Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Luxury goods conglomerate Compagnie Financiere Richemont SA (SIX:CFR) reported solid sales growth in its first quarter of fiscal year 2026, according to the company’s presentation released on July 16, 2025. The Swiss luxury group, which owns prestigious brands including Cartier, Van Cleef & Arpels, and Montblanc, achieved 6% growth at constant exchange rates despite continued challenges in key Asian markets and its specialist watchmaking segment.

The results highlight Richemont’s ability to navigate a complex global luxury market where consumer spending patterns vary significantly by region. The company’s diversified portfolio and strong performance in jewelry have helped offset weaknesses in other segments, particularly in watchmaking where the industry continues to face headwinds.

Quarterly Performance Highlights

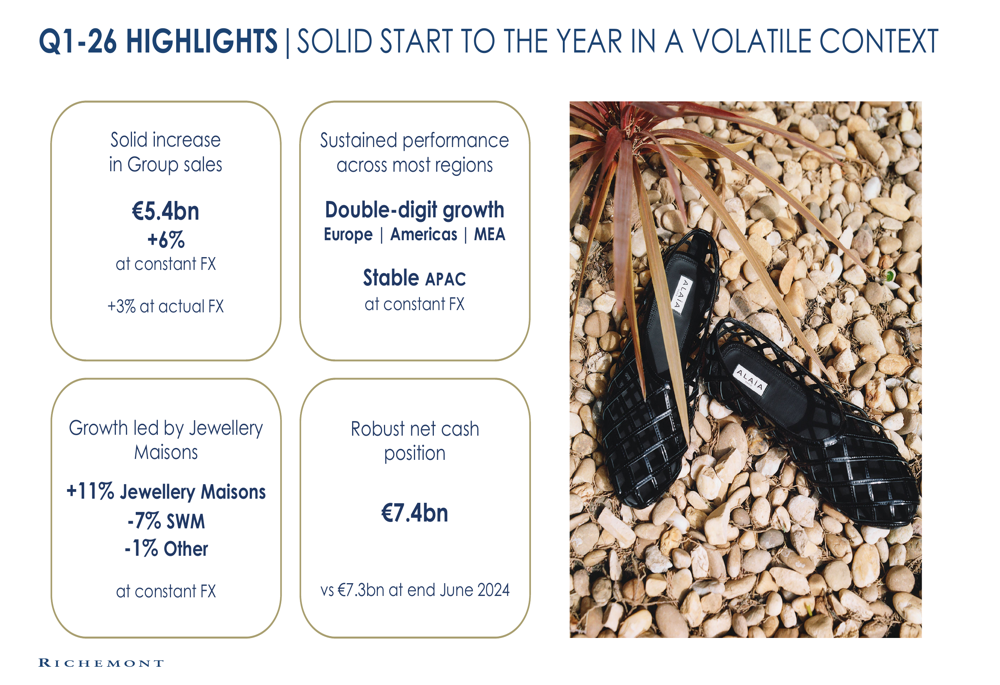

Richemont reported group sales of €5.4 billion for Q1 FY26, representing a 6% increase at constant exchange rates and 3% growth at actual exchange rates. The company also maintained a robust net cash position of €7.4 billion, slightly improved from €7.3 billion at the end of June 2024.

As shown in the following quarterly highlights, the company’s performance was primarily driven by its Jewellery Maisons, while other segments faced more challenging conditions:

The results demonstrate Richemont’s resilience in a luxury market that continues to see uneven recovery across regions. The company’s strong performance in jewelry has been a consistent bright spot, helping to counterbalance challenges in other areas of the business.

