Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Rogers Communications Inc (NYSE:RCI) reported solid financial results for the second quarter of 2025, with growth across all business segments and a significant improvement in free cash flow. The company presented its quarterly performance on July 23, 2025, highlighting consistent revenue growth and strategic acquisitions while raising its full-year guidance.

Quarterly Performance Highlights

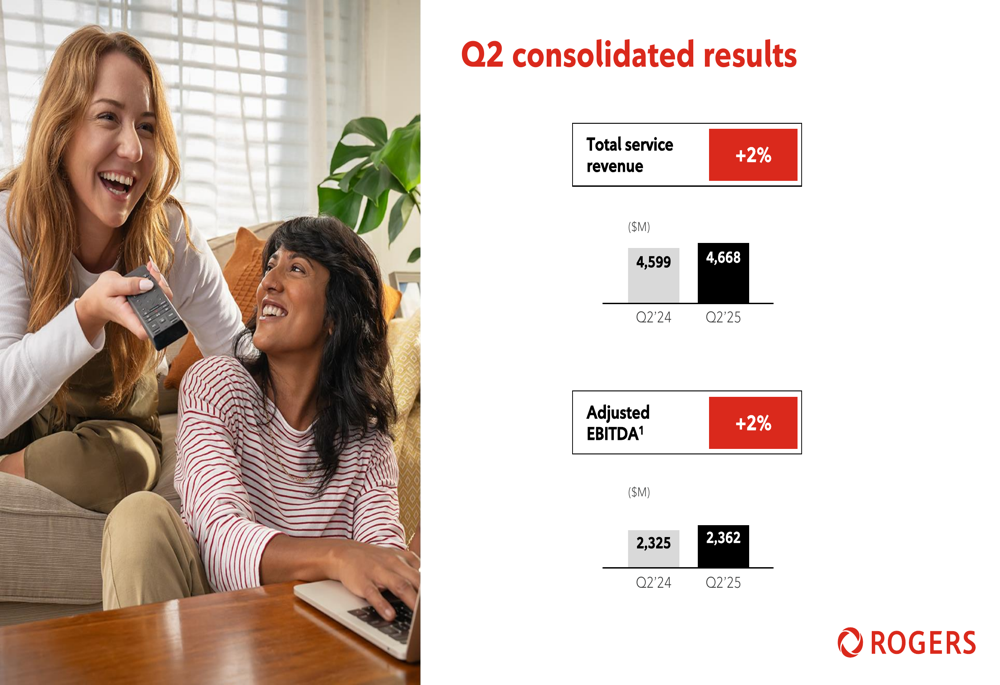

Rogers delivered strong results in a competitive market environment, with total service revenue increasing by 2% year-over-year to $4,668 million and adjusted EBITDA also growing by 2% to $2,362 million. The company added 61,000 mobile phone subscribers and 26,000 retail internet subscribers during the quarter.

As shown in the following consolidated results chart, Rogers maintained consistent growth in its core financial metrics:

Free cash flow was a particular bright spot, surging 39% year-over-year to $925 million, driven by stronger operational performance and reduced capital expenditures. The company also highlighted its improved balance sheet management, with the debt leverage ratio improving to 3.6x, nearly a full turn better since the beginning of the year.

