Stock market today: S&P 500 ekes gain as hopes for end of shutdown get major boost

Introduction & Market Context

Revolve Group LLC (NYSE:RVLV) presented its third-quarter 2025 financial results on November 4, showcasing significant margin expansion and profitability growth despite modest sales increases. The fashion e-commerce company reported a 4% year-over-year increase in net sales, which slightly missed analyst expectations and contributed to a 6.2% stock decline in after-hours trading to $21.30.

The presentation highlighted Revolve’s ability to drive substantial bottom-line improvements through operational efficiency and strategic inventory management, even as revenue growth moderated in a challenging consumer environment.

Quarterly Performance Highlights

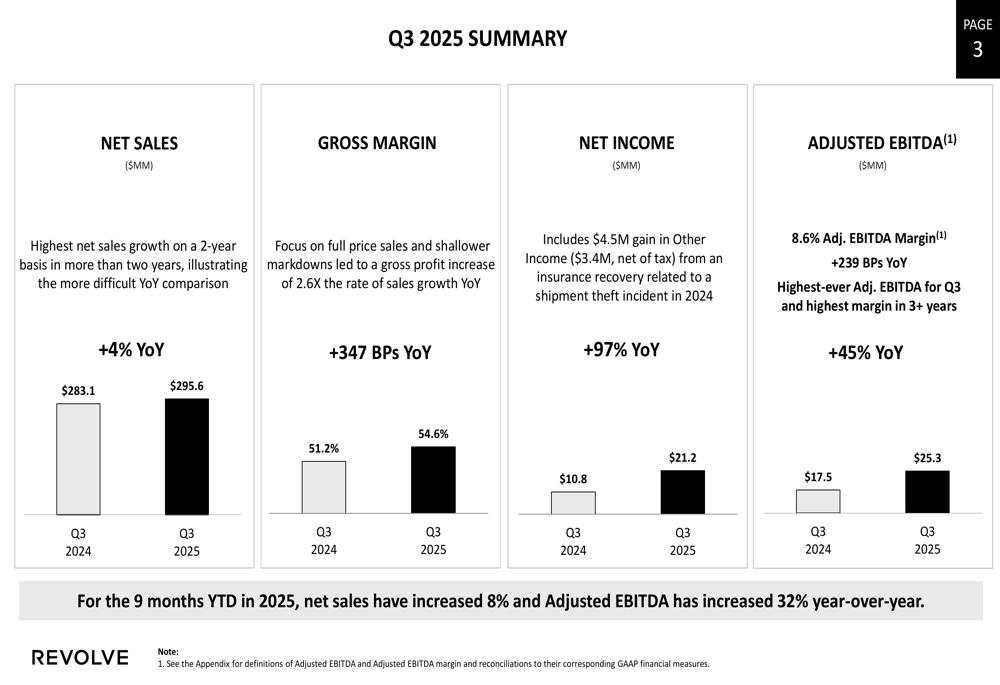

Revolve reported net sales of $295.6 million for Q3 2025, representing a 4% year-over-year increase. While this growth rate was modest, the company achieved its strongest profitability metrics in several years, with gross margin expanding by 347 basis points to 54.6% compared to 51.2% in Q3 2024.

As shown in the following summary of Q3 2025 performance:

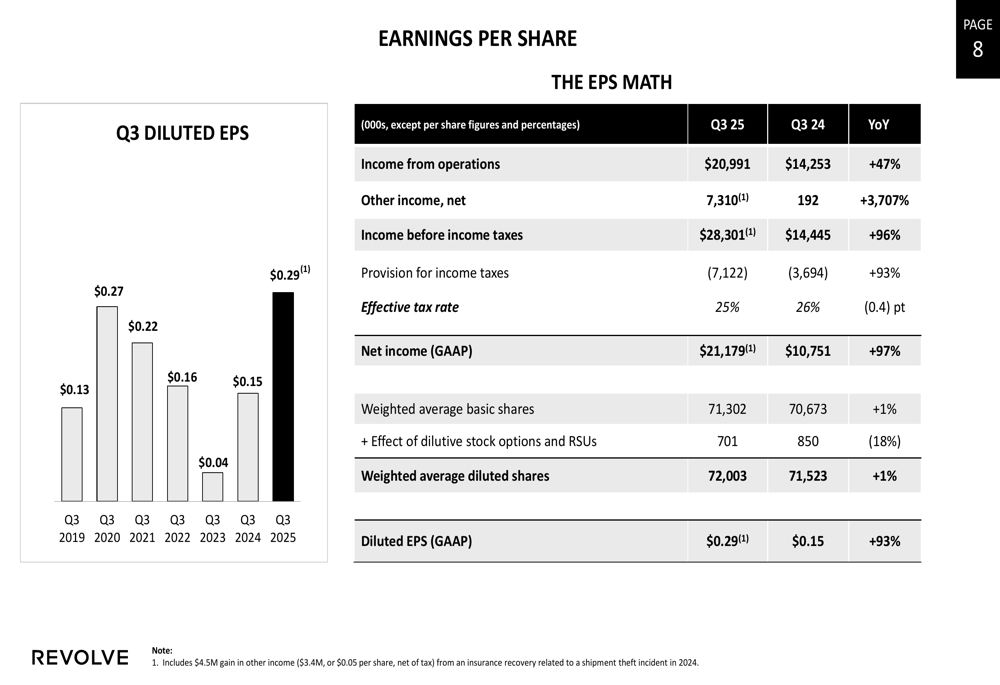

Net income surged 97% year-over-year to $21.2 million, though this figure included a $4.5 million gain ($3.4 million after tax) from an insurance recovery related to a shipment theft incident in 2024. Even adjusting for this one-time gain, profitability showed substantial improvement.

Adjusted EBITDA reached $25.3 million, representing an 8.6% margin and a 239 basis point improvement from the previous year. This marked the highest-ever Q3 Adjusted EBITDA for the company and the highest margin in over three years.

Segment and Geographic Performance

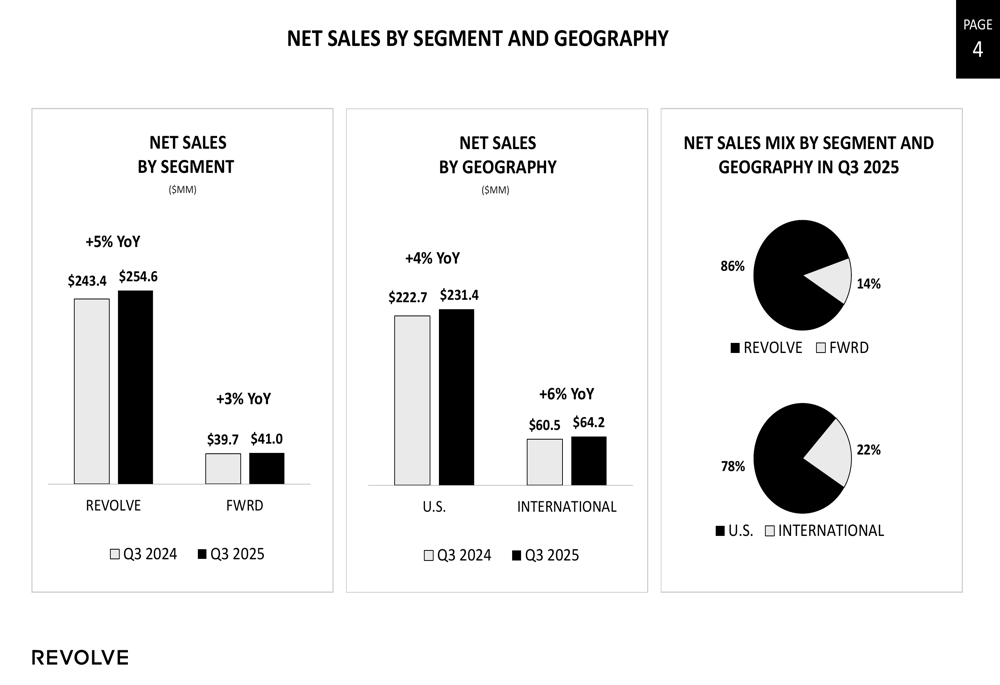

Revolve’s performance was balanced across its business segments and geographic regions, with both the core REVOLVE segment and luxury-focused FWRD segment showing growth.

