Street Calls of the Week

Introduction & Market Context

Ribbon Communications Inc (NASDAQ:RBBN) released its first quarter 2025 results on April 29, revealing a mixed performance with stable revenue but declining profitability. The company’s stock reacted negatively in after-hours trading, dropping 10.79% to $3.35, suggesting investor disappointment despite management maintaining its full-year outlook.

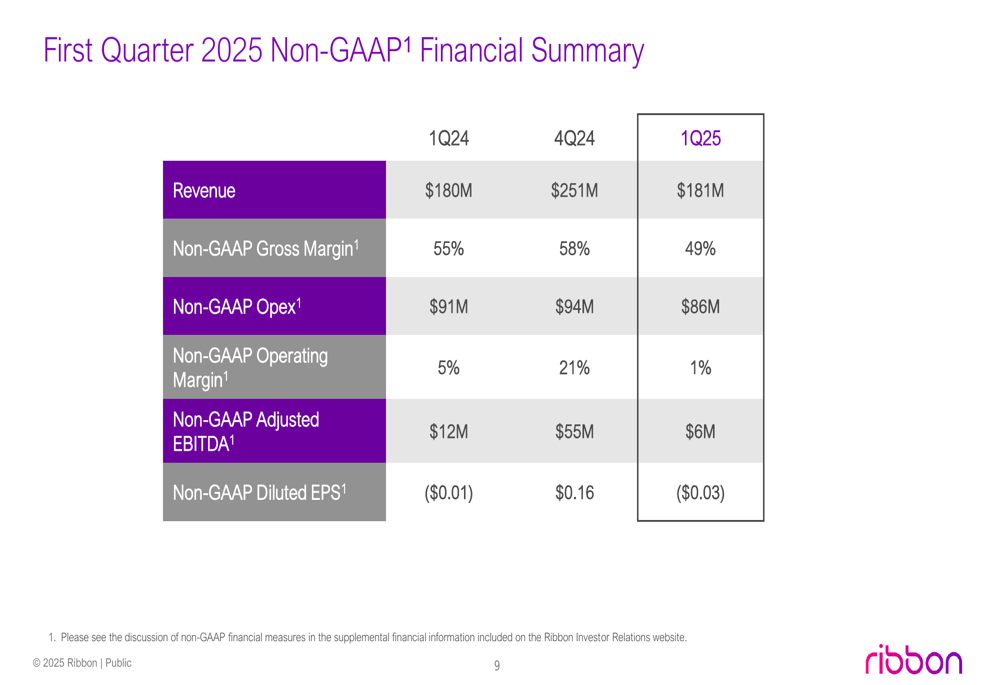

The communications technology provider reported modest 1% year-over-year revenue growth to $181 million, while adjusted EBITDA fell to $6 million, representing a 3.2% margin compared to $12 million (6.7% margin) in the same period last year. The results highlight diverging performance between the company’s two main business segments.

Quarterly Performance Highlights

Ribbon’s Q1 2025 results showed relatively flat topline performance with revenue reaching $181 million, a slight 1% increase year-over-year. However, profitability metrics declined significantly, with gross margin falling to 49% from 55% in Q1 2024, and adjusted EBITDA dropping to $6 million from $12 million in the prior year.

As shown in the following quarterly business highlights:

The company’s product and services backlog increased 35% compared to 2024, suggesting potential future revenue growth. Cash from operations was negative at ($4 million), which included annual employee incentive compensation payments. The company ended the quarter with $74 million in cash and a net debt leverage ratio of 2.4x.

