European shares fall: Trump threatens ’massive’ tariff increase on China

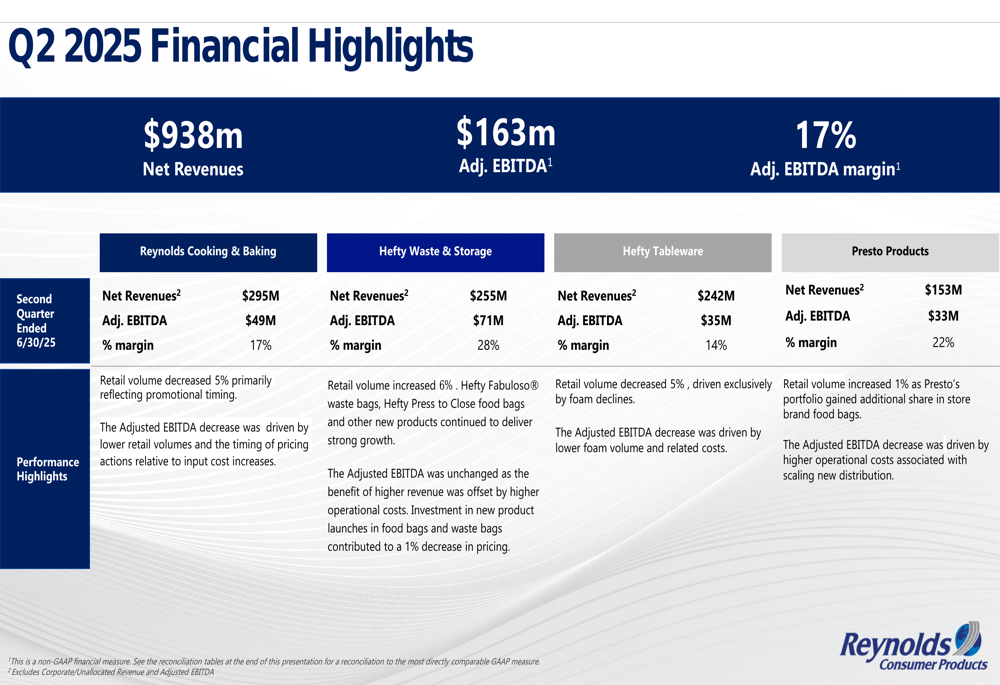

Reynolds Consumer Products Inc (NASDAQ:REYN) reported second quarter 2025 results with $938 million in net revenue and $163 million in adjusted EBITDA, representing a 17% margin, according to the company’s earnings presentation released on July 30, 2025. The household products manufacturer maintained its full-year guidance despite acknowledging ongoing challenges in the consumer and operating environment.

Quarterly Performance Highlights

Reynolds delivered what it characterized as "a solid quarter in a challenging consumer and operating environment," with net income of $73 million and adjusted diluted earnings per share of $0.39. This represents a decline from the same period last year when the company reported net income of $97 million and adjusted diluted EPS of $0.46.

The company emphasized its focus on meeting consumers’ needs for affordability, value, and convenience while implementing pricing strategies to offset high input costs.

As shown in the following financial highlights breakdown, performance varied across the company’s four business segments:

Reynolds Cooking & Baking generated $295 million in revenue with a 17% adjusted EBITDA margin, while Hefty Waste & Storage delivered the highest profitability with a 28% margin on $255 million in revenue. Hefty Tableware recorded $242 million in revenue with a 14% margin, and Presto Products contributed $153 million with a 22% margin.

