Gold bars to be exempt from tariffs, White House clarifies

Regions Financial Corporation (NYSE:RF) reported solid second-quarter 2025 results on July 18, with adjusted earnings per share of $0.60 and improved guidance for the full year, showcasing the bank’s continued momentum in a challenging environment.

Quarterly Performance Highlights

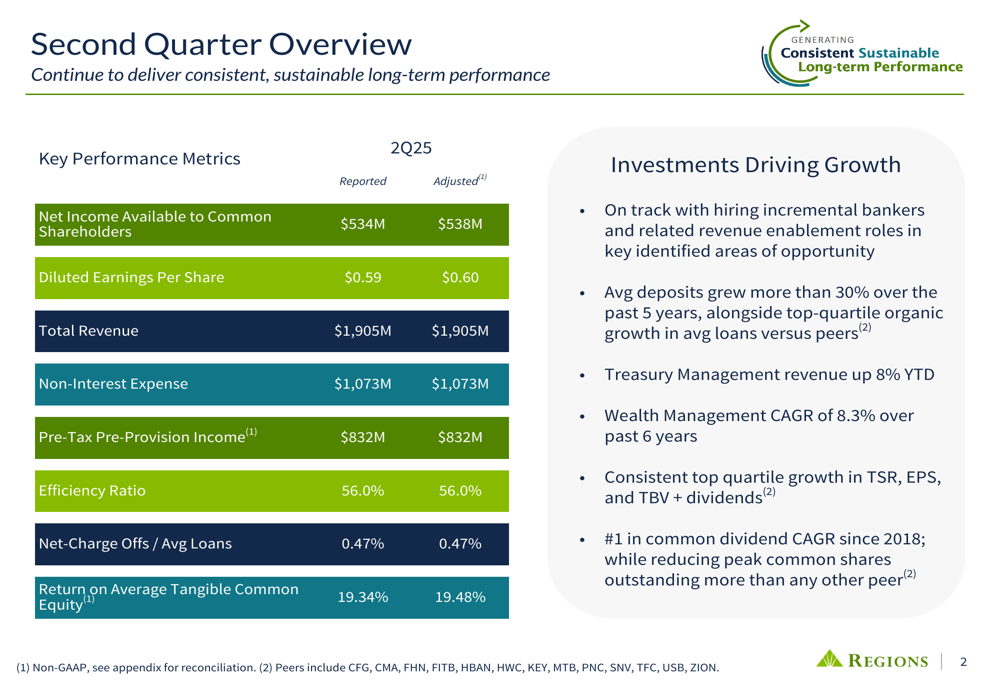

Regions delivered adjusted earnings per share of $0.60 for the second quarter, up from $0.54 in Q1 2025, with reported net income available to common shareholders reaching $534 million. The company achieved total revenue of $1.9 billion and pre-tax pre-provision income of $832 million, demonstrating strong operational performance with an efficiency ratio of 56.0%.

Return on average tangible common equity remained robust at 19.48% on an adjusted basis, positioning Regions favorably among its peers. The company’s performance was driven by growth in both net interest income and non-interest income, alongside disciplined expense management.

As shown in the following comprehensive performance overview:

Detailed Financial Analysis

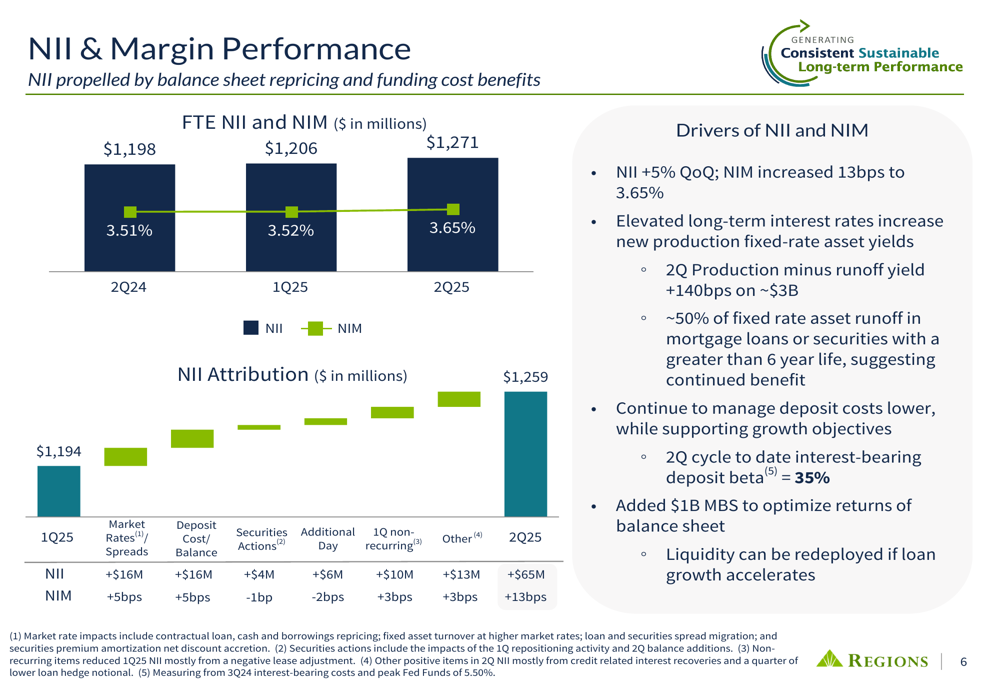

Regions’ net interest income increased 5% quarter-over-quarter, with net interest margin expanding by 13 basis points to 3.65%. This improvement was driven by higher long-term interest rates increasing new production fixed-rate asset yields, with new production exceeding runoff yield by 140 basis points on approximately $3 billion. The company also continued to manage deposit costs lower, with a cycle-to-date interest-bearing deposit beta of 35%.

The following chart illustrates the strong NII and margin performance:

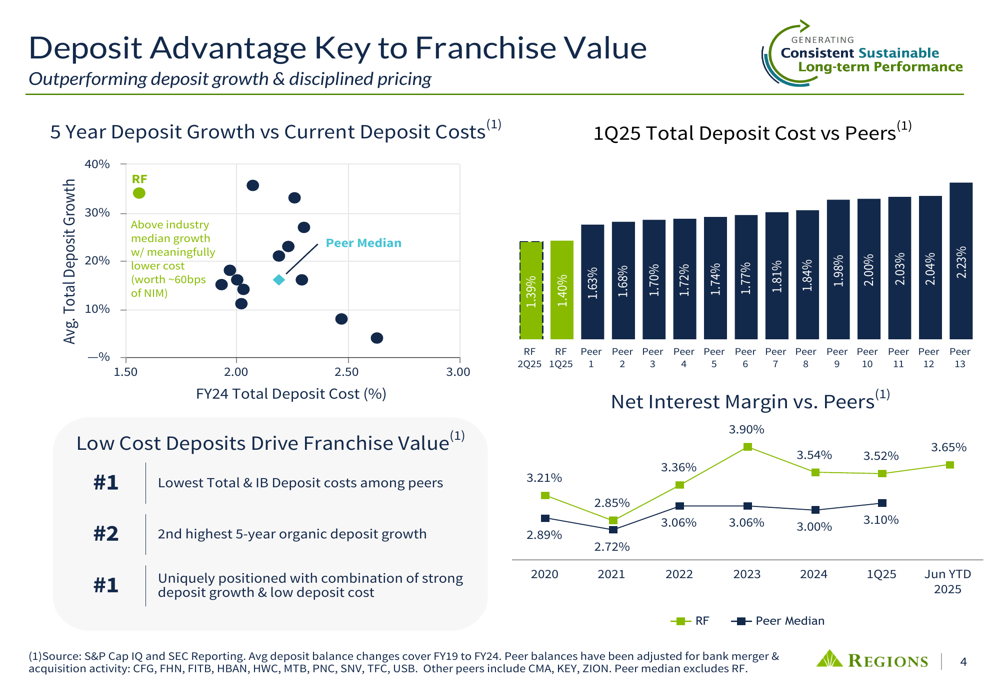

Deposit performance remained a key competitive advantage for Regions, with average deposits increasing over 1% quarter-over-quarter. The bank maintained significantly lower deposit costs compared to peers, with a total deposit cost of 1.39% versus the peer median of approximately 2.35%. This cost advantage, combined with strong deposit growth, creates substantial franchise value.

The company’s deposit advantage is clearly illustrated in this comparative analysis:

Non-interest income increased 5% on an adjusted basis and 9% on a reported basis, reaching $646 million. Wealth management income grew 3% quarter-over-quarter, marking another record quarter, while card and ATM fees increased 7%, benefiting from seasonally higher transaction volume. Mortgage income jumped 20%, primarily driven by a $13 million favorable MSR valuation adjustment, and capital markets income increased 5%.

