Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

REV Group Inc (NYSE:REVG), a manufacturer of specialty vehicles including fire apparatus, ambulances, and recreational vehicles, reported strong third-quarter fiscal 2025 results on September 3, 2025, showcasing significant growth in both revenue and profitability. The company’s shares responded positively in premarket trading, rising 5.21% to $54.50, reflecting investor confidence in the company’s performance and raised outlook.

The results come amid a period of strategic focus on the company’s core specialty vehicle segments, including the completed sale of Lance Camper during the quarter and continued investment in production facilities. REV Group has maintained momentum in throughput increases year-over-year, driving improved financial performance despite some headwinds in the recreational vehicle segment.

Quarterly Performance Highlights

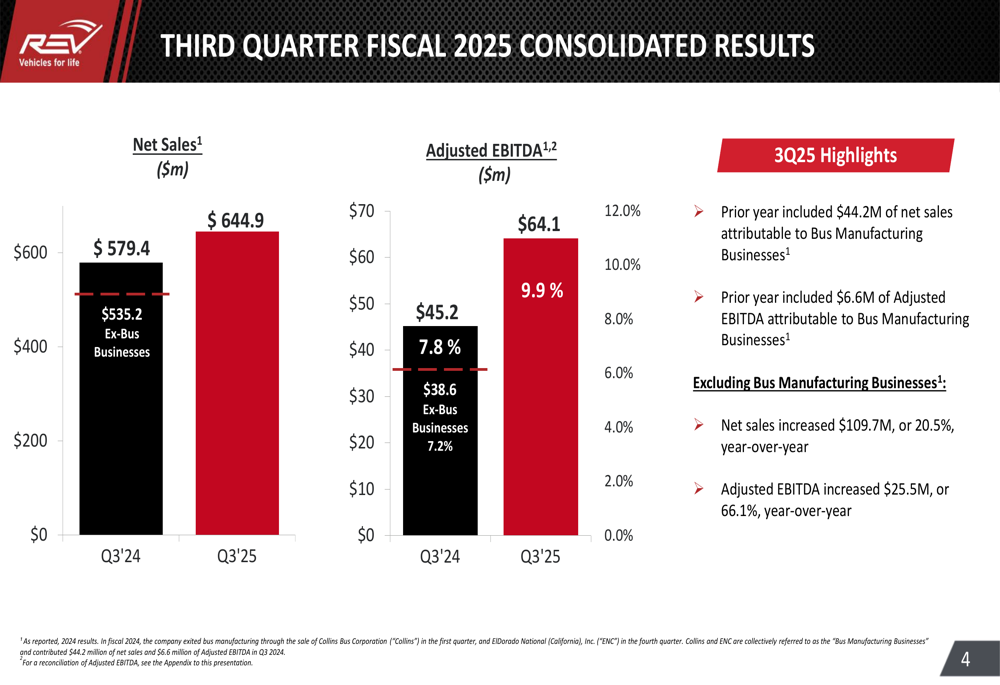

REV Group reported consolidated net sales of $644.9 million for the third quarter, representing a significant increase from $579.4 million in the same period last year. Adjusted EBITDA showed even stronger growth, reaching $64.1 million compared to $45.2 million in Q3 2024.

When excluding the divested Bus Manufacturing Businesses, the results are even more impressive, with net sales increasing by $109.7 million or 20.5% year-over-year, and adjusted EBITDA growing by $25.5 million or 66.1%.

As shown in the following consolidated results chart:

The company’s net income for the quarter reached $29.1 million, up from $18.0 million in the prior year period, demonstrating substantial bottom-line improvement. This performance builds on the momentum seen in the previous quarter, where REV Group had also exceeded analyst expectations with an EPS of $0.70 against a forecast of $0.55.

