Street Calls of the Week

Introduction & Market Context

RE/MAX Holdings, Inc. (NYSE:RMAX) presented its second quarter 2025 earnings results on July 30, revealing a company navigating challenging domestic real estate conditions while finding growth internationally. The stock has risen 4.03% to $8.52 following the presentation, suggesting investors responded positively to the company’s ability to maintain profitability despite revenue challenges.

The real estate franchisor, which operates both the RE/MAX and Motto Mortgage brands, continues to face headwinds in the U.S. and Canadian markets while achieving significant growth in international regions. This quarter’s results demonstrate the company’s focus on operational efficiency and margin improvement amid declining revenue.

Quarterly Performance Highlights

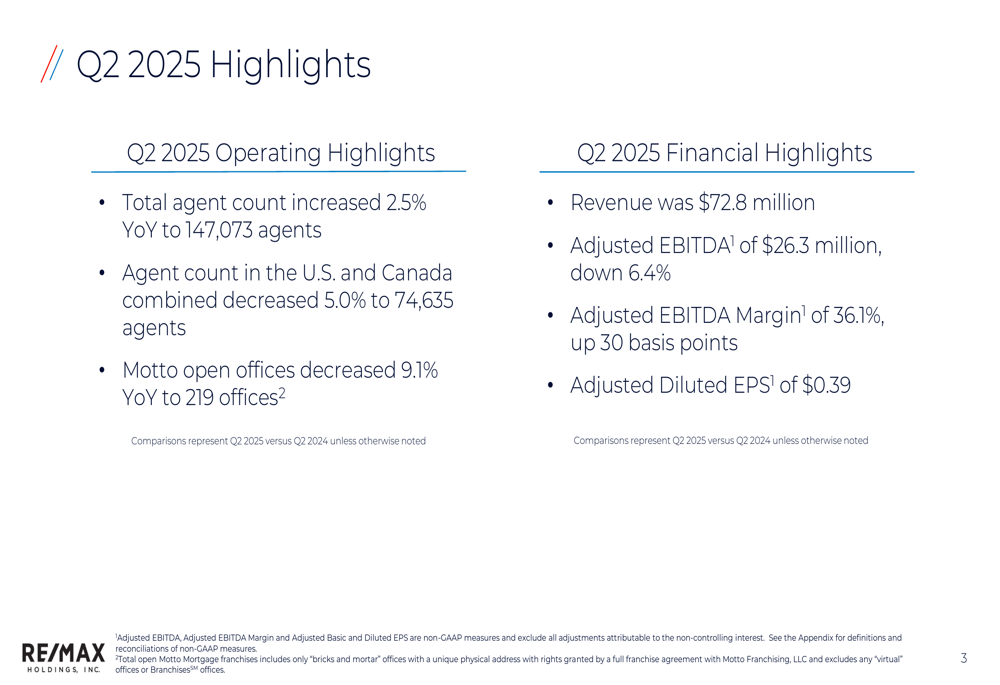

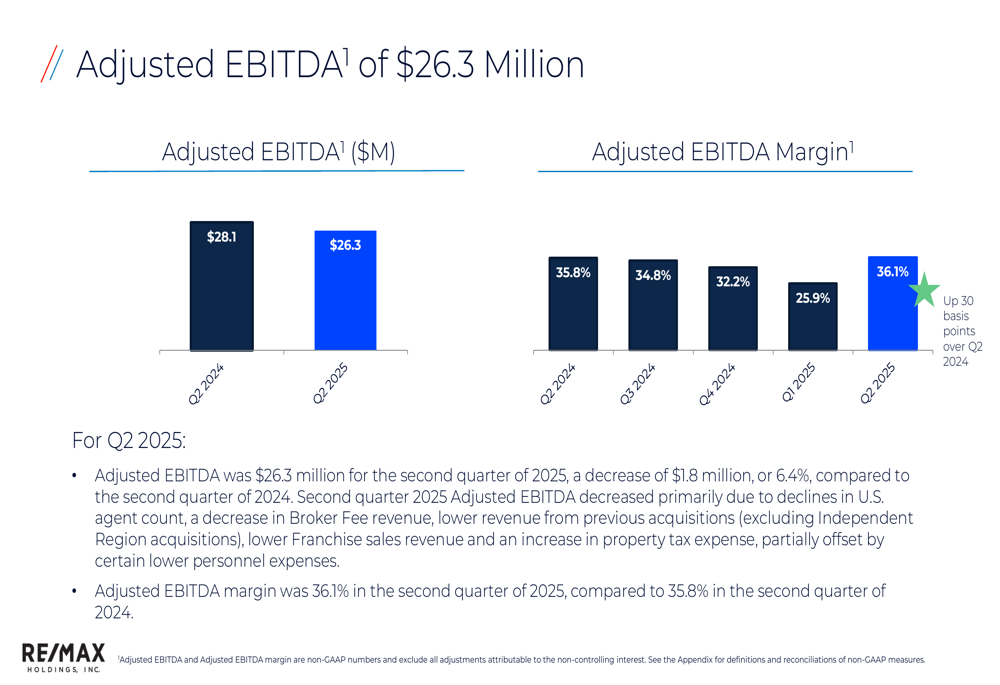

RE/MAX reported Q2 2025 revenue of $72.8 million, representing a 7.3% decrease compared to the same period last year. Despite this revenue decline, the company improved its adjusted EBITDA margin to 36.1%, up 30 basis points year-over-year, though adjusted EBITDA itself decreased 6.4% to $26.3 million.

The company’s adjusted diluted earnings per share came in at $0.39, exceeding the first quarter’s performance of $0.24, which had already surpassed analyst expectations at that time.

As shown in the following summary of key performance metrics:

The company’s ability to exceed the previously guided adjusted EBITDA range of $22.5-$25.5 million (as mentioned in their Q1 earnings) demonstrates effective cost management despite revenue pressures.

