These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Rithm Capital Corp (NYSE:RITM) released its Q2 2025 presentation on July 28, showcasing strong financial performance across its diversified alternative asset management platform. The company reported Earnings Available for Distribution (EAD) of $0.54 per share, representing 15% year-over-year growth, while book value per share increased to $12.71, up 2.6% from $12.39 in the previous quarter.

The company’s stock closed at $12.19 on July 25, 2025, and showed a modest gain of 0.25% in premarket trading on July 28, reaching $12.22. Rithm continues to trade below its book value with a price-to-book ratio of 0.96x, which management argues significantly undervalues the company’s diverse business segments.

As shown in the following overview of Rithm’s business model and key metrics:

Quarterly Performance Highlights

Rithm Capital reported strong financial results for Q2 2025, with GAAP net income of $283.9 million and Earnings Available for Distribution of $291.1 million ($0.54 per share). The company maintained its quarterly dividend of $0.25 per share, representing an 8.9% dividend yield based on the current share price. Notably, this marks the 23rd consecutive quarter where EAD exceeded common dividends paid, demonstrating the sustainability of Rithm’s dividend policy.

The company’s book value increased to $6.7 billion ($12.71 per share), while maintaining a strong liquidity position with $2.1 billion in cash. Return on equity remained robust at 17-18%, reflecting the company’s efficient capital allocation across its diverse business segments.

The following slide highlights Rithm’s key financial metrics for Q2 2025:

Detailed Financial Analysis

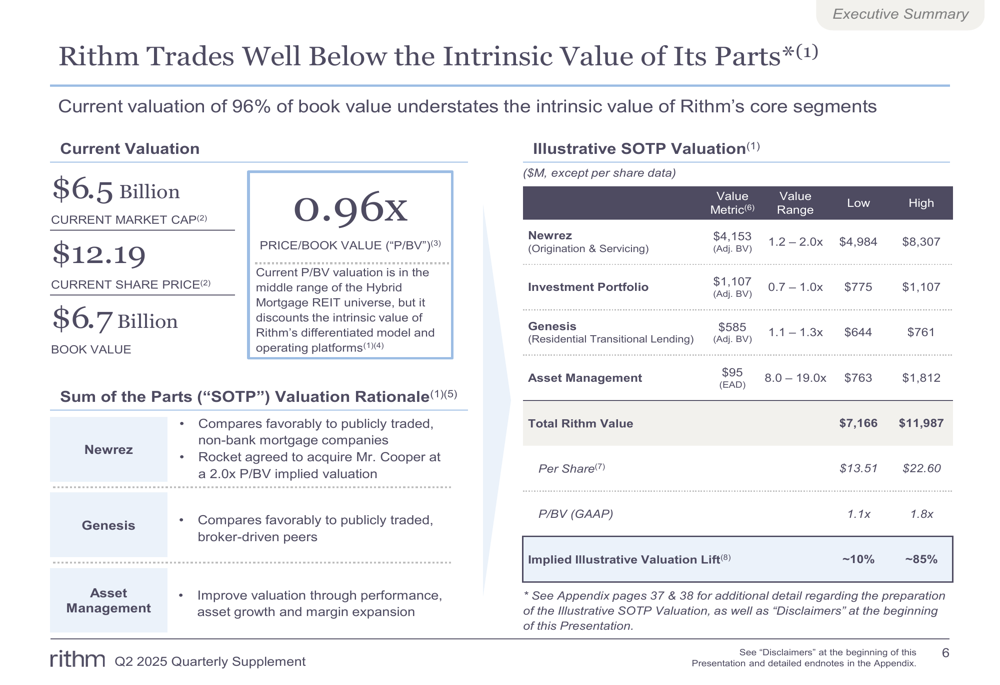

Rithm Capital’s presentation emphasized that the company trades below the intrinsic value of its parts, with a current market capitalization of $6.5 billion representing just 96% of its book value. Management presented a Sum of the Parts (SOTP) valuation suggesting that Rithm’s true value could be between $7.2 billion and $12.0 billion, or $13.51 to $22.60 per share, implying a potential valuation uplift of approximately 10% to 85%.

