Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

REV Group Inc. (NYSE:REVG) released its fiscal second quarter 2025 results on June 4, 2025, showcasing strong performance driven primarily by its Specialty Vehicles segment. The company, which manufactures specialty vehicles including fire trucks, ambulances, and recreational vehicles, reported significant year-over-year growth in adjusted EBITDA despite modest revenue increases. REV Group’s stock has performed well in 2025, with shares trading at $37.22 as of the previous close, representing a 1.89% gain and approaching its 52-week high of $38.78.

Quarterly Performance Highlights

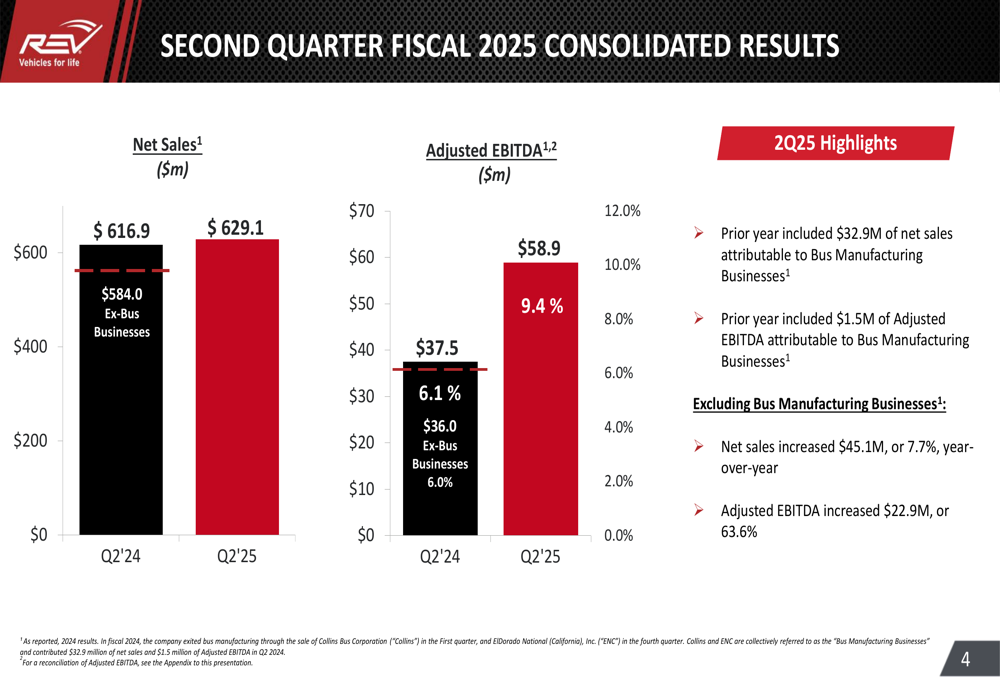

REV Group reported Q2 2025 net sales of $629.1 million, compared to $616.9 million in Q2 2024. However, when excluding the divested Bus Manufacturing Businesses, which contributed $32.9 million to the prior year’s results, organic net sales increased by $45.1 million or 7.7% year-over-year. More impressively, adjusted EBITDA jumped to $58.9 million, a substantial increase from $37.5 million in the same period last year, representing a 63.6% improvement excluding the divested bus operations.

As shown in the following chart of consolidated quarterly results:

Segment Analysis

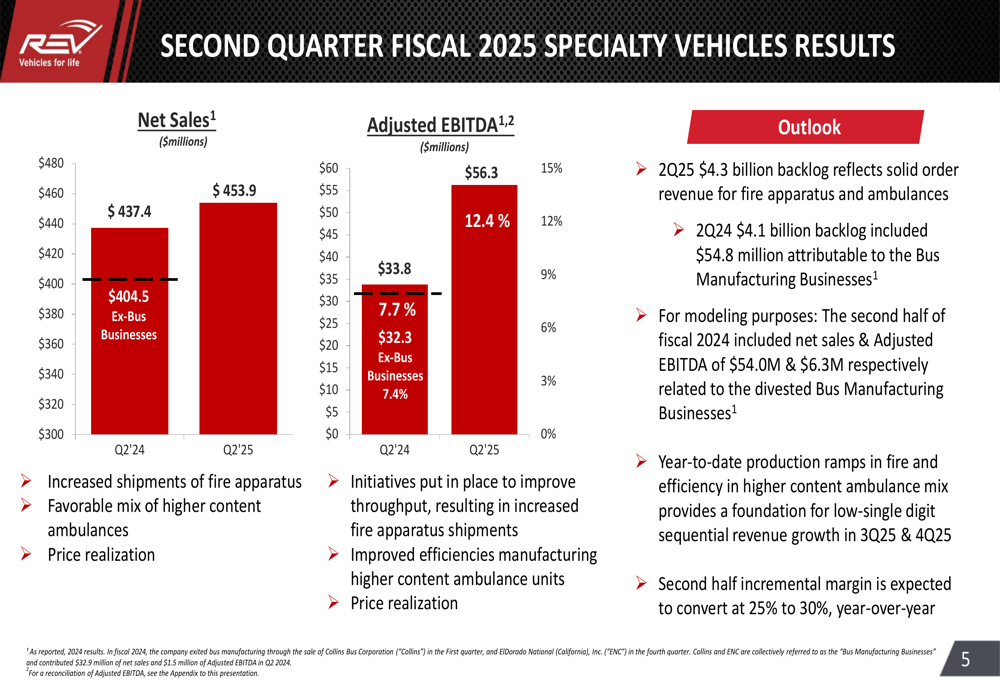

The Specialty Vehicles segment, which includes fire apparatus and ambulances, was the primary driver of REV Group’s strong performance. This segment reported net sales of $453.9 million, up from $404.5 million in the prior year (excluding bus businesses). Adjusted EBITDA for the segment reached $56.3 million, a dramatic improvement from $32.3 million in Q2 2024.

Key drivers for the Specialty Vehicles segment included increased shipments of fire apparatus, favorable mix of higher content ambulances, and effective price realization. The company highlighted initiatives to improve throughput and manufacturing efficiencies. The segment maintained a robust backlog of $4.3 billion, reflecting solid order revenue for fire apparatus and ambulances.

The following chart illustrates the Specialty Vehicles segment’s strong performance:

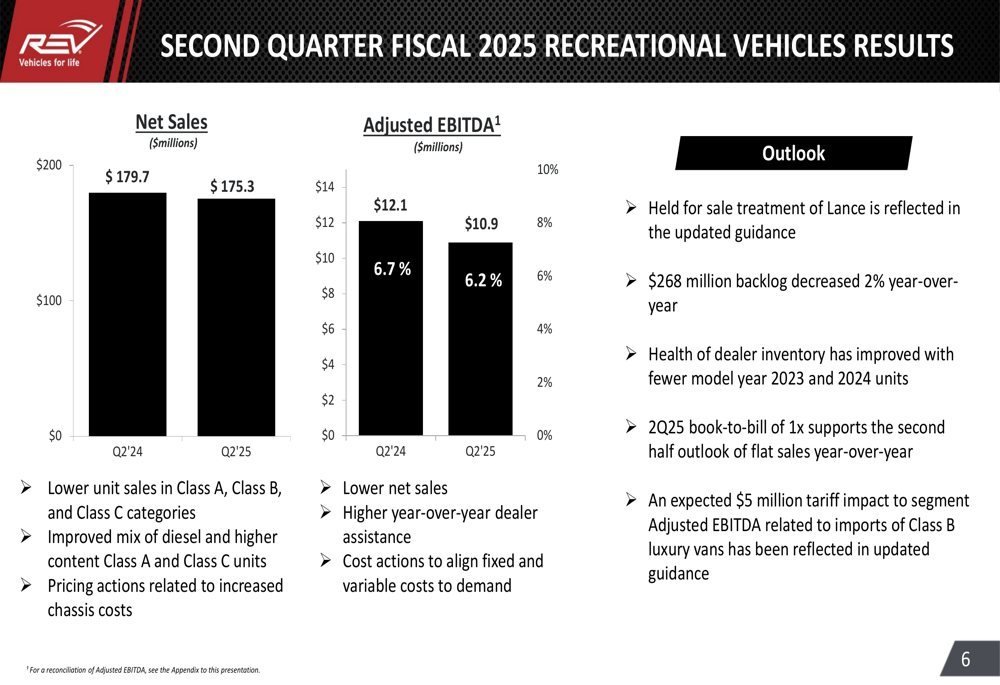

In contrast, the Recreational Vehicles segment faced challenges with net sales declining to $175.3 million from $179.7 million in Q2 2024. Adjusted EBITDA for this segment decreased to $10.9 million (6.2% margin) from $12.1 million (6.7% margin) in the prior year. The decline was attributed to lower unit sales across Class A, B, and C categories, partially offset by improved mix of diesel and higher content units.

The RV segment’s performance is detailed in this chart:

Management noted that dealer inventory health has improved with fewer older model year units, and the segment achieved a book-to-bill ratio of 1x, supporting expectations of flat sales year-over-year in the second half of fiscal 2025. However, the company expects a $5 million tariff impact to segment Adjusted EBITDA related to imports of Class B luxury vans.