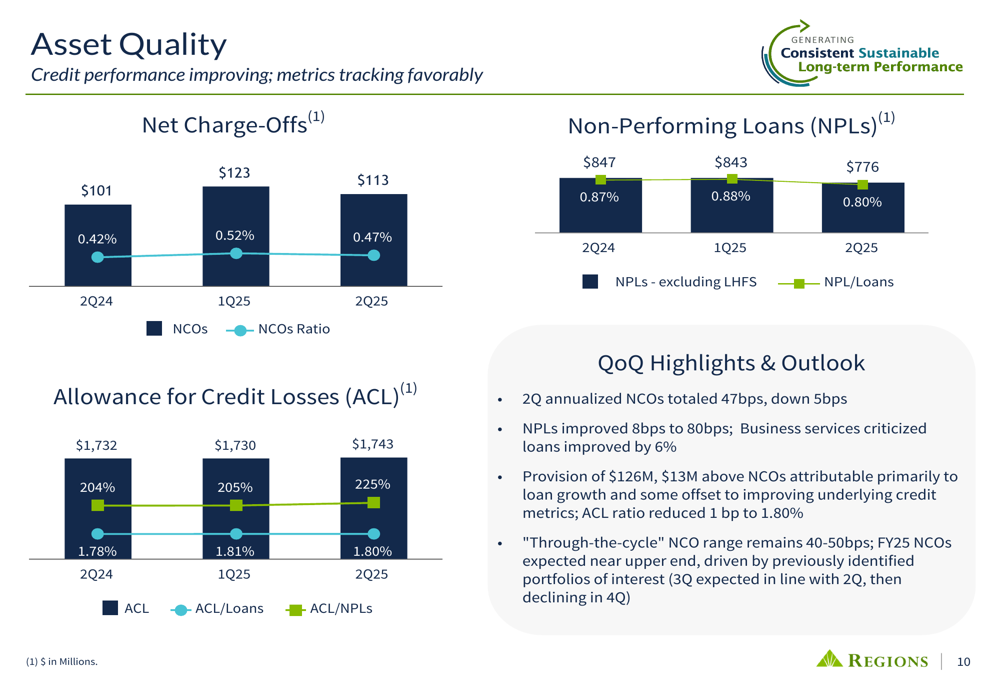

Asset quality metrics showed improvement, with net charge-offs decreasing to 0.47% of average loans from 0.52% in the previous quarter. Non-performing loans improved 8 basis points to 0.80%, and business services criticized loans improved by 6%. The company’s allowance for credit losses remained strong at 1.80% of loans, providing 225% coverage of non-performing loans.

The following chart demonstrates the improving asset quality trends:

Strategic Initiatives

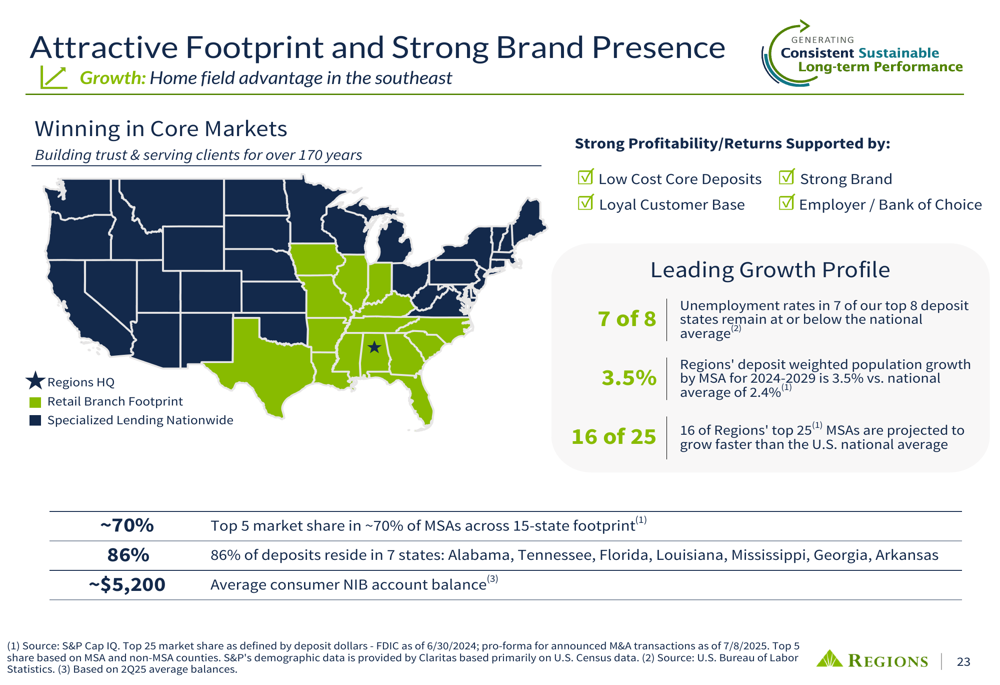

Regions continues to leverage its strong footprint in the Southeast, a region experiencing above-average population and economic growth. The company maintains top 5 market share in approximately 70% of MSAs across its 15-state footprint, with 86% of deposits residing in seven core states: Alabama, Tennessee, Florida, Louisiana, Mississippi, Georgia, and Arkansas.

