China smartphone shipments slumped in June on inventory overhang: Jefferies

Roper Technologies Inc. (NYSE:NASDAQ:ROP) presented its second quarter 2025 financial results on July 21, 2025, highlighting accelerating revenue growth, strong free cash flow generation, and a significant acquisition. The company also raised its full-year guidance, signaling confidence in continued momentum for the remainder of the year.

Quarterly Performance Highlights

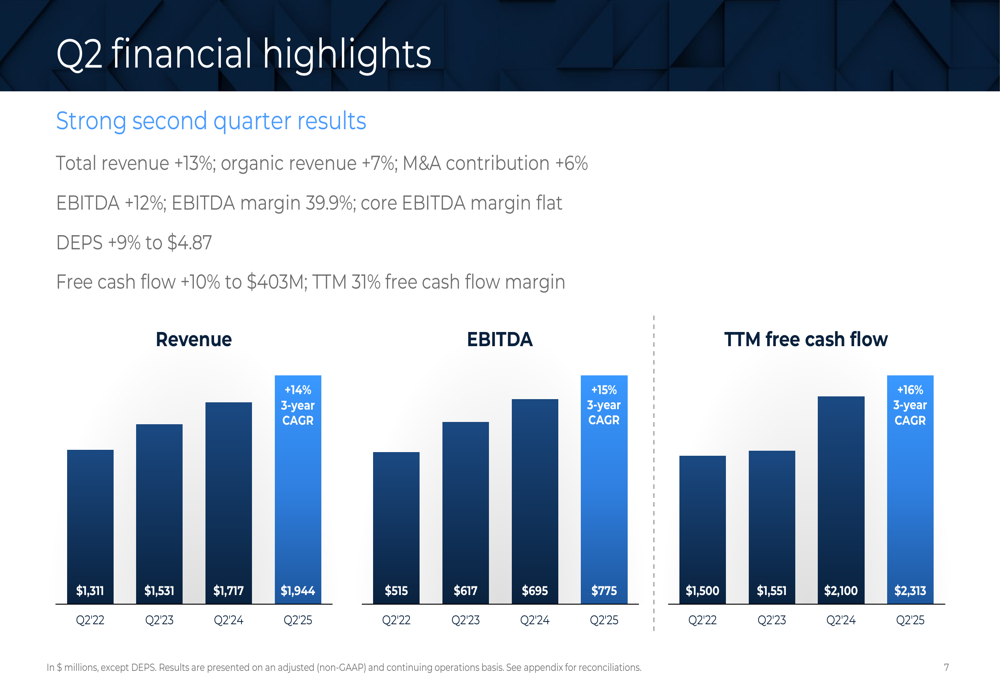

Roper reported robust second-quarter results with total revenue increasing 13% to $1.94 billion, comprising 7% organic growth and a 6% contribution from acquisitions. The company’s adjusted earnings per share (DEPS) grew 9% year-over-year to $4.87, while free cash flow increased 10% to $403 million.

"We delivered strong second quarter results across all our segments, demonstrating the resilience of our business model and the value of our mission-critical solutions," said Neil Hun, CEO of Roper Technologies, according to the presentation materials.

As shown in the following chart of quarterly financial performance, Roper has maintained consistent growth across key metrics with impressive 3-year compound annual growth rates (CAGR):

The company’s EBITDA increased 12% to $775 million with a 39.9% margin. While reported EBITDA margin was flat year-over-year on a core basis, segment core margins improved by 40 basis points, indicating operational efficiency at the business unit level.