Strategic Initiatives

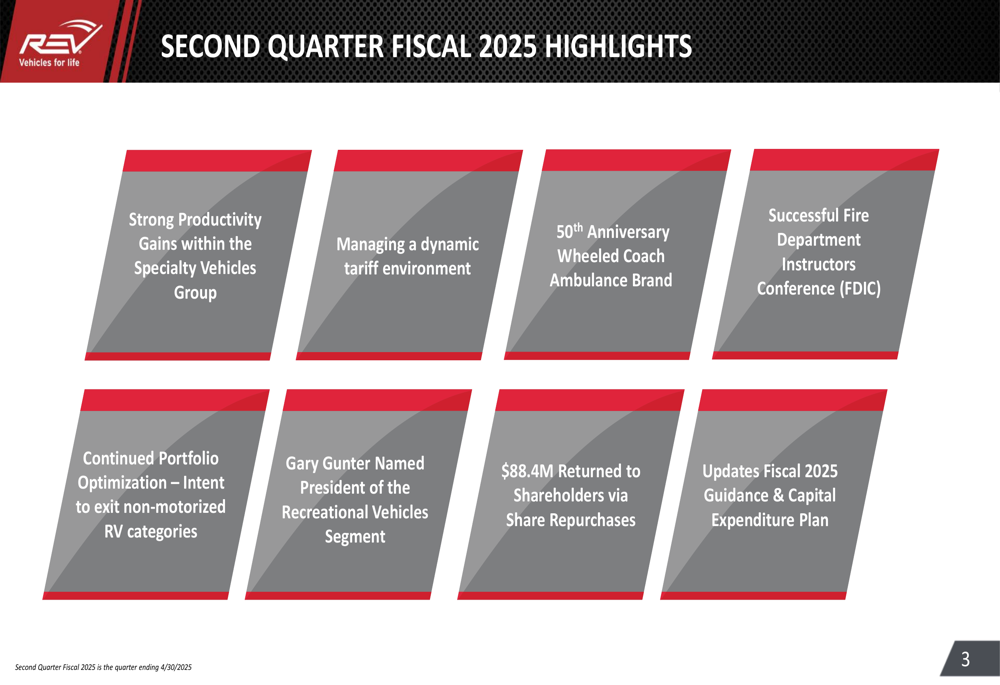

REV Group continues to optimize its portfolio, announcing its intent to exit non-motorized RV categories. This follows the company’s previous divestiture of its bus manufacturing businesses in fiscal 2024. The company also appointed Gary Gunter as President of the Recreational Vehicles Segment, signaling a focus on leadership to navigate challenges in that market.

The company highlighted several operational achievements during the quarter, including:

- Strong productivity gains within the Specialty Vehicles Group

- Celebration of the 50th Anniversary of Wheeled Coach (NYSE:TPR) Ambulance Brand

- Successful participation in the Fire Department Instructors Conference (FDIC)

- Initiatives to improve manufacturing throughput and efficiency

These key highlights from the quarter are summarized in the following slide:

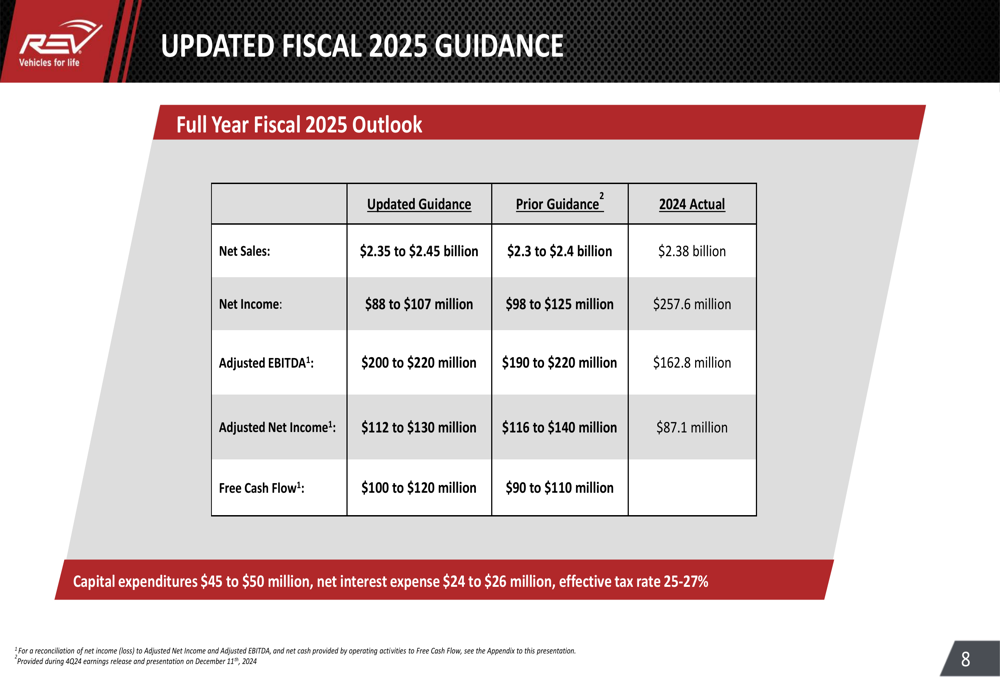

Updated Guidance

REV Group raised its fiscal 2025 guidance for net sales and free cash flow while maintaining its adjusted EBITDA range. The company now expects:

- Net Sales of $2.35 to $2.45 billion (up from $2.3 to $2.4 billion previously)

- Adjusted EBITDA of $200 to $220 million (narrowed from $190 to $220 million)

- Free Cash Flow of $100 to $120 million (increased from $90 to $110 million)

However, the company reduced its net income guidance to $88 to $107 million from the previous range of $98 to $125 million, likely reflecting the impact of tariffs and challenges in the RV segment.

The complete updated guidance is presented in this comprehensive table:

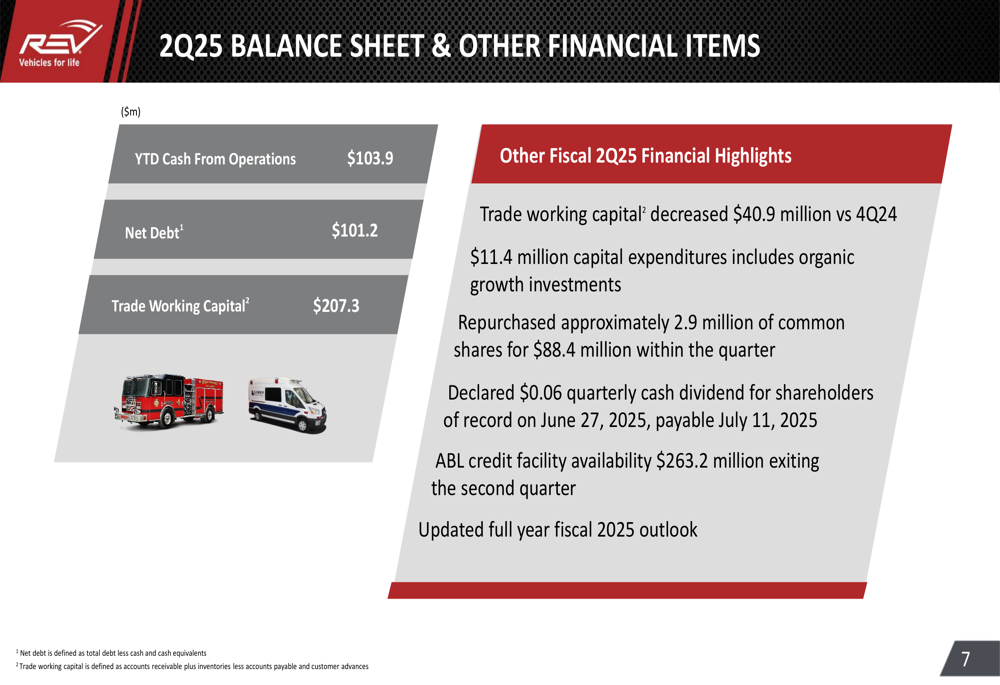

Financial Position

REV Group demonstrated strong financial discipline with year-to-date cash from operations of $103.9 million. The company reduced its net debt to $101.2 million and decreased trade working capital by $40.9 million compared to Q4 2024. Capital expenditures totaled $11.4 million, including organic growth investments.

Notably, REV Group returned significant value to shareholders during the quarter, repurchasing approximately 2.9 million common shares for $88.4 million. The company also declared a quarterly cash dividend of $0.06 per share, payable on July 11, 2025, to shareholders of record as of June 27, 2025.

The company’s balance sheet strength and capital allocation priorities are illustrated in this slide:

REV Group maintained strong liquidity with $263.2 million in ABL credit facility availability at the end of the second quarter, positioning the company well for continued strategic investments and shareholder returns.

The company’s Q2 results build upon its strong Q1 performance, where it reported an EPS of 0.4, significantly exceeding the forecasted 0.28, and achieved revenue of $525.1 million. While facing some headwinds in the RV segment and navigating tariff challenges, REV Group’s operational improvements and focus on high-margin specialty vehicles continue to drive financial performance and shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.