Segment Analysis

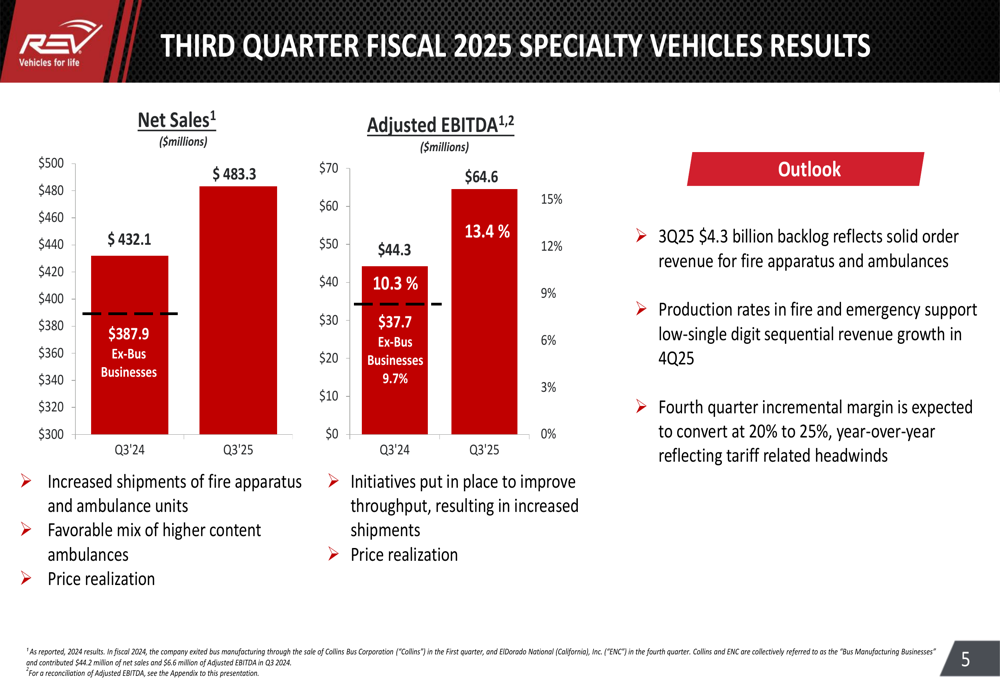

The Specialty Vehicles segment, which includes fire apparatus and ambulances, was the primary driver of growth for REV Group in the third quarter. The segment reported net sales of $483.3 million, up from $432.1 million in the prior year period, while adjusted EBITDA increased significantly to $64.6 million from $44.3 million. The adjusted EBITDA margin expanded by 310 basis points to 13.4%.

This impressive performance in the Specialty Vehicles segment is illustrated in the following chart:

The company attributed the strong performance to increased shipments of fire apparatus and ambulance units, a favorable mix of higher content ambulances, price realization, and initiatives to improve throughput. The segment maintains a robust backlog of $4.3 billion, providing visibility into future quarters.