Segment Performance Analysis

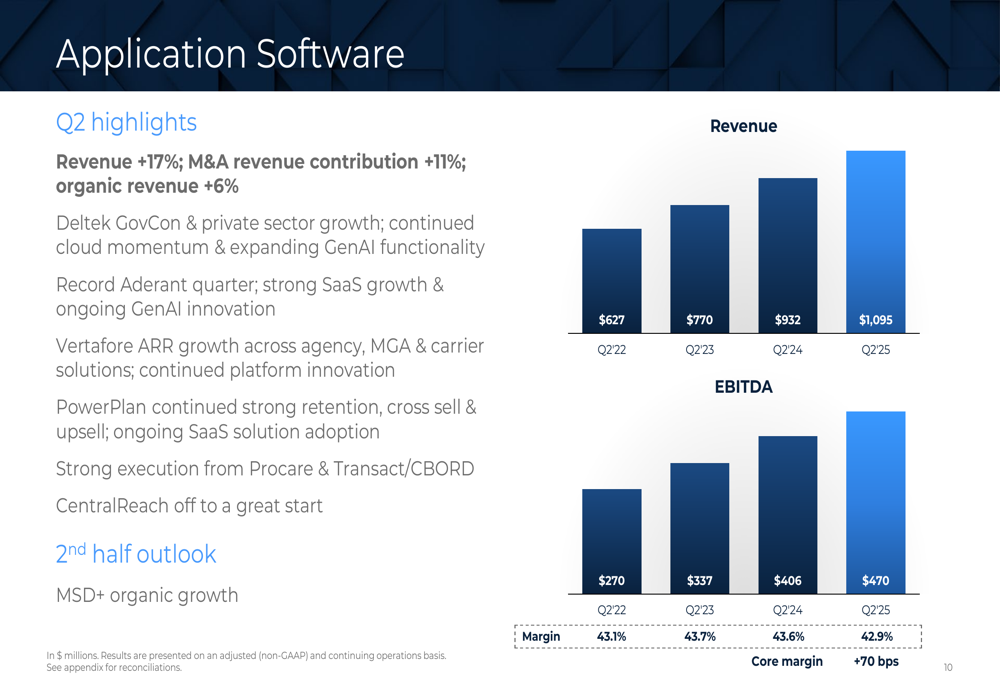

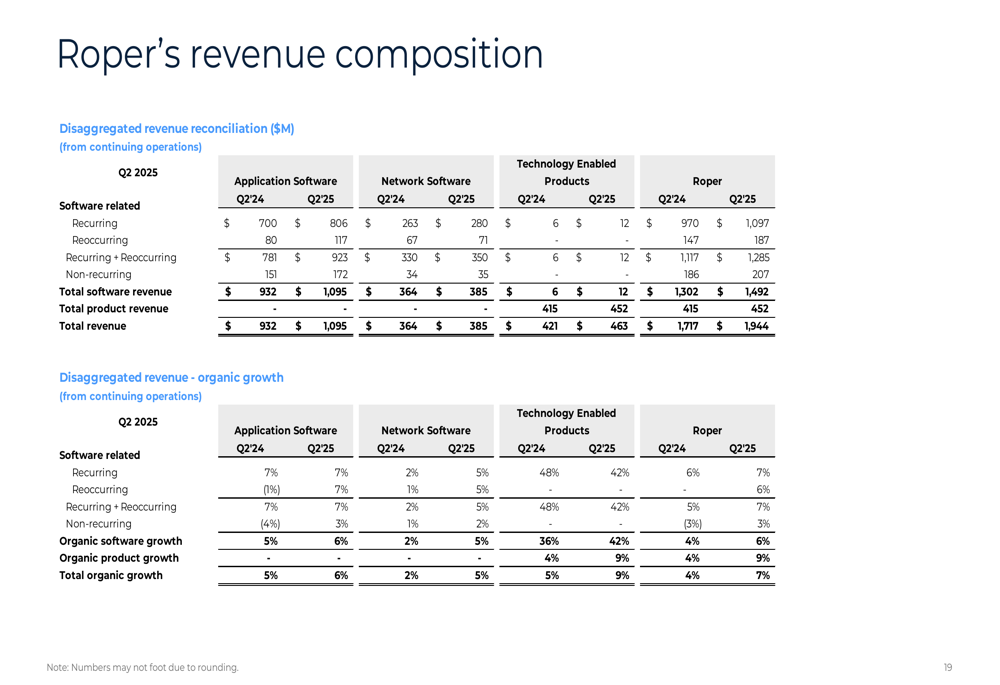

Roper’s Application Software (ETR:SOWGn) segment, the largest contributor to revenue, delivered exceptional performance with 17% growth, including 11% from acquisitions and 6% organic growth. Key drivers included Deltek’s government contracting and private sector growth, a record quarter for Aderant, strong ARR growth at Vertafore, and continued strength in PowerPlan.

