Functional Brands closes $8 million private placement and completes Nasdaq listing

Introduction & Market Context

Repsol SA (BME:REP) presented its third-quarter 2025 results on October 30, highlighting substantial year-over-year growth across all business segments despite missing earnings per share forecasts. The Spanish energy company’s stock dipped 0.72% to €15.75 following the announcement, reflecting investor reaction to the 7.44% negative surprise on EPS, which came in at €0.5835 against expectations of €0.6304.

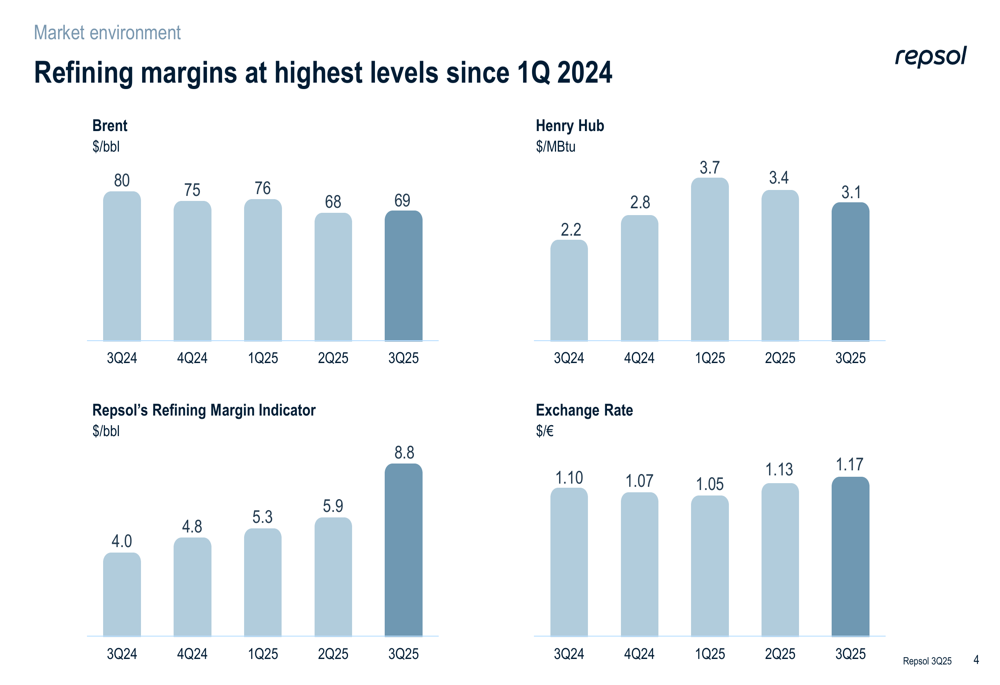

The company operated in a market environment characterized by relatively stable Brent crude prices at $69/bbl (compared to $68/bbl in Q2 2025) and slightly declining Henry Hub natural gas prices at $3.1/MBtu (versus $3.4/MBtu in Q2 2025). Most notably, refining margins significantly improved to $8.8/bbl in Q3 2025, reaching their highest levels since Q1 2024 and substantially outperforming the $5.9/bbl recorded in the previous quarter.

As shown in the following market environment chart:

Quarterly Performance Highlights

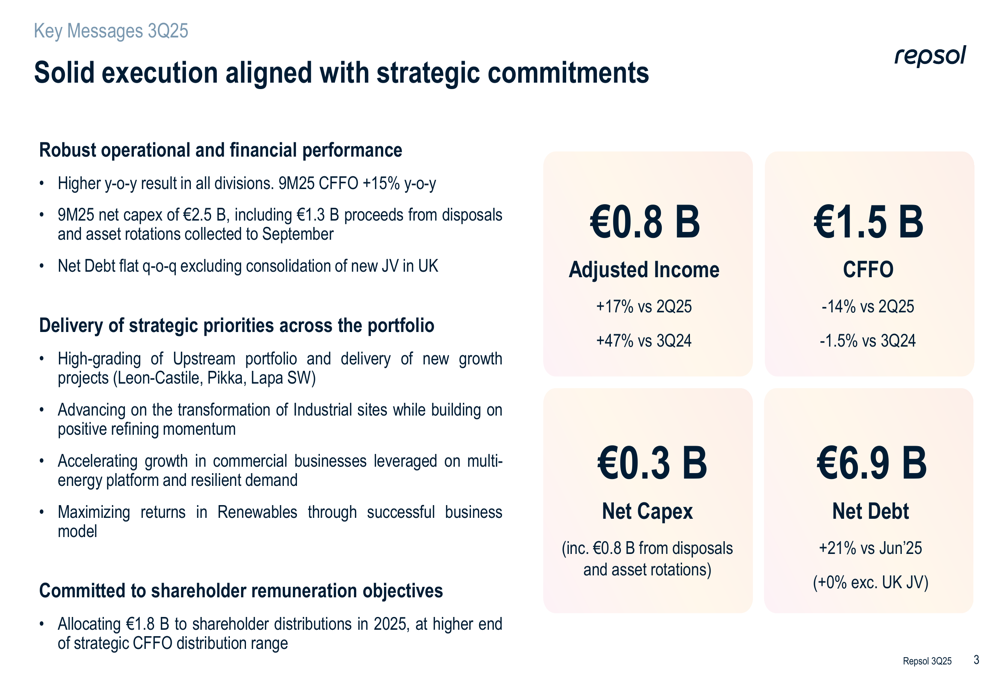

Repsol reported adjusted income of €820 million for Q3 2025, representing a 17% increase from Q2 2025 and an impressive 47% rise compared to Q3 2024. Cash flow from operations (CFFO) reached €1.5 billion for the quarter, though this marked a 14% decrease from Q2 2025 and a slight 1.5% decline year-over-year. For the first nine months of 2025, CFFO totaled €4.3 billion, up 15% from the same period in 2024.

The key messages from Repsol’s presentation emphasize solid execution aligned with strategic commitments:

All business segments demonstrated strong year-over-year growth in adjusted income:

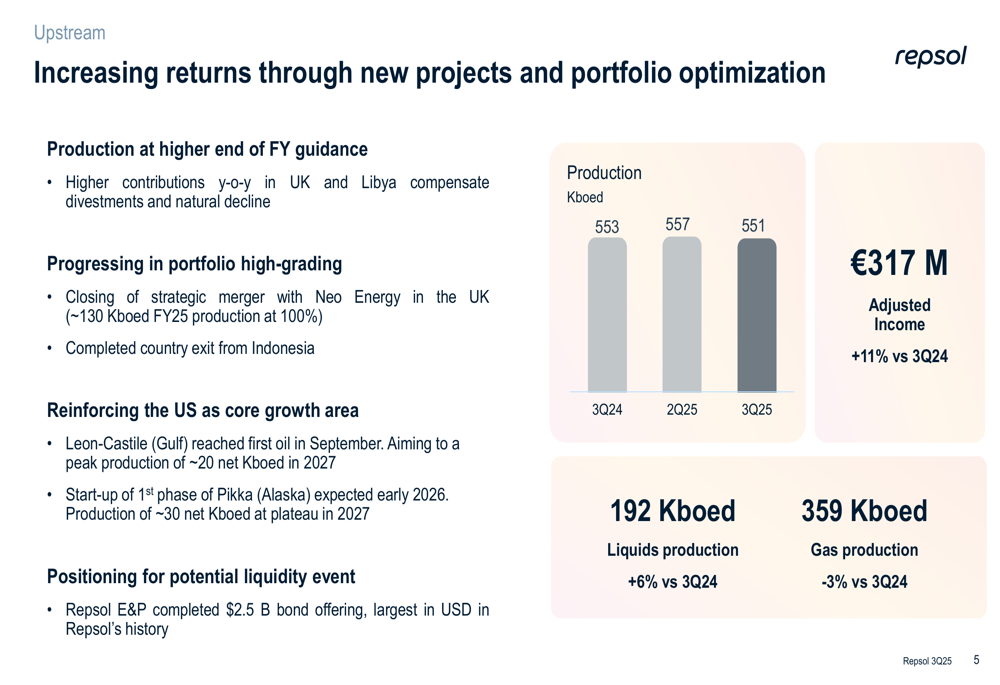

1. Upstream: €317 million (+11% vs Q3 2024)

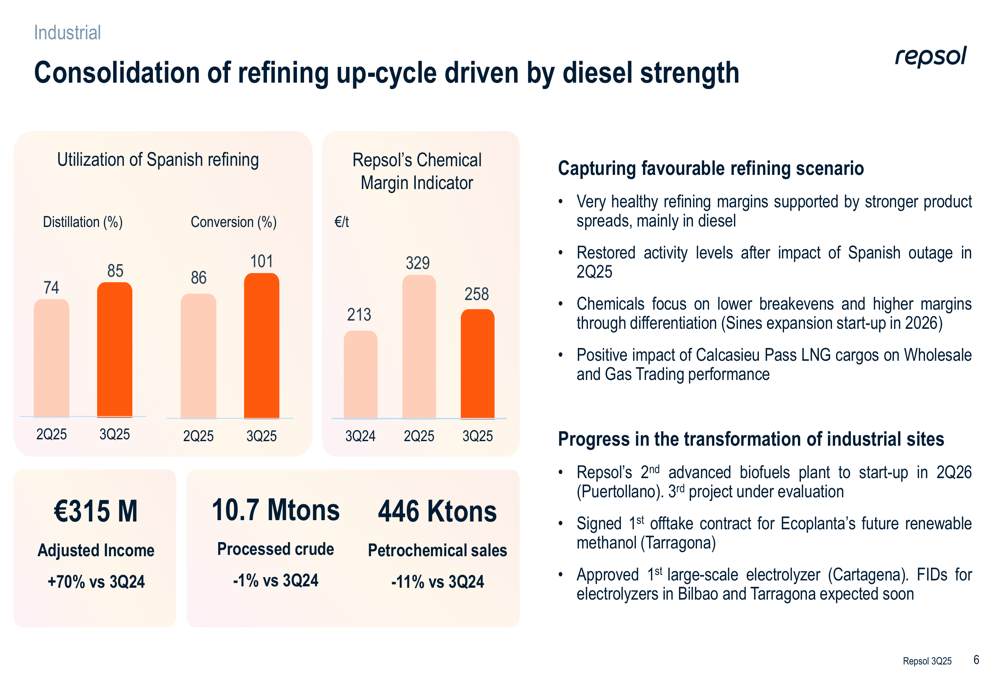

2. Industrial: €315 million (+70% vs Q3 2024)

3. Customer: €241 million (+34% vs Q3 2024)

4. Low Carbon Generation: €31 million (up €38 million vs Q3 2024)

Net debt increased to €6.9 billion, up 21% from June 2025, though the company noted this was flat excluding the impact of the UK joint venture with NEO Energy.

Detailed Financial Analysis

Upstream Performance

Repsol’s Upstream segment maintained strong production at 551 thousand barrels of oil equivalent per day (Kboed), positioning at the higher end of full-year guidance. The company is progressing with portfolio optimization while reinforcing the US as a core growth area.

The following chart illustrates Upstream performance metrics:

Industrial Performance

The Industrial segment demonstrated remarkable growth, with adjusted income reaching €315 million, a 70% increase compared to Q3 2024. This performance was primarily driven by the consolidation of the refining up-cycle, particularly strength in diesel markets. Conversion utilization reached 101% in Q3 2025, though distillation utilization decreased to 74% from 85% in the previous quarter.

The following chart details Industrial segment metrics:

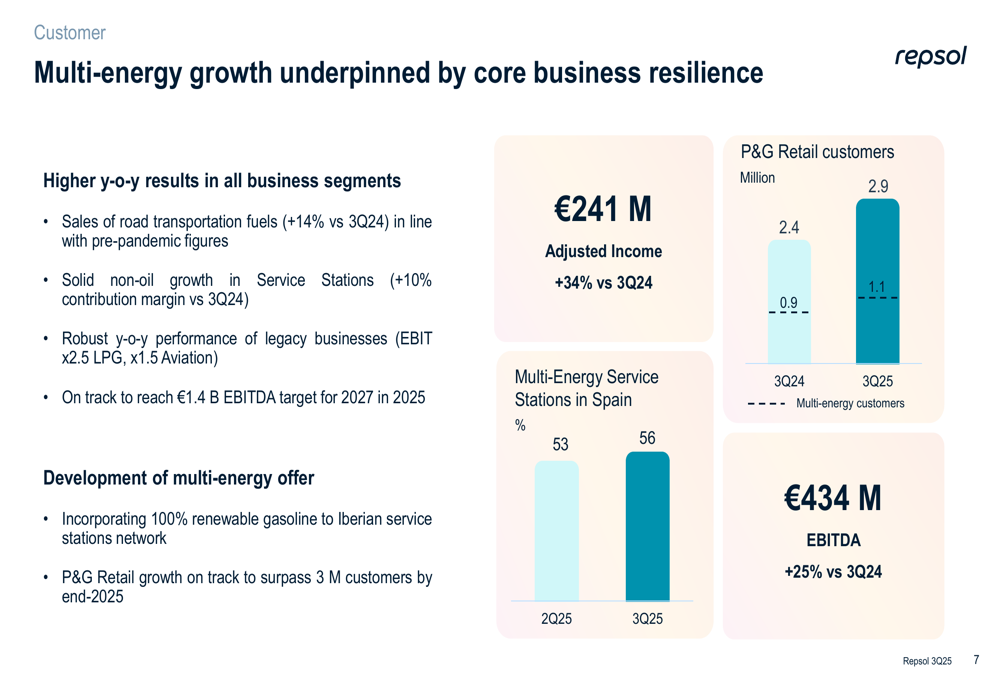

Customer Performance

The Customer segment continued its strong trajectory with adjusted income of €241 million, up 34% year-over-year, and EBITDA of €434 million, a 25% increase from Q3 2024. Power and gas retail customers grew to 2.9 million, up from 2.4 million in Q3 2024, while multi-energy service stations in Spain increased to 56% of the network.

The following chart shows Customer segment performance:

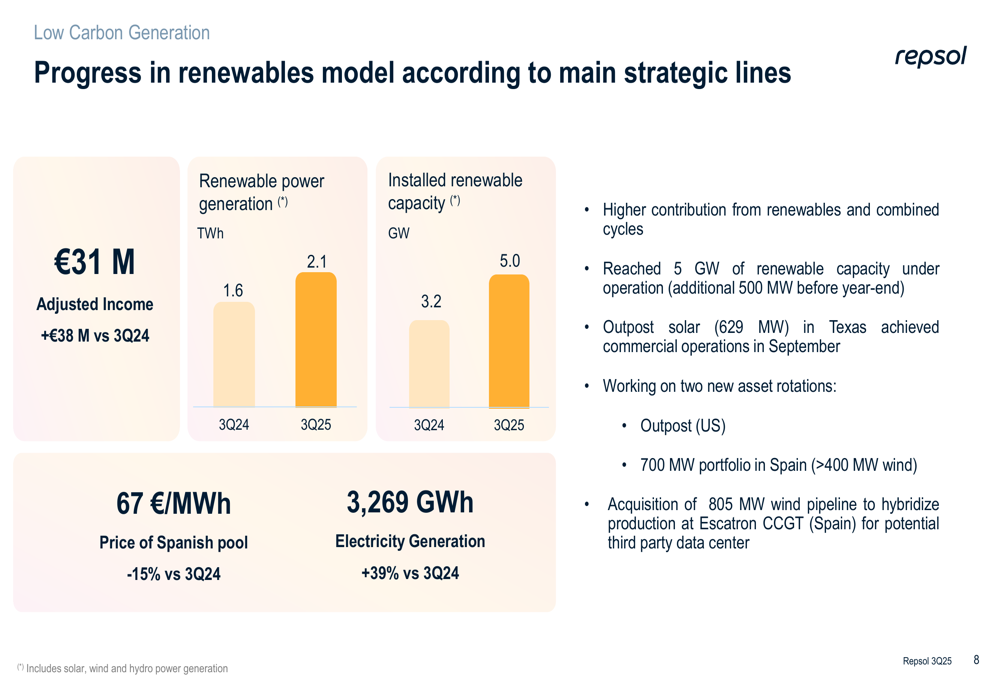

Low Carbon Generation Performance

Repsol’s strategic focus on renewable energy showed significant progress, with installed renewable capacity reaching 5.0 GW, up from 3.2 GW in Q3 2024. Renewable power generation increased to 2.1 TWh from 1.6 TWh in the same period last year. Adjusted income for the segment was €31 million, a €38 million improvement from Q3 2024.

