Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

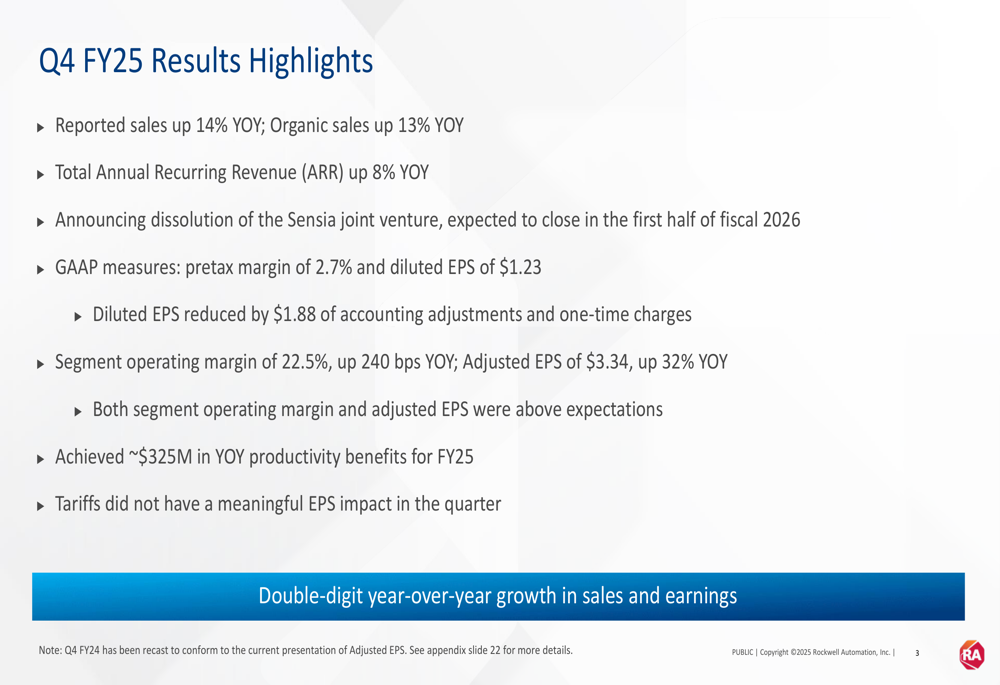

Rockwell Automation Inc (NYSE:ROK) reported strong fourth-quarter results for fiscal year 2025, with double-digit growth in both sales and earnings. The industrial automation company's shares jumped 6.21% in pre-market trading following the November 6 announcement, reflecting investor optimism about the company's performance and outlook.

The company's Q4 results significantly exceeded analyst expectations, with adjusted earnings per share of $3.34 compared to the forecasted $2.94, representing a 13.61% beat. Revenue also surpassed expectations at $2.32 billion versus the projected $2.21 billion, demonstrating Rockwell's resilience in a challenging economic environment.

Quarterly Performance Highlights

Rockwell reported Q4 fiscal 2025 sales of $2.32 billion, up 14% year-over-year, with organic sales growth of 13%. The quarter's segment operating margin reached 22.5%, a substantial improvement of 240 basis points compared to the same period last year.

As shown in the following comprehensive overview of Rockwell's quarterly performance:

