Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Ring Energy Inc (NYSE American:REI) presented its Q2 2025 earnings and updated guidance on August 7, 2025, revealing significant operational improvements despite ongoing challenges in the oil and gas sector. The company’s stock has experienced pressure over the past year, trading at $0.735 as of August 6, 2025, down from its 52-week high of $1.94.

The Q2 results mark a substantial turnaround from Q1 2025, when the company missed both revenue and earnings expectations. This improvement appears largely driven by the integration of the Lime Rock Resources acquisition and operational efficiencies.

Quarterly Performance Highlights

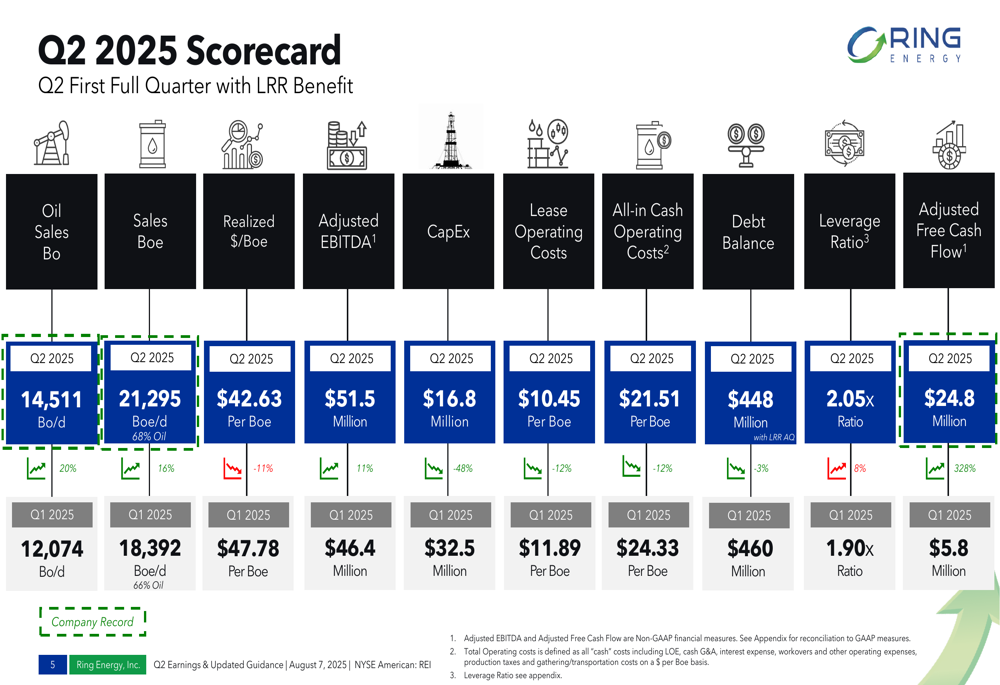

Ring Energy reported impressive Q2 2025 results, with total sales volumes reaching 21,295 Boe/d (68% oil), representing a 16% increase from Q1 2025. Oil sales grew even more substantially to 14,511 Bo/d, a 20% increase quarter-over-quarter.

As shown in the following Q2 2025 scorecard, the company achieved significant improvements across multiple metrics:

Particularly notable was the 328% increase in Adjusted Free Cash Flow to $24.8 million, compared to just $5.8 million in Q1. This dramatic improvement was supported by a 12% reduction in lease operating costs to $10.45 per Boe and a 12% decrease in all-in cash operating costs to $21.51 per Boe.

The company also reduced capital expenditures by 48% to $16.8 million while increasing Adjusted EBITDA by 11% to $51.5 million. These operational improvements helped Ring Energy reduce its debt balance by 3% to $448 million, though the leverage ratio increased slightly to 2.05x.

