JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Roche Holding AG (SIX:ROG) presented its half-year 2025 results on July 24, showing continued growth momentum despite currency headwinds and challenges in its diagnostics division. The Swiss pharmaceutical giant reported 7% sales growth at constant exchange rates (CER), primarily driven by its pharmaceutical division’s strong 10% growth, while diagnostics remained flat due to healthcare pricing reforms in China.

The results build upon the positive trend reported in Q1 2025, when the company announced 6% group sales growth and 8% pharmaceutical sales growth. Roche’s stock has remained relatively stable amid mixed market conditions, with the company maintaining its full-year guidance despite projected currency impacts.

Quarterly Performance Highlights

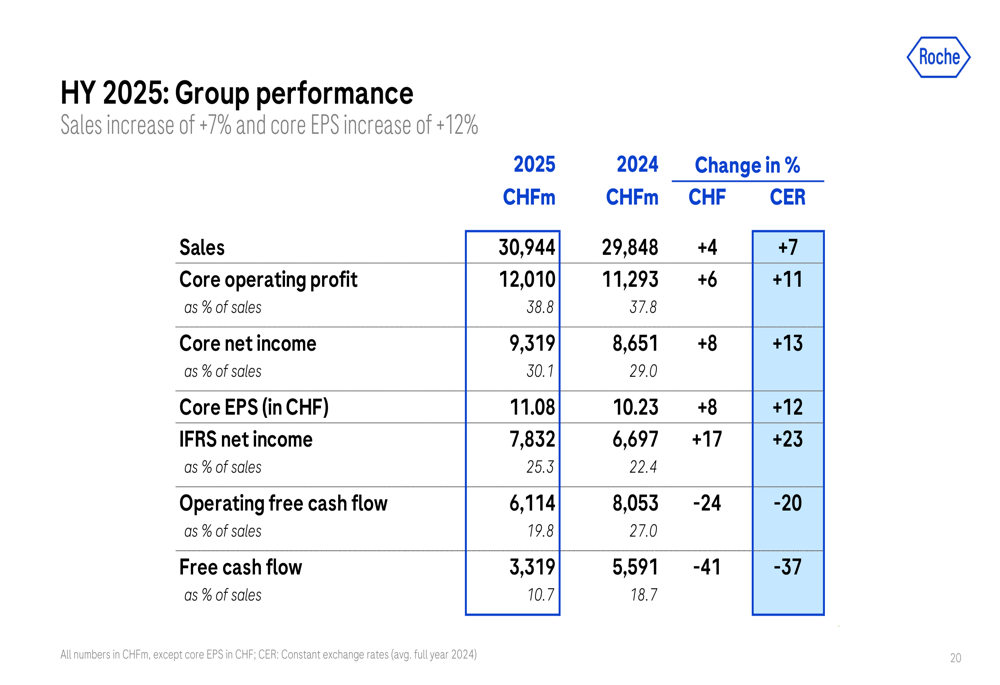

Roche reported strong financial performance for the first half of 2025, with group sales reaching CHF 30.9 billion, representing a 7% increase at CER and 4% in Swiss francs. Core operating profit rose by 11% at CER to CHF 12.0 billion, with the core operating profit margin improving by 1.1 percentage points to 38.8% of sales.

As shown in the following comprehensive financial overview, core earnings per share (EPS) increased by 12% at CER to CHF 11.08, while IFRS net income grew by 23% at CER:

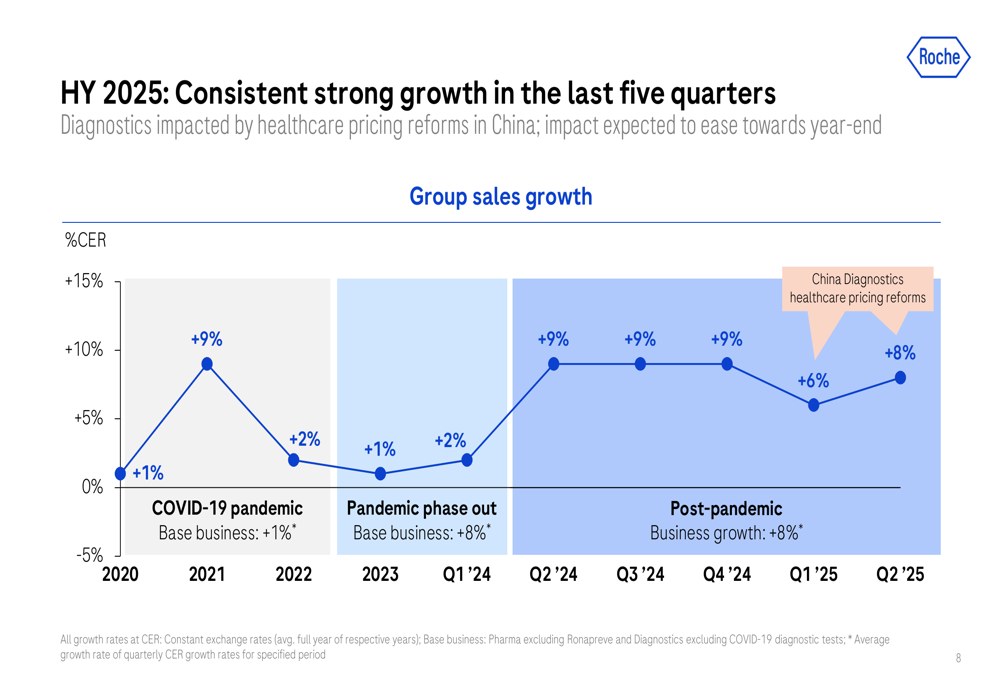

The company’s performance was driven by consistent growth over the past five quarters, demonstrating resilience in the post-pandemic environment. This chart illustrates Roche’s steady growth trajectory:

Divisional Performance

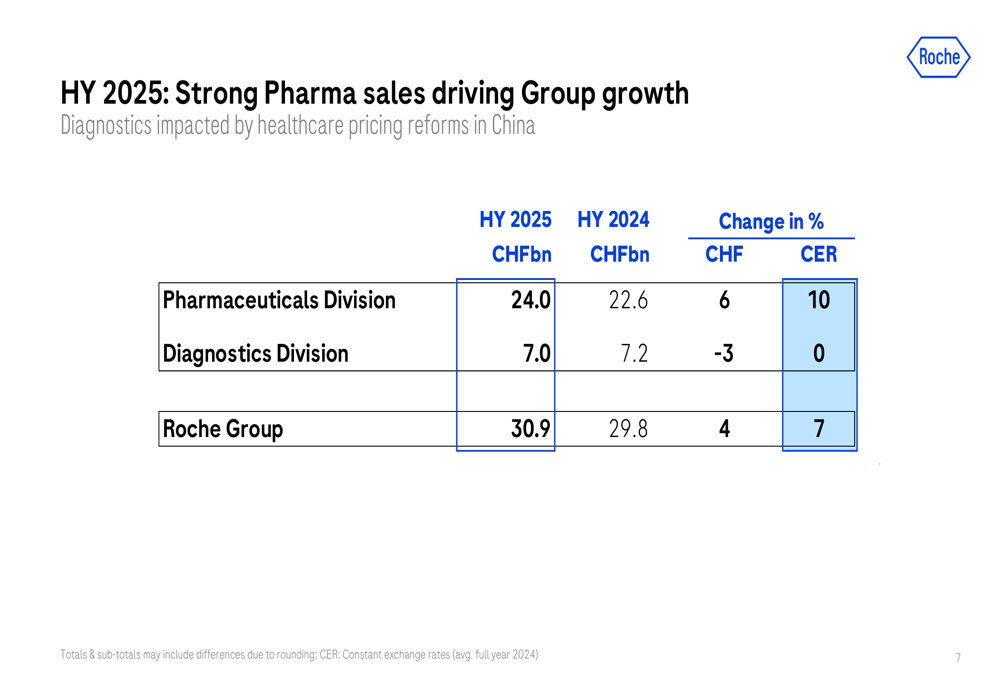

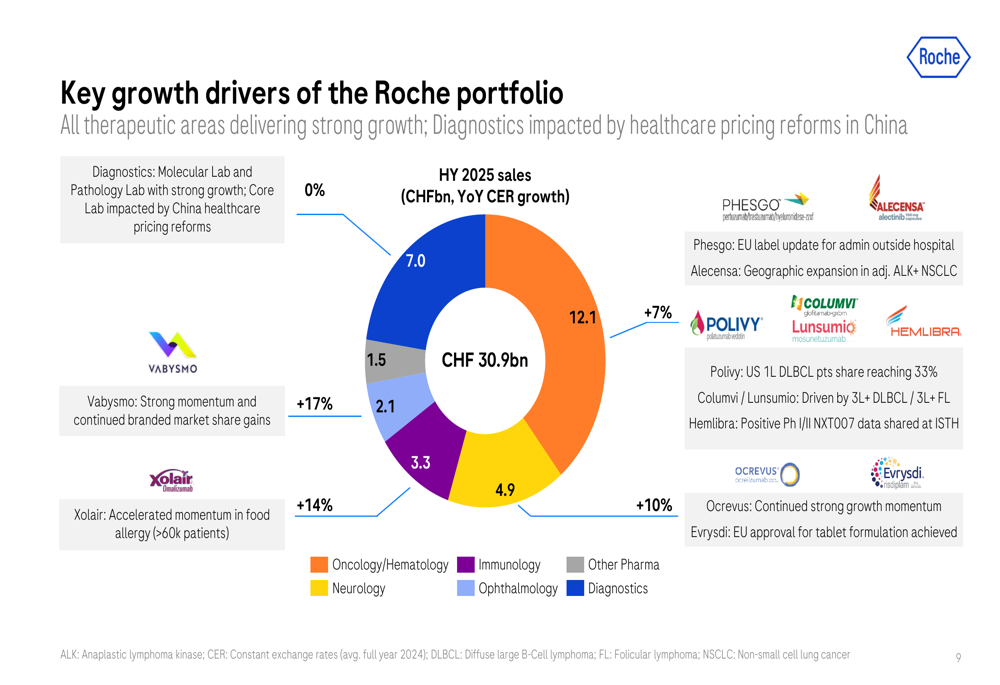

The pharmaceutical division was the primary growth driver, with sales of CHF 24.0 billion representing a 10% increase at CER. Meanwhile, the diagnostics division, with sales of CHF 7.0 billion, remained flat at CER due to the impact of healthcare pricing reforms in China.

The following breakdown shows the contribution of each division to overall group sales:

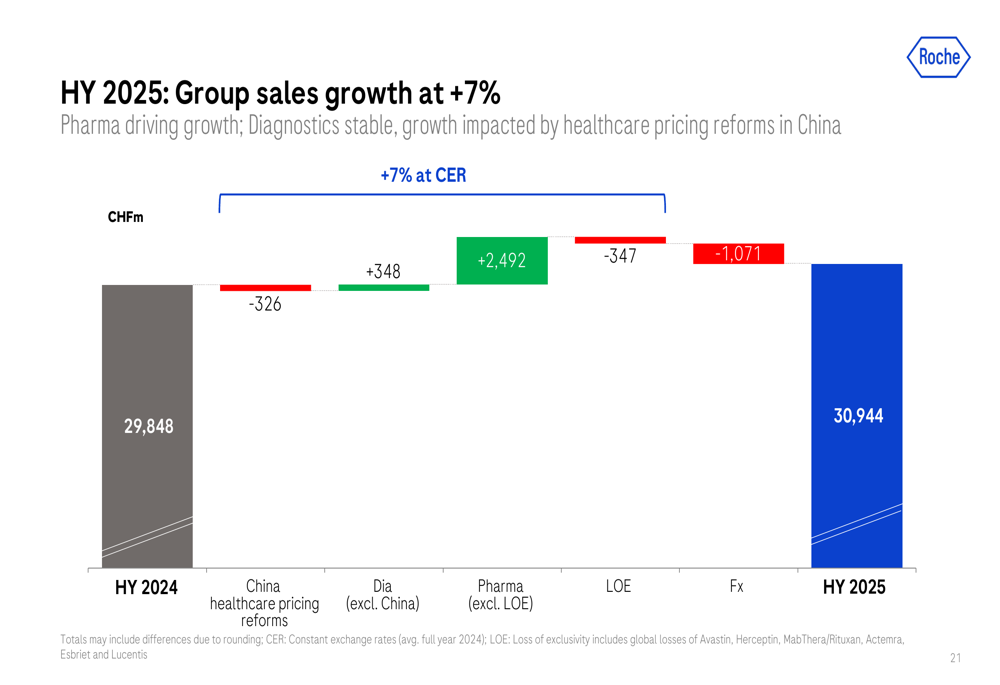

A detailed analysis of the sales growth drivers reveals that while the pharmaceutical division (excluding Loss of Exclusivity impacts) contributed CHF 2,492 million to growth, this was partially offset by China healthcare pricing reforms (-CHF 326 million) and currency effects (-CHF 1,071 million):

The company’s portfolio is well-diversified across therapeutic areas, with all segments except diagnostics showing strong growth. As illustrated in this breakdown, ophthalmology (+10%), neurology (+14%), and oncology/hematology (+17%) were particularly strong performers:

Pipeline and R&D Strategy

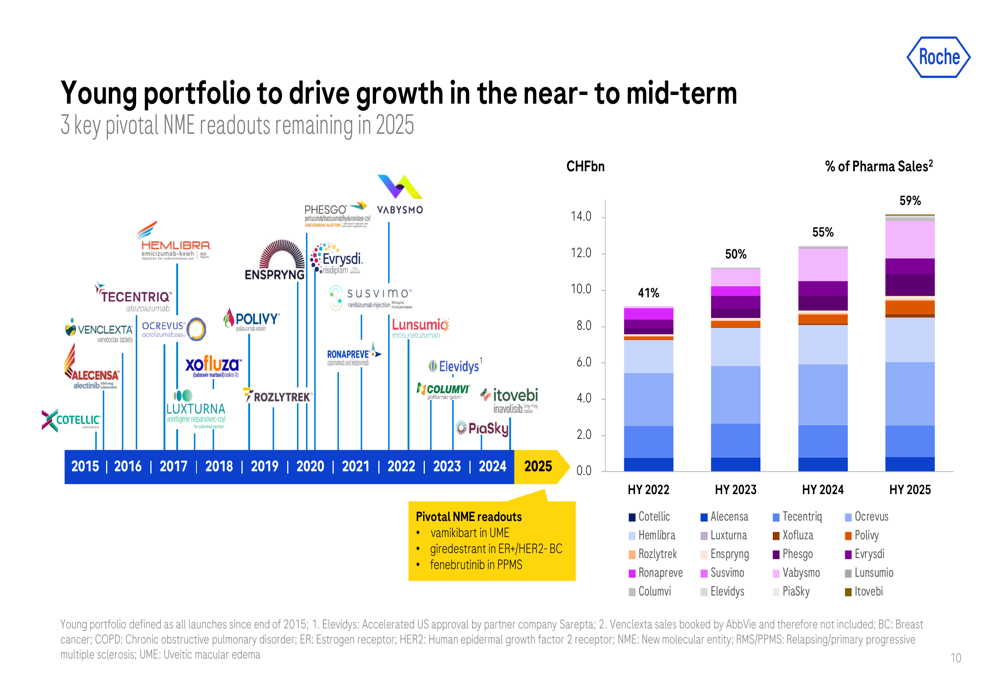

A key highlight of Roche’s presentation was the increasing contribution of its young portfolio (products launched since the end of 2015) to overall pharmaceutical sales. This segment now represents 59% of pharma sales, up from 41% in HY 2022, demonstrating the company’s successful pipeline progression and commercial execution:

Roche is also enhancing its R&D productivity through strategic resource reallocation. The company is redirecting approximately CHF 1 billion to transformative programs and productivity initiatives, which has already resulted in accelerated development timelines for key assets and an increase in high-value assets.

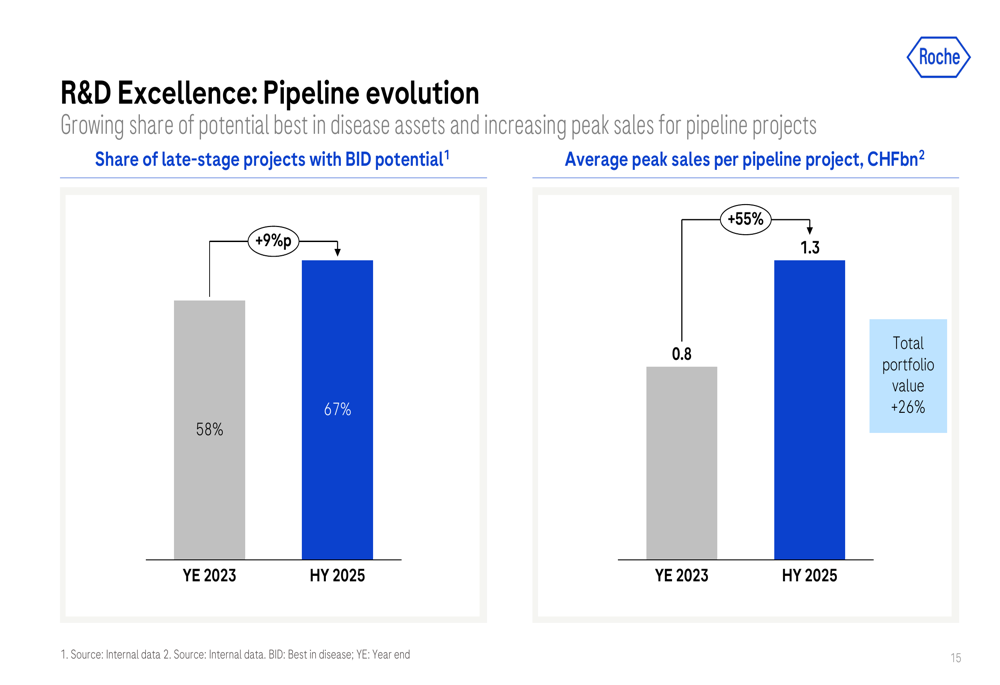

The pipeline evolution shows promising trends, with the share of late-stage projects with best-in-disease potential increasing from 58% at the end of 2023 to 67% in HY 2025. Additionally, the average peak sales per pipeline project has risen by 55% to CHF 1.3 billion:

Financial Position and Cash Flow

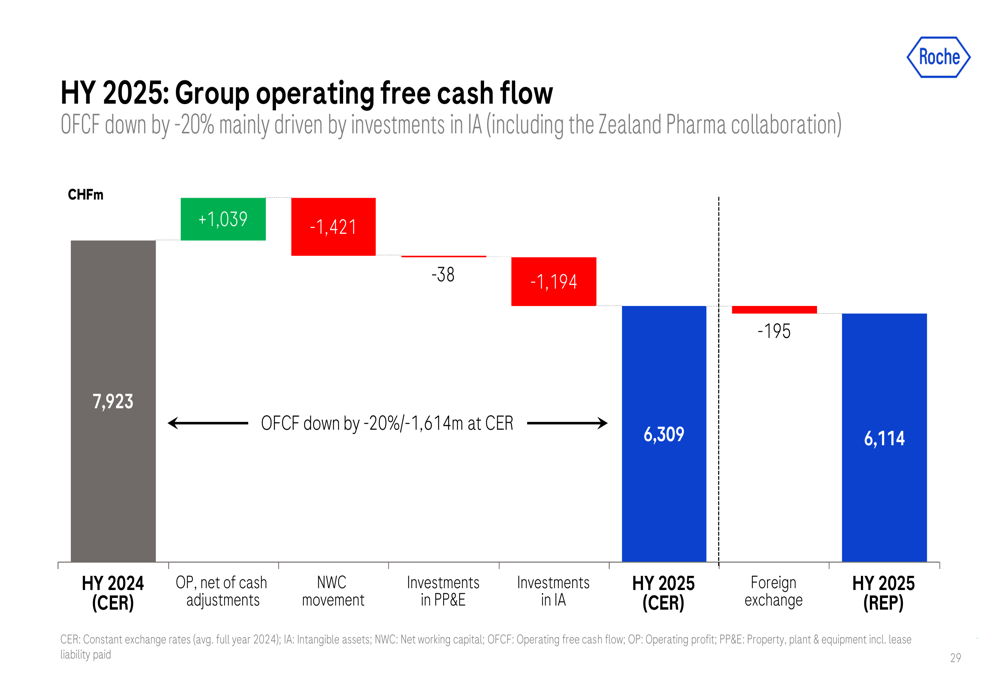

While Roche’s sales and profit growth were strong, operating free cash flow decreased by 20% at CER to CHF 6.1 billion, representing 19.8% of sales compared to 27.0% in the previous year. This decline was primarily due to working capital movements and increased investments in intangible assets:

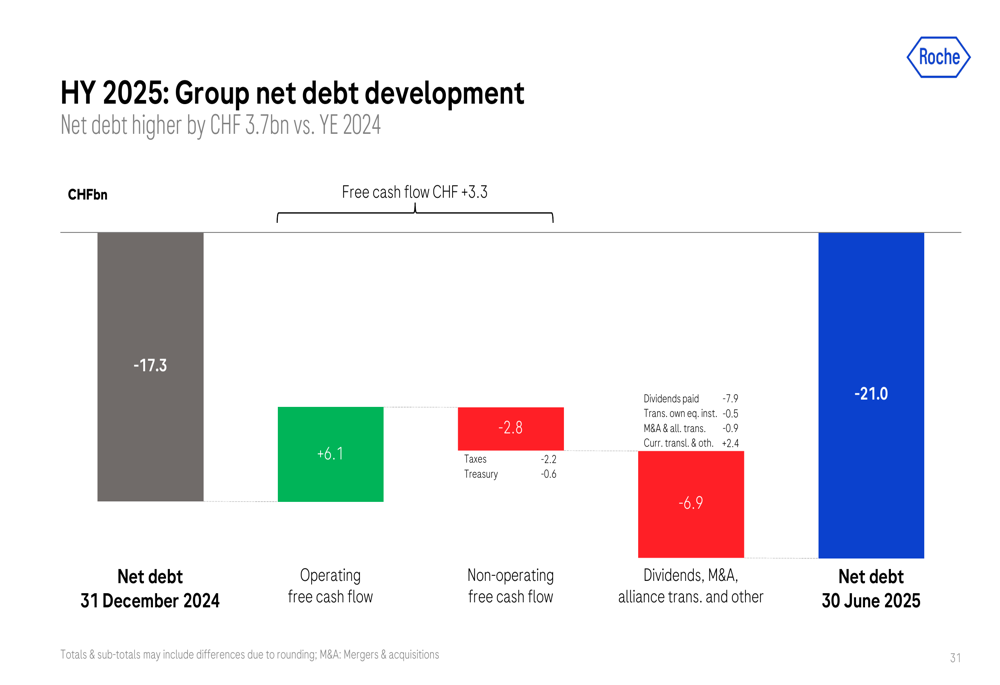

The company’s net debt increased by CHF 3.7 billion compared to year-end 2024, reaching CHF 21.0 billion as of June 30, 2025. This increase was primarily driven by dividend payments, M&A activities, and alliance transactions:

Forward-Looking Statements

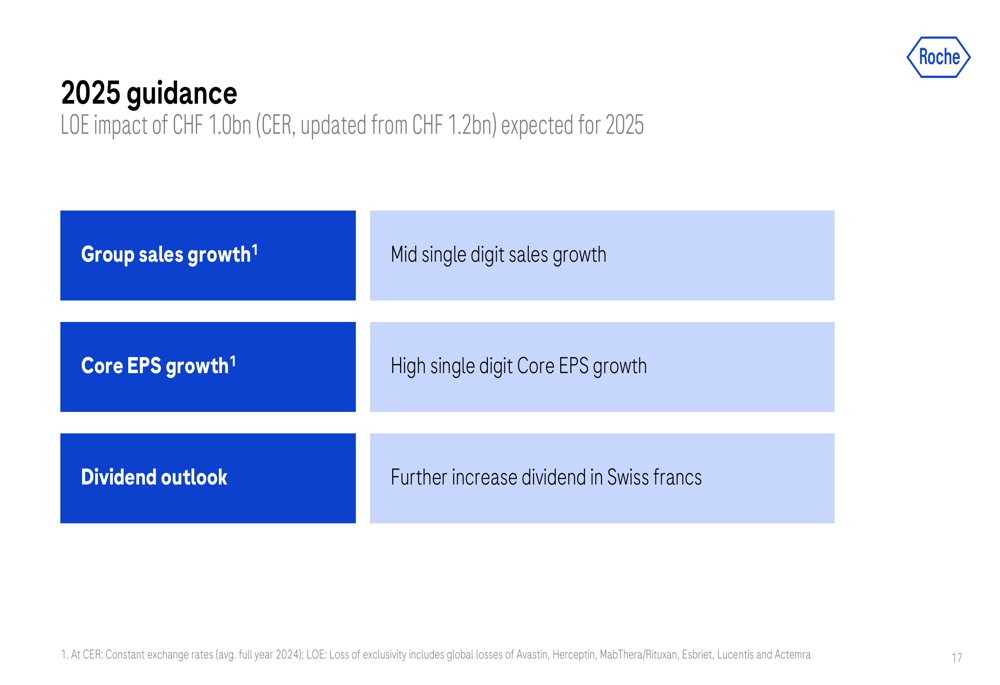

Despite currency headwinds, Roche maintained its full-year 2025 guidance, expecting mid-single-digit sales growth and high-single-digit core EPS growth at constant exchange rates. The company also plans to further increase its dividend in Swiss francs.

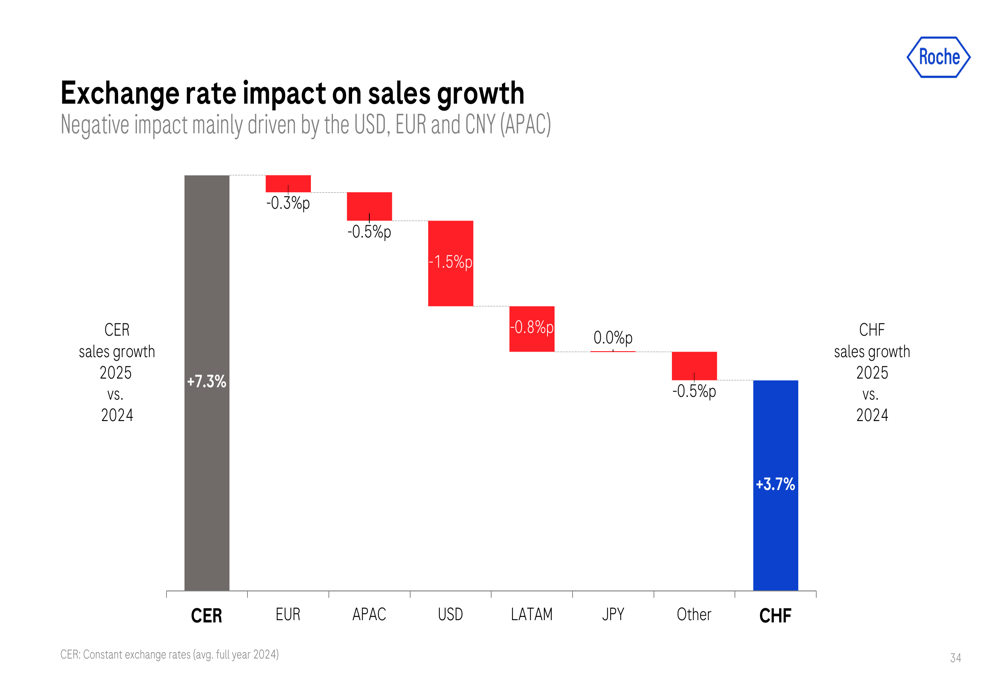

Currency fluctuations are expected to have a negative impact on reported results, with the USD, EUR, and currencies in the Asia-Pacific region being the main contributors to this effect:

CEO Thomas Schinecker expressed confidence in the company’s strategy during the Q1 earnings call, stating, "We will deliver," emphasizing the disciplined and swift implementation of Roche’s strategic initiatives. The company continues to invest in its future, with plans to invest $50 billion in US R&D and manufacturing by the end of the decade.

Roche’s pipeline remains robust, with several pivotal Phase III readouts expected in the remainder of 2025, including giredestrant in breast cancer, fenebrutinib in primary progressive multiple sclerosis, and vamikibart in uveitic macular edema. These potential new treatments, along with the company’s evolving diagnostics portfolio, position Roche to maintain growth momentum despite ongoing challenges in certain markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.