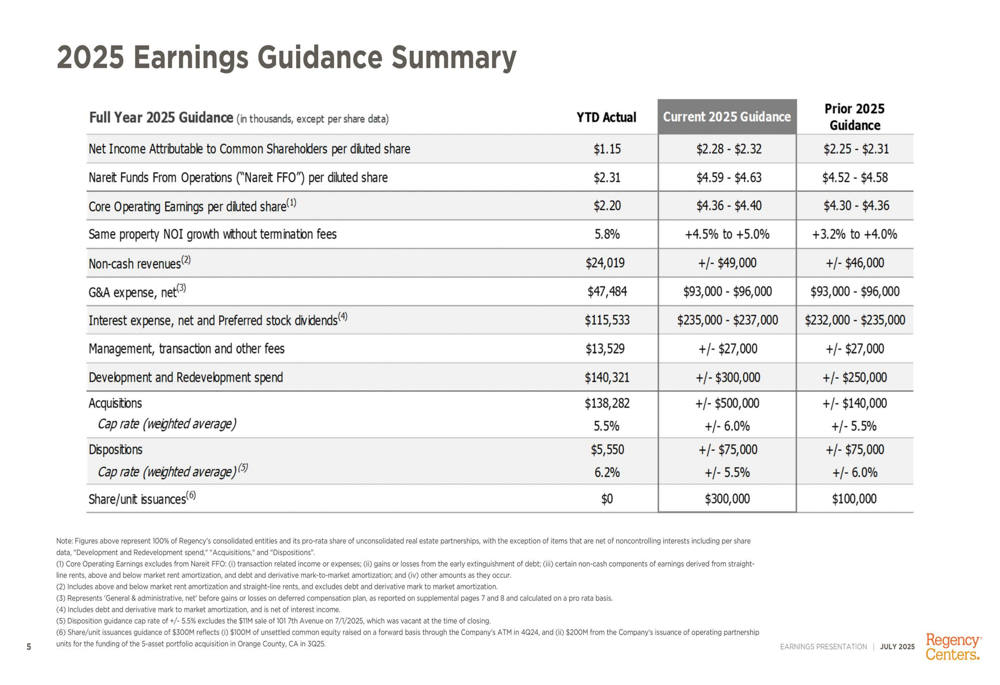

Regency Centers raised its 2025 guidance across all key metrics, reflecting strong second-quarter performance and improved outlook for the remainder of the year. The company now expects Net Income per diluted share of $2.28-$2.32, up from its previous guidance of $2.25-$2.31.

As shown in the following comprehensive guidance summary:

The most notable improvement came in same property NOI growth, which is now projected at +4.5% to +5.0%, significantly higher than the prior guidance of +3.2% to +4.0%. This follows the strong momentum established in Q1 2025, when the company reported same property NOI growth of 4.3%.

Regency’s Nareit Funds From Operations (FFO) guidance was raised to $4.59-$4.63 per diluted share, up from $4.52-$4.58, representing approximately 7% year-over-year growth at the midpoint. Core Operating Earnings guidance was similarly increased to $4.36-$4.40 per diluted share.