Detailed Financial Analysis

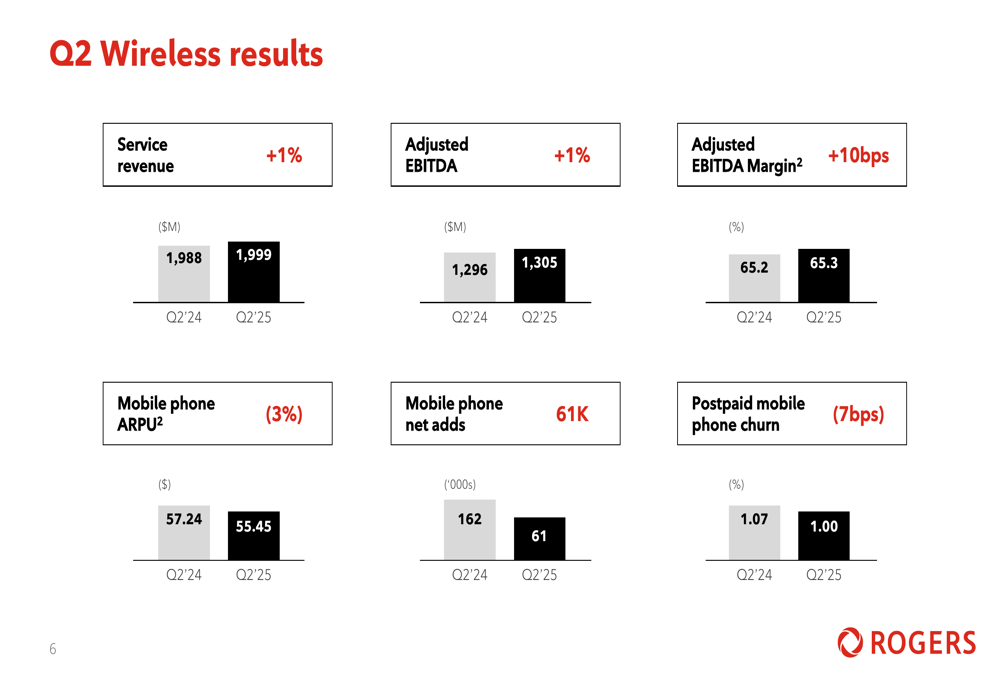

In the wireless segment, Rogers reported service revenue growth of 1% to $1,999 million and adjusted EBITDA growth of 1% to $1,305 million. The wireless segment maintained a strong adjusted EBITDA margin of 65.3%, a slight improvement of 10 basis points year-over-year. Notably, postpaid mobile phone churn improved to 1.00%, down 7 basis points from the previous year, indicating improved customer retention.

The following chart illustrates the key wireless segment metrics:

The cable segment showed similar performance with service revenue increasing by 1% to $1,961 million, while adjusted EBITDA grew by 3% to $1,147 million. The adjusted EBITDA margin for the cable segment improved significantly by 150 basis points to 58.3%, reflecting operational efficiencies.

The media segment was the standout performer, with revenue increasing by 10% to $808 million, driven by expanded media content and a strong NHL season on Sportsnet. The segment returned to positive adjusted EBITDA of $5 million, compared to a loss in the same period last year.

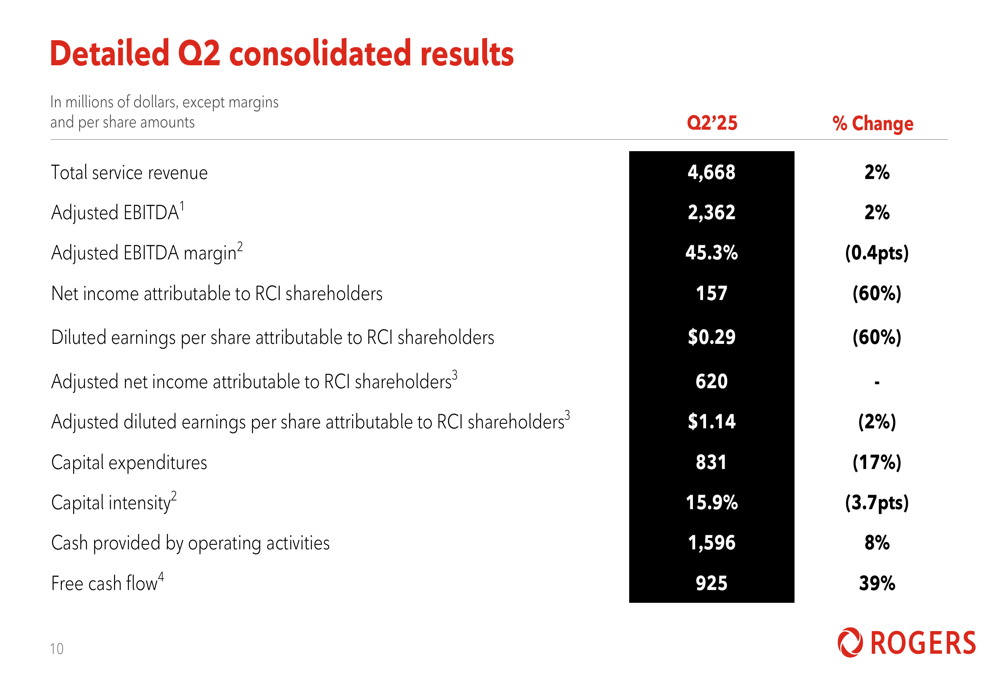

As shown in the comprehensive financial results table below, despite the positive operational performance, net income attributable to shareholders decreased significantly by 60% to $157 million:

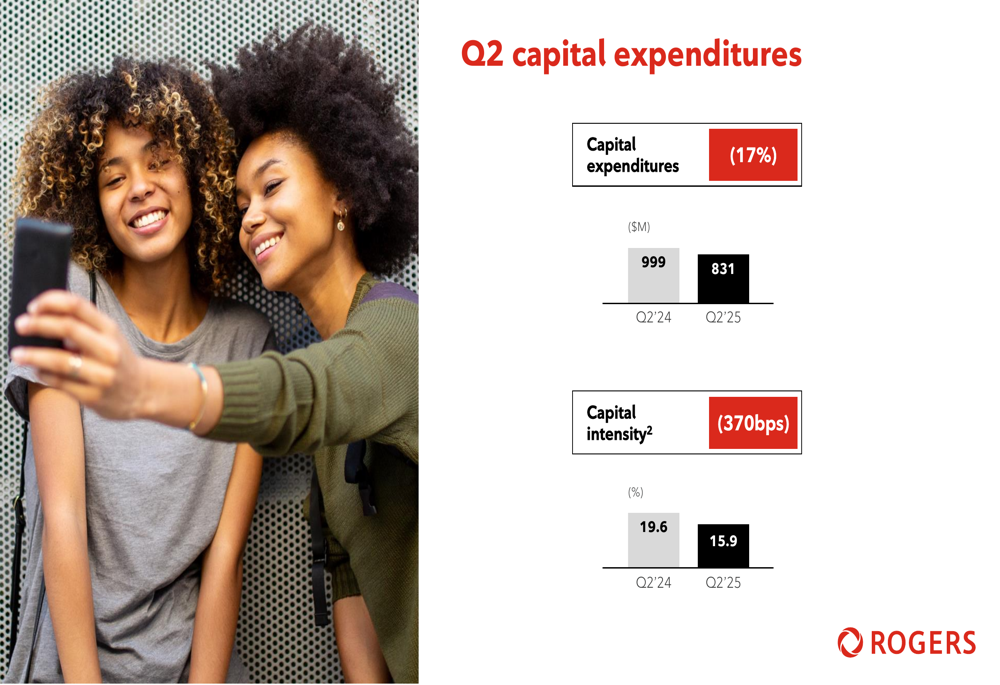

Capital expenditures decreased by 17% year-over-year to $831 million, with capital intensity improving from 19.6% to 15.9%. This reduction in spending, combined with an 8% increase in cash provided by operating activities, contributed to the substantial improvement in free cash flow.

Strategic Initiatives & Forward Guidance

A key strategic development was Rogers’ acquisition of an additional 37.5% ownership stake in Maple Leaf Sports & Entertainment (MLSE), making Rogers the 75% majority owner of the iconic sports organization. This acquisition, which closed after the quarter end, represents a significant expansion of Rogers’ sports and media portfolio.