Regional Performance Analysis

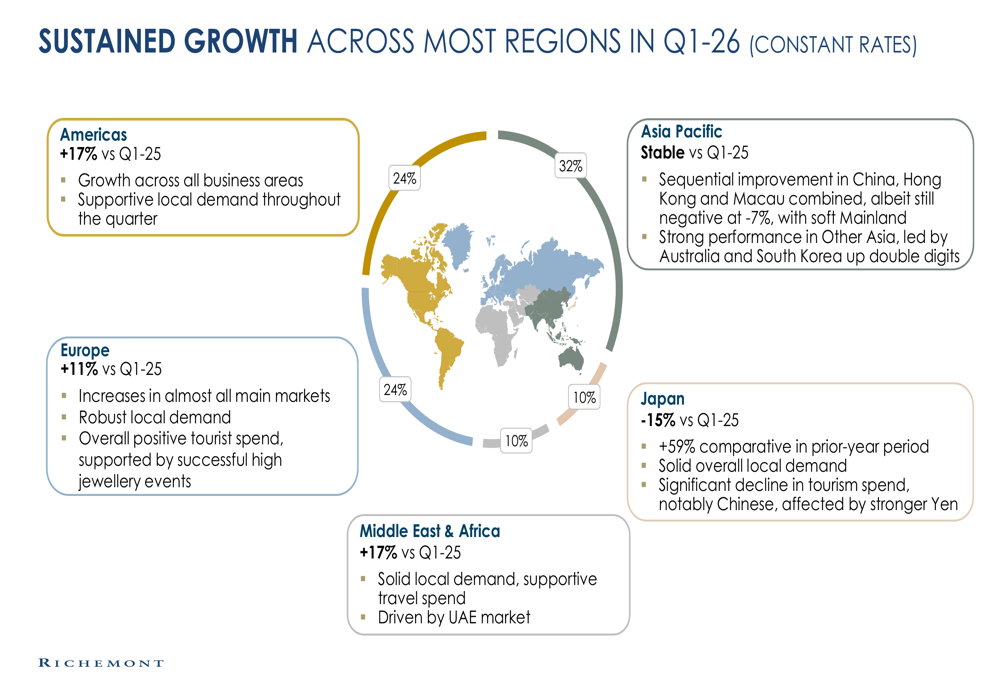

Richemont’s sales growth was geographically diverse, with strong performance in Western markets and the Middle East offsetting more challenging conditions in Asia. The Americas led growth with a 17% increase, while Europe and the Middle East & Africa both delivered double-digit growth as well.

The following regional breakdown illustrates the varied performance across markets:

The Americas region benefited from supportive local demand across all business areas, resulting in 17% growth compared to Q1 FY25. European markets saw an 11% increase, driven by robust local demand, positive tourist spending, and successful high jewelry events.

The Middle East & Africa region matched the Americas’ strong performance with 17% growth, led particularly by the UAE market, which benefited from both solid local demand and supportive travel spending.

Asia Pacific remained stable year-over-year, though with significant variation within the region. China, Hong Kong, and Macau showed sequential improvement but still declined 7% overall, with particular weakness in mainland China. This was offset by strong performance in other Asian markets, with Australia and South Korea achieving double-digit growth.

Japan was the only major region to show a significant decline, dropping 15% compared to Q1 FY25. However, this follows an exceptionally strong comparative period when sales surged 59% in the prior year. While local demand remained solid, the significant reduction in tourism spending heavily impacted overall results.