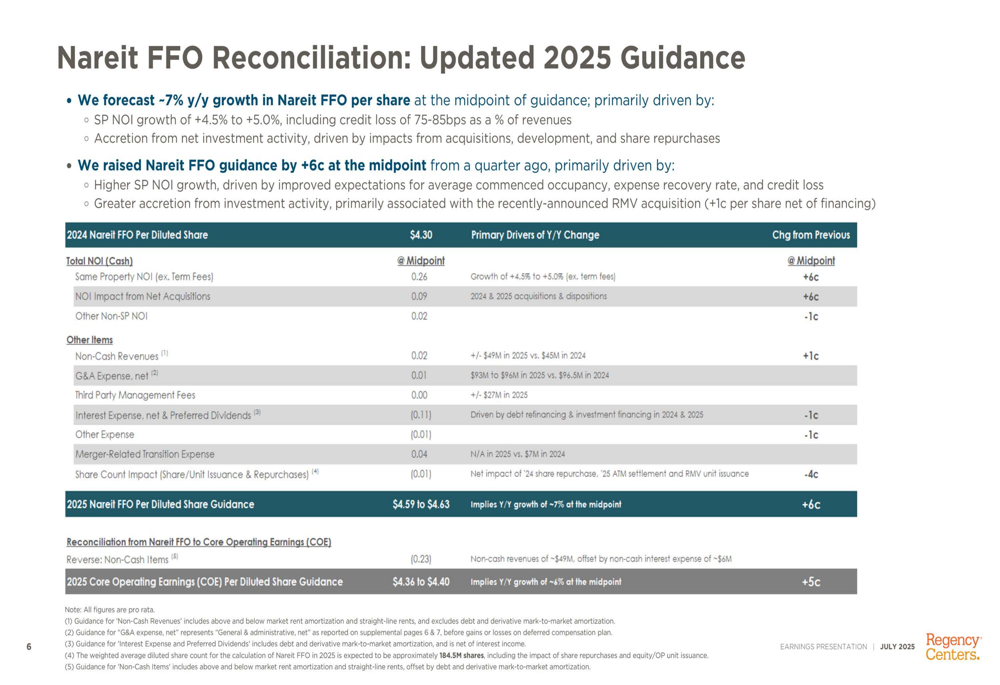

The company provided a detailed reconciliation of the factors driving its improved outlook:

Strategic Initiatives

A significant highlight of the presentation was Regency’s announcement of the Rancho Mission Viejo ("RMV") portfolio acquisition in Southern California, completed on July 23, 2025, for $357 million. This strategic acquisition comprises five high-quality centers totaling approximately 630,000 square feet in South Orange County, featuring strong demographics with a three-mile average household income exceeding $200,000.

The acquisition details, including property images and financing structure, were presented as follows:

The transaction was funded primarily through operating partnership units at $72 per share and the assumption of $150 million of debt at a favorable 4.2% weighted average interest rate with an average term to maturity of approximately 12 years. The acquisition is expected to contribute approximately 1 cent per share to Nareit FFO, as noted in the company’s guidance reconciliation.

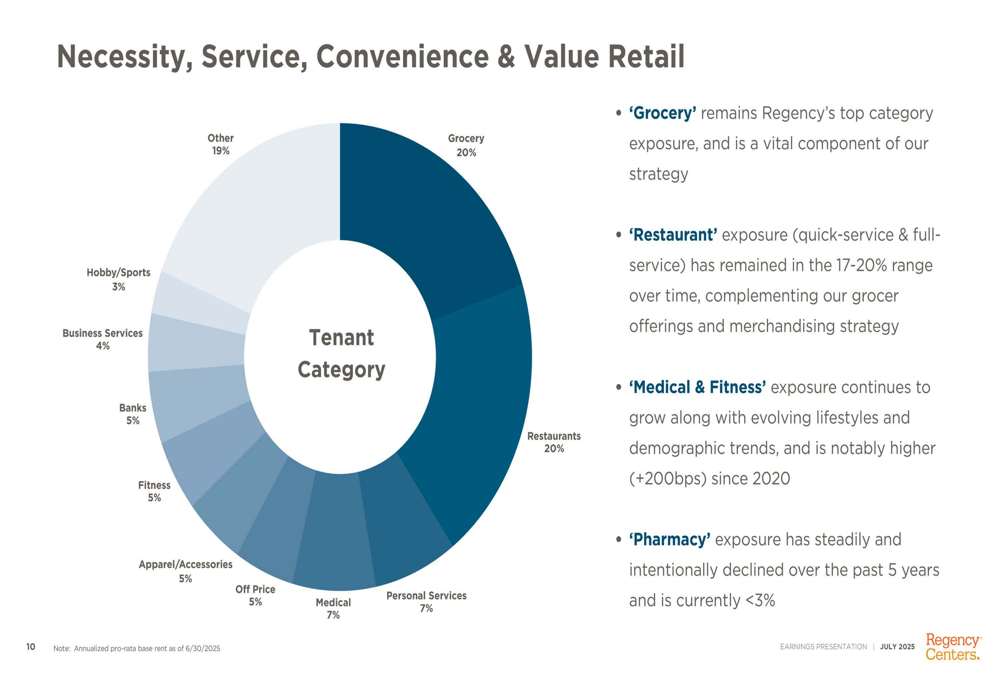

Regency continues to emphasize its tenant mix strategy focused on necessity, service, convenience, and value retail. The company’s portfolio composition shows grocery anchors representing 20% of annualized base rent, with restaurants also accounting for 20%.