Strategic Initiatives & Acquisitions

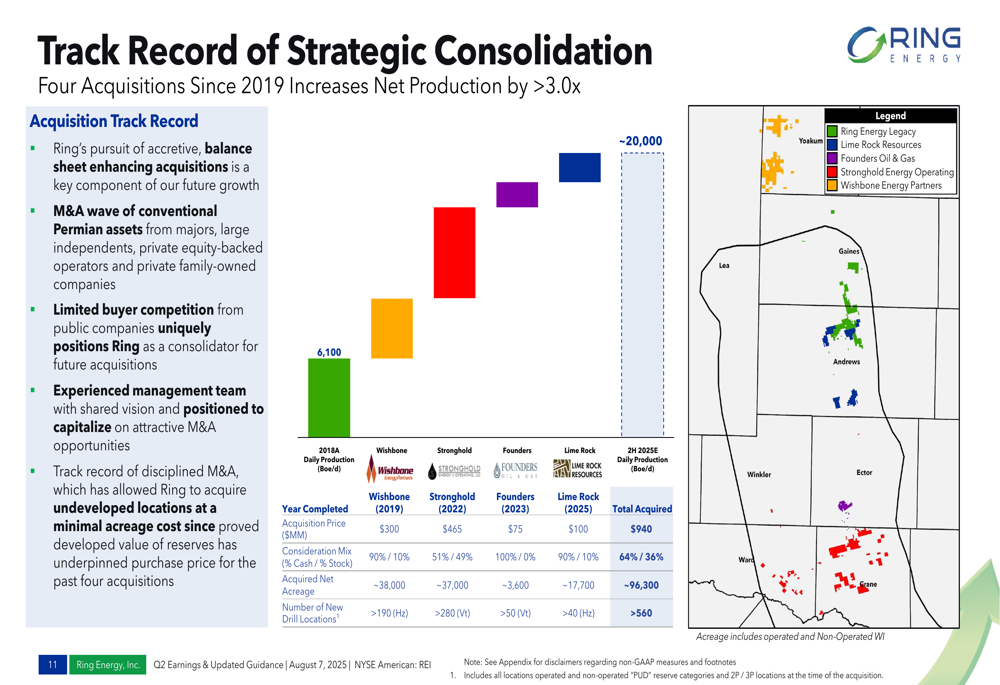

Ring Energy’s presentation emphasized its focus on conventional Permian Basin assets, particularly in the Central Basin Platform and Northwest Shelf regions. The company highlighted its strategic consolidation efforts, which have included multiple acquisitions since 2019.

The following slide illustrates Ring Energy’s acquisition history and current footprint:

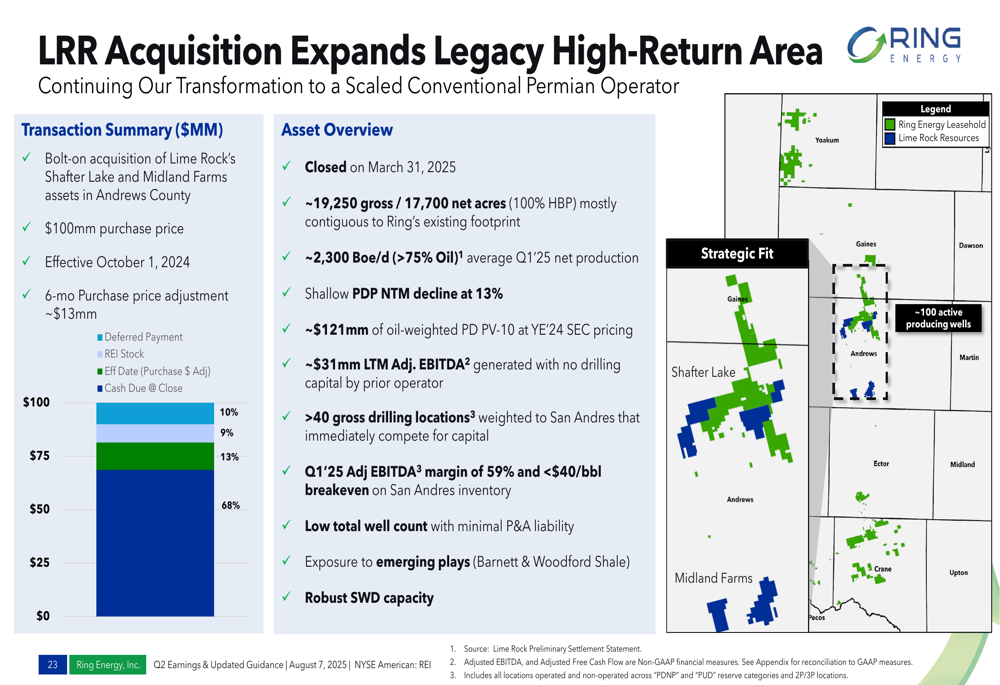

The recent Lime Rock Resources acquisition, completed for $100 million, has been a key driver of the company’s improved performance. This acquisition added approximately 12 MMBoe with a PV-10 value of about $160 million, expanding Ring’s presence in its legacy high-return area.

