Conservative commentator Charlie Kirk shot and killed at Utah event

Introduction & Market Context

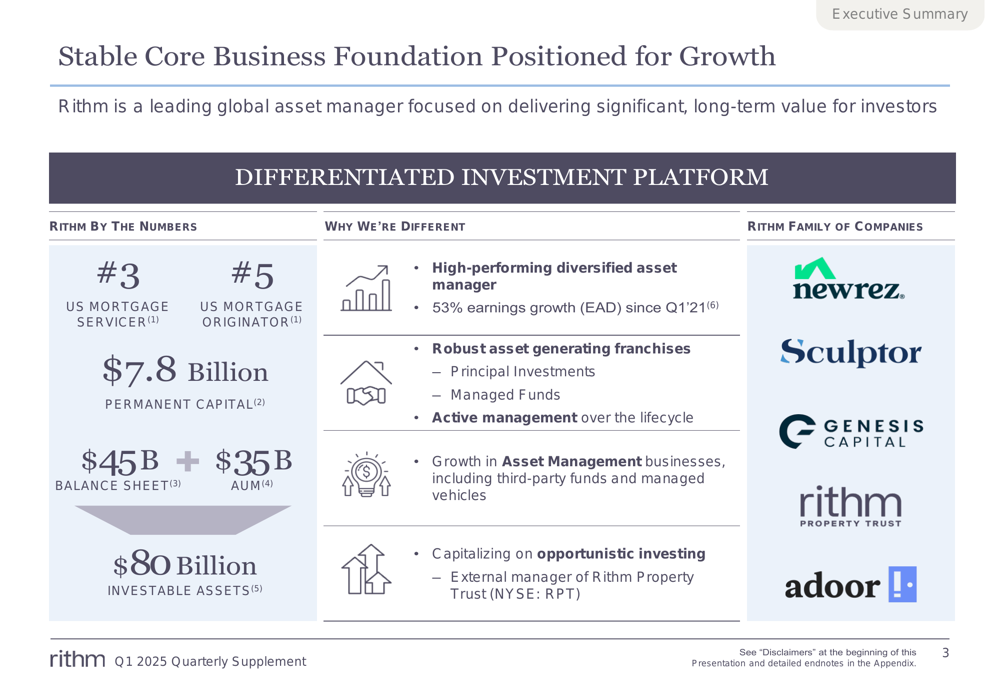

Rithm Capital Corp (NYSE:RITM) released its Q1 2025 quarterly supplement on April 25, highlighting solid performance across its diversified investment platform. The company reported Earnings Available for Distribution (EAD) of $0.52 per share, representing 8% year-over-year growth, while maintaining its position as a leading player in mortgage servicing, origination, and asset management.

The company’s performance comes amid a period of market volatility, with Rithm positioning itself as well-equipped to navigate fluctuating interest rates and economic conditions through its diversified business model. With a current share price of $10.47 in premarket trading, up 0.67% from the previous close, Rithm continues to argue that its market valuation significantly underrepresents its intrinsic value.

As shown in the following overview of Rithm’s business foundation, the company has established itself as a major player in multiple segments of the financial services industry:

Quarterly Performance Highlights

Rithm Capital delivered strong financial results in Q1 2025, reporting GAAP net income of $36.5 million (2% return on equity) and Earnings Available for Distribution of $275.3 million (17% return on equity). The company maintained its quarterly dividend of $0.25 per common share, representing an 8.7% dividend yield at current prices, marking the 22nd consecutive quarter where EAD exceeded common dividends paid.

Book value stood at $6.6 billion ($12.39 per common share), representing a slight decrease from $12.56 per share in Q4 2024. The company maintained a strong liquidity position with $1.9 billion in cash and available liquidity.

The following financial highlights summarize Rithm’s Q1 2025 performance:

Business Segment Analysis

Rithm’s diversified business model continues to drive performance across multiple segments, with particularly strong results in mortgage servicing, residential transitional lending, and asset management.

