Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

Grupo Rotoplas SAB de CV (AGUA) presented its second quarter 2025 earnings results on July 24, 2025, highlighting sequential improvements in key financial metrics despite year-over-year challenges. The water solutions company has been navigating varied market conditions across its operating regions while maintaining its strategic focus on profitability and cash flow discipline.

The company’s stock closed at 13.30 MXN on the day of the earnings call, with a modest 0.45% increase. Rotoplas continues to operate in a challenging environment, particularly in its home market of Mexico, while seeing stronger performance in markets like the United States.

Quarterly Performance Highlights

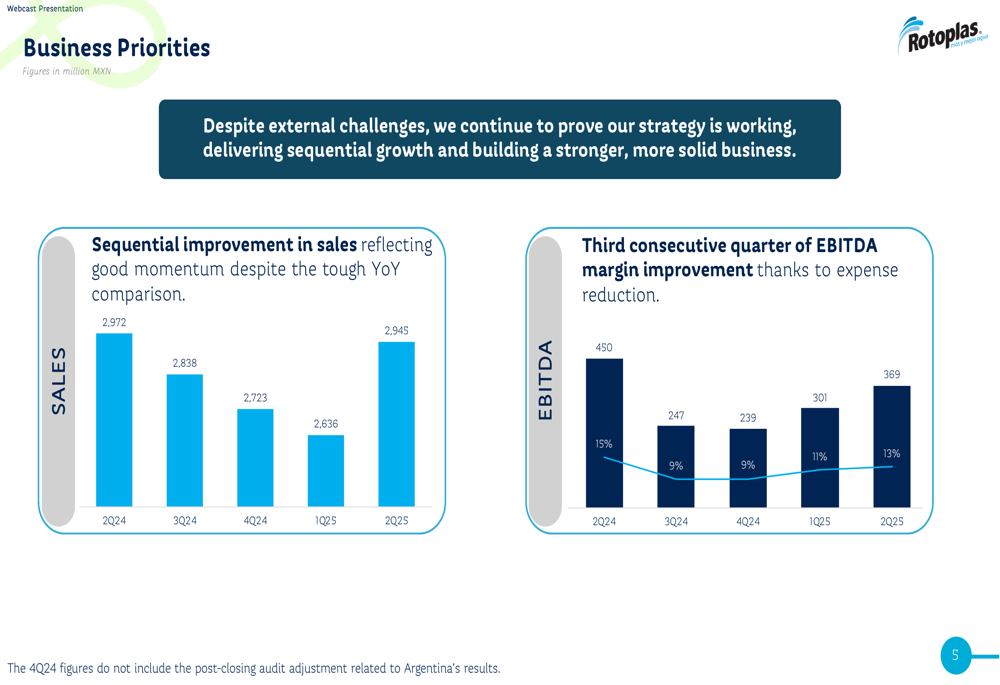

Rotoplas reported sales of 2,945 million MXN in Q2 2025, representing a slight year-over-year decline of 0.9% from 2,972 million MXN in Q2 2024. However, the company achieved a 12% sequential improvement compared to Q1 2025 (2,636 million MXN), marking the beginning of a potential recovery trend.

As shown in the following chart of quarterly sales and EBITDA performance:

EBITDA for the quarter reached 369 million MXN, down 18% year-over-year but up 23% sequentially from Q1 2025. The EBITDA margin stood at 13%, showing sequential improvement for the third consecutive quarter (from 9% in Q4 2024 and 11% in Q1 2025), though still below the 15% achieved in Q2 2024.

CEO Carlos Rojas Aboumrad and CFO Andrés Pliego Rivero-Borrell emphasized the company’s focus on sustainable growth, highlighting strong market acceptance of vertical tinaco and IoT-enabled water level sensors in Mexico, e-commerce growth, and double-digit revenue growth in the U.S. market.