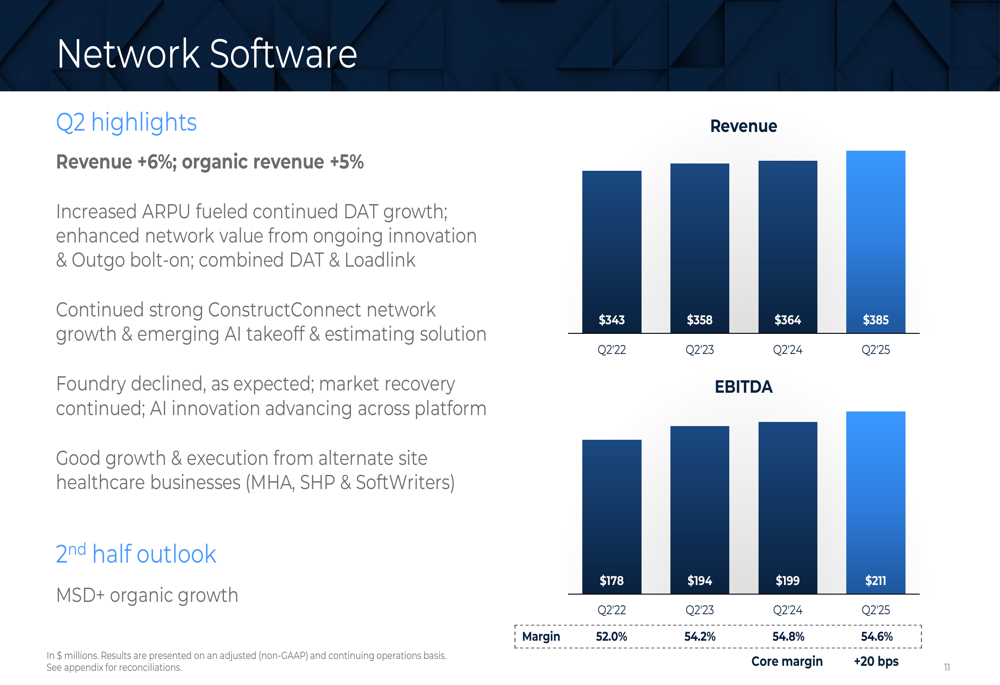

The Network Software segment posted 6% revenue growth (5% organic), driven by increased average revenue per user (ARPU) at DAT and continued strength at ConstructConnect. The Foundry declined as expected, but the segment maintained strong profitability with a 54.6% EBITDA margin.