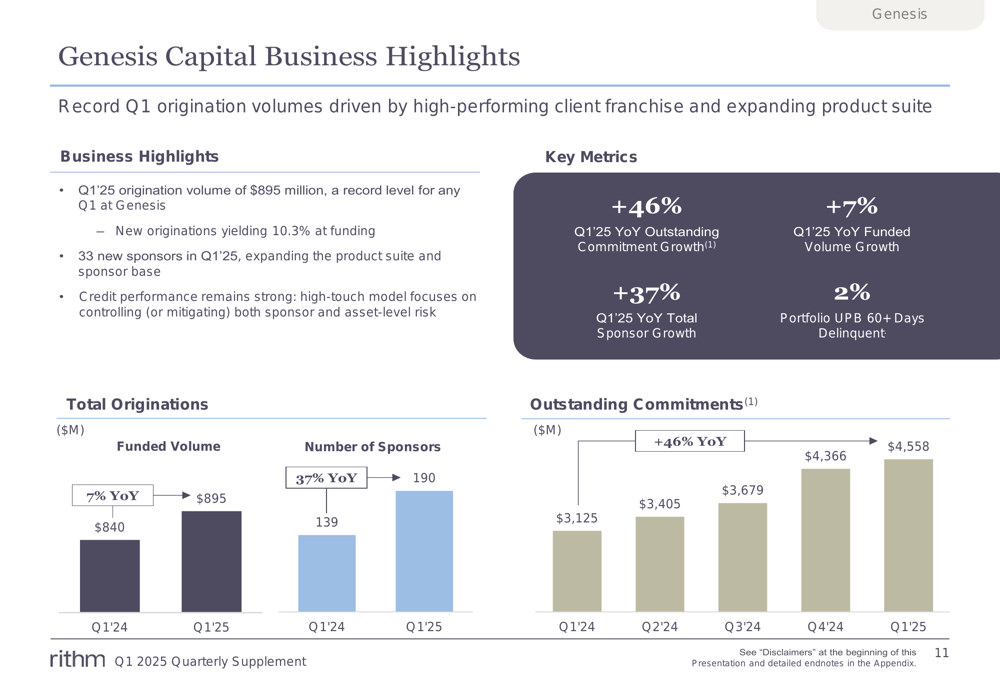

Genesis Capital (Residential Transitional Lending)

Genesis Capital, Rithm’s residential transitional lending platform, achieved record Q1 origination volumes of $895 million, representing a 7% year-over-year increase. The business added 33 new sponsors in Q1 2025 and demonstrated 46% year-over-year growth in outstanding commitments, reaching $4.56 billion. Credit performance remained strong with only 2% of portfolio UPB 60+ days delinquent.

The following chart illustrates Genesis Capital’s growth trajectory:

Asset Management

Rithm’s asset management business, anchored by Sculptor, continued to demonstrate strong fundraising momentum with $1.4 billion of gross inflows in Q1 2025. Sculptor closed on $870 million of commitments for Real Estate Fund V and a new European CLO for $420 million of AUM. Total (EPA:TTEF) assets under management reached $35 billion, with over 70% representing longer-duration assets.

The following highlights showcase Sculptor’s business performance:

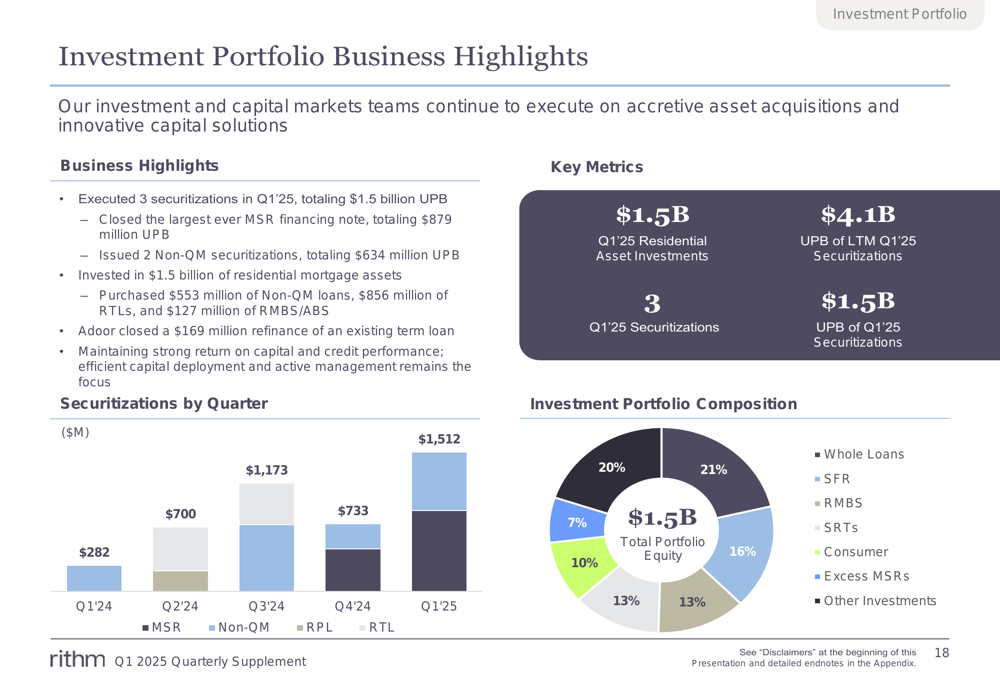

Investment Portfolio

Rithm’s investment and capital markets teams executed three securitizations in Q1 2025, totaling $1.5 billion UPB, including the largest ever MSR financing note at $879 million UPB. The company invested $1.5 billion in residential mortgage assets during the quarter, including $553 million of Non-QM loans, $856 million of residential transitional loans, and $127 million of RMBS/ABS.

The following details the investment portfolio’s performance:

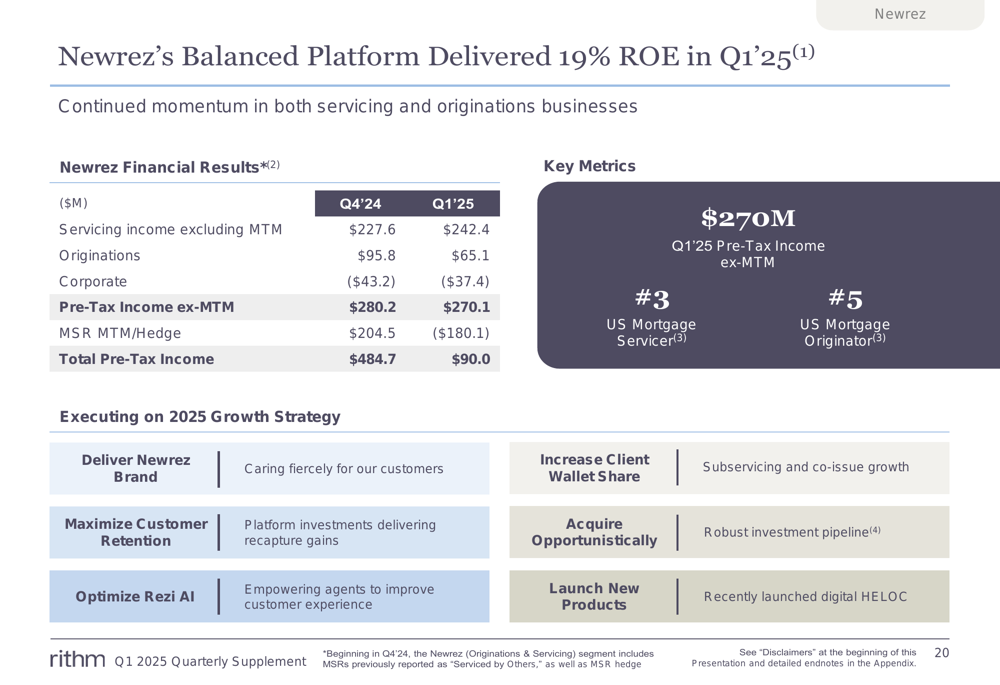

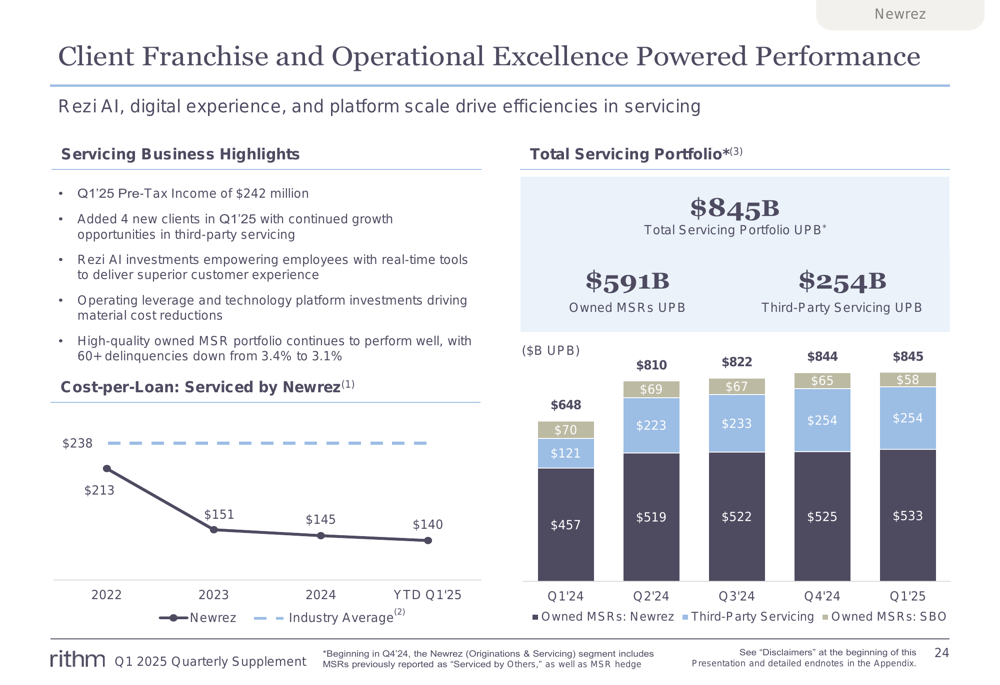

Newrez (Origination & Servicing)

Newrez, Rithm’s mortgage origination and servicing platform, delivered a 19% ROE in Q1 2025, with pre-tax income excluding mark-to-market adjustments of $270 million, up 14% year-over-year. As the #3 US mortgage servicer and #5 US mortgage originator, Newrez managed a servicing portfolio of $845 billion UPB and generated $11.8 billion in funded volume during the quarter.

The following chart illustrates Newrez’s balanced platform performance:

Operational excellence in servicing has driven significant cost efficiencies, with cost-per-loan decreasing from $213 in 2022 to $140 in YTD Q1 2025. The company has also improved its recapture rates, reaching 56% in Q1 2025 compared to 52% in 2024.

Valuation Analysis

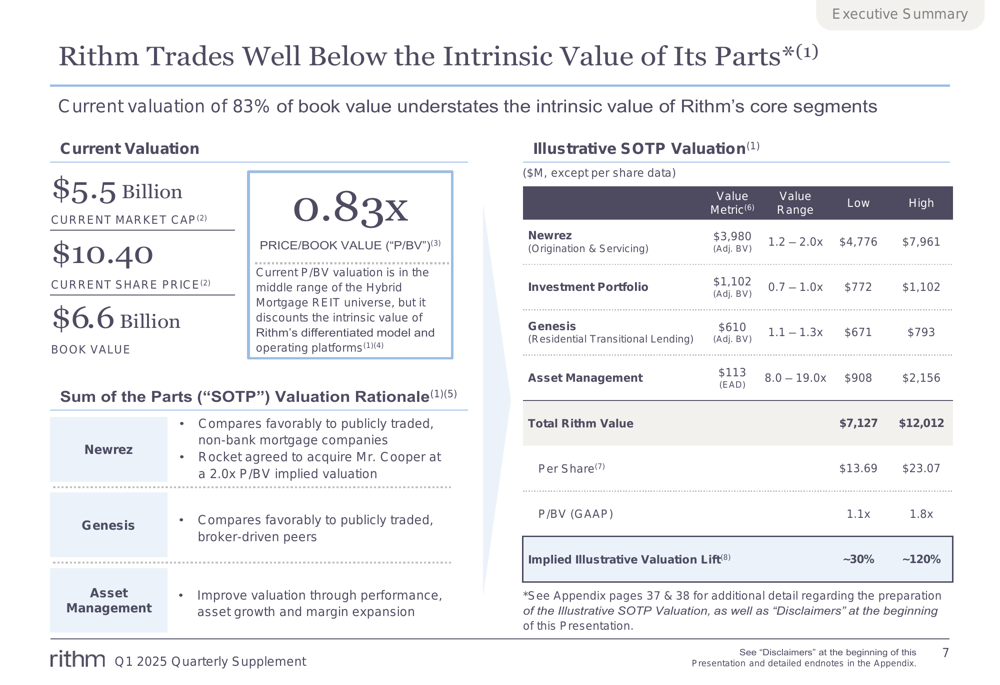

A key focus of Rithm’s presentation was its argument that the company trades significantly below its intrinsic value. With a current market capitalization of $5.5 billion and a share price of $10.40 (as of the presentation date), Rithm trades at 0.83x its book value of $6.6 billion.

Management presented an illustrative sum-of-the-parts valuation suggesting potential upside of 30% to 120%, with an implied per-share value range of $13.69 to $23.07. This analysis values each business segment separately using peer multiples and industry benchmarks.