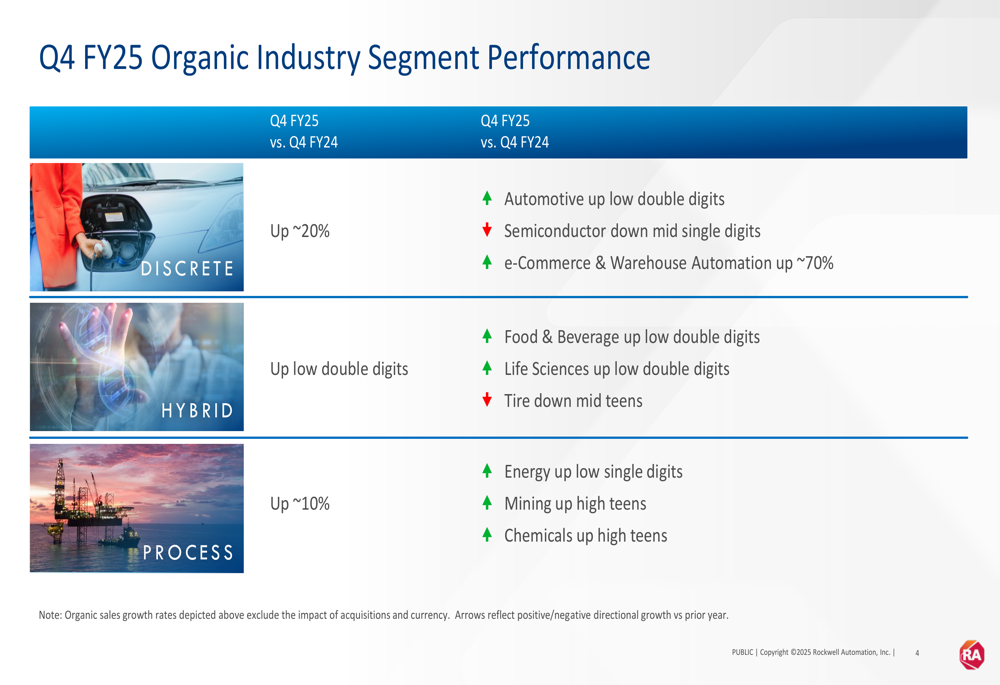

The company's performance varied significantly across industry segments. The Discrete segment showed the strongest growth at approximately 20%, driven by a remarkable 70% increase in e-Commerce & Warehouse Automation. The Hybrid and Process segments also performed well, with growth rates of low double digits and approximately 10%, respectively.

The following chart breaks down the organic industry segment performance for Q4 FY25:

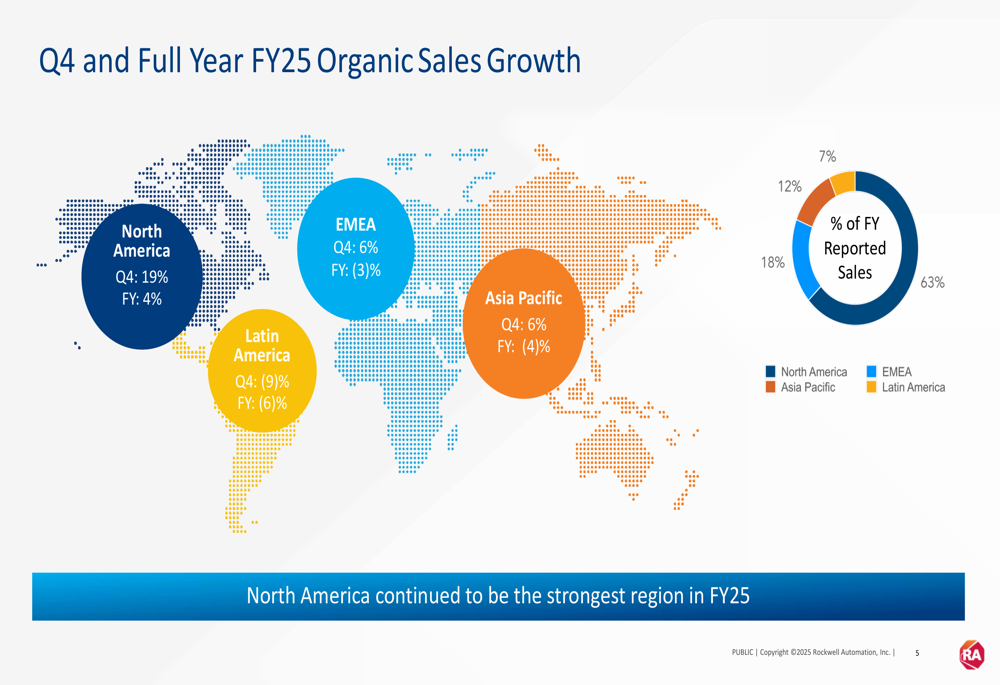

Geographically, North America continued to be Rockwell's strongest region, with Q4 organic sales growth of 19%, while other regions showed more modest growth. The company's full-year regional performance reveals the challenges faced in international markets, with Latin America, EMEA, and Asia Pacific all showing negative growth for the full year despite positive Q4 results.