Detailed Financial Analysis

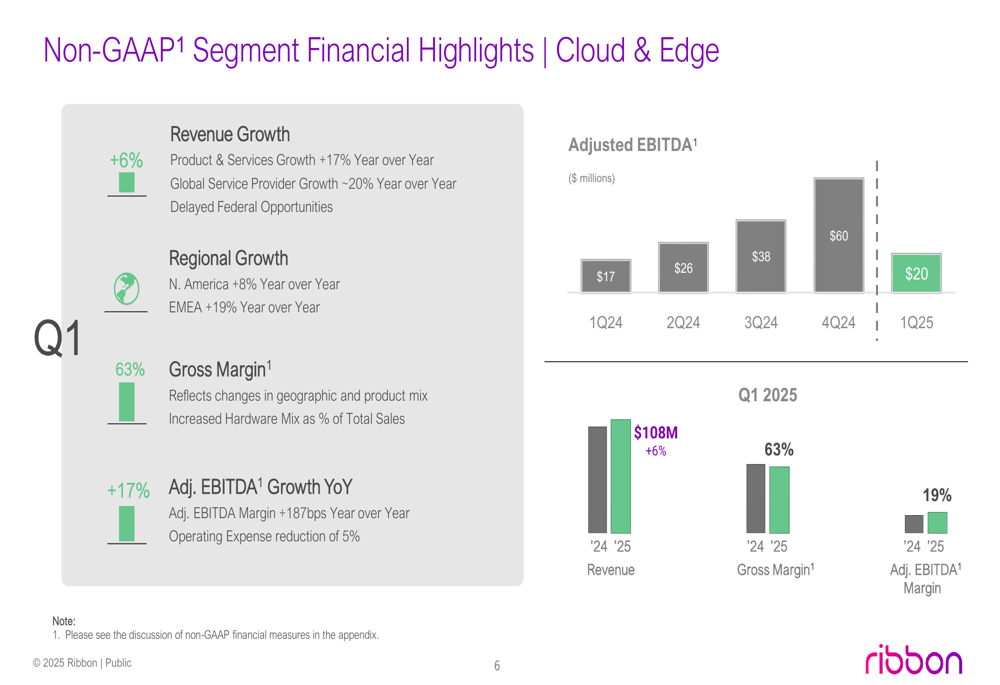

Ribbon’s financial performance reveals a stark contrast between its two business segments. The Cloud & Edge segment demonstrated solid growth, while IP Optical Networks faced significant challenges.

The Cloud & Edge segment posted revenue of $108 million, up 6% year-over-year, with particularly strong performance in North America (+8%) and EMEA (+19%). This segment maintained a healthy gross margin of 63% and achieved adjusted EBITDA growth of 17% year-over-year, with a 19% margin.

The segment’s performance is detailed in the following slide:

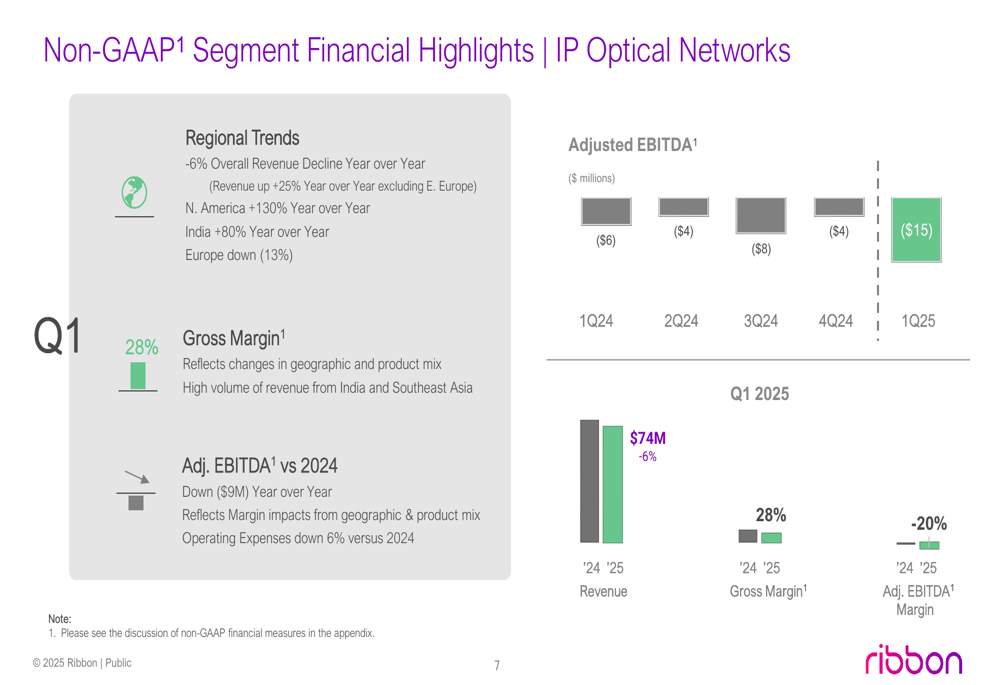

In contrast, the IP Optical Networks segment struggled considerably, with revenue declining 6% year-over-year to $74 million. More concerning was the segment’s profitability, with gross margin dropping to 28% from 41% in Q1 2024, and adjusted EBITDA deteriorating to ($15 million) from ($6 million) in the prior year.

The challenges in the IP Optical segment are illustrated here:

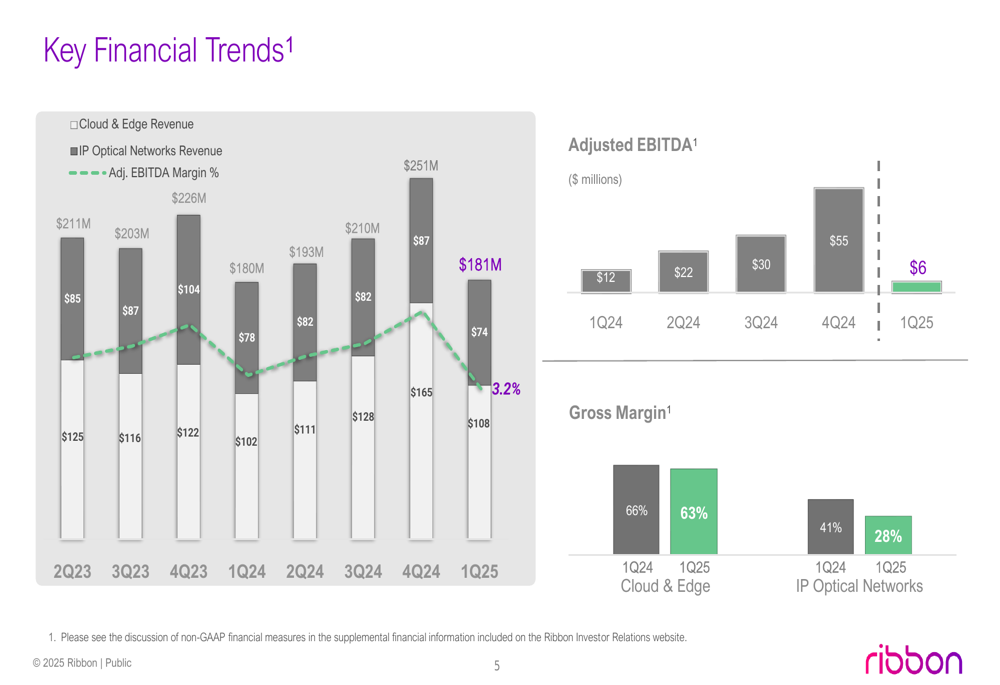

The company’s overall financial trends show the impact of these divergent segment performances:

Ribbon’s consolidated financial summary provides a clear comparison across recent quarters, highlighting the significant drop in profitability from Q4 2024 to Q1 2025:

Strategic Initiatives & Competitive Position

Despite the challenging quarter, Ribbon continues to focus on key growth areas, particularly network modernization and government/defense secure communications. The company highlighted its strength in service provider spending for voice network modernization and unified communications, as well as strategic wins in the government sector.