As detailed in the acquisition overview below, the Lime Rock assets include approximately 17,700 net acres contiguous to Ring’s existing footprint and added about 2,300 Boe/d of production (over 75% oil):

Ring Energy’s management emphasized that these acquisitions align with their strategy of pursuing "accretive, balance sheet enhancing acquisitions" while focusing on conventional assets that have been underexplored during the "shale era."

Competitive Industry Position

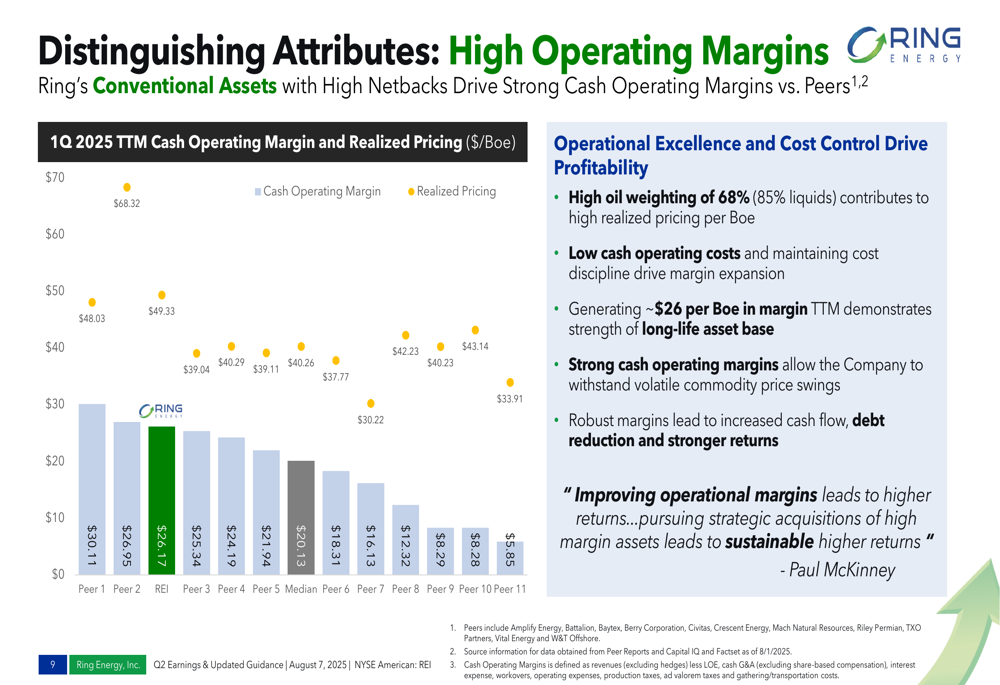

The presentation positioned Ring Energy as having distinct advantages compared to its peers, particularly in terms of operating margins. The company highlighted its conventional assets with high netbacks as driving strong cash operating margins.

As illustrated in the following comparative analysis, Ring Energy’s cash operating margin of approximately $26 per Boe demonstrates the strength of its long-life asset base relative to peers:

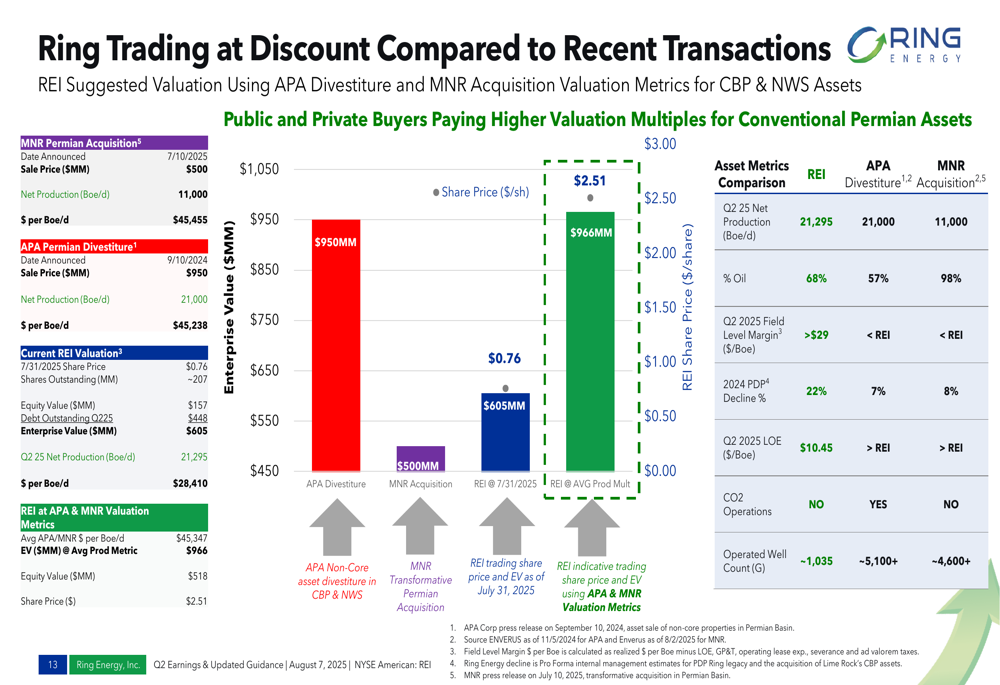

The company also argued that it is trading at a discount compared to recent transactions in the Permian Basin, specifically referencing the APA divestiture and MNR acquisition. This valuation gap was presented as a potential opportunity for investors:

Ring Energy’s competitive positioning is further strengthened by its operational characteristics, including shallow base decline rates, long-life wells (over 35 years), and high operational ownership with approximately 96% operated working interest.

Forward-Looking Statements & Guidance

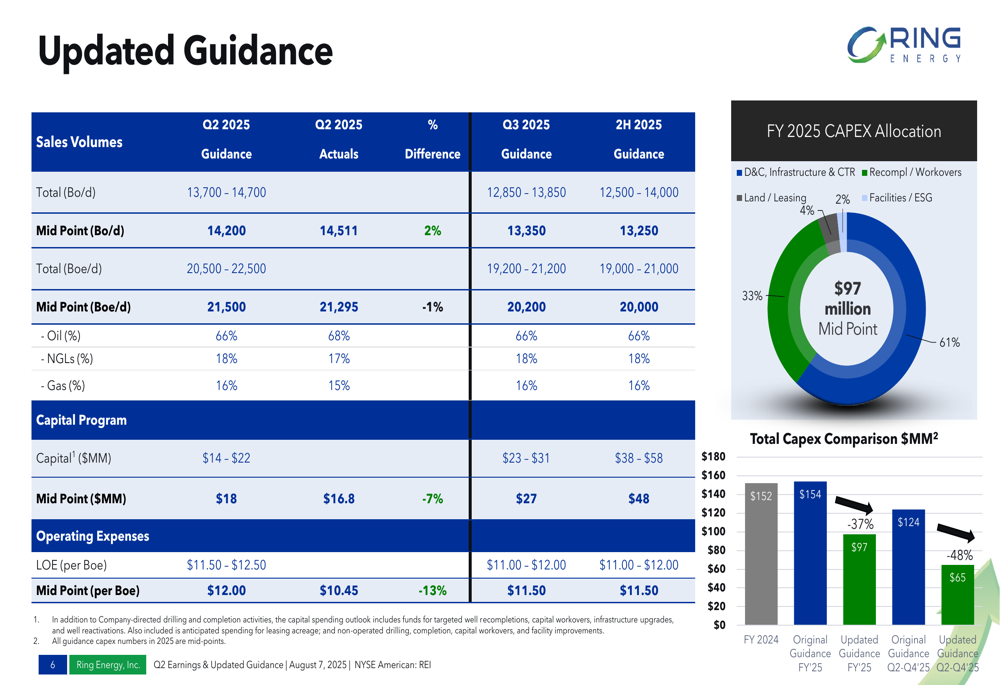

Looking ahead, Ring Energy provided updated guidance for Q3 and the second half of 2025. The company expects oil sales volumes to decrease slightly to 13,350 Bo/d in Q3 2025, with total sales volumes of approximately 20,200 Boe/d.

