How are energy investors positioned?

Royal Caribbean Group (NYSE:RCL) shares climbed 3.56% in premarket trading to $224 following the release of its Q1 2025 earnings presentation on April 29, which revealed robust financial performance and an improved outlook for the full year. The cruise operator reported a 35% year-over-year increase in adjusted earnings per share, demonstrating strong operational execution and effective cost management.

Quarterly Performance Highlights

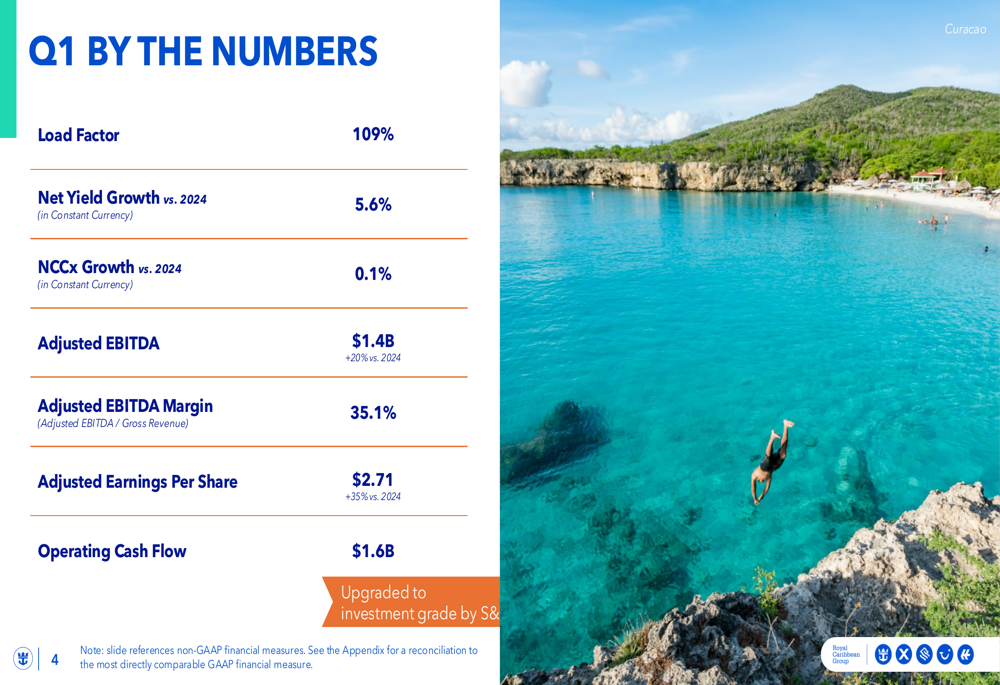

Royal Caribbean delivered impressive first-quarter results, highlighted by a 35% increase in adjusted earnings per share to $2.71 compared to the same period last year. The company achieved a 109% load factor, indicating ships operating above nominal capacity, while net yield growth reached 5.6% in constant currency terms.

The company’s cost control measures proved effective, with net cruise costs excluding fuel (NCCx) increasing by just 0.1% year-over-year in constant currency. This disciplined approach to expenses, combined with strong revenue growth, resulted in adjusted EBITDA of $1.4 billion, representing a 20% increase from Q1 2024.

As shown in the following financial summary from the presentation:

"We’ve delivered exceptional results this quarter, demonstrating the strength of our business model and our ability to execute effectively," said Jason Liberty, CEO of Royal Caribbean Group, according to the presentation materials. The company also highlighted its upgraded credit rating to investment grade by S&P, reflecting its improved financial position.

Forward Guidance

Following the strong Q1 performance, Royal Caribbean raised its full-year 2025 earnings guidance to $14.55-$15.55 per share, up from the previous range of $14.35-$14.65 announced in January. This represents approximately 28% year-over-year growth in adjusted EPS.

The guidance upgrade was attributed to several factors, including $0.13 from Q1 business outperformance, $0.05 from reduced share count, and $0.37 from favorable foreign exchange and fuel rates.

The detailed breakdown of the guidance upgrade is illustrated here:

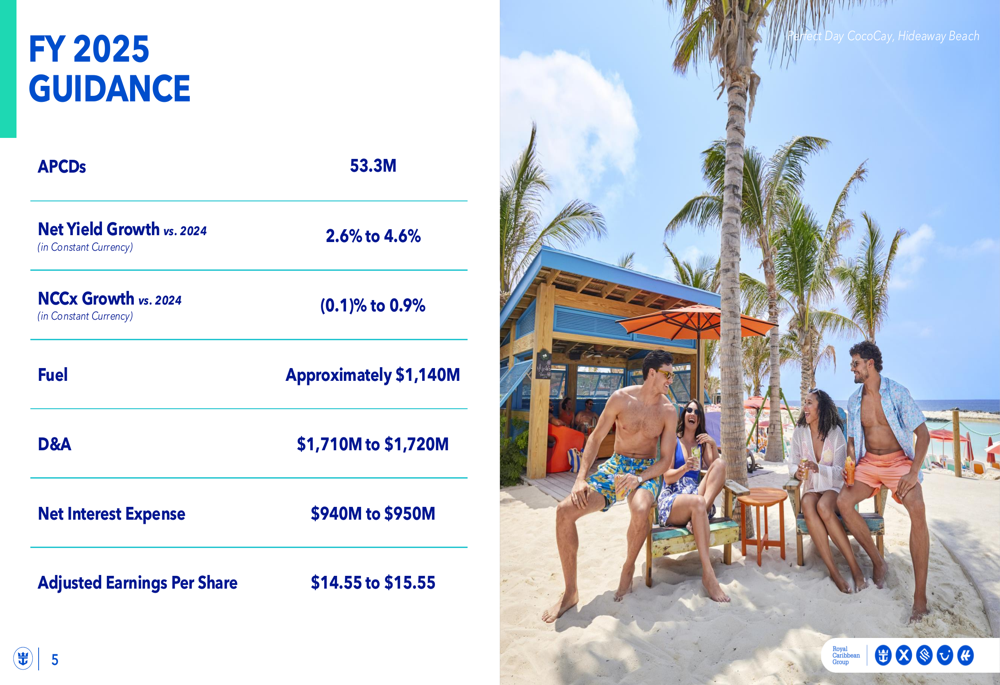

For the full year 2025, Royal Caribbean expects:

- Available Passenger Cruise Days (APCDS) of 53.3 million

- Net yield growth of 2.6% to 4.6% in constant currency

- NCCx growth of -0.1% to 0.9% in constant currency

- Adjusted earnings per share of $14.55 to $15.55

The company’s full-year guidance is presented in detail below:

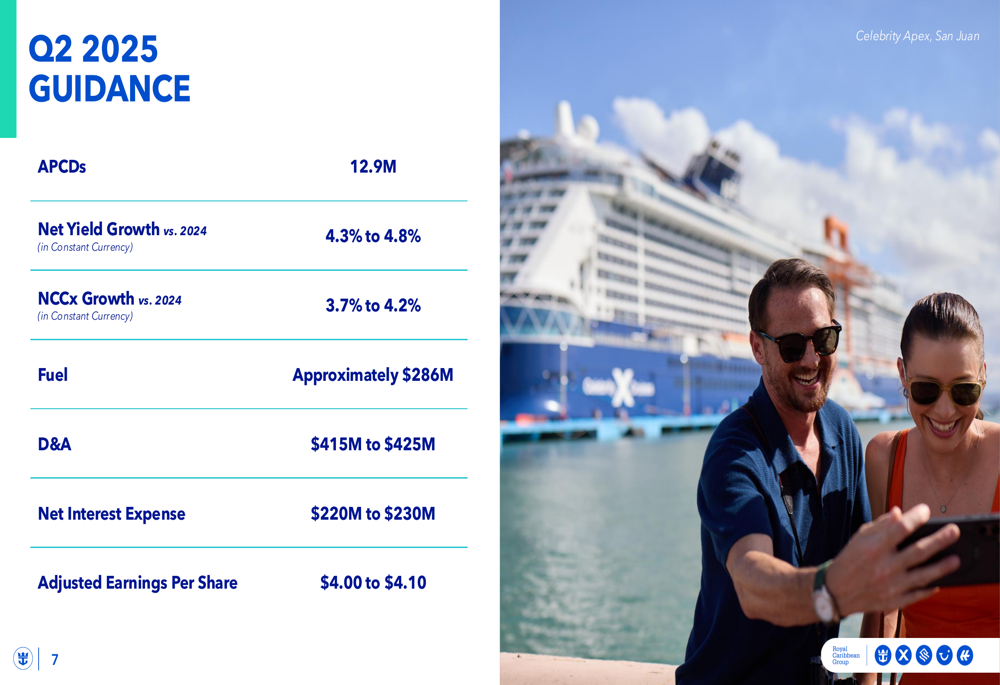

For the upcoming second quarter, Royal Caribbean projects adjusted earnings per share of $4.00 to $4.10, with net yield growth of 4.3% to 4.8% in constant currency. The company expects slightly higher cost growth in Q2, with NCCx increasing by 3.7% to 4.2% compared to the same period last year.

Strategic Initiatives

Royal Caribbean emphasized its long-term strategic program called "PERFECTA," which aims to deliver 20% EPS compound annual growth rate (CAGR) and high teens return on invested capital (ROIC) by 2027. The initiative focuses on maintaining solid investment grade metrics while delivering exceptional vacation experiences.

The PERFECTA program is visualized in this slide:

The company also highlighted its "Proven Formula" for delivering long-term shareholder value, which consists of three key elements: moderate capacity growth, moderate yield growth, and disciplined