The following chart illustrates Low Carbon Generation metrics:

Strategic Initiatives

Repsol continues to execute on key strategic initiatives across all business segments. In Upstream, the company is progressing with portfolio high-grading and positioning for a potential liquidity event, while reinforcing the US as a core growth area. The Industrial segment is advancing in the transformation of industrial sites, while the Customer business is developing its multi-energy offering.

In the Low Carbon Generation segment, Repsol has reached 5 GW of renewable capacity and is working on two new asset rotations to optimize its portfolio. The company remains committed to shareholder remuneration, allocating €1.8 billion to distributions, including a dividend of €0.975 per share (an 8.3% increase versus 2024) and a €700 million share buyback program.

Forward-Looking Statements

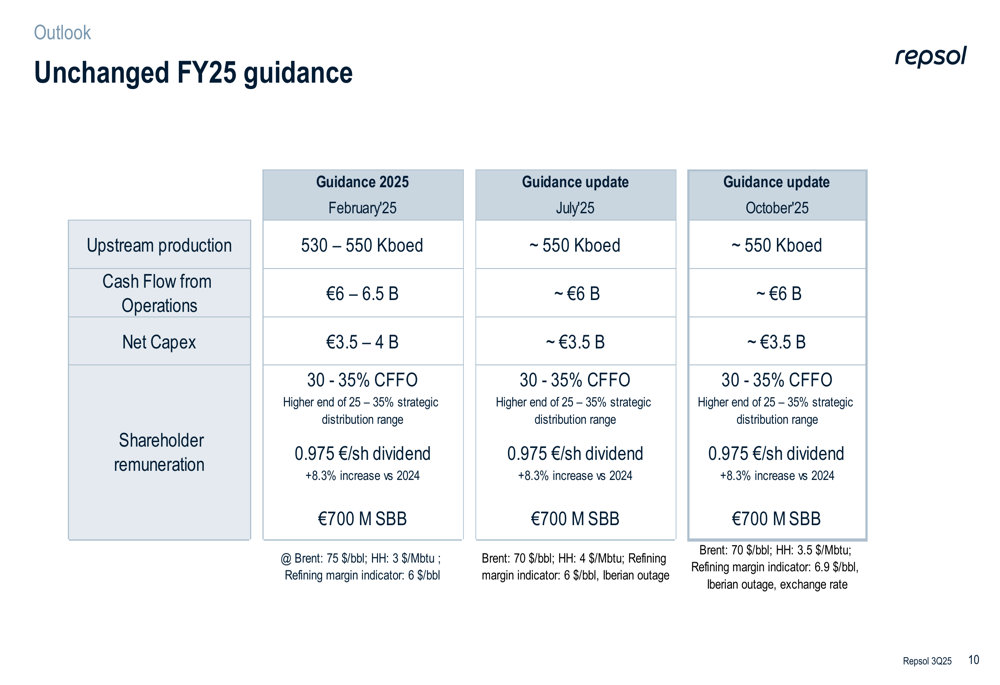

Repsol maintained its full-year 2025 guidance unchanged from previous communications, projecting:

The company expects production to reach approximately 550 Kboed, at the upper end of its original guidance range. Cash flow from operations is projected at approximately €6 billion, while net capital expenditure is expected to be around €3.5 billion, at the lower end of the original guidance range.

CEO Josu Jon Imaz emphasized during the earnings call that "Repsol is delivering on its commitments," highlighting the company’s strategic progress. He also noted preparation for a "liquidity event in 2026" and the significant contribution of the customer business to cash dividends.

Despite the positive outlook, investors should note the increasing net debt, which rose by €1.2 billion since June, and the integration challenges following the merger with NEO Energy. The company’s performance will continue to be influenced by volatile oil and gas prices, with diesel supply deficits currently supporting strong refining margins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.