Agent Count Trends

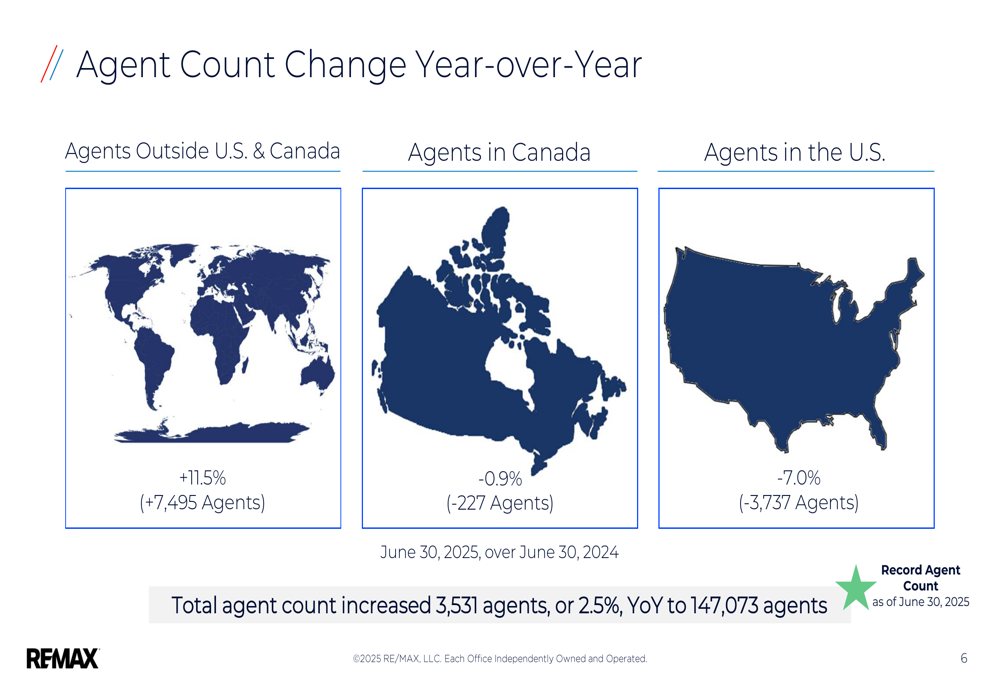

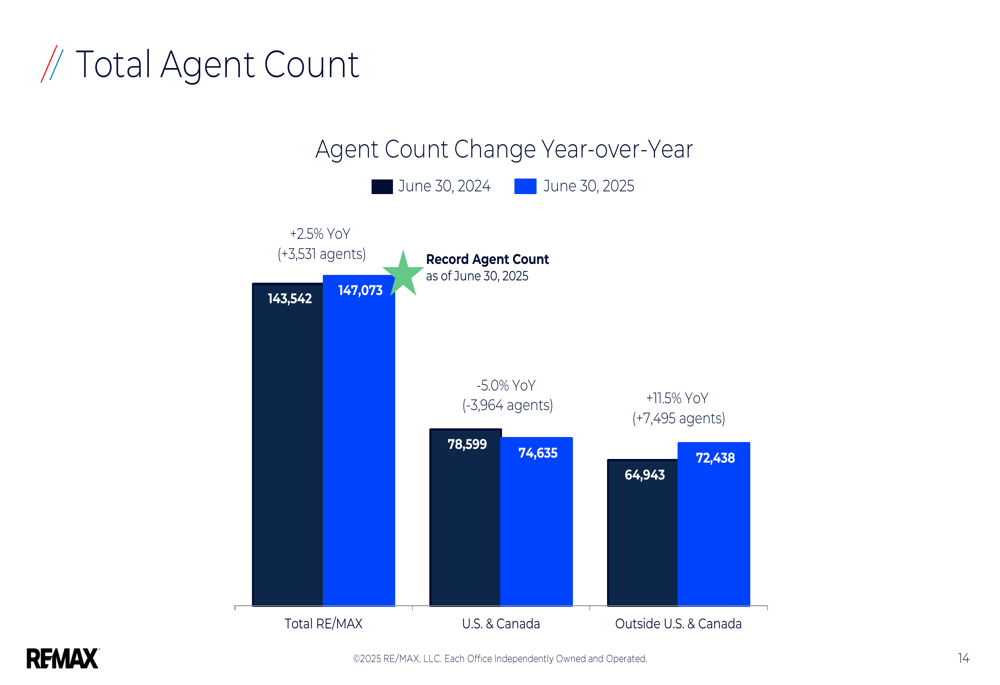

One of the most notable aspects of RE/MAX’s performance is the diverging trend between domestic and international agent counts. While the total agent count increased by 2.5% year-over-year to a record 147,073 agents, this growth was entirely driven by international expansion.

The company experienced an 11.5% increase in agents outside the U.S. and Canada, adding 7,495 agents year-over-year. Meanwhile, the U.S. agent count decreased by 7.0% (-3,737 agents) and Canadian agent count declined by 0.9% (-227 agents).

This regional disparity is clearly illustrated in the following breakdown:

The visualization of total agent count further highlights this divergence between domestic and international markets:

To address the domestic agent count challenges, RE/MAX has implemented its "Aspire" program, a comprehensive onboarding system designed to improve new agent productivity through education, marketing, technology, and a variable fee structure during the first twelve months.

Financial Analysis

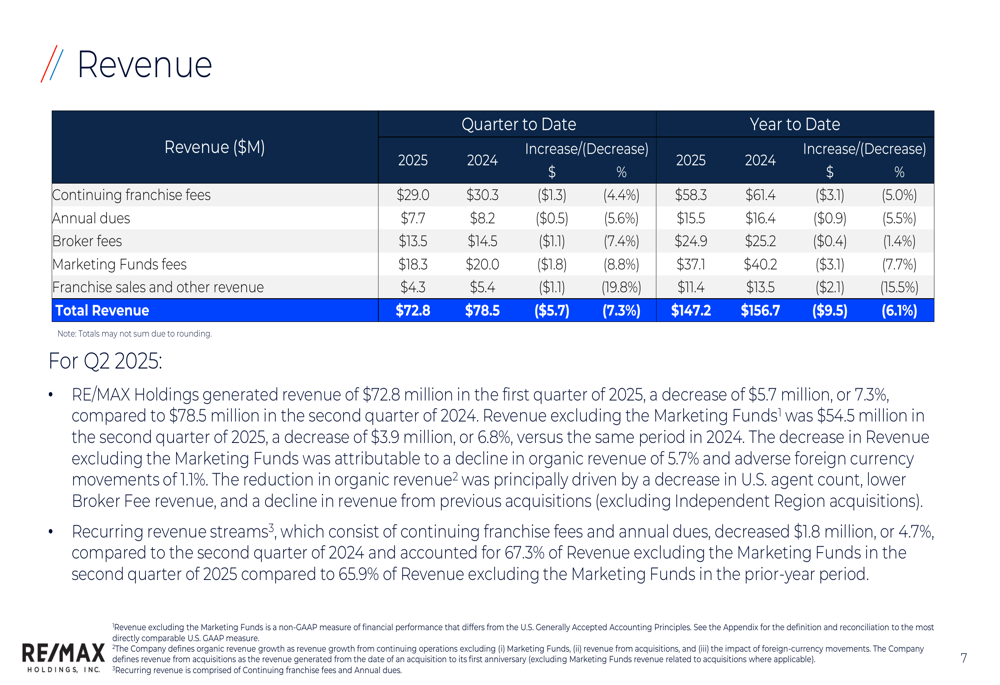

RE/MAX’s revenue decline of 7.3% affected all major revenue categories. Continuing franchise fees decreased 4.4% to $29.0 million, annual dues fell 5.6% to $7.7 million, and broker fees declined 7.4% to $13.5 million. Marketing funds fees saw the largest percentage drop at 8.8% to $18.3 million.

