Powell’s speech, Nvidia’s chips, Meta deal - what’s moving markets

Introduction & Market Context

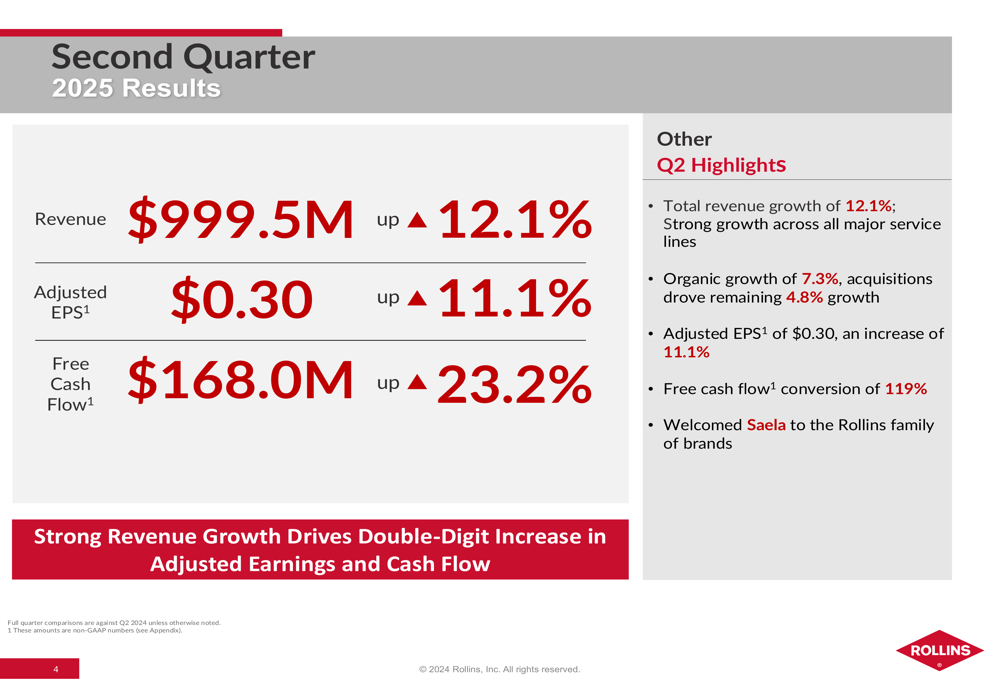

Rollins Inc . (NYSE:ROL) released its second quarter 2025 earnings presentation on July 24, showing continued strong performance with double-digit revenue growth across all service lines. The pest control company reported total revenue of $999.5 million, up 12.1% year-over-year, driven by a combination of organic growth and strategic acquisitions.

The company’s stock closed at $55.16 on July 23, with a slight increase of 0.18% in premarket trading following the earnings release. Rollins shares have been trading near their 52-week high of $58.65, reflecting investor confidence in the company’s business model and growth trajectory.

Quarterly Performance Highlights

Rollins delivered impressive financial results for Q2 2025, with revenue reaching $999.5 million, representing a 12.1% increase compared to the same period last year. Adjusted earnings per share rose to $0.30, up 11.1% year-over-year, while free cash flow grew by 23.2% to $168 million.

As shown in the following chart of quarterly performance metrics, the company maintained strong growth across all key indicators:

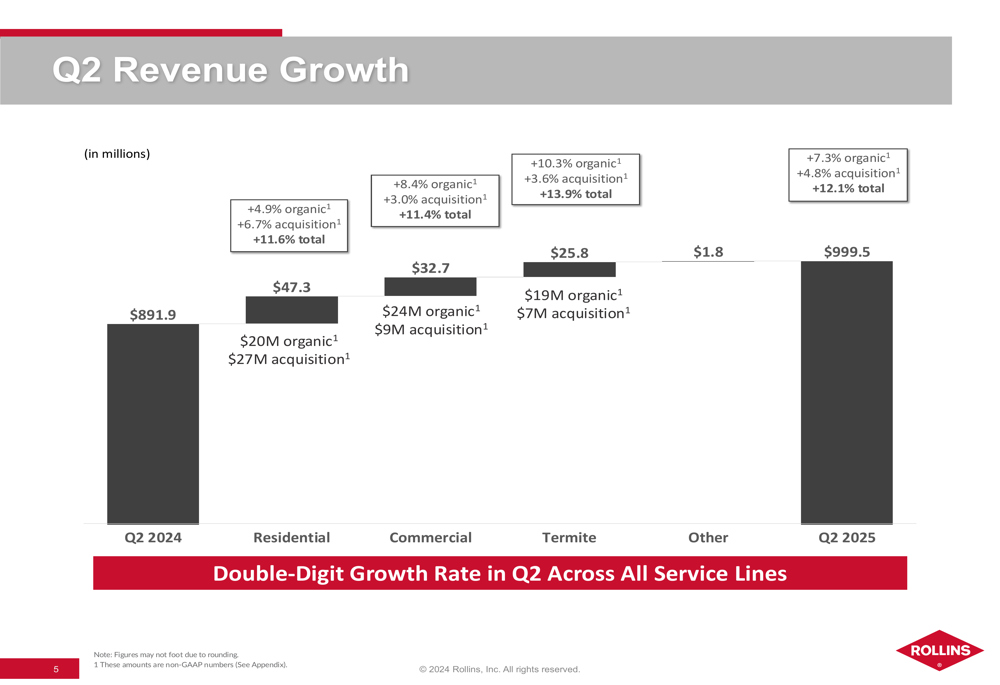

The company’s growth was balanced across all major service lines, with each segment achieving double-digit increases. Organic growth contributed 7.3% to the overall revenue increase, while acquisitions added another 4.8%.

The following breakdown illustrates how each service line contributed to the company’s overall growth:

Residential services, which represent the largest portion of Rollins’ business, grew by 11.6%, with 4.9% coming from organic growth and 6.7% from acquisitions. Commercial services increased by 11.4% (8.4% organic, 3.0% acquisition), while termite services showed the strongest growth at 13.9% (10.3% organic, 3.6% acquisition).

Detailed Financial Analysis

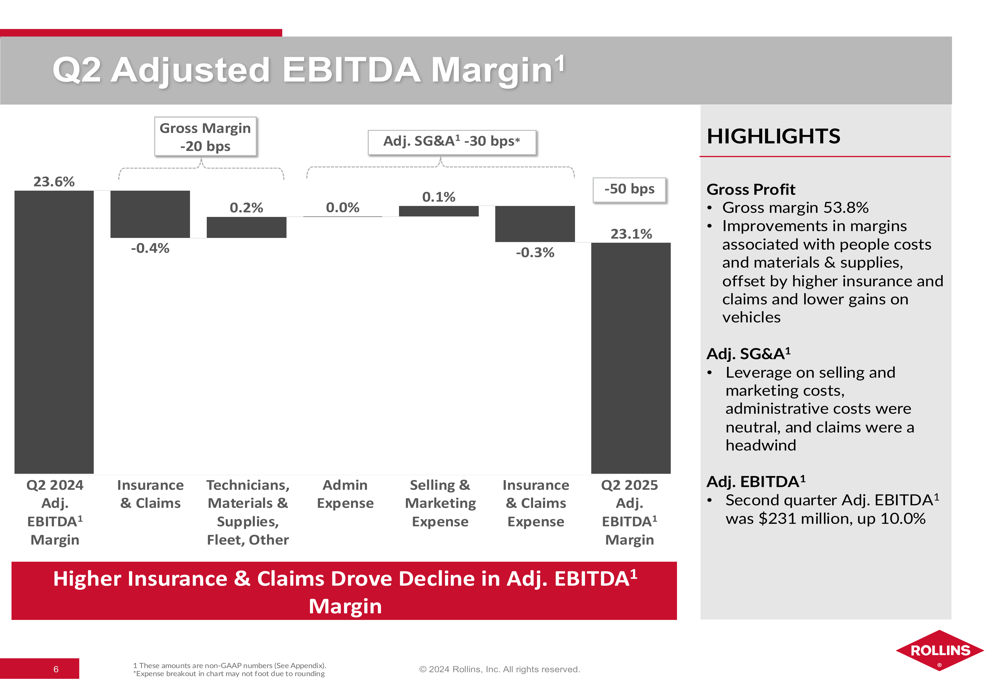

Despite strong revenue growth, Rollins experienced a slight compression in its adjusted EBITDA margin, which decreased from 23.6% in Q2 2024 to 23.1% in Q2 2025. This decline was primarily attributed to higher insurance and claims expenses, partially offset by improvements in people costs and materials and supplies.