The following chart details Rithm’s sum-of-the-parts valuation analysis:

Strategic Initiatives

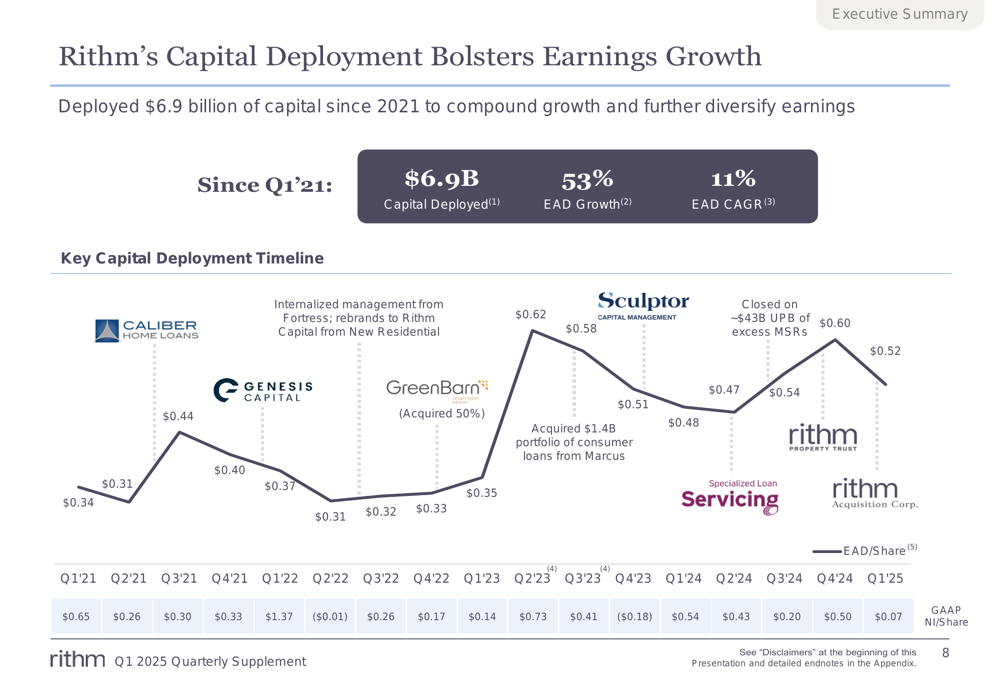

Rithm Capital has deployed $6.9 billion in capital since Q1 2021, resulting in 53% EAD growth (11% CAGR) over that period. Key strategic initiatives have included the acquisitions of Caliber Home Loans, Genesis Capital, and Sculptor, along with the launch of Rithm Property Trust and Rithm Acquisition Corporation.

The following timeline illustrates how these capital deployment initiatives have contributed to earnings growth:

Looking forward, Rithm is focused on:

1. Diversifying capital sources by growing off-balance sheet capital

2. Expanding investment verticals through Rithm Property Trust, Rithm Acquisition Corp., asset-based finance, energy transition, and infrastructure

3. Developing investor partnerships

4. Delivering attractive, risk-adjusted earnings to investors

Forward-Looking Statements

Rithm Capital believes it is well-positioned to execute amid market volatility, highlighting asset-based finance as a haven during economic disruptions due to stable cash flows, tailored asset selection, prudent leverage, and attractive returns.

For Newrez, the company’s 2025 growth strategy focuses on delivering the Newrez brand, increasing client wallet share through subservicing and co-issue growth, maximizing customer retention through platform investments, acquiring opportunistically, optimizing AI capabilities, and launching new products such as its recently launched digital HELOC.

The company continues to see opportunities in residential transitional lending through Genesis Capital, which benefits from bank retrenchment in the sector and maintains a differentiated business model focused on long-term relationships with high-quality sponsors.

Conclusion

Rithm Capital’s Q1 2025 results demonstrate the benefits of its diversified business model, with strong performance across mortgage servicing, origination, asset management, and investment portfolio segments. The 8% year-over-year growth in EAD and 17% return on equity highlight the company’s ability to generate consistent returns despite market volatility.

Management continues to emphasize what it sees as a significant valuation gap, with the stock trading at 0.83x book value despite strong operational performance. With $1.9 billion in cash and liquidity, Rithm remains well-positioned to pursue additional growth opportunities while maintaining its 8.7% dividend yield.

As the company continues to execute on its strategy of diversifying capital sources and expanding investment verticals, investors will be watching to see if the market begins to recognize the value that management believes is embedded in Rithm’s diversified platform.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.