Forward-Looking Statements

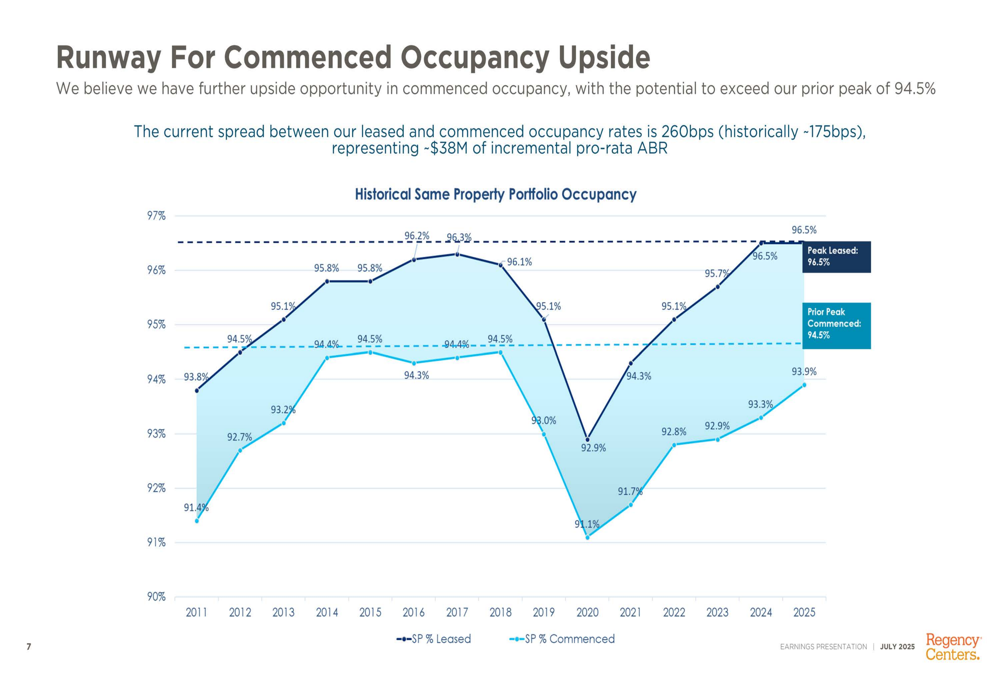

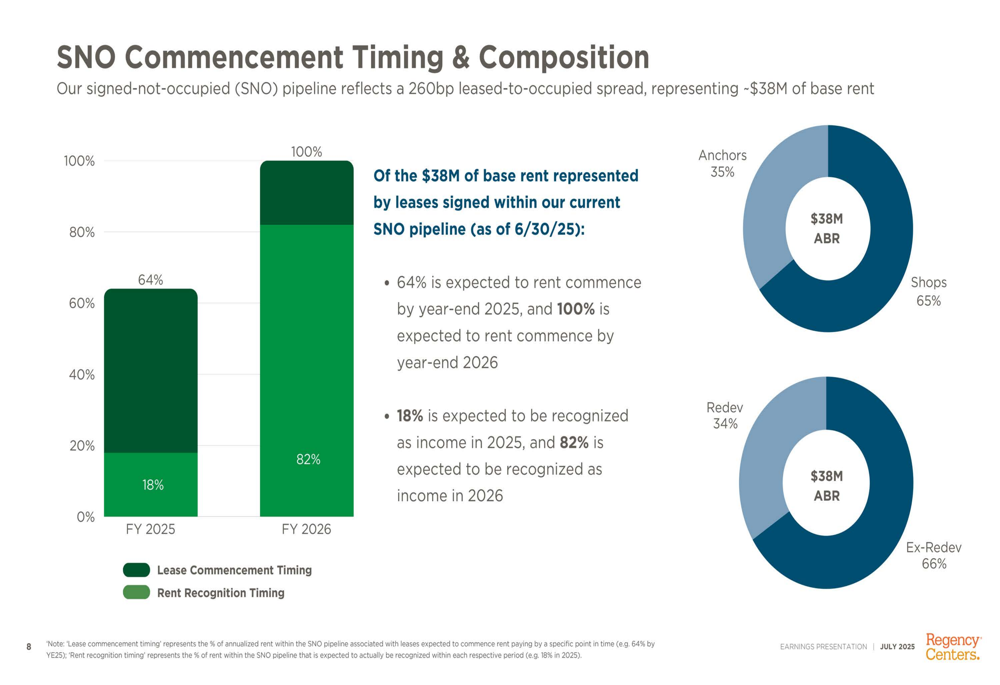

A key driver of Regency’s improved outlook is the significant spread between leased and commenced occupancy, currently at 260 basis points compared to a historical average of approximately 175 basis points. This spread represents approximately $38 million of incremental pro-rata annualized base rent that will materialize as tenants take occupancy and begin paying rent.