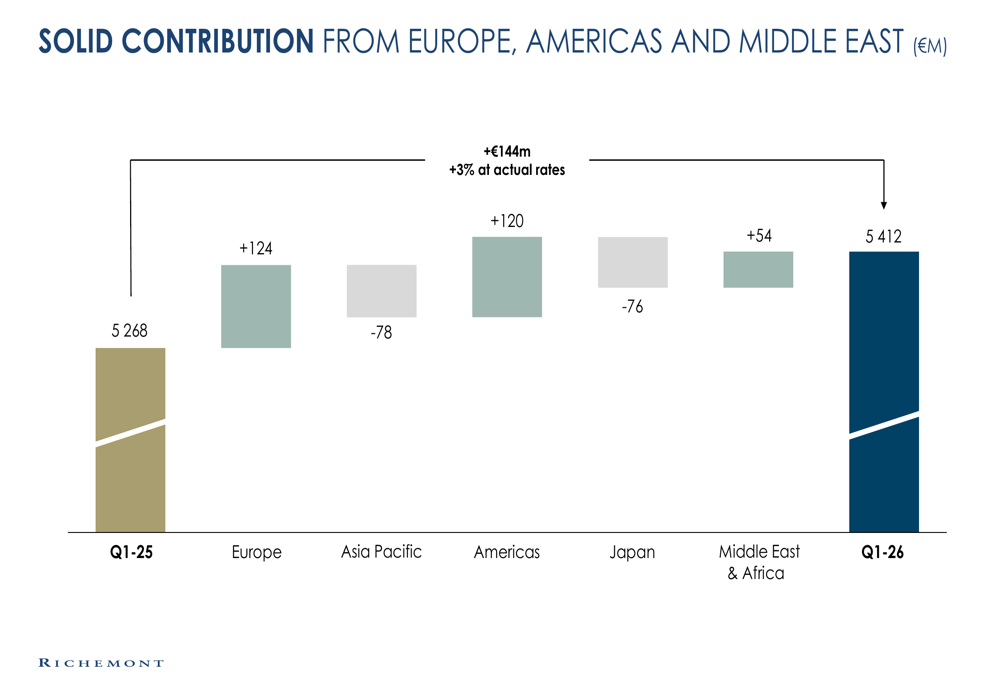

The waterfall chart below provides a clear visualization of how each region contributed to the overall sales change:

Business Segment Breakdown

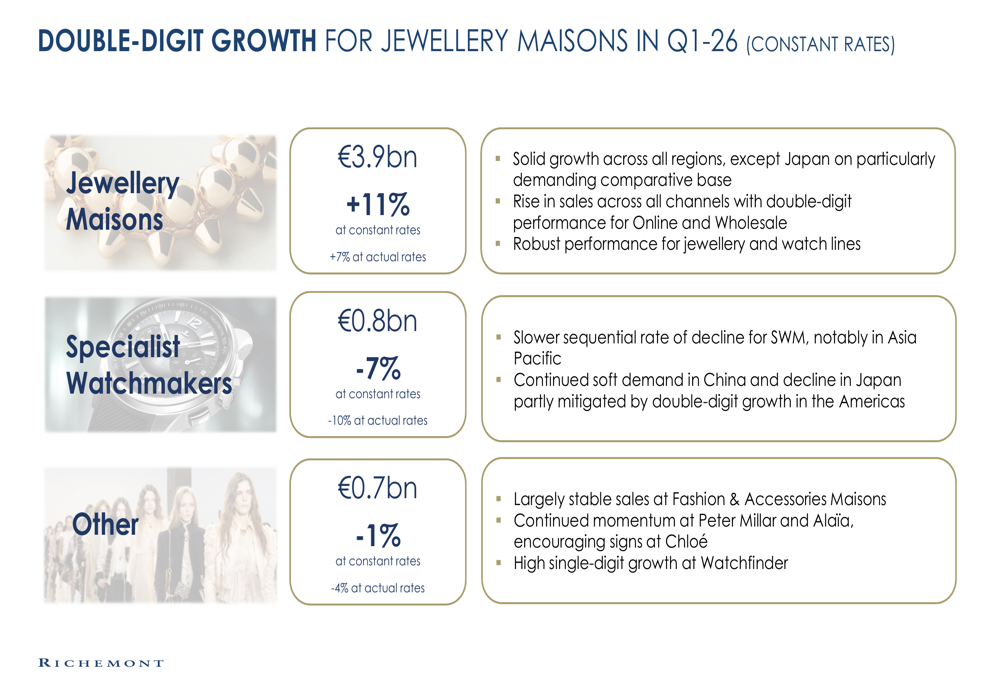

Richemont’s business segments showed divergent performance, with Jewellery Maisons delivering exceptional results while Specialist Watchmakers and Other businesses faced more challenging conditions.

The following breakdown illustrates performance across the company’s major business segments:

The Jewellery Maisons segment, which includes flagship brands Cartier and Van Cleef & Arpels, was the standout performer with sales of €3.9 billion, representing 11% growth at constant exchange rates (7% at actual rates). This segment showed solid growth across all regions except Japan, with increased sales across all channels and robust performance in both jewelry and watch lines.

In contrast, Specialist Watchmakers recorded sales of €0.8 billion, declining 7% at constant rates (10% at actual rates). While this represents a slower sequential rate of decline for the segment, it continues to face challenges from soft demand in China and declining sales in Japan.

The Other segment, which includes Fashion & Accessories Maisons, reported sales of €0.7 billion, essentially flat with a 1% decline at constant rates (4% at actual rates). Within this segment, Peter Millar and Alaïa continued to show momentum, helping to stabilize overall performance.