The company’s geographic advantage is highlighted in this regional overview:

Regions is strategically investing in talent and technology to capitalize on growth opportunities. The bank is on track with hiring incremental bankers and related revenue enablement roles, focusing on expanding in markets with the greatest opportunity. Treasury Management revenue is up 8% year-to-date, and Wealth Management has achieved a compound annual growth rate of 8.3% over the past six years.

The company is also preparing for the implementation of Basel III Endgame regulations, managing its CET1 ratio inclusive of AOCI closer to the lower end of its 9.25%-9.75% operating range. Regions has taken steps to reduce volatility, including reclassifying available-for-sale securities into held-to-maturity and implementing derivative hedging strategies.

Forward-Looking Statements

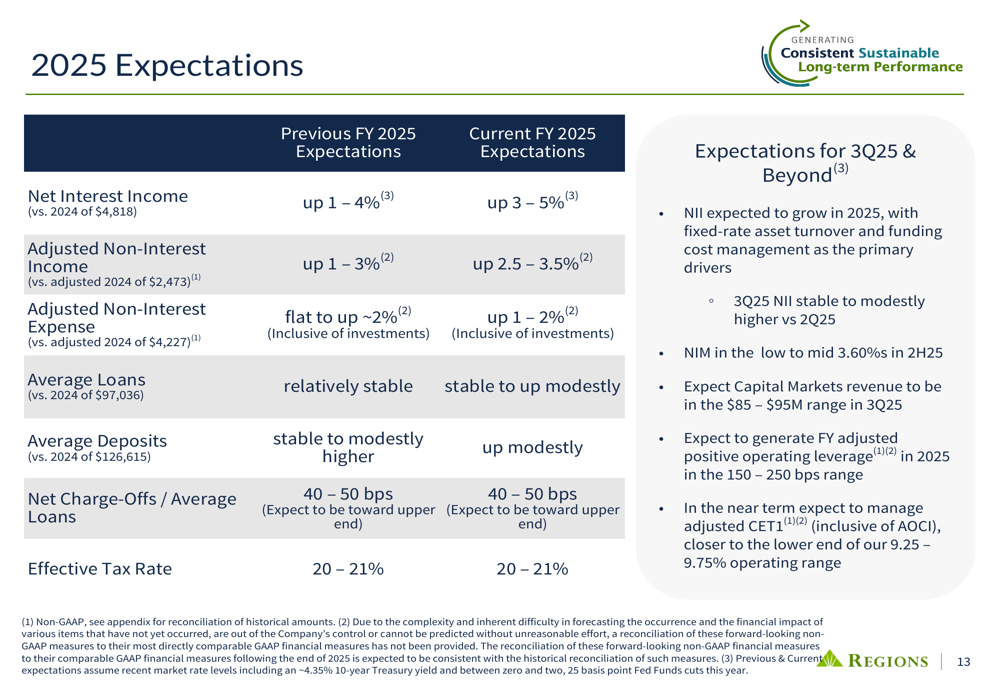

Based on strong second-quarter performance, Regions has raised its full-year 2025 guidance. The company now expects net interest income to grow between 3-5% (up from previous guidance of 1-4%) and adjusted non-interest income to increase 2.5-3.5% (up from 1-3%). Adjusted non-interest expense is projected to rise 1-2%, enabling the company to generate full-year adjusted positive operating leverage in the 150-250 basis point range.

For the third quarter of 2025, Regions expects net interest income to be stable to modestly higher compared to the second quarter, with capital markets revenue projected in the $85-95 million range.

The company’s updated 2025 expectations are summarized in this guidance table:

Regions Financial’s stock closed at $24.51 on July 17, 2025, and was trading slightly higher at $24.52 in pre-market trading following the earnings release. The stock remains within its 52-week range of $17.74 to $27.96, suggesting potential upside as the company continues to execute on its strategic priorities and deliver consistent financial performance.

The bank’s focus on sound risk management, profitability through diversified revenue streams and disciplined expense management, and strategic growth investments positions it well to continue generating value for shareholders in the coming quarters, despite ongoing economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.