The detailed guidance, shown below, includes an increase in capital expenditures to $27 million in Q3 2025, up from $16.8 million in Q2:

Despite this increase in quarterly capex, Ring Energy has reduced its full-year 2025 capital expenditure guidance by 36% year-over-year while still projecting approximately 2% production growth. The company expects to generate between $50-75 million in adjusted free cash flow for the full year 2025.

Ring Energy’s hedging strategy includes protection for approximately 1.3 million barrels of oil for the remainder of 2025 at an average floor price of $64.87 per barrel, and approximately 2.3 million barrels for 2026 at an average floor price of $65.44 per barrel.

ESG Initiatives

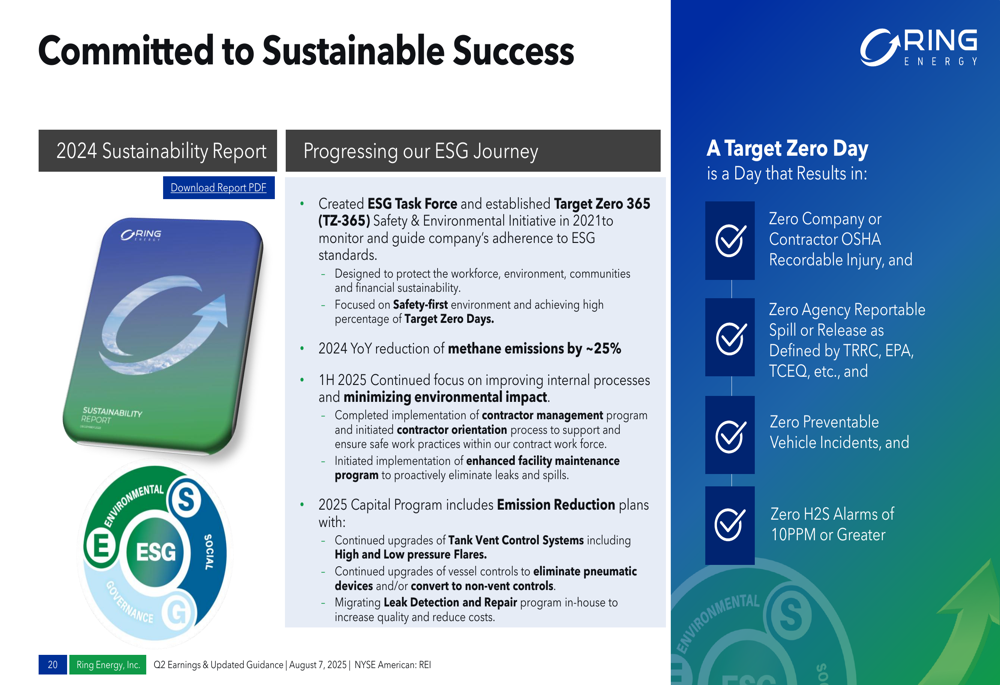

The company also highlighted its commitment to environmental, social, and governance (ESG) initiatives, including the creation of an ESG Task Force and the establishment of a " Target (NYSE:TGT) Zero 365" safety and environmental program.

As shown in the following slide, Ring Energy reported a 25% year-over-year reduction in methane emissions in 2024 and continues to upgrade tank vent control systems:

Conclusion

Ring Energy’s Q2 2025 presentation painted a picture of significant operational improvement, with substantial increases in free cash flow and production alongside meaningful cost reductions. The Lime Rock acquisition appears to be delivering the anticipated benefits, contributing to the company’s enhanced performance.

However, challenges remain, particularly regarding the company’s leverage ratio of 2.05x, which remains above its stated target of below 1.0x. Additionally, the disconnect between operational improvements and stock performance suggests investors may require further evidence of sustained progress before rewarding the company with a higher valuation.

As Ring Energy continues its strategy of conventional asset consolidation in the Permian Basin, its ability to maintain cost discipline while integrating acquisitions will be crucial to achieving its stated goals of maximizing free cash flow and reducing leverage.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.