The detailed breakdown of net sales by segment and geography reveals:

The REVOLVE segment generated $254.6 million in net sales, up 5% year-over-year, while the FWRD segment contributed $41.0 million, increasing 3% from the previous year. Notably, international sales grew at a faster pace than domestic, with international revenue up 6% to $64.2 million compared to a 4% increase in U.S. sales to $231.4 million.

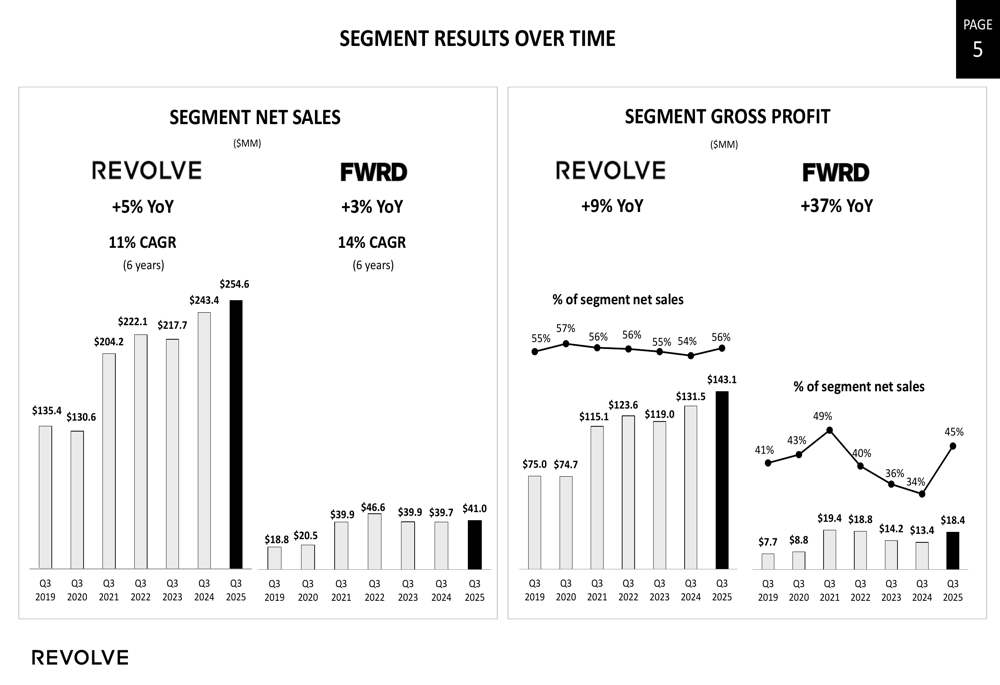

The company’s long-term growth trajectory remains impressive, with the REVOLVE segment achieving an 11% CAGR over six years and the FWRD segment growing at a 14% CAGR during the same period:

Customer Metrics and Engagement

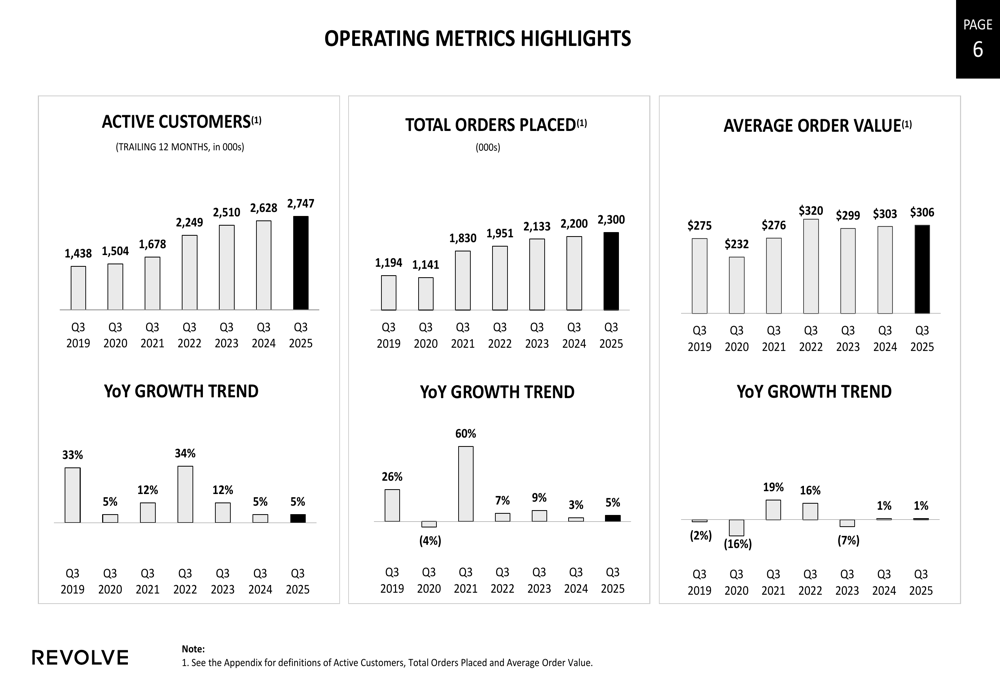

Revolve’s customer engagement metrics showed consistent improvement, with active customers increasing 5% year-over-year to 2.75 million in the trailing 12 months. Total orders also grew 5% to 2.3 million, while average order value increased slightly by 1% to $306.

The following chart illustrates these key operating metrics:

These engagement metrics suggest that Revolve is successfully attracting and retaining customers despite a challenging retail environment, though the modest growth in average order value indicates some pricing pressure.

Margin and Profitability Analysis

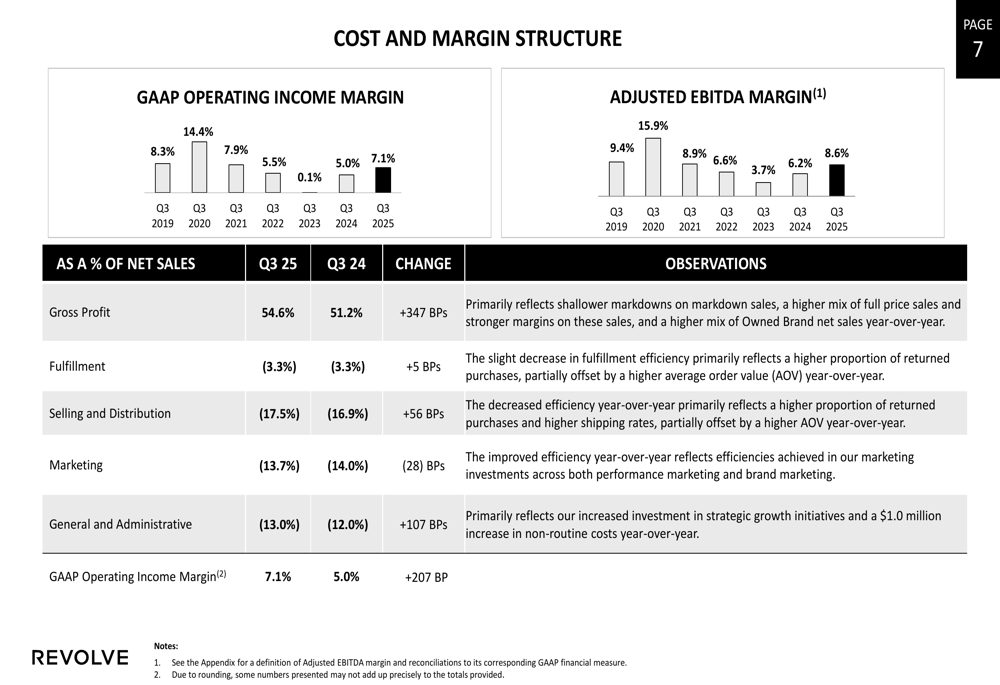

The most impressive aspect of Revolve’s Q3 performance was its significant margin expansion. The company’s detailed cost and margin structure reveals substantial improvements in gross profit margin, which was partially offset by increases in certain operating expenses:

The 347 basis point improvement in gross margin was attributed to shallower markdowns, a higher mix of full-price sales, and stronger margins on owned brand sales. While selling and distribution costs increased by 56 basis points and general and administrative expenses rose by 107 basis points, the company managed to reduce marketing expenses by 28 basis points.

These factors combined to drive a 207 basis point improvement in GAAP operating income margin, which reached 7.1% compared to 5.0% in the prior year.

