Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

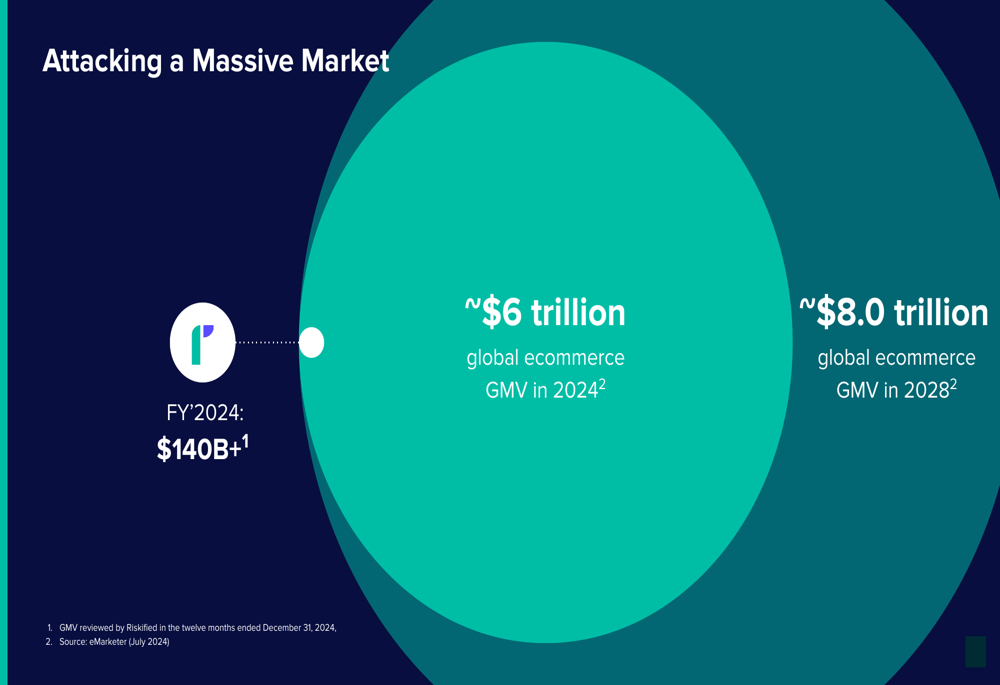

Riskified Ltd (NYSE:RSKD), an AI-powered fraud management and risk intelligence platform for e-commerce, reported its first quarter 2025 results showing continued revenue growth despite some margin pressure. The company’s investor presentation highlighted its position in the expanding global e-commerce market, which is projected to reach approximately $6 trillion in 2024 and grow to around $8 trillion by 2028.

As shown in the following chart, Riskified processes over $140 billion in annual Gross Merchandise Volume (GMV), positioning it as a significant player in the e-commerce risk intelligence sector:

Quarterly Performance Highlights

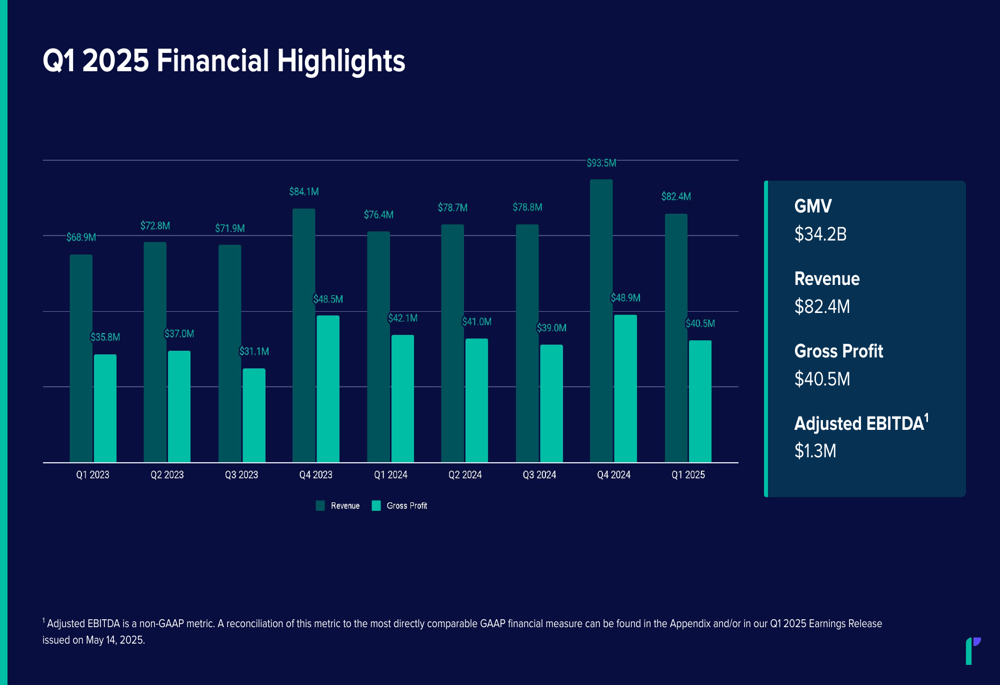

Riskified reported Q1 2025 revenue of $82.4 million, representing an 8% year-over-year increase from $76.4 million in Q1 2024. This marks a record first quarter for the company. The presentation highlighted that Riskified has maintained positive Adjusted EBITDA for six consecutive quarters, posting $1.3 million for Q1 2025.

The following chart illustrates Riskified’s quarterly revenue and gross profit performance over the past two years:

Despite the revenue growth, the company’s gross profit remained flat at $40.5 million compared to the same period last year, while gross profit margin declined from 55% in Q1 2024 to 49% in Q1 2025. This margin compression comes despite continued expense discipline, with non-GAAP operating expenses as a percentage of revenue declining year-over-year from 53% to 48%.

The company’s share repurchase program remained active, with 4.1 million shares repurchased for a total of $20.7 million during the quarter. This buyback activity reflects management’s confidence in the company’s long-term prospects despite the near-term margin challenges.

Detailed Financial Analysis

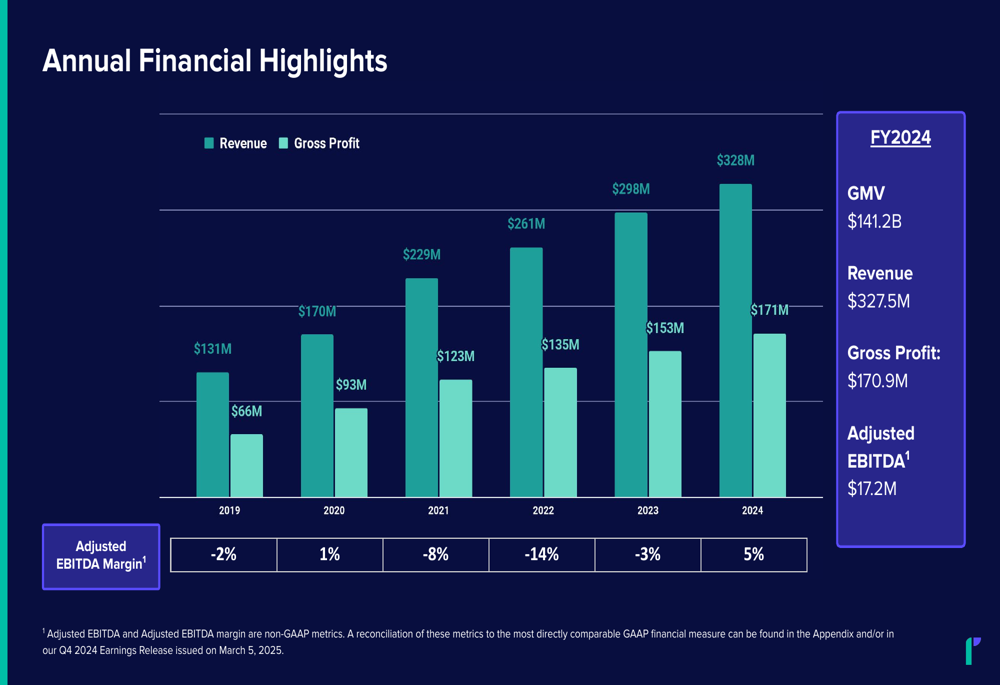

Riskified’s long-term financial trajectory continues to show improvement, with annual revenue growing from $131 million in 2019 to $327.5 million in 2024, as illustrated in the following chart:

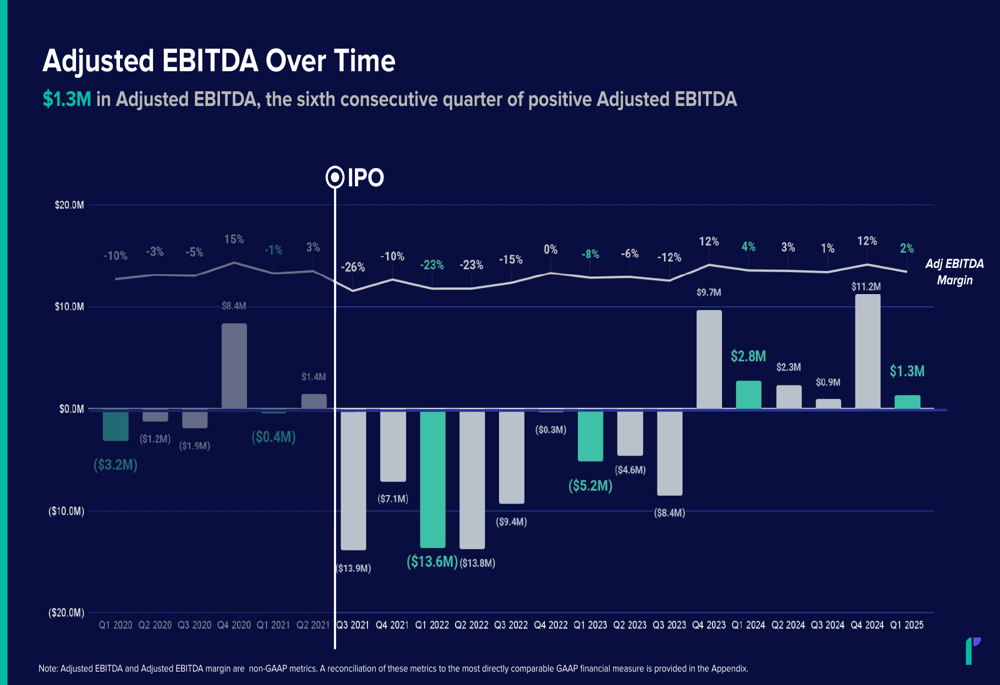

The company’s Adjusted EBITDA has shown significant improvement over time, turning consistently positive in recent quarters after several years of negative results. This trend demonstrates Riskified’s progress toward sustainable profitability:

However, it’s worth noting that while Adjusted EBITDA was positive at $1.3 million for Q1 2025, the company still reported a GAAP net loss of $13.9 million for the quarter. Additionally, Free Cash Flow decreased to $3.6 million in Q1 2025 compared to $10.5 million in Q1 2024.

The company maintains a strong balance sheet with $357 million in cash, deposits, and investments as of March 31, 2025, and zero debt. Management expects approximately $30 million in Free Cash Flow for the full year 2025.