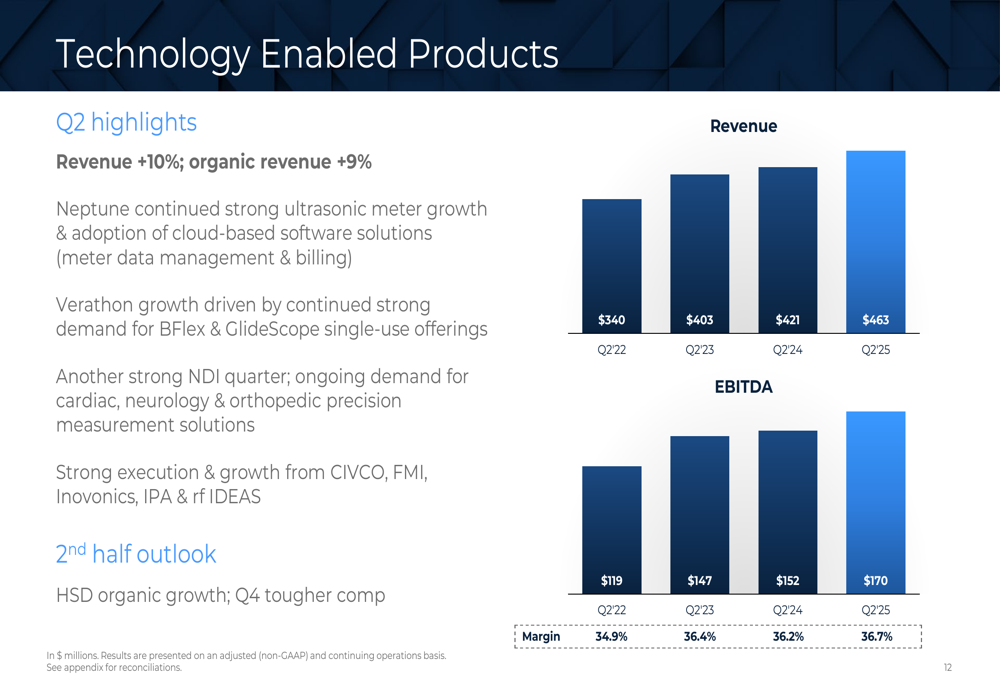

Technology Enabled Products, Roper’s hardware-focused segment, delivered impressive 10% revenue growth (9% organic). Neptune showed continued strong ultrasonic meter growth and increased adoption of cloud-based software solutions, while Verathon’s growth was driven by demand for BFlex and GlideScope products. The segment also benefited from another strong quarter at NDI and solid execution across CIVCO, FMI, Inovonics, IPA, and rf IDEAS.

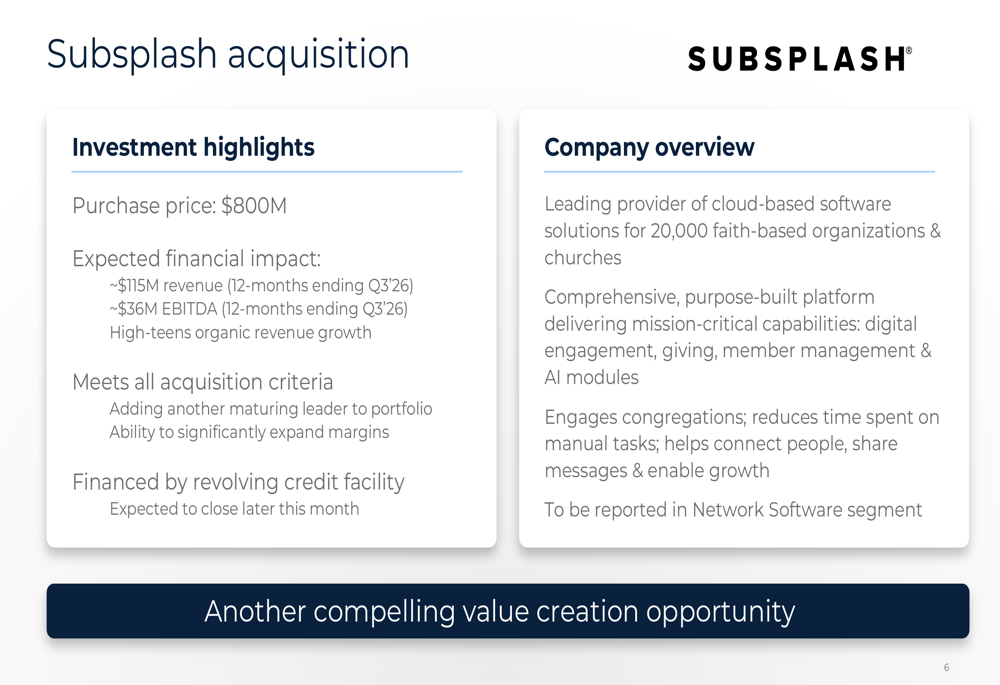

Subsplash Acquisition

A significant highlight of the quarter was Roper’s announcement of the Subsplash acquisition for $800 million. Subsplash is a leading provider of cloud-based software solutions for 20,000 faith-based organizations and churches, offering digital engagement, giving, member management, and AI modules.