Segment Results Analysis

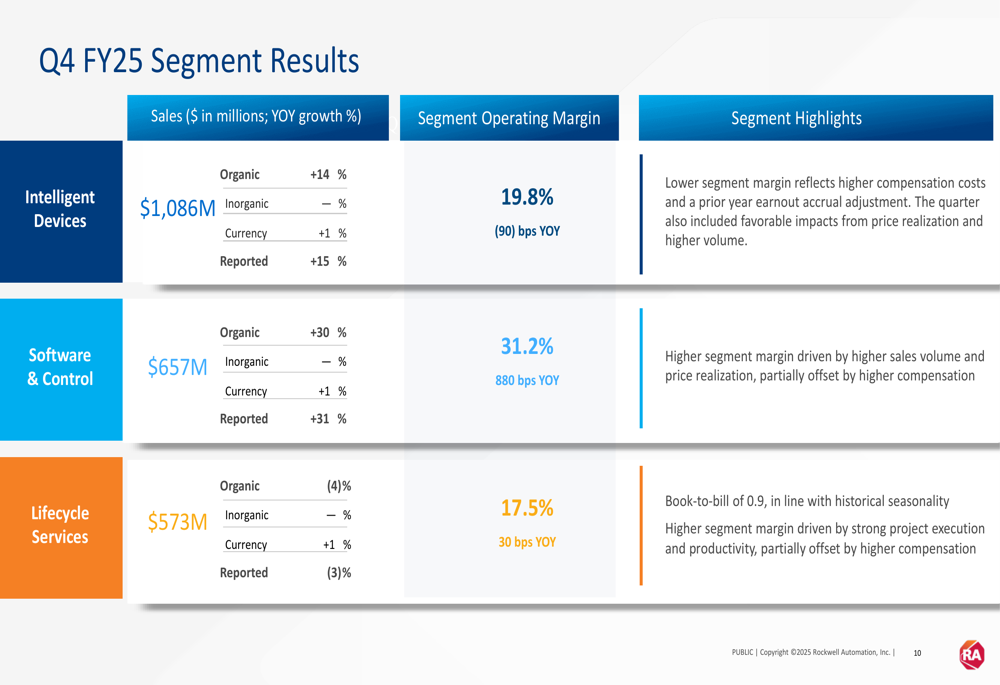

Rockwell's performance varied significantly across its three business segments. The Software & Control segment was the standout performer, with organic sales growth of 30% and an impressive segment operating margin of 31.2%, up 880 basis points year-over-year. This exceptional performance was driven by higher sales volume and price realization.

The Intelligent Devices segment also performed strongly with organic sales growth of 14%, though its operating margin declined slightly by 90 basis points to 19.8%, primarily due to higher compensation costs. The Lifecycle Services segment faced challenges with organic sales declining by 4%, though its operating margin improved slightly by 30 basis points to 17.5%.

The following breakdown illustrates the performance of each segment:

Strategic Initiatives

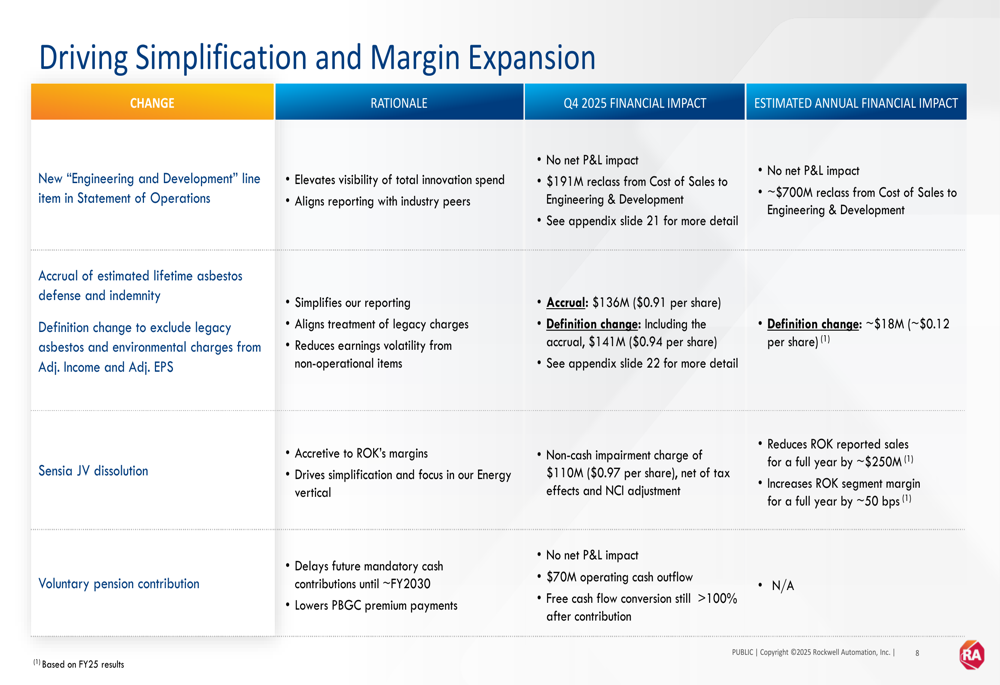

Rockwell outlined several strategic initiatives aimed at driving simplification and margin expansion. These include the dissolution of the Sensia joint venture, which is expected to close in the first half of fiscal 2026 and increase Rockwell's segment margin by approximately 50 basis points on a full-year basis.

The company is also implementing accounting changes, including a new "Engineering and Development" line item in its Statement of Operations to better align with industry peers and provide greater visibility into innovation spending. Additionally, Rockwell has made a voluntary pension contribution to delay future mandatory cash contributions until approximately fiscal 2030.

As shown in the following detailed breakdown of these strategic initiatives:

Detailed Financial Analysis

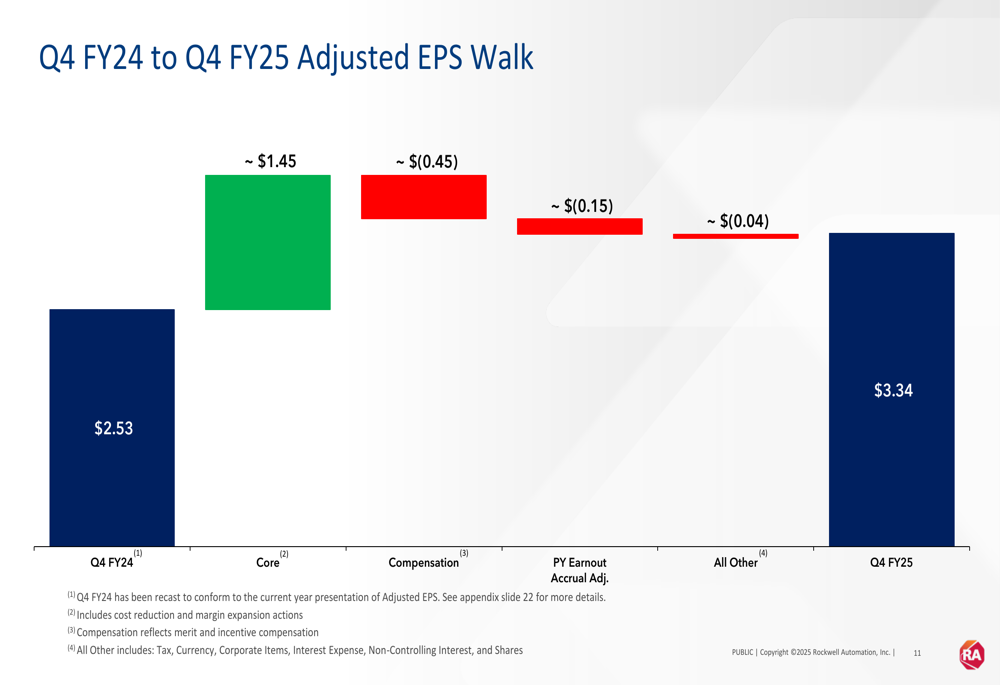

Rockwell's adjusted EPS for Q4 FY25 increased by 32% year-over-year to $3.34. This improvement was primarily driven by core business performance, which contributed approximately $1.45 to the EPS growth, partially offset by higher compensation costs of approximately $0.45.