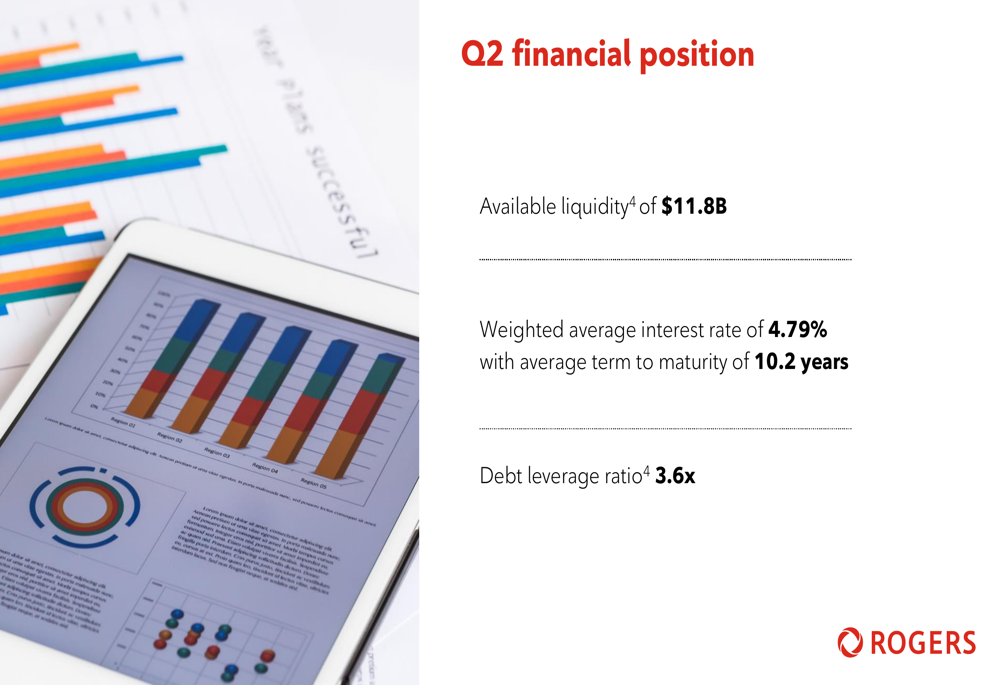

The company also highlighted its strong balance sheet position, with available liquidity of $11.8 billion and a weighted average interest rate of 4.79% with an average term to maturity of 10.2 years.

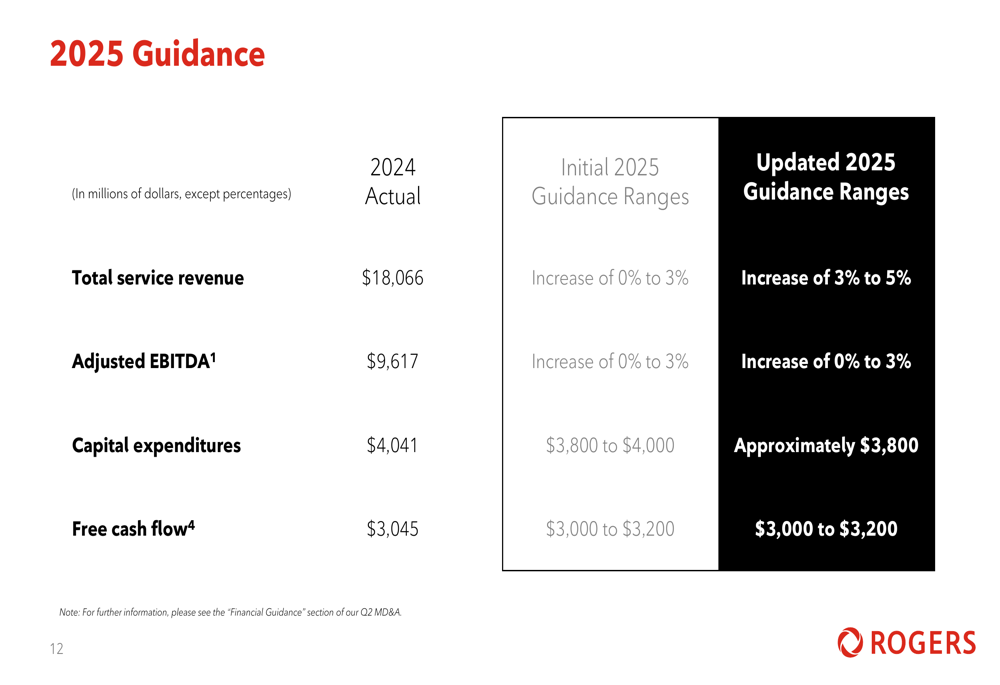

In a sign of increased confidence, Rogers updated its 2025 guidance, raising its total service revenue growth forecast to 3-5%, up from the initial guidance of 0-3%. The company maintained its adjusted EBITDA growth guidance at 0-3% and refined its capital expenditure forecast to approximately $3,800 million, down from the initial range of $3,800-$4,000 million.

The following chart details the updated guidance compared to 2024 actuals and initial 2025 guidance:

Financial Position & Balance Sheet Management

Rogers’ improved financial position is reflected in its debt leverage ratio of 3.6x, which has improved by almost a full turn since the beginning of the year. This improvement comes after the completion of an equity investment transaction, strengthening the company’s balance sheet.

The company’s focus on financial discipline aligns with statements made in previous quarters. In Q1 2023, CFO Glenn Brandt had highlighted the company’s efforts to lower debt, noting, "We have substantially lowered our debt, which positions us well for today’s more uncertain market." The continued improvement in the debt leverage ratio demonstrates Rogers’ commitment to this strategy.

While Rogers continues to show consistent growth in service revenue and adjusted EBITDA, the significant decline in net income attributable to shareholders (down 60% year-over-year) represents a potential area of concern that investors may want to monitor in future quarters. However, the strong free cash flow generation and improved balance sheet metrics suggest the company is well-positioned to navigate competitive market conditions while pursuing strategic growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.