Segment Analysis

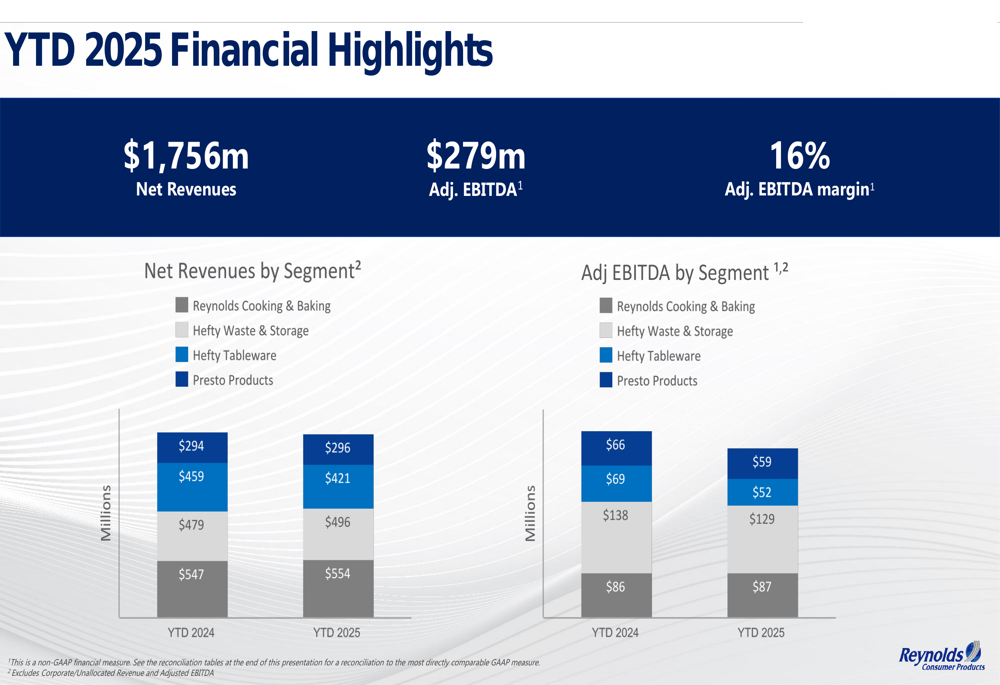

Year-to-date performance through Q2 2025 shows mixed results across segments when compared to the previous year. The company’s total net revenues for the first half of 2025 reached $1,756 million, with adjusted EBITDA of $279 million, representing a 16% margin.

The following chart illustrates the year-over-year comparison by segment:

Hefty Tableware showed the strongest year-over-year revenue growth, while Hefty Waste & Storage experienced the most significant decline. On the profitability side, all segments except Presto Products saw lower adjusted EBITDA compared to the same period in 2024.

These results align with trends observed in Q1 2025, when Reynolds reported challenges related to retailer inventory management and declining consumer confidence. The stock has continued to face pressure, trading at $21.56 as of July 29, 2025, down from $23.70 after Q1 results.

Strategic Initiatives

Reynolds outlined its strategic framework focused on three key pillars: revenue growth, margin expansion, and return on investment. The company aims to accelerate growth through distribution wins and product innovation while executing cost reduction initiatives across the supply chain.

As illustrated in the following strategic framework:

"We are executing well in a challenging operating environment, while also investing in the long-term potential of our business," said Scott Huckins, President and CEO. "We believe our US-centric business model is a competitive advantage, and we are building on that advantage by implementing programs to drive additional growth, margin and returns."

The company is advancing several priorities for 2025, including safety as a top priority, accelerating growth through distribution and innovation, executing cost savings for margin expansion, delivering more stable earnings growth, and investing in people development.

Outlook & Guidance

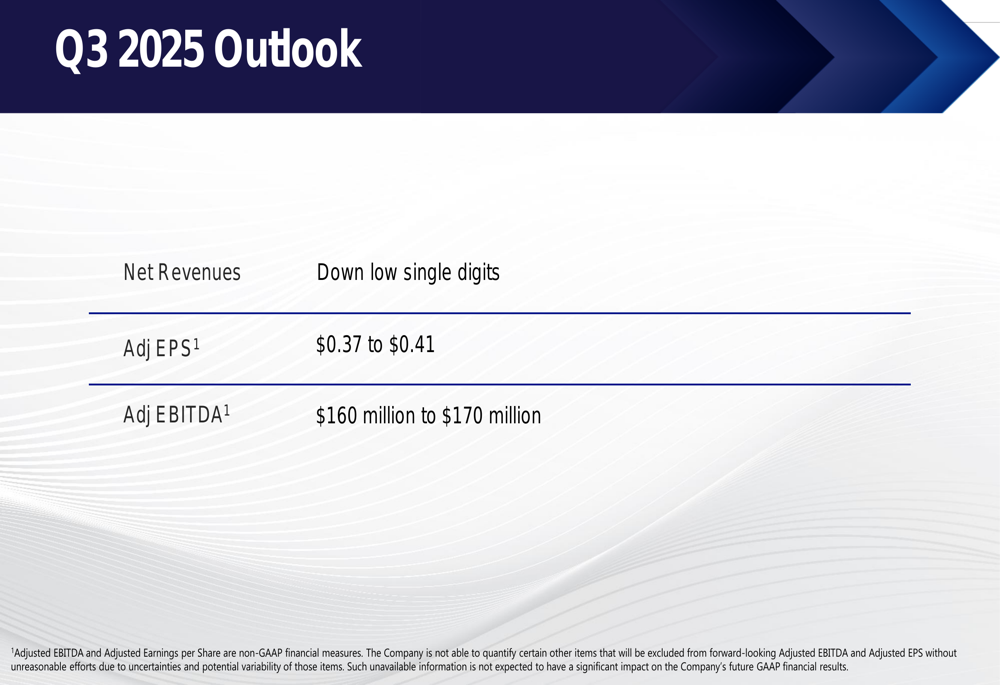

For the third quarter of 2025, Reynolds expects net revenues to decline in the low single digits, with adjusted earnings per share between $0.37 and $0.41 and adjusted EBITDA between $160 million and $170 million.