Strategic Initiatives

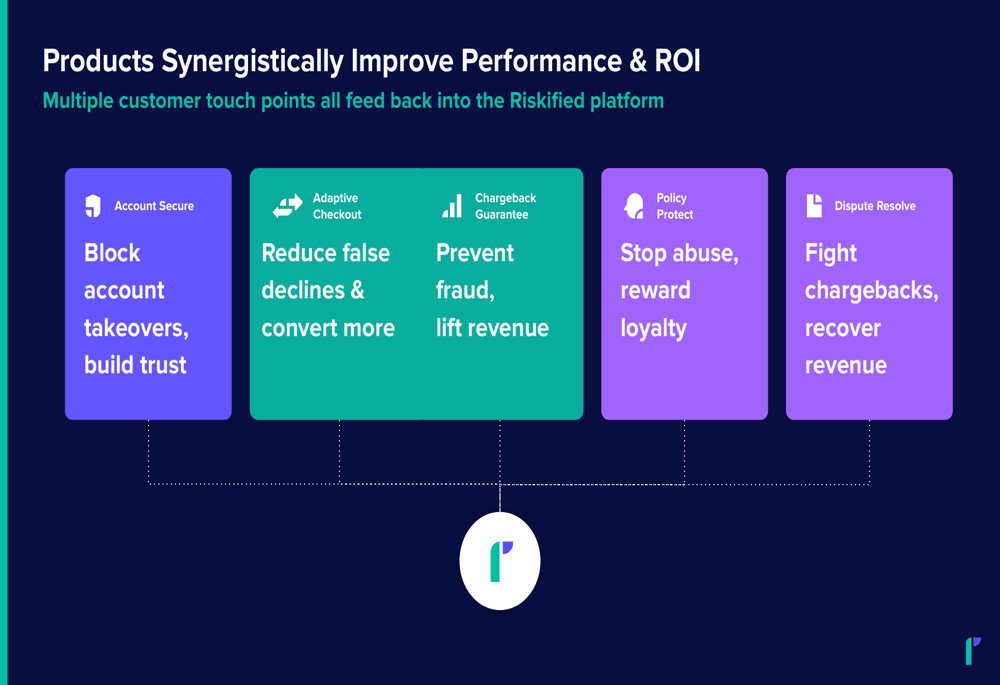

A key strategic focus for Riskified is diversifying beyond its core Chargeback Guarantee product. The presentation highlighted that revenue from products outside this core offering increased by approximately 190% year-over-year, indicating successful execution of the company’s platform expansion strategy.

The following image illustrates how Riskified’s various products work synergistically across the customer journey:

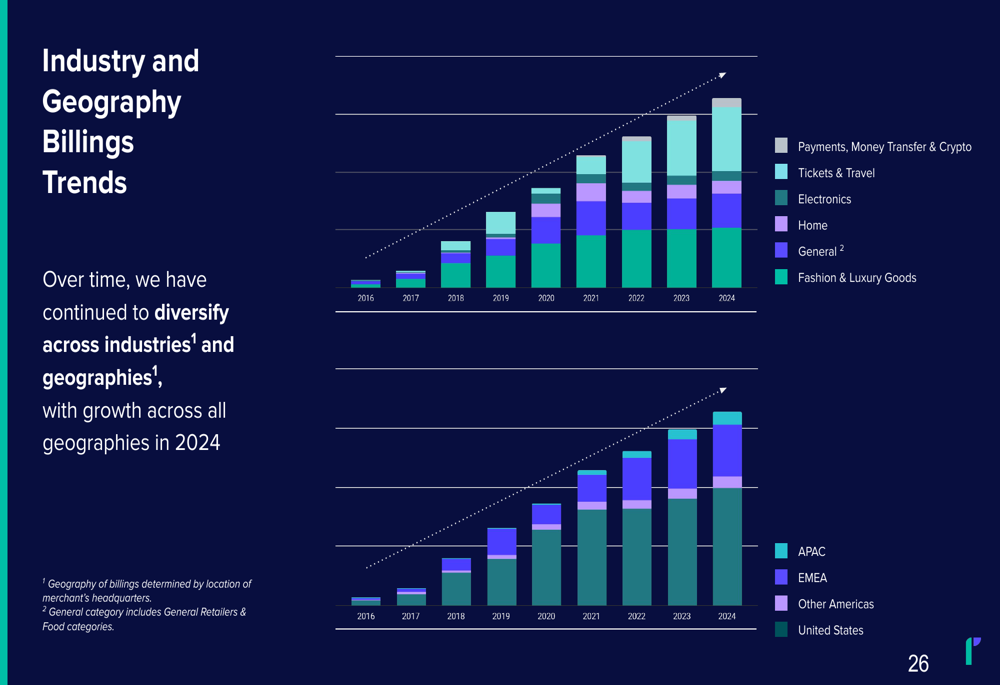

Riskified is also achieving greater vertical and geographic diversification. The presentation noted that the top ten new logos added in Q1 2025 were spread across four verticals and all four geographic regions. Particularly strong was the Money Transfer & Payments category, which showed revenue growth rates exceeding 90%.