The following chart illustrates this occupancy trend and potential upside:

The company provided additional detail on the timing of this revenue recognition, noting that 64% of the $38 million in signed-not-occupied leases is expected to commence by year-end 2025, with the remainder commencing in 2026:

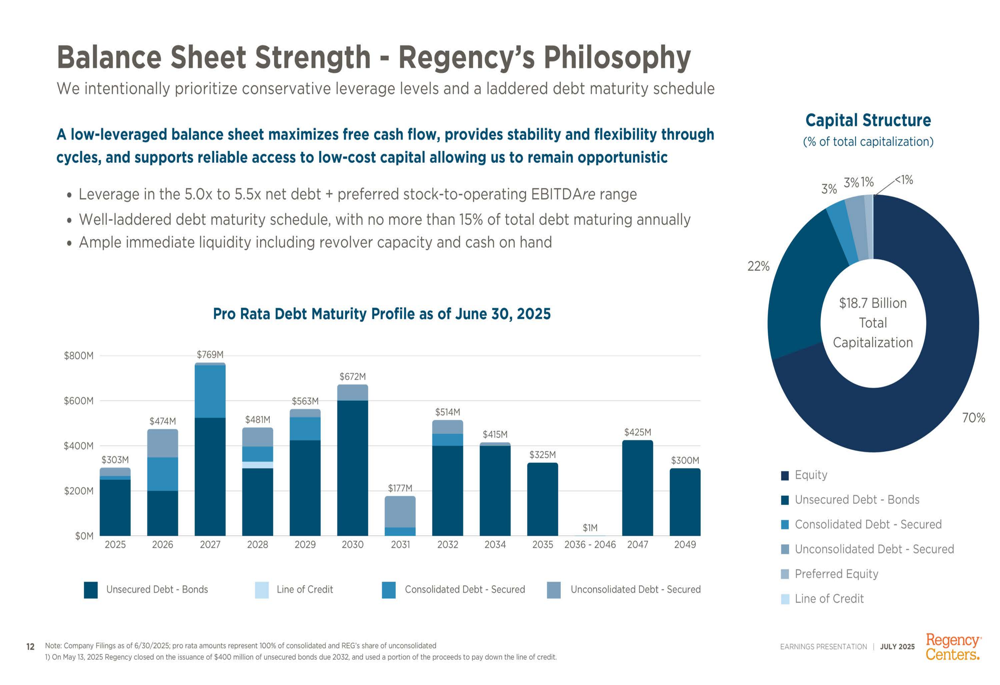

Regency maintains a strong balance sheet with conservative leverage metrics, positioning the company for continued growth. The company reported Net Debt & Preferred Stock to Trailing 12-Month EBITDAre of 5.3x, with approximately $1.5 billion in revolver availability as of June 30, 2025.

The company’s capital structure and debt maturity profile demonstrate its financial flexibility:

Competitive Industry Position

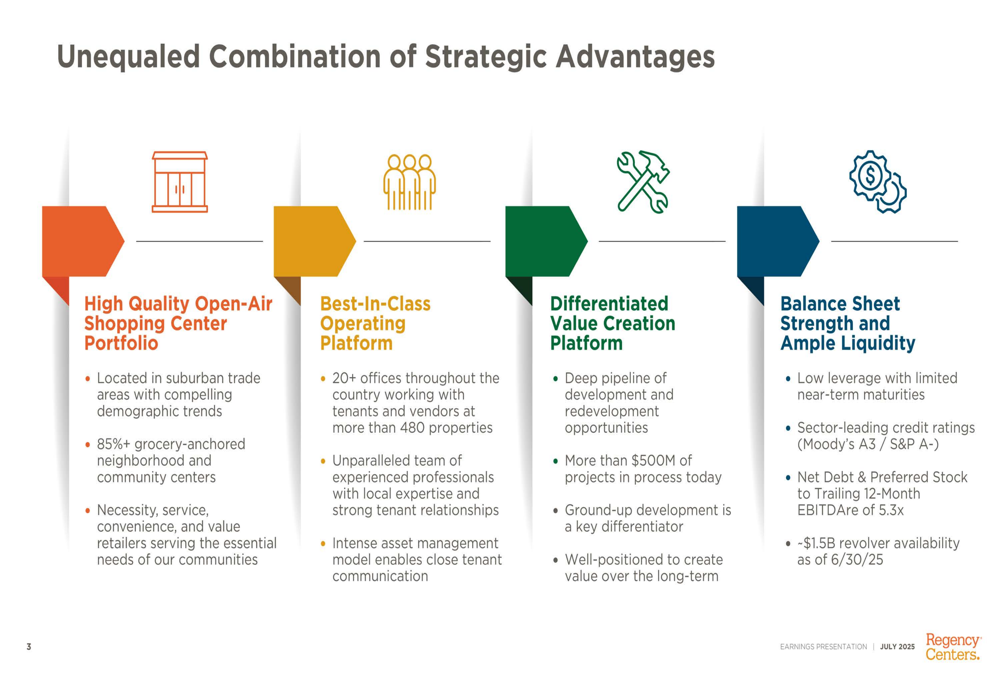

Regency Centers highlighted its strategic advantages in the competitive retail REIT landscape, emphasizing four key differentiators: its high-quality open-air shopping center portfolio, best-in-class operating platform, differentiated value creation capabilities, and balance sheet strength.

The company’s strategic positioning was summarized as follows:

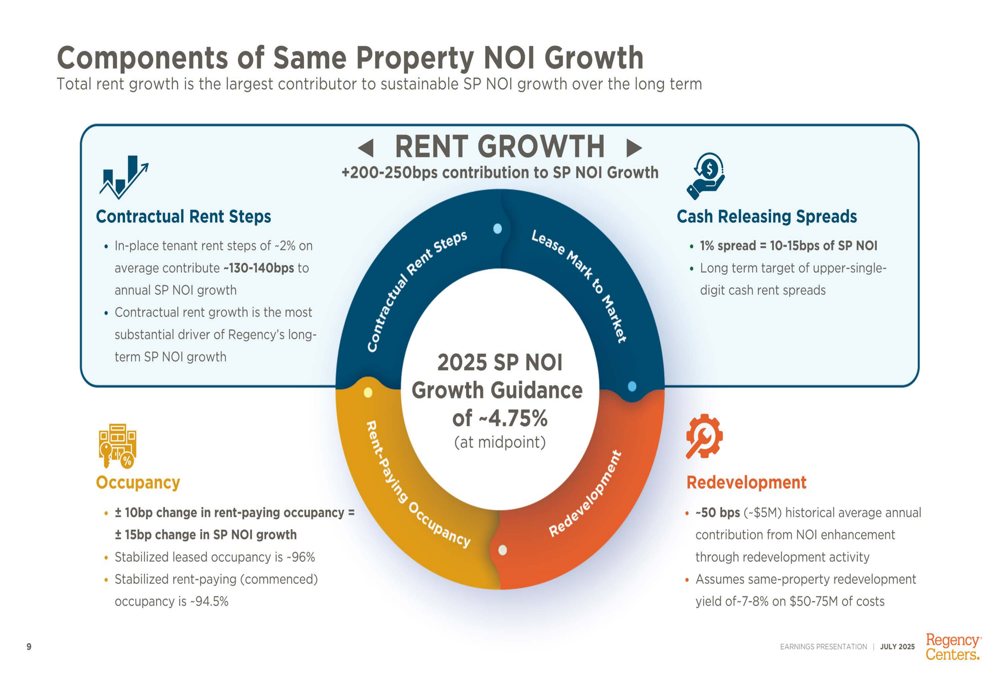

Regency’s focus on components driving same property NOI growth shows a comprehensive approach to value creation, with contractual rent growth contributing 200-250 basis points annually, complemented by occupancy gains and redevelopment initiatives:

With its updated guidance, strategic acquisition activity, and significant occupancy upside potential, Regency Centers appears well-positioned to continue its growth trajectory through the remainder of 2025, building on the strong performance demonstrated in the first quarter when the company significantly exceeded earnings expectations with an EPS of 1.09 compared to the forecast of 0.5458.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.