The acquisition is expected to contribute approximately $115 million in revenue and $36 million in EBITDA in the 12 months ending Q3 2026, with high-teens organic revenue growth. Roper plans to finance the acquisition through its revolving credit facility, with closing expected later in July 2025. Subsplash will be reported within the Network Software segment.

Financial Position & Balance Sheet Strength

Roper maintains a strong financial position with a 2.9x net debt-to-EBITDA ratio as of Q2 2025. The company reported $242 million in cash and $1.4 billion drawn on its $3.5 billion revolving credit facility.

The company’s revenue composition continues to shift toward higher-margin recurring software revenue, which accounted for a significant portion of total revenue in Q2 2025. This recurring revenue base provides stability and visibility for future performance.

Updated Guidance & Outlook

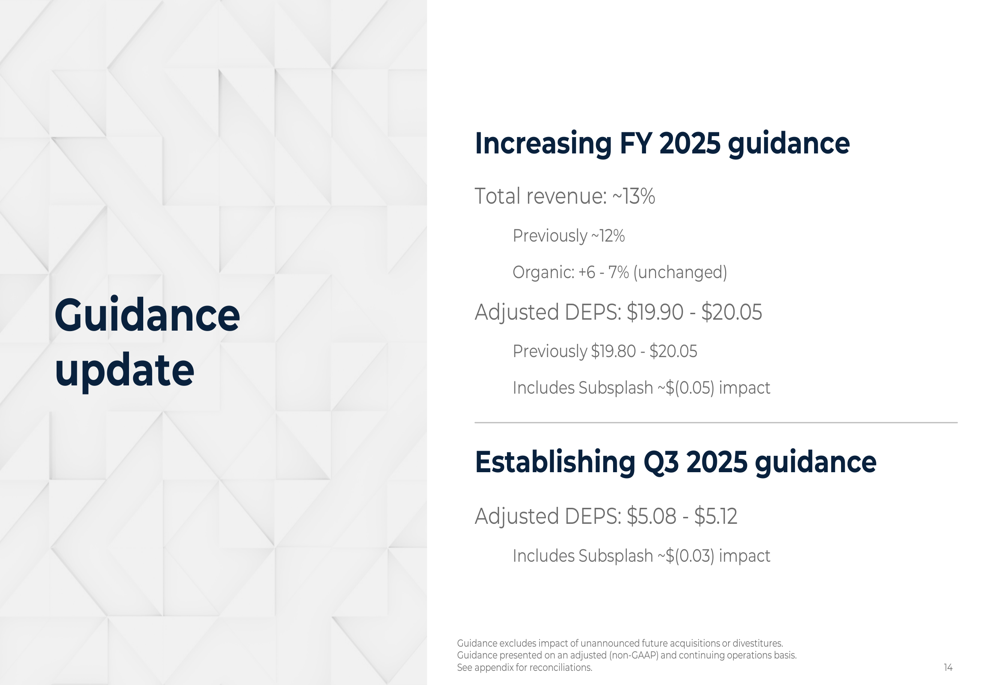

Based on strong first-half performance and confidence in continued momentum, Roper raised its full-year 2025 revenue growth guidance to approximately 13%, up from the previous estimate of approximately 12%. Organic growth guidance remained unchanged at 6-7%.

The company also tightened its adjusted DEPS guidance to $19.90-$20.05, compared to the previous range of $19.80-$20.05. This includes an expected approximately $0.05 dilutive impact from the Subsplash acquisition. For Q3 2025, Roper expects adjusted DEPS of $5.08-$5.12, including an approximately $0.03 impact from Subsplash.

Roper’s stock closed at $544.79 on July 18, 2025, and was trading slightly higher at $545.02 in pre-market activity on July 21, up 0.04%. The stock has traded in a 52-week range of $499.47 to $595.17.

The company’s presentation emphasized its strong position for continued capital deployment, citing its robust balance sheet, strong cash flow generation, and a large pipeline of attractive acquisition opportunities. Management indicated that all segments are expected to deliver mid-single-digit or higher organic growth in the second half of 2025, with Technology Enabled Products potentially achieving high-single-digit growth despite tougher comparisons in Q4.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.