Ribbon’s innovation strategy centers on several key technologies driving future growth:

1. Telco Cloud Transition (Hardware → Virtualized → Cloud Native)

2. TDM over IP (Circuit Emulation)

3. Data Center Interconnect

4. Apollo 9408 and MUSE platforms

5. IP Router NPT 2714, which received the 2025 Lightwave Innovation Award

The company identified five key areas shaping its 2025 operating environment:

Forward-Looking Statements

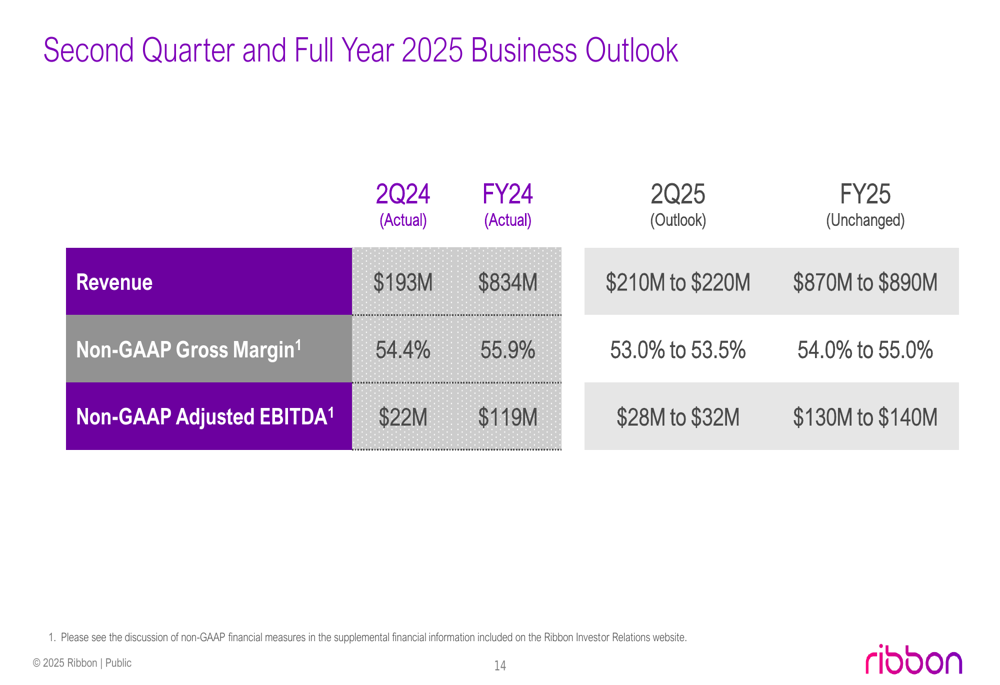

Despite Q1 challenges, Ribbon maintained its full-year 2025 guidance, suggesting confidence in stronger performance for the remainder of the year. For Q2 2025, the company expects:

- Revenue of $210-220 million (compared to $193 million in Q2 2024)

- Non-GAAP gross margin of 53.0-53.5% (compared to 54.4% in Q2 2024)

- Non-GAAP adjusted EBITDA of $28-32 million (compared to $22 million in Q2 2024)

For the full year 2025, Ribbon continues to project:

- Revenue of $870-890 million (compared to $834 million in FY 2024)

- Non-GAAP gross margin of 54.0-55.0% (compared to 55.9% in FY 2024)

- Non-GAAP adjusted EBITDA of $130-140 million (compared to $119 million in FY 2024)

The detailed outlook is presented in this slide:

The maintained guidance suggests Ribbon expects significant improvement in coming quarters, particularly in the IP Optical Networks segment, which would need to recover from its Q1 performance to meet full-year targets.

Market Reaction & Outlook

The market’s negative reaction to Ribbon’s Q1 results, with shares falling nearly 11% in after-hours trading, indicates investor concern about the company’s ability to achieve its full-year targets given the weak start to 2025. The significant decline in profitability, particularly in the IP Optical Networks segment, appears to have overshadowed the positive performance in the Cloud & Edge business.

For Ribbon to meet its full-year guidance, the company will need to demonstrate substantial improvement in the IP Optical Networks segment while maintaining momentum in Cloud & Edge. The projected Q2 2025 results suggest the beginning of this recovery, with expected revenue growth of 9-14% year-over-year and significantly improved adjusted EBITDA.

The company’s success will likely depend on its ability to capitalize on the network modernization opportunities it has identified, particularly in voice infrastructure and government/defense communications, while addressing the profitability challenges in its optical business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.