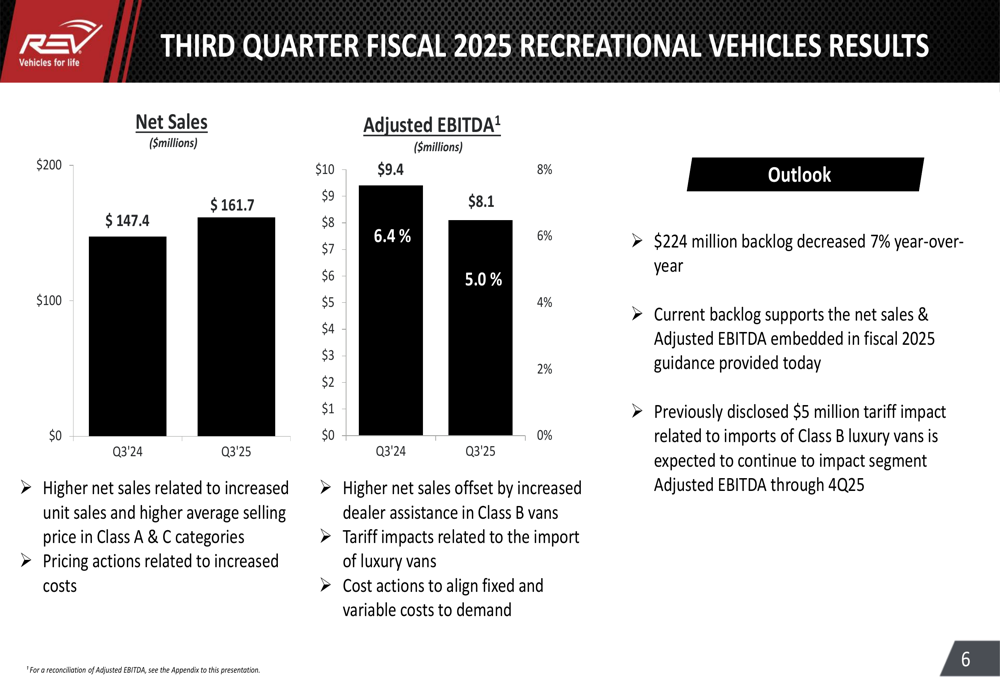

In contrast, the Recreational Vehicles segment showed mixed results. Net sales increased to $161.7 million from $147.4 million in the prior year period, but adjusted EBITDA declined to $8.1 million from $9.4 million, with margins contracting from 6.4% to 5.0%.

The following chart details the Recreational Vehicles segment performance:

The company cited increased dealer assistance, tariff impacts on luxury vans, and cost actions as factors affecting profitability in the RV segment. The previously disclosed $5 million tariff impact is expected to continue through Q4 2025. The segment’s backlog stands at $224 million, representing a 7% decrease year-over-year.

Balance Sheet and Cash Flow

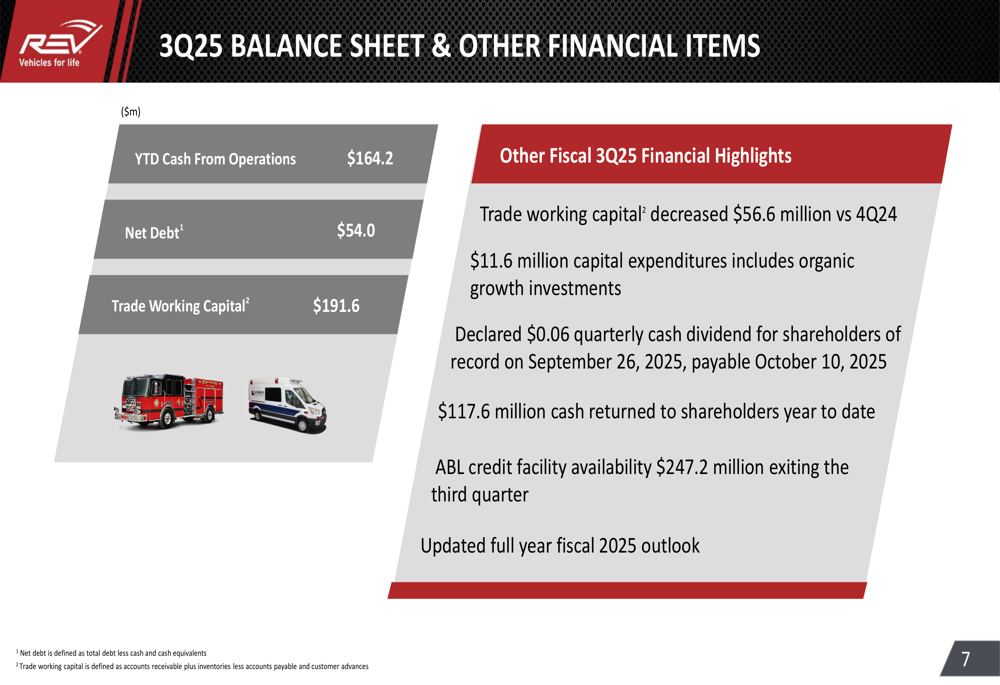

REV Group continued to demonstrate strong financial discipline, generating $164.2 million in cash from operations year-to-date. The company’s net debt position improved to $54.0 million, while trade working capital decreased by $56.6 million compared to Q4 2024, reaching $191.6 million.