The earnings per share breakdown further illustrates the company’s profitability improvements:

Cash Flow and Balance Sheet Strength

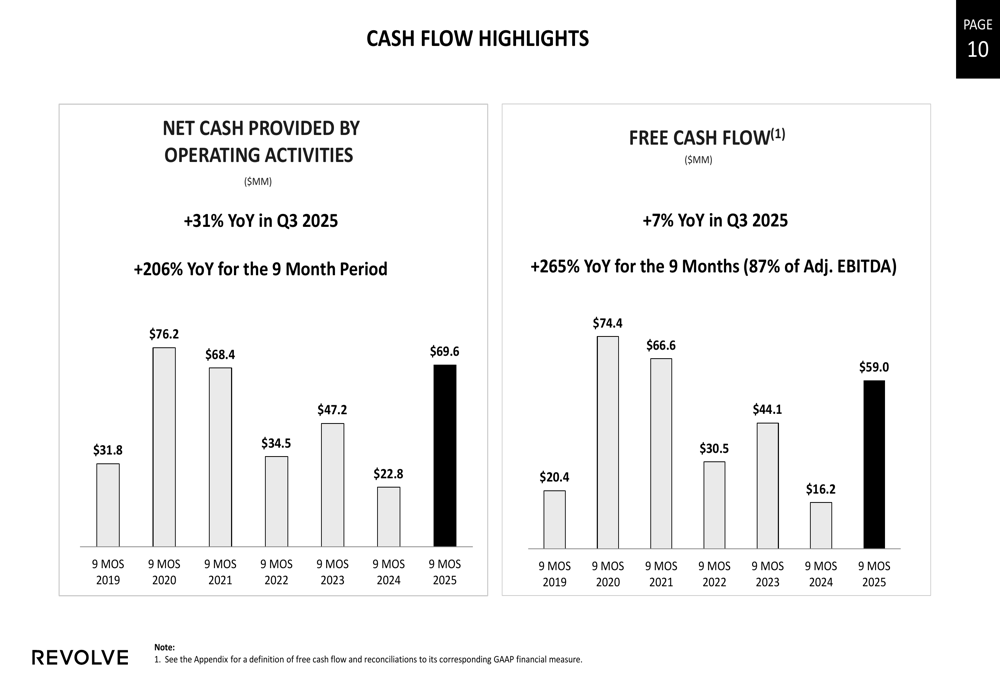

Revolve demonstrated exceptional cash generation capabilities in Q3 2025, with significant improvements in both operating cash flow and free cash flow:

For the first nine months of 2025, net cash provided by operating activities reached $69.6 million, representing a remarkable 206% increase year-over-year. Free cash flow totaled $59.0 million for the same period, up 265% from the previous year and representing 87% of Adjusted EBITDA.