The following waterfall chart details the factors affecting the company’s EBITDA margin:

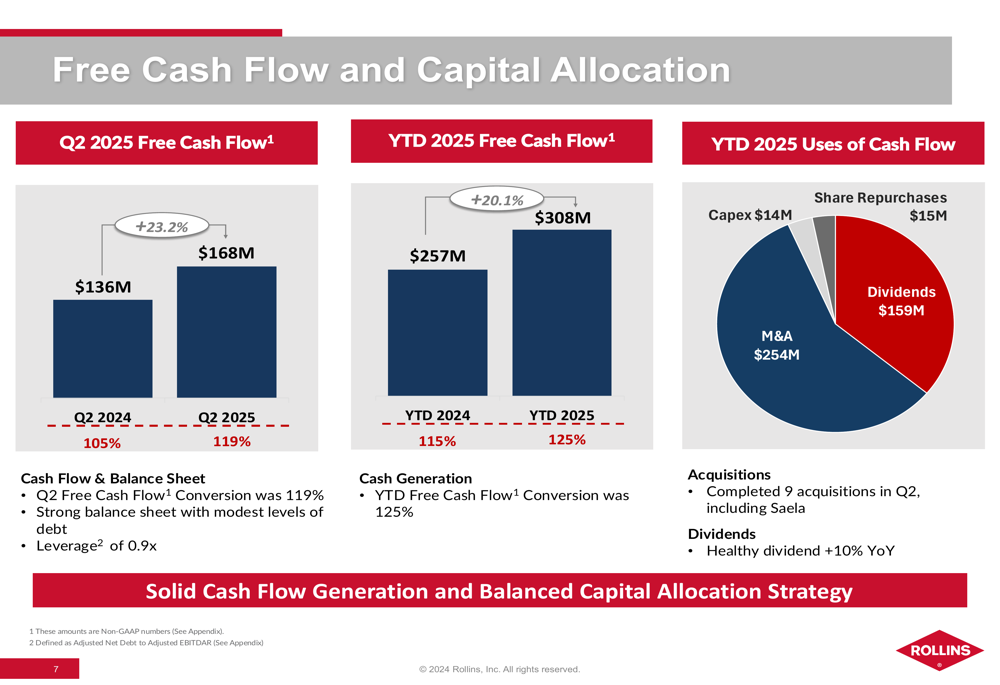

Rollins’ cash generation remained robust, with Q2 free cash flow of $168 million representing a conversion rate of 119%, up from 105% in the same period last year. Year-to-date free cash flow reached $308 million with a 125% conversion rate, a 20.1% increase compared to the first half of 2024.

The company’s capital allocation strategy focused on strategic acquisitions ($254 million), dividends ($159 million), share repurchases ($15 million), and capital expenditures ($14 million).

Rollins maintained a strong balance sheet with a leverage ratio of 0.9x, providing financial flexibility for future growth initiatives. The company completed nine acquisitions in Q2, including Saela Pest Control, continuing its strategy of growth through targeted M&A activity.