The company’s balance sheet strength is illustrated in the following financial items summary:

Capital expenditures for the quarter totaled $11.6 million, including organic growth investments such as the groundbreaking for a $20 million investment in the Brandon, SD facility. REV Group also maintained its commitment to shareholder returns, declaring a $0.06 quarterly cash dividend and returning a total of $117.6 million to shareholders year to date.

The company’s ABL credit facility availability stood at $247.2 million, providing ample liquidity for operations and strategic initiatives.

Updated Guidance

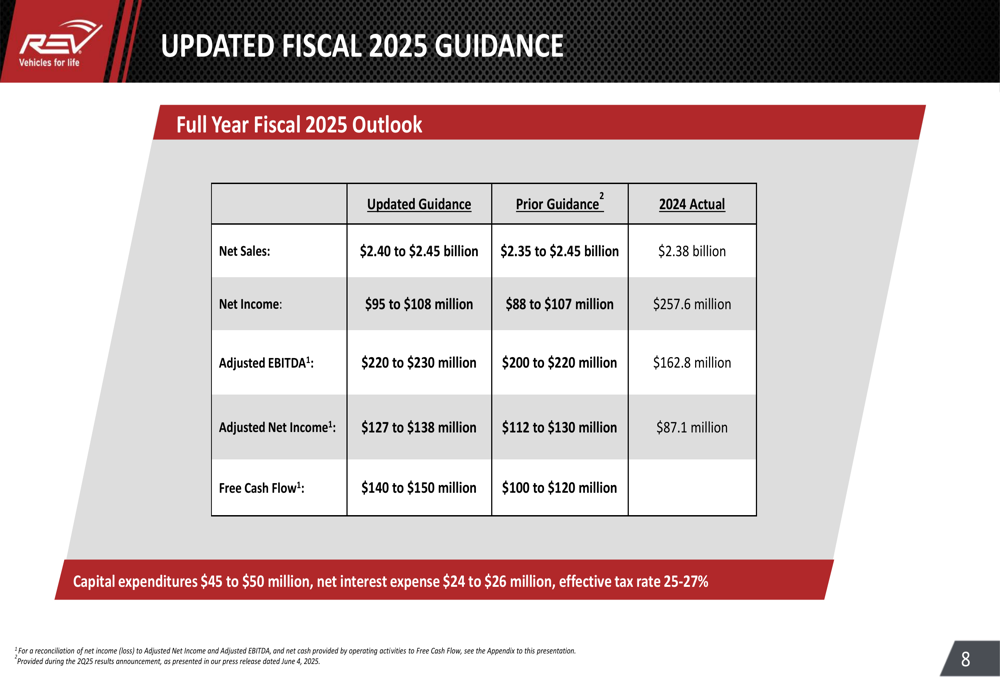

Based on the strong performance in the third quarter, REV Group raised its full-year fiscal 2025 guidance across multiple metrics. The company now expects net sales of $2.40 to $2.45 billion, up from the previous range of $2.35 to $2.45 billion. Adjusted EBITDA guidance was raised significantly to $220 to $230 million, compared to the prior range of $200 to $220 million.

The updated guidance is detailed in the following table:

The company also raised its free cash flow guidance to $140 to $150 million, up from the previous range of $100 to $120 million, reflecting confidence in continued strong cash generation. Capital expenditures are projected at $45 to $50 million, net interest expense at $24 to $26 million, and an effective tax rate of 25-27%.

Forward-Looking Statements

Looking ahead, REV Group expects continued momentum in its Specialty Vehicles segment, with sequential revenue growth anticipated in Q4 2025 and incremental margin conversion of 20% to 25%. The company’s strong backlog in this segment provides visibility into future quarters.

For the Recreational Vehicles segment, challenges are expected to persist with the continued impact of tariffs through Q4. However, the company’s strategic focus on operational efficiency and pricing actions should help mitigate some of these headwinds.

Overall, REV Group’s raised guidance reflects management’s confidence in the company’s ability to execute its strategic initiatives and deliver strong financial results for the full fiscal year 2025. The company’s focus on cash generation and balance sheet strength positions it well for continued investment in growth opportunities while maintaining shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.