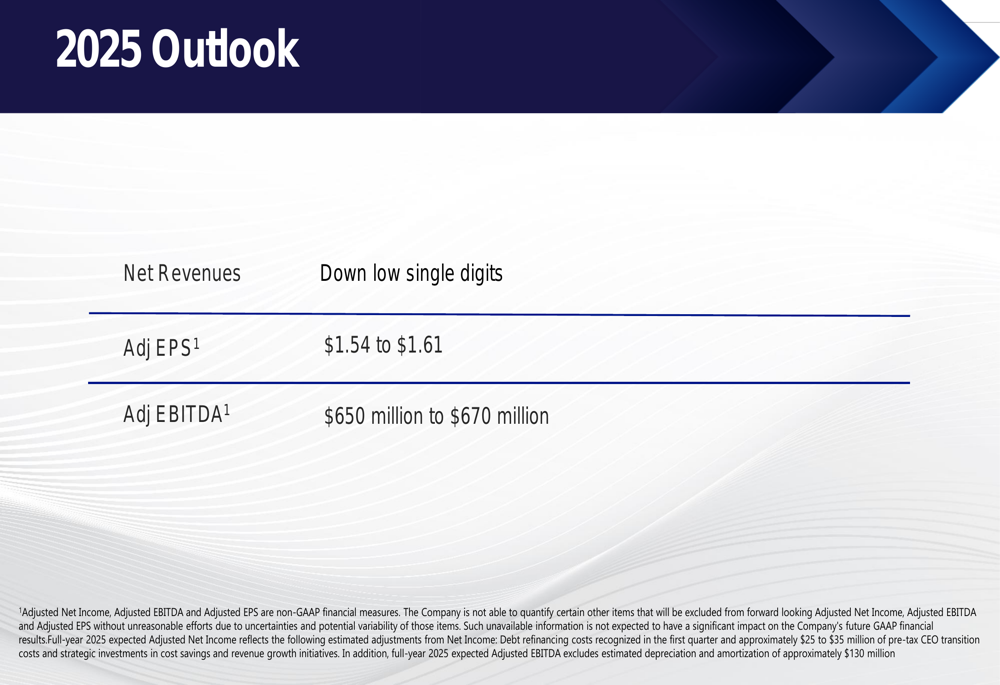

The full-year 2025 outlook remains consistent with previous guidance, projecting net revenues to decline in the low single digits, with adjusted earnings per share between $1.54 and $1.61 and adjusted EBITDA between $650 million and $670 million.

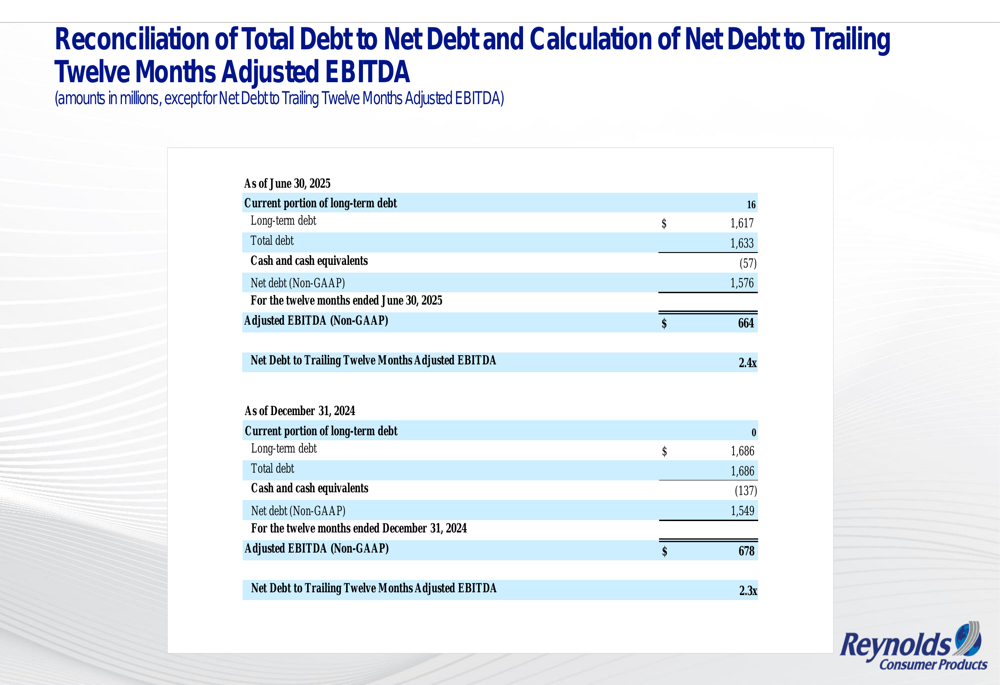

Reynolds maintains a relatively stable balance sheet with total debt of $1,633 million and net debt of $1,576 million as of June 30, 2025. The company’s net debt to trailing twelve months adjusted EBITDA ratio stands at 2.4x, a slight increase from 2.3x at the end of 2024.

The company’s financial outlook reflects ongoing challenges in the consumer products sector, including tariff impacts, retailer destocking, and cost headwinds. However, management remains focused on implementing strategic initiatives to drive long-term growth and structural margin expansion despite these near-term pressures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.