This valuation breakdown assigns different multiples to each of Rithm’s business segments:

- Newrez (mortgage origination and servicing): 1.2-2.0x multiple

- Investment Portfolio: 0.7-1.0x multiple

- Genesis (residential transitional lending): 1.1-1.3x multiple

- Asset Management: 8.0-19.0x multiple

The following slide details Rithm’s SOTP valuation analysis:

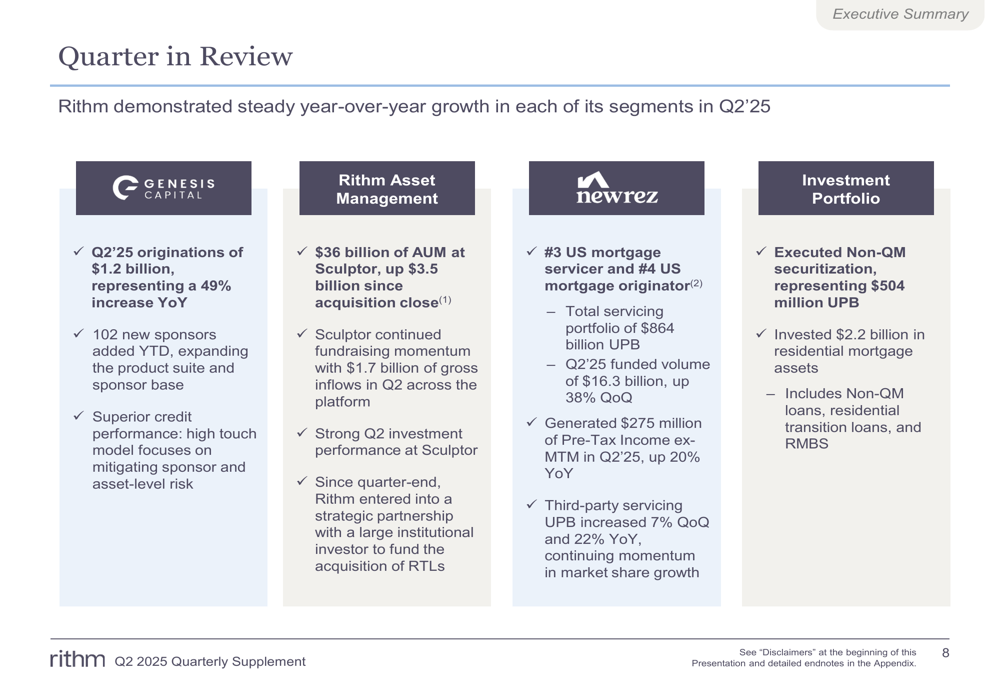

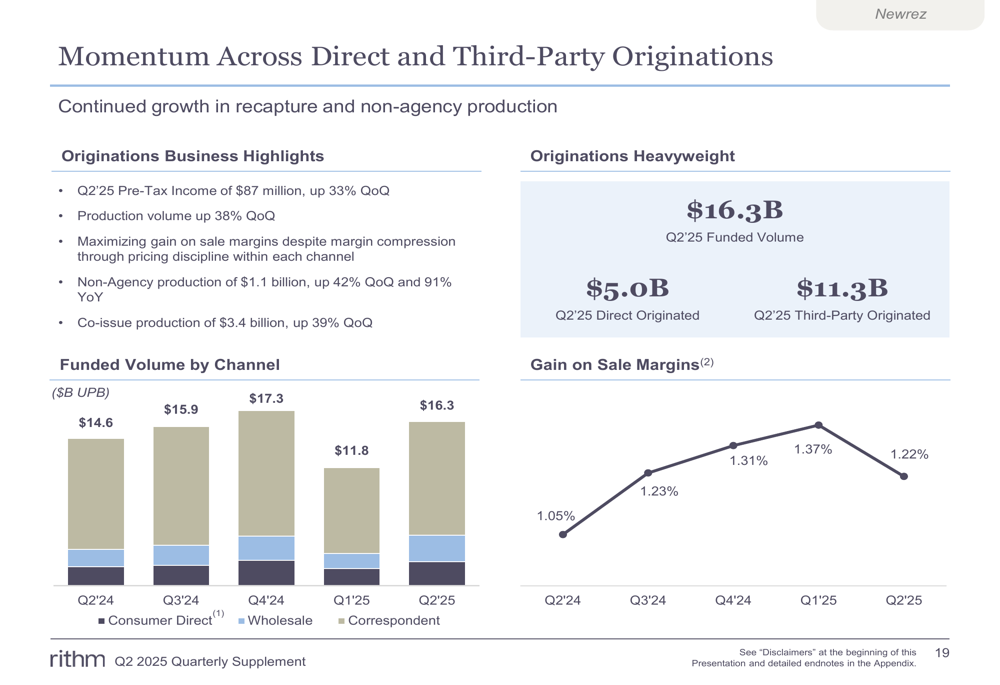

Across its business segments, Rithm demonstrated strong performance in Q2 2025. Genesis Capital achieved record origination volume of $1.2 billion, up 49% year-over-year, while adding 102 new sponsors. Rithm Asset Management reported $36 billion in AUM at Sculptor, with $1.7 billion of gross inflows during the quarter. Newrez maintained its position as the #3 US mortgage servicer and #4 US mortgage originator, with a servicing portfolio of $864 billion UPB and funded volume of $16.3 billion (up 38% quarter-over-quarter).

The following slide summarizes the quarter’s performance across Rithm’s key business segments:

Strategic Initiatives

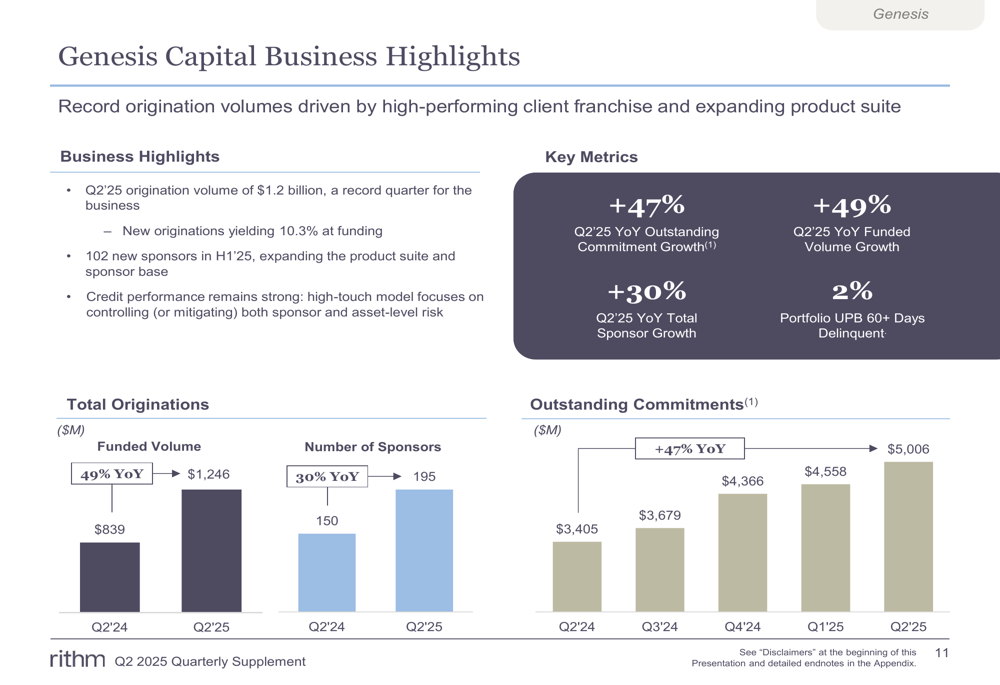

Genesis Capital, Rithm’s residential transitional lending business, showed particularly strong growth in Q2 2025. The company achieved record origination volume of $1.2 billion, representing a 49% increase year-over-year. Genesis also added 102 new sponsors during the quarter, a 30% increase compared to the same period last year. Management attributed this growth to bank retrenchment creating opportunities in the residential transitional lending market.

The following slide highlights Genesis Capital’s business performance:

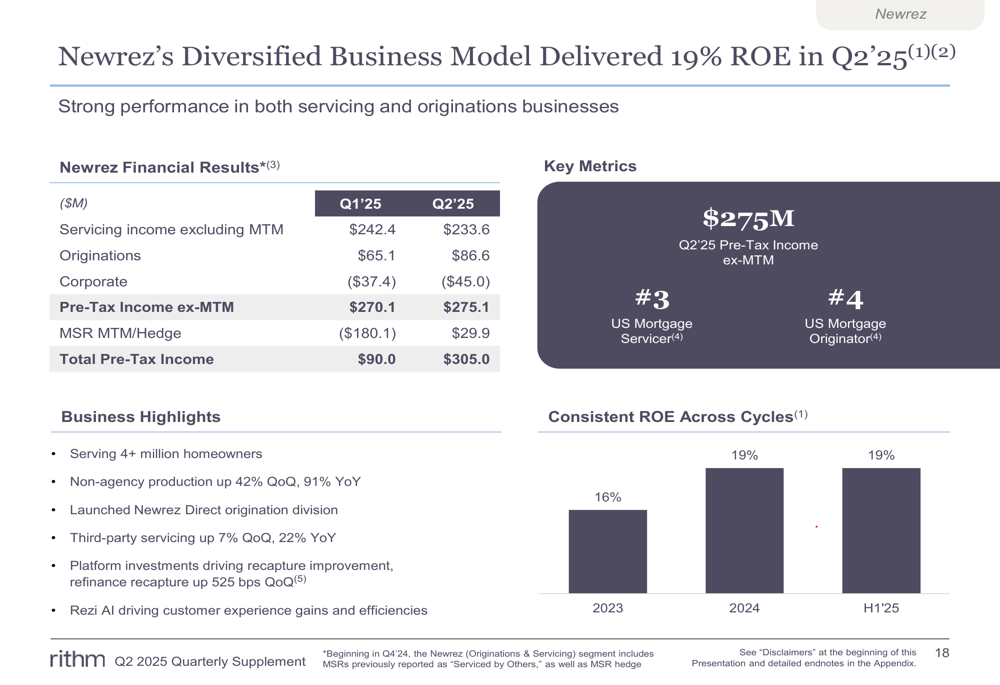

Newrez, Rithm’s mortgage origination and servicing business, delivered a 19% return on equity in Q2 2025. The segment reported pre-tax income excluding mark-to-market adjustments of $275 million, with strong contributions from both servicing ($233.6 million) and origination ($86.6 million). Newrez’s diversified business model has enabled it to maintain consistent returns across different market cycles.

The following slide details Newrez’s financial performance:

Newrez also demonstrated strong momentum in both direct and third-party originations, with Q2 2025 pre-tax income of $87 million, up 33% quarter-over-quarter. Production volume increased 38% quarter-over-quarter, with non-agency production of $1.1 billion (up 42% QoQ and 91% YoY) and co-issue production of $3.4 billion (up 39% QoQ).

The following slide shows Newrez’s origination performance:

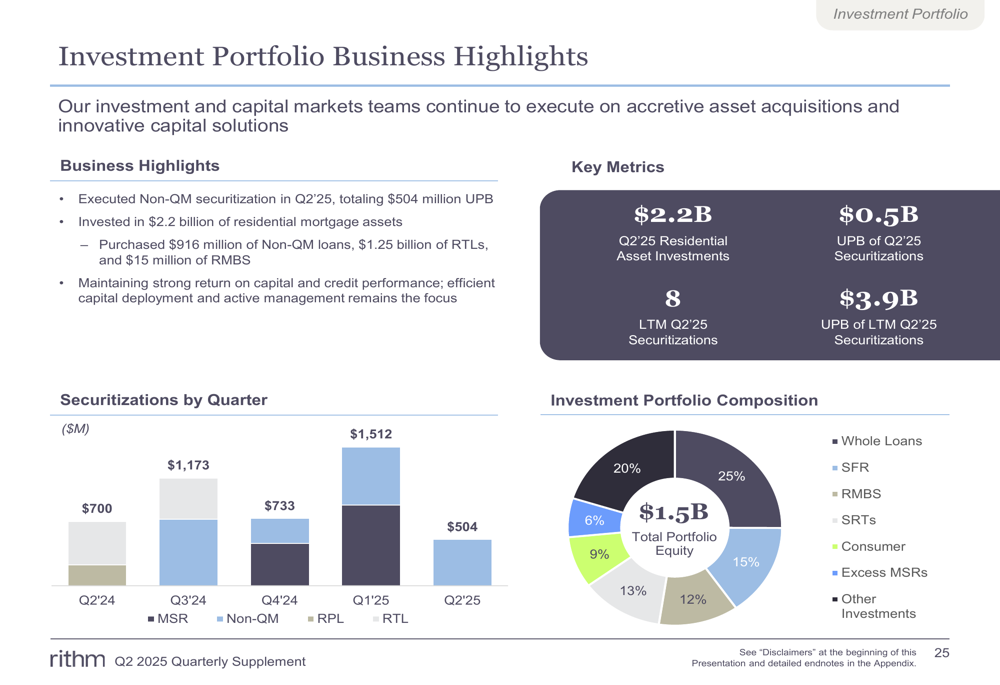

Rithm’s investment portfolio continued to execute on accretive asset acquisitions and innovative capital solutions. During Q2 2025, the company invested $2.2 billion in residential mortgage assets and executed a non-QM securitization of $504 million UPB. The investment portfolio remains diversified across various asset classes, including whole loans, single-family rentals, RMBS, and consumer loans.

The following slide presents the investment portfolio’s composition and highlights:

Forward-Looking Statements

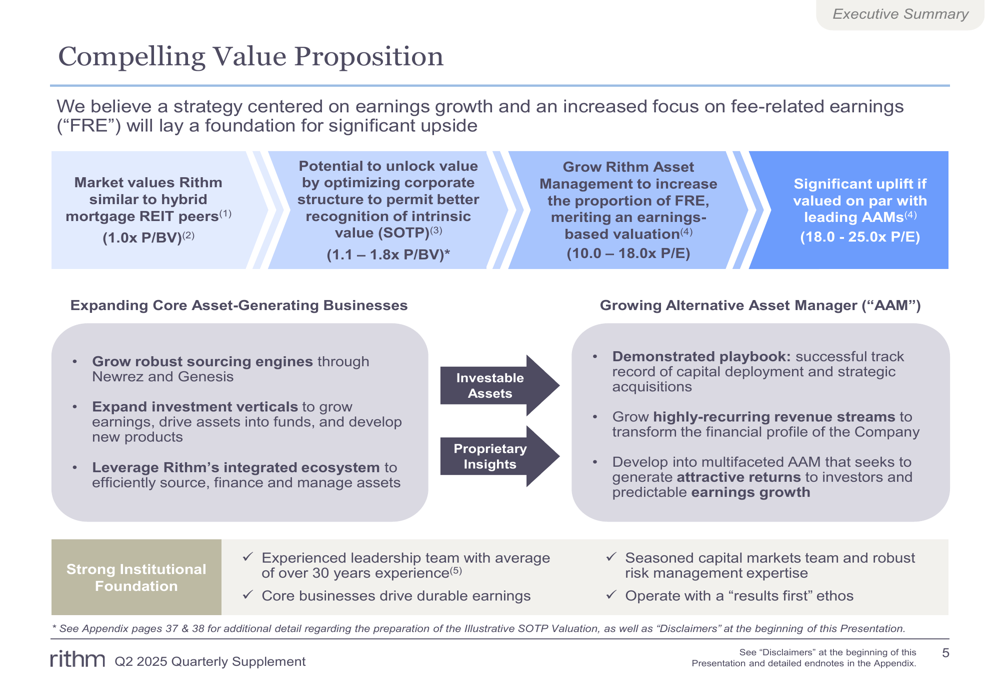

Rithm Capital’s presentation outlined its value proposition centered on earnings growth and an increased focus on fee-related earnings. The company is pursuing several strategies to unlock shareholder value, including:

1. Growing core asset-generating businesses (Newrez and Genesis)

2. Expanding as an alternative asset manager

3. Optimizing corporate structure to unlock value through a Sum of the Parts approach

Management believes that Rithm could achieve valuations similar to hybrid mortgage REIT peers (1.0x P/BV) or potentially higher through its SOTP value (1.1-1.8x P/BV). The company’s asset management business could command valuations of 10.0-18.0x P/E, compared to leading alternative asset managers valued at 18.0-25.0x P/E.

The following slide illustrates Rithm’s value proposition:

Rithm Capital’s Q2 2025 presentation demonstrates continued momentum across all business segments, building on the positive trends reported in Q1 2025. The company’s EAD growth of 15% year-over-year and book value increase to $12.71 per share reflect strong operational execution and effective capital allocation. With a diversified business model spanning mortgage servicing, origination, residential transitional lending, and asset management, Rithm appears well-positioned to continue delivering value to shareholders while trading at a discount to its book value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.