Strategic Initiatives & Growth Algorithm

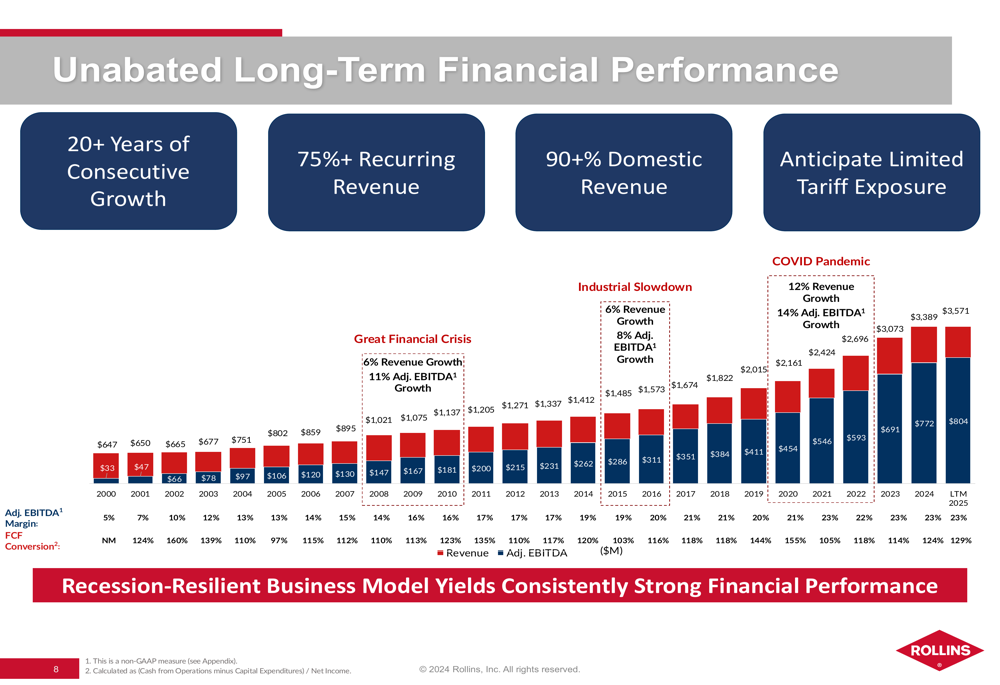

Rollins highlighted its long-term financial performance, emphasizing 20+ years of consecutive growth and the resilience of its business model through various economic cycles. With 75%+ recurring revenue and 90%+ domestic operations, the company has demonstrated stability even during challenging economic periods.

The following chart illustrates Rollins’ consistent growth trajectory since 2000:

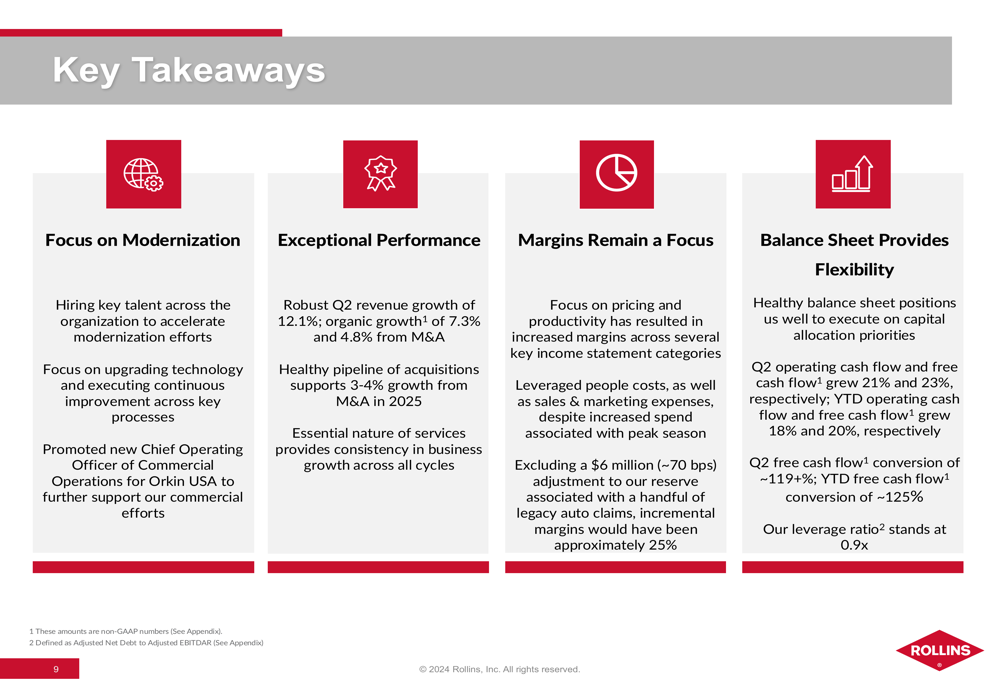

The company’s modernization initiatives focus on hiring key talent, upgrading technology, and improving key processes. These efforts are designed to support continued growth and operational efficiency, as outlined in the key takeaways slide:

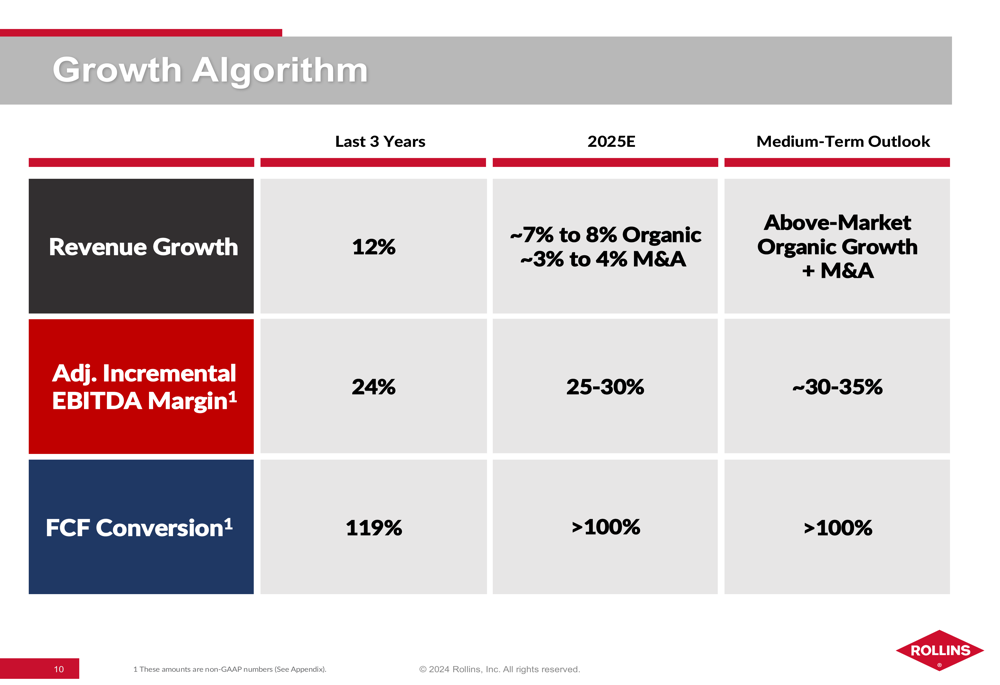

Looking ahead, Rollins presented its growth algorithm, projecting organic growth of 7-8% supplemented by 3-4% growth from M&A activities. The company expects adjusted incremental EBITDA margins of 25-30% for 2025, with a medium-term outlook of 30-35%.

Forward-Looking Statements

Rollins’ management expressed confidence in the company’s ability to maintain its growth trajectory, citing its recession-resilient business model and the essential nature of its services. The company anticipates limited exposure to tariffs due to its predominantly domestic revenue base.

The presentation emphasized Rollins’ balanced capital allocation strategy, focusing on organic growth investments, strategic acquisitions, and shareholder returns through dividends and share repurchases. With a healthy acquisition pipeline and strong cash flow generation, the company is well-positioned to execute its growth strategy.

For 2025, Rollins expects to maintain its free cash flow conversion rate above 100%, supporting its capital allocation priorities while maintaining modest debt levels. The company’s focus on pricing and productivity improvements is expected to drive margin expansion in the medium term, despite near-term headwinds from insurance and claims expenses.

Building on its Q1 2025 performance, where the company reported a 9.9% year-over-year revenue increase and a record Q1 gross margin of 51.4%, Rollins continues to demonstrate the effectiveness of its multi-brand strategy and variable cost model in delivering consistent financial results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.