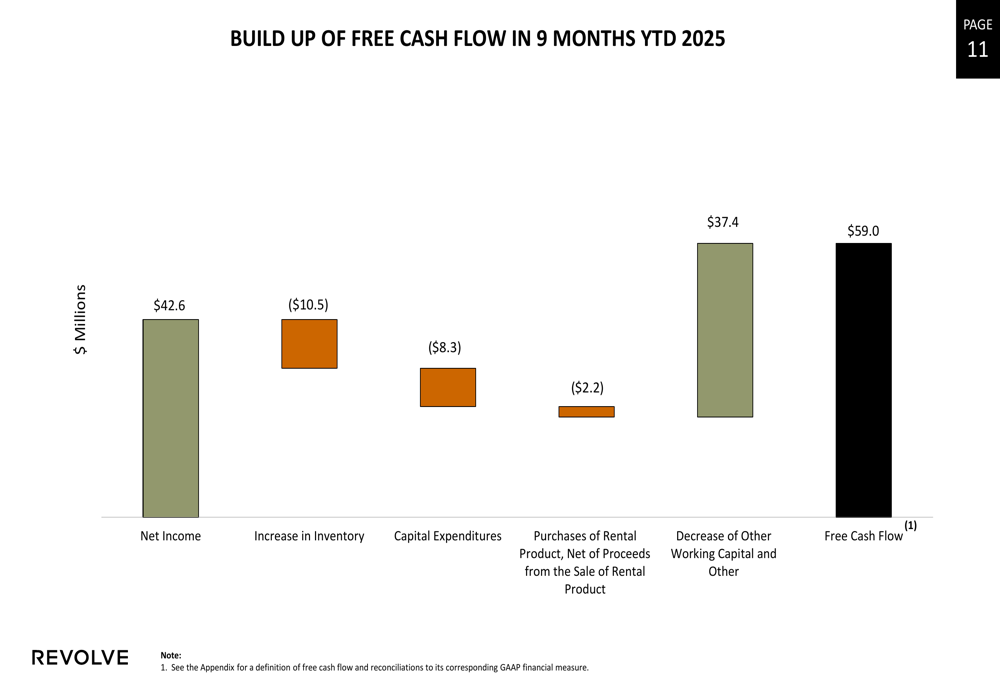

The components of free cash flow highlight Revolve’s efficient working capital management:

The company’s balance sheet remains exceptionally strong, with $315.4 million in cash and cash equivalents. Revolve also continued its stock repurchase program, buying back 14,612 shares at an average cost of $19.36 per share during Q3.

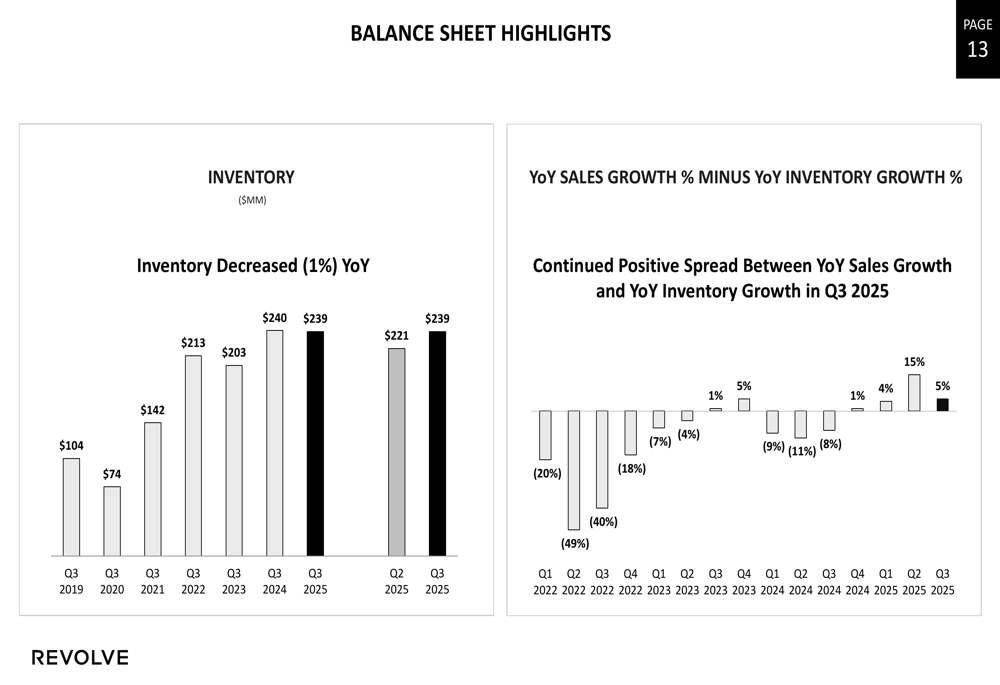

Inventory management was particularly impressive, with inventory decreasing 1% year-over-year to $239 million despite the 4% sales growth:

Forward-Looking Statements

Looking ahead, Revolve plans to participate in several investor conferences in December 2025, including the Morgan Stanley Global Consumer and Retail Conference, Barclays Eat, Sleep, Play, Shop Conference, and Raymond James TMT and Consumer Conference.

The company has increased its full-year 2025 gross margin guidance to approximately 53.5% and expects Q4 gross margins between 53.1% and 53.6%. Management indicated plans for significant marketing investments in 2026, focusing on international expansion and physical retail opportunities, including a new store at The Grove in Los Angeles.

Despite the strong financial performance highlighted in the presentation, investors appeared concerned about the modest revenue growth rate, resulting in the stock’s decline following the earnings release. However, the company’s robust profitability metrics, strong cash generation, and solid balance sheet position it well to navigate ongoing market uncertainties while investing in future growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.