The following chart demonstrates the company’s industry and geographic diversification:

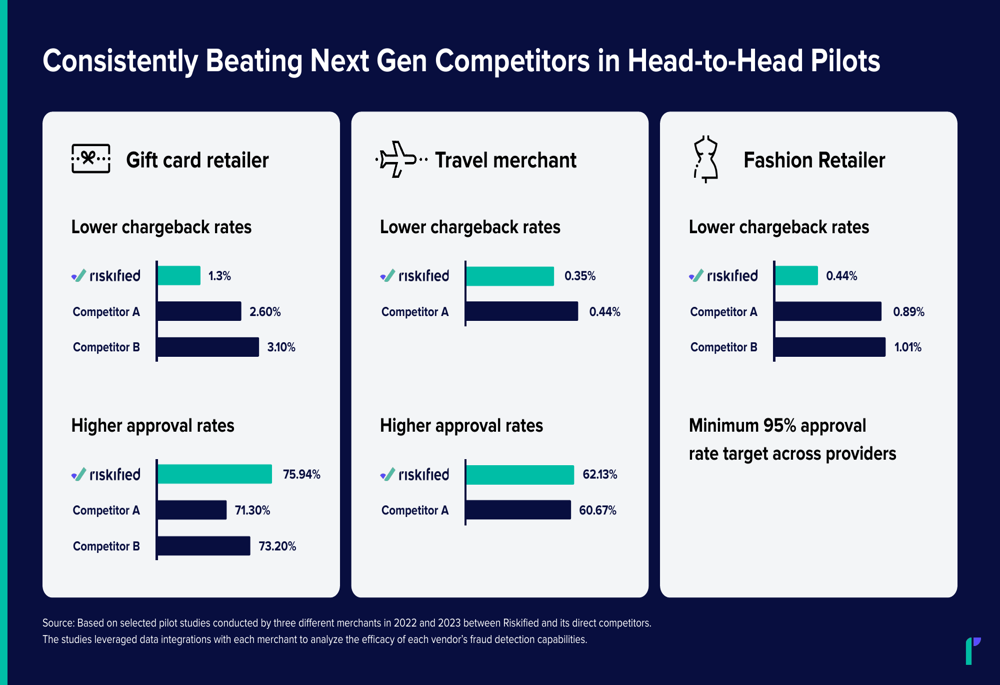

Riskified’s competitive positioning remains strong, with the presentation highlighting superior performance in head-to-head pilots against competitors across various retail sectors:

Forward-Looking Statements

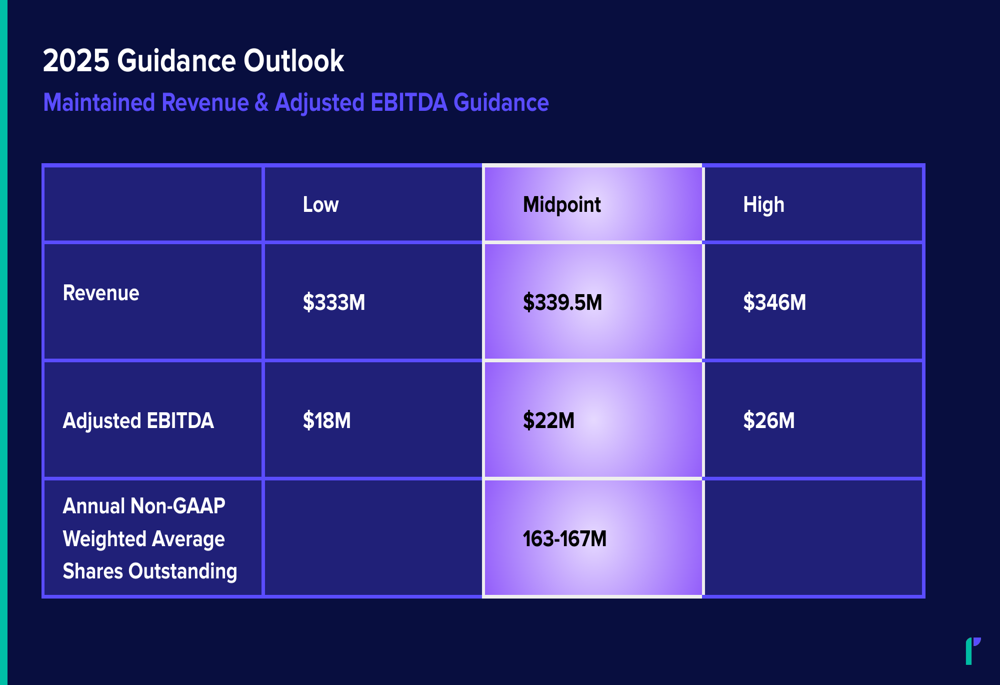

Riskified maintained its full-year 2025 guidance, projecting revenue between $333 million and $346 million, representing growth of approximately 1.7% to 5.6% over 2024. The company expects Adjusted EBITDA between $18 million and $26 million for the year.

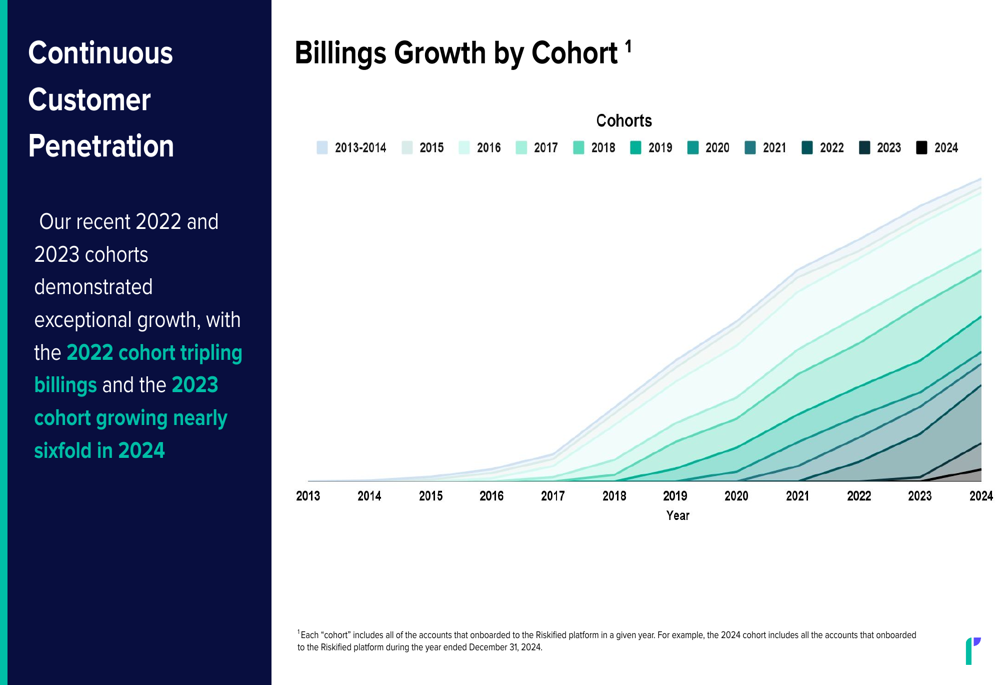

The company’s cohort analysis suggests strong potential for future growth, with recent merchant cohorts showing exceptional performance. The 2022 cohort tripled its billings and the 2023 cohort grew nearly sixfold in 2024:

This cohort performance, combined with the company’s expanding product portfolio and geographic reach, forms the foundation of Riskified’s growth strategy. However, investors should note the tension between revenue growth and margin pressure, as evidenced by the declining gross profit margin in Q1 2025.

Despite beating expectations in its previous quarter with Q4 2024 EPS of $0.06 versus a forecast of -$0.0047, Riskified’s stock has faced pressure. The stock closed at $4.94 on May 13, 2025, well below its 52-week high of $6.645, suggesting that investors remain cautious about the company’s path to consistent profitability despite its revenue growth and strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.