Detailed Financial Analysis

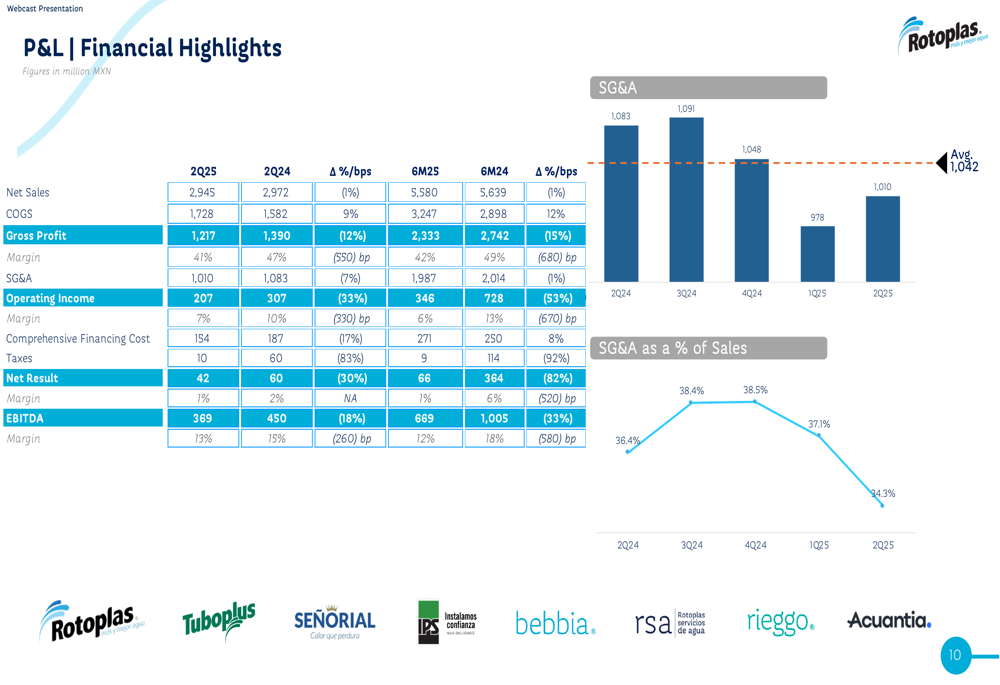

The company’s detailed profit and loss statement reveals mixed results across key financial metrics. Net income for Q2 2025 was 42 million MXN, down from 60 million MXN in Q2 2024, while operating income declined to 207 million MXN from 307 million MXN in the same period last year.

The following comprehensive financial overview shows the full P&L breakdown:

Selling, general, and administrative (SG&A) expenses decreased by 6.7% year-over-year to 1,010 million MXN, reflecting the company’s cost discipline efforts. However, cost of goods sold (COGS) increased by 9.2% to 1,728 million MXN, pressuring gross margins.

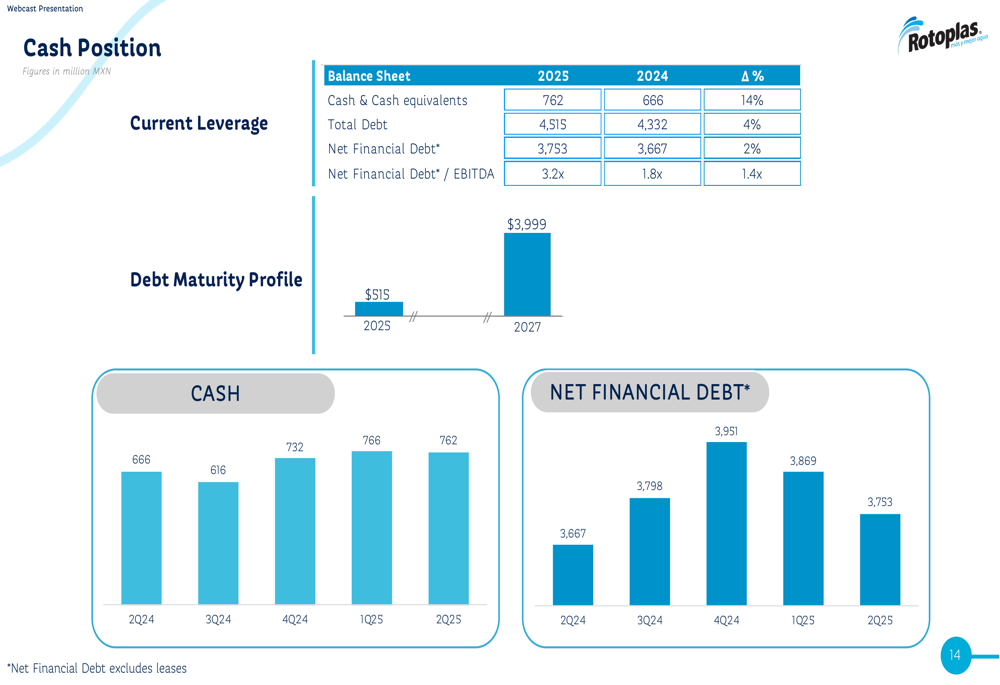

The company’s financial position shows some concerning trends in leverage, with the net financial debt to EBITDA ratio increasing to 3.2x from 1.8x a year earlier. Total (EPA:TTEF) debt stood at 4,515 million MXN as of Q2 2025.