Distribution Channel Performance

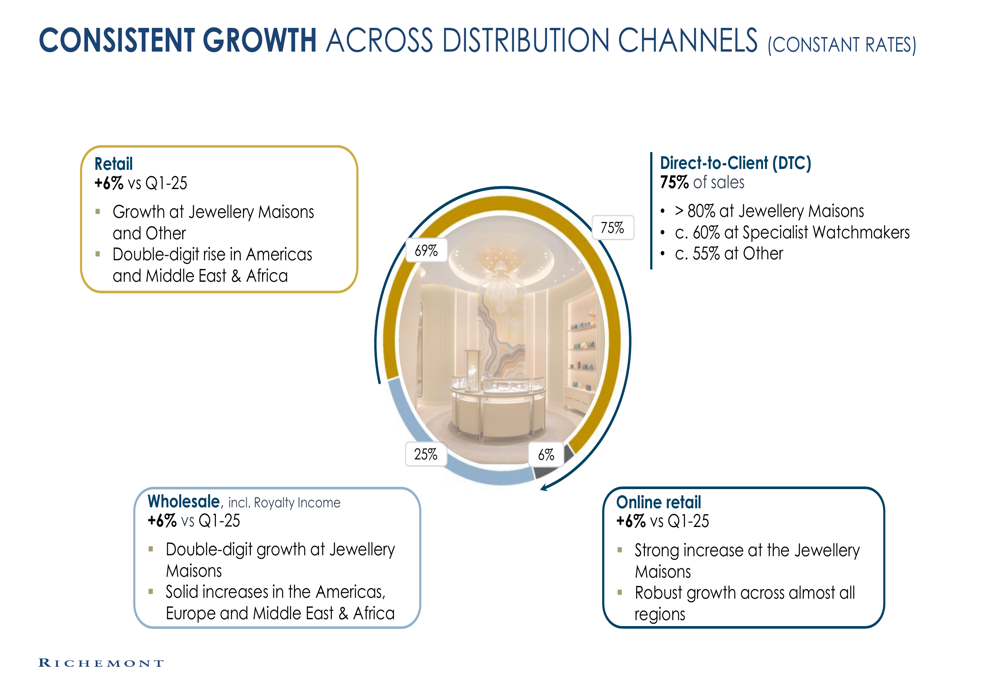

Richemont maintained consistent growth across its distribution channels, with Direct-to-Client (DTC) sales representing 75% of total revenue. The company’s balanced approach to distribution has helped ensure stable performance despite regional variations.

The following chart breaks down sales by distribution channel:

Retail, which forms the largest component of Richemont’s DTC strategy, grew 6% compared to Q1 FY25. This growth was primarily driven by the Jewellery Maisons and Other segments, with particularly strong performance in the Americas and Middle East & Africa, where double-digit increases were recorded.

Wholesale channels also grew 6% year-over-year, with double-digit growth at Jewellery Maisons and solid increases in the Americas, Europe, and Middle East & Africa regions.

Online Retail maintained the same growth rate of 6%, with strong increases at the Jewellery Maisons and robust growth across almost all regions. The consistent performance across channels demonstrates Richemont’s effective omnichannel strategy and ability to meet customers through their preferred shopping methods.

Forward-Looking Statements

While Richemont’s Q1 FY26 presentation focused primarily on reporting results rather than providing specific forward guidance, the company’s performance indicates several trends likely to influence future quarters.

The continued strength in Jewellery Maisons suggests this segment will remain the primary growth driver for Richemont in the near term. The sequential improvement in China, Hong Kong, and Macau, though still negative, offers cautious optimism for potential stabilization in these important luxury markets.

The challenges facing Specialist Watchmakers appear likely to persist, though the slowing rate of decline may indicate the segment is approaching an inflection point. Meanwhile, the consistent performance across distribution channels provides Richemont with a stable foundation for future growth initiatives.

Richemont’s robust net cash position of €7.4 billion gives the company significant financial flexibility to weather market uncertainties and potentially pursue strategic acquisitions or investments to strengthen its portfolio further.

As the luxury market continues to evolve, Richemont’s diversified regional presence and strong performance in key segments position the company to navigate the varied global economic landscape, though challenges in specific markets and segments will require continued strategic attention.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.