The following waterfall chart illustrates the key factors contributing to the EPS growth:

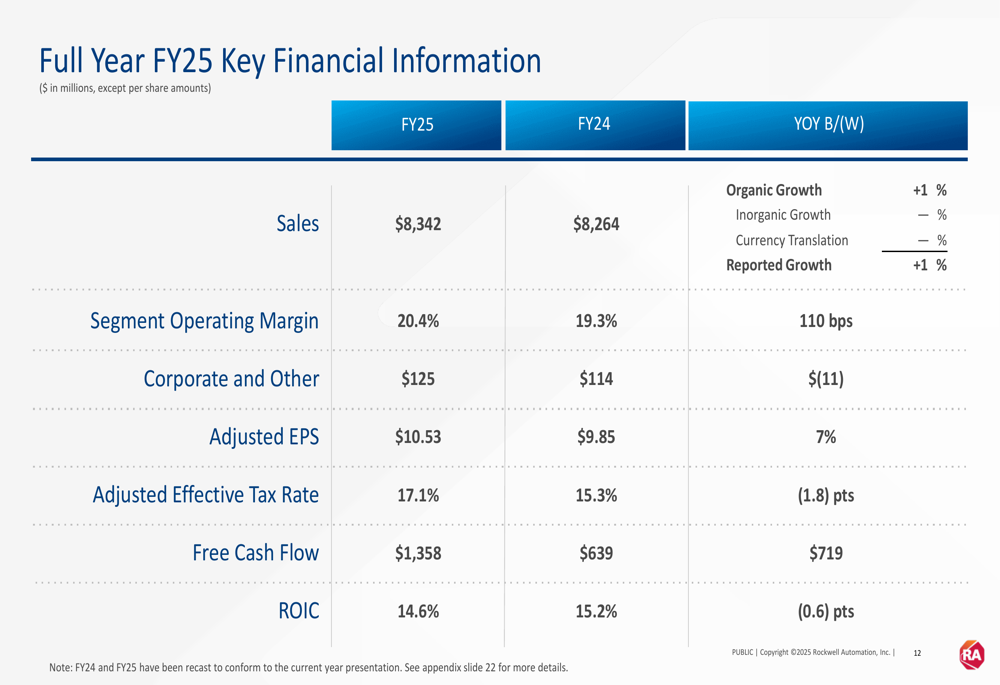

For the full fiscal year 2025, Rockwell achieved reported and organic sales growth of 1% year-over-year, with segment operating margin improving by 110 basis points to 20.4%. The company's adjusted EPS for the full year increased by 7% to $10.53, and free cash flow conversion was strong at approximately 114%.

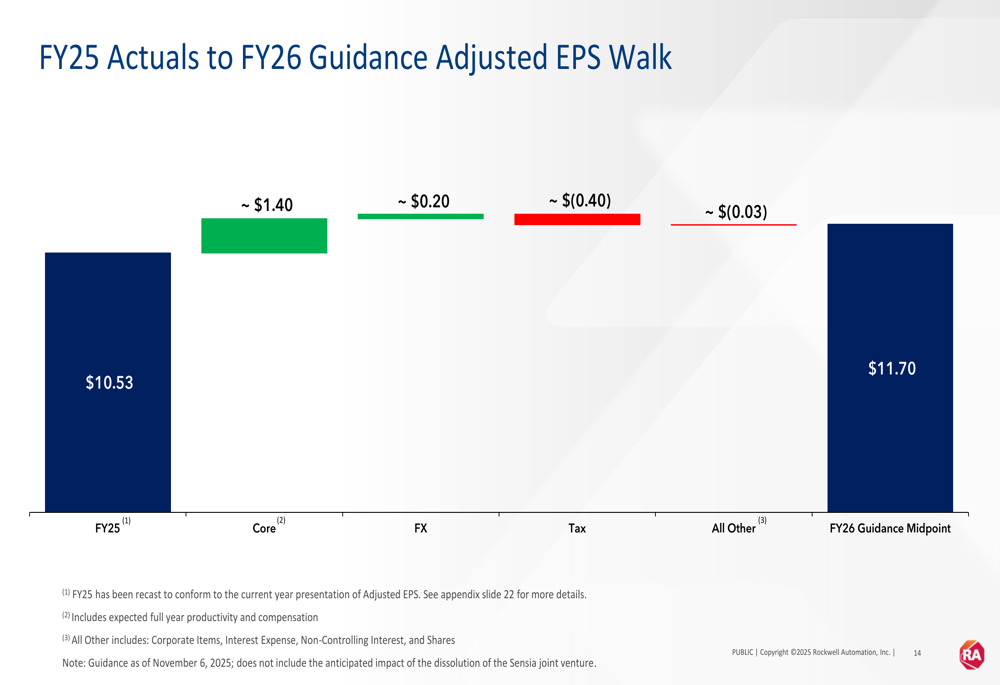

Looking ahead to fiscal 2026, Rockwell expects adjusted EPS to increase by approximately 10% at the midpoint to a range of $11.20 to $12.20. This growth will be driven primarily by core business performance, contributing approximately $1.40, and favorable foreign exchange impact of approximately $0.20, partially offset by higher tax rates.