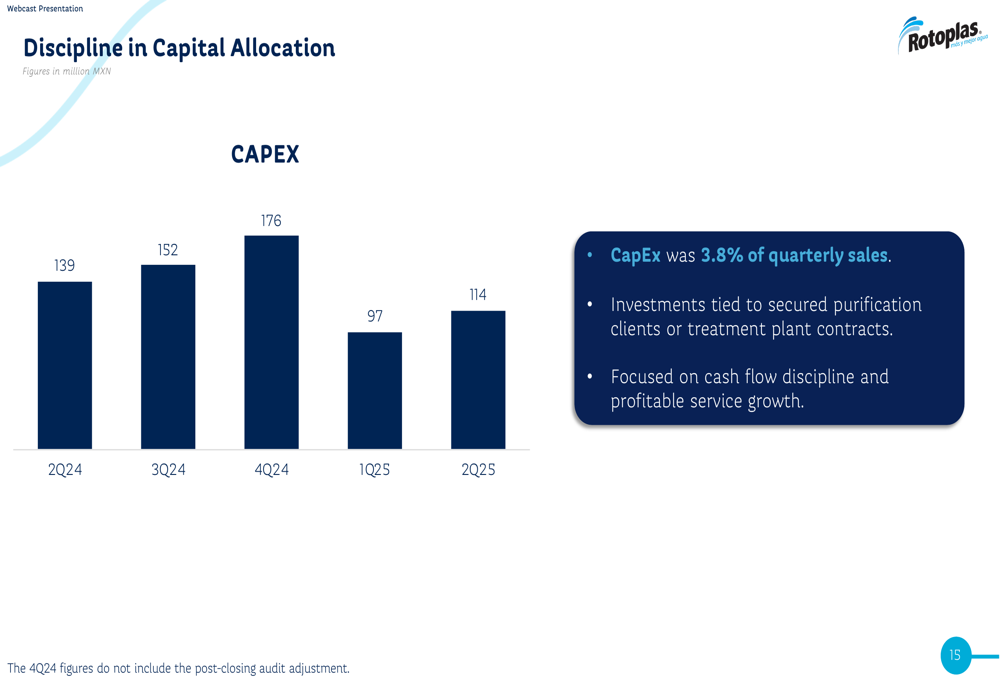

Capital expenditure (CAPEX) for the quarter was 114 million MXN, representing 3.8% of quarterly sales. This reflects the company’s disciplined approach to investments, focusing primarily on secured purification clients and treatment plant contracts.

Geographic Performance

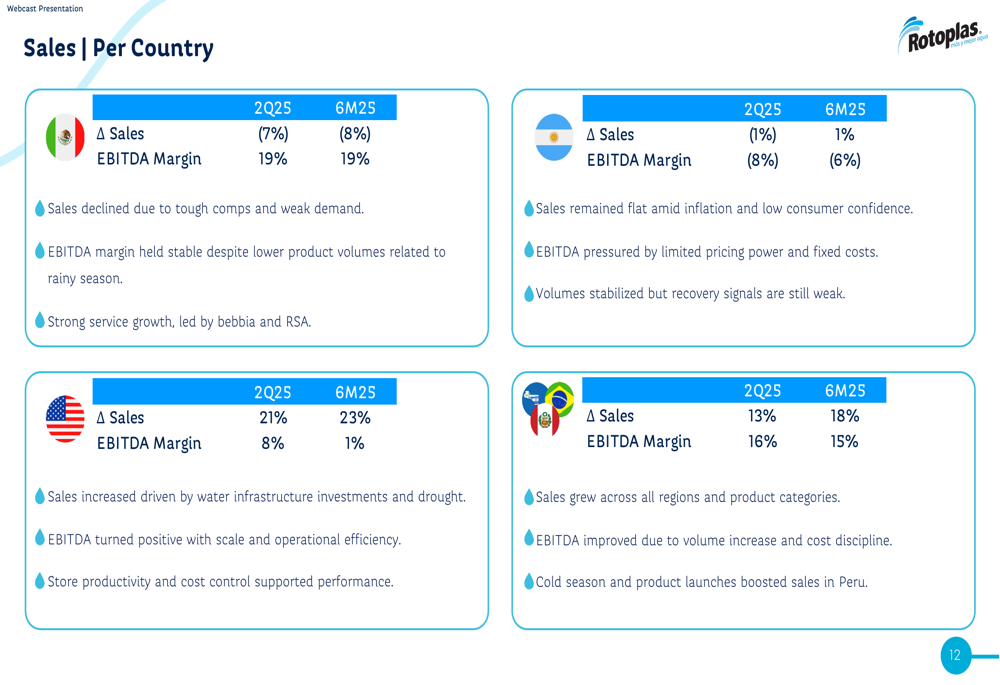

Rotoplas’s performance varied significantly across its operating regions, with the U.S. market showing the strongest results while Mexico faced headwinds.

In Mexico, sales declined due to challenging year-over-year comparisons, though the company maintained healthy EBITDA margins. Argentina showed flat sales amid ongoing inflation challenges, while Peru demonstrated growth across regions and product categories.

The U.S. market was a particular bright spot, with increased sales driven by water infrastructure investments and positive EBITDA contribution, marking an important milestone for the company’s international expansion strategy.

Strategic Initiatives

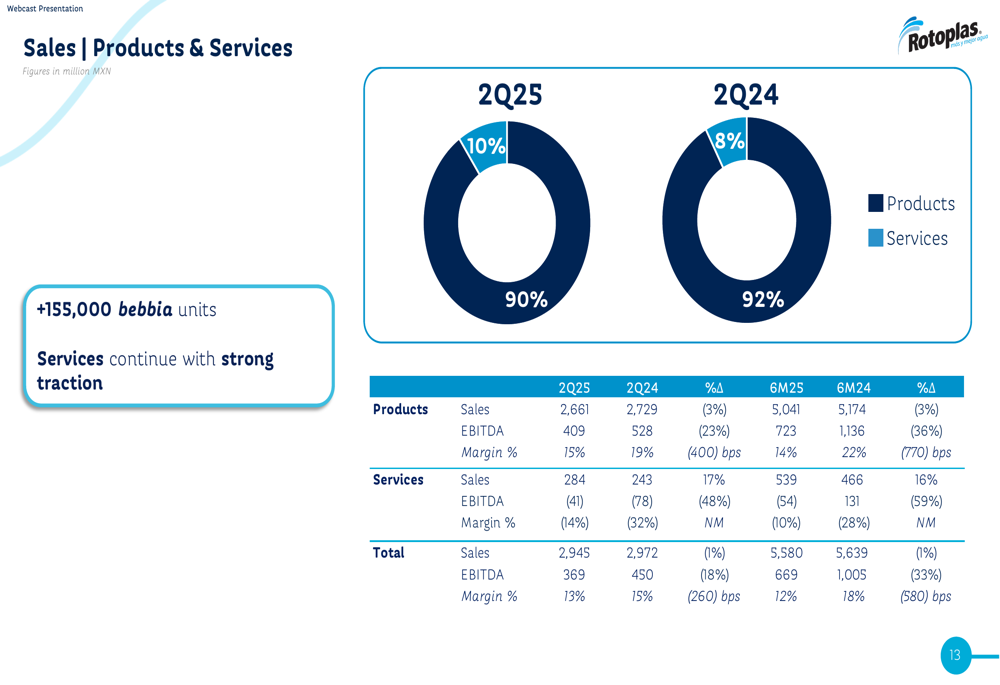

Rotoplas continues to balance its product and service offerings, with products generating 90% of revenues (2,661 million MXN) and services accounting for 10% (284 million MXN) in Q2 2025. While the product segment delivered a healthy EBITDA margin, the services segment still reported negative EBITDA.

The company highlighted several strategic initiatives, including digital transformation through B2B and B2B2C e-commerce platforms and a national logistics control tower in Mexico. Sustainability remains a key focus, with partnerships delivering rainwater harvesting systems and community projects.

The Board of Directors approved a capital reimbursement of MXN 0.25 per share in cash, which is half the amount distributed in previous years, reflecting the company’s more cautious financial approach in the current environment.

Forward-Looking Statements

Looking ahead, Rotoplas management emphasized their continued focus on profitability and cash flow improvement, investing in technology and services for long-term growth, and maintaining discipline in their approach to what they can control.

The company faces several challenges, including economic volatility in key markets, competitive pressures, and the need to improve its debt metrics. However, management expressed confidence in their strategic direction and ability to navigate the current market conditions.

With sequential improvements in key metrics for three consecutive quarters, Rotoplas appears to be stabilizing its performance despite year-over-year declines. Investors will be watching closely to see if this recovery trend continues in the coming quarters and whether the company can successfully execute its strategic initiatives while improving its financial position.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.