The following chart details the revenue breakdown:

Despite these revenue challenges, RE/MAX demonstrated strong cost control, reducing selling, operating and administrative expenses by 2.8% year-over-year to $33.9 million. Personnel costs decreased by 3.3%, and "other" expenses fell by 11.4%, though professional fees increased by 22.9%.

The company’s adjusted EBITDA and margin trends show resilience in the face of revenue pressures:

From a balance sheet perspective, RE/MAX reported a cash balance of $94.3 million as of June 30, 2025, with $439.0 million in outstanding debt. This results in a Total (EPA:TTEF) Debt to TTM Adjusted EBITDA ratio of 4.6:1 and a Net Debt to TTM Adjusted EBITDA ratio of 3.6:1. The company maintains a stock repurchase program with $62.5 million remaining available as of quarter-end.

Outlook & Guidance

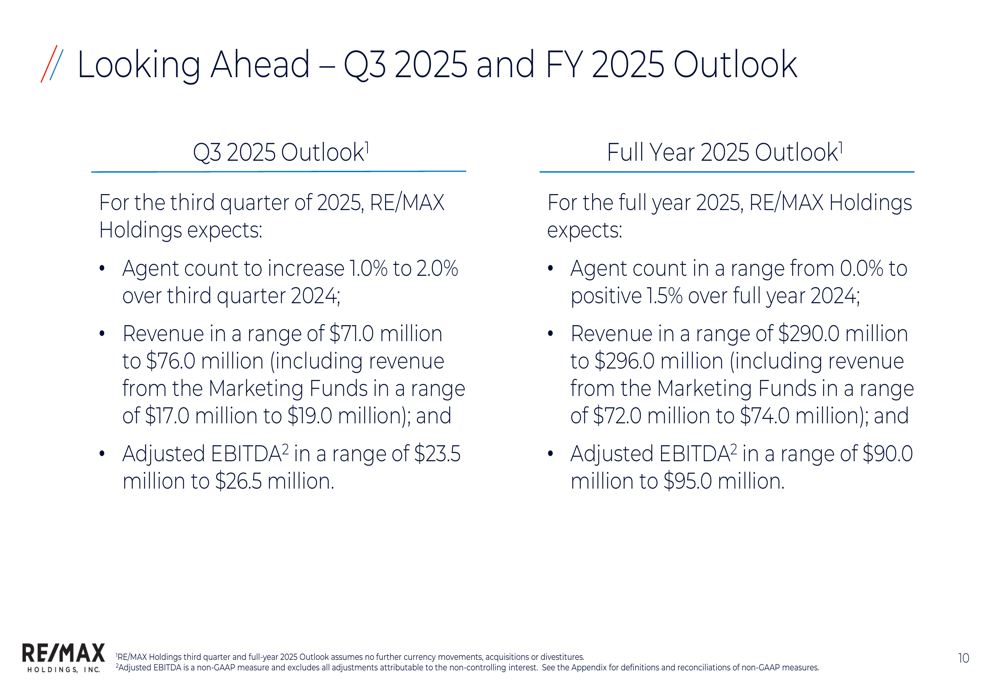

Looking ahead, RE/MAX provided guidance for both Q3 2025 and the full year. For the third quarter, the company expects agent count to increase 1.0% to 2.0% year-over-year, with revenue projected between $71.0 million and $76.0 million. Adjusted EBITDA is forecast between $23.5 million and $26.5 million.

For the full year 2025, RE/MAX anticipates agent count growth between 0.0% and 1.5%, with revenue between $290.0 million and $296.0 million and adjusted EBITDA between $90.0 million and $95.0 million.

The company’s detailed outlook is presented here:

These projections suggest that RE/MAX expects the current trends to continue, with international growth offsetting domestic challenges while maintaining profitability through operational efficiency.

Competitive Positioning

RE/MAX continues to emphasize its competitive advantages in the marketplace, highlighting that its agents average double the sales of other agents in the RealTrends Verified rankings of large brokerages. The company also points to its recognition as the most trusted real estate agency in the USA and Canada according to BrandSpark studies.

The company positions itself as a dual-brand franchisor with compelling growth opportunities through both its real estate and mortgage businesses. However, the 9.1% year-over-year decrease in Motto open offices to 219 indicates challenges in the mortgage segment amid a difficult interest rate environment.

As the real estate market navigates through current challenges, RE/MAX appears focused on leveraging its strong brand, improving agent productivity, and expanding internationally while maintaining disciplined cost management to preserve profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.