Forward-Looking Statements

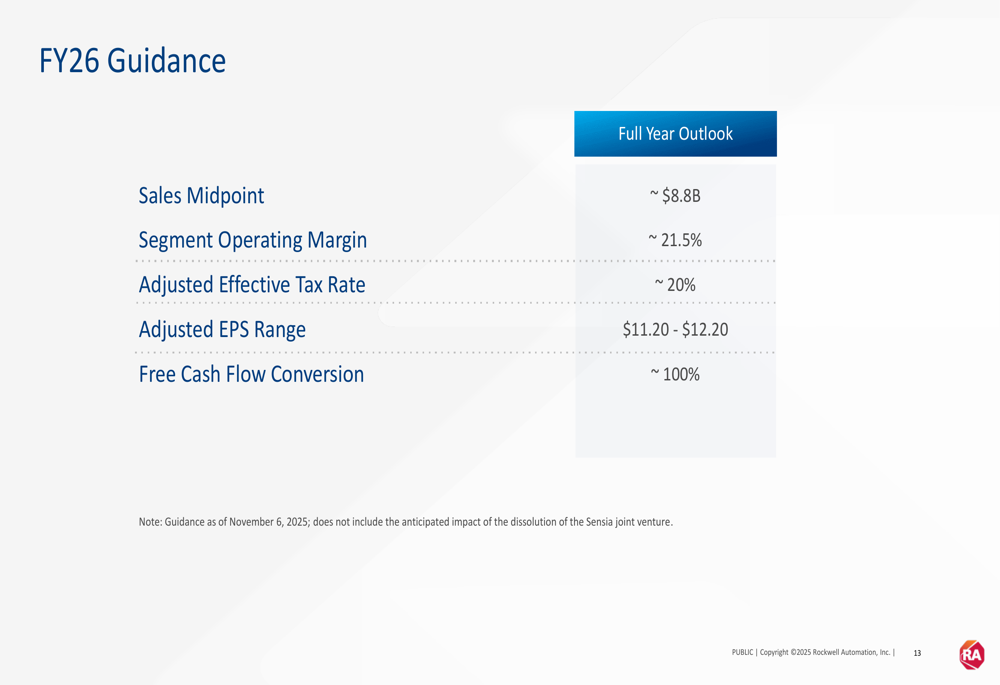

For fiscal year 2026, Rockwell provided an optimistic outlook with total reported sales growth projected between 3% and 7%, and organic sales growth between 2% and 6%. The company expects segment operating margin to improve to approximately 21.5% and adjusted EPS to range from $11.20 to $12.20, representing approximately 10% growth at the midpoint.

The following slide details Rockwell's guidance for fiscal 2026:

By industry segment, Rockwell anticipates growth across all three of its major segments in fiscal 2026. The Discrete segment is expected to grow mid-single digits, with e-Commerce & Warehouse Automation continuing its strong performance with projected growth of approximately 10%. The Hybrid segment is also forecast to grow mid-single digits, with all sub-segments showing positive growth. The Process segment is expected to return to growth with a low-single-digit increase after declining in fiscal 2025.

CEO Blake Moret expressed confidence in the company's position, stating, "Rockwell is well positioned for sustained market-beating growth and profitability." The company plans to share more details about its long-term strategy at its upcoming Investor Day scheduled for November 18-19, 2025, in Chicago.

In conclusion, Rockwell Automation's Q4 and full-year fiscal 2025 results demonstrate the company's ability to execute effectively in a challenging environment. With strategic initiatives focused on simplification and margin expansion, combined with continued growth in high-value areas like software and e-commerce, Rockwell appears well-positioned to deliver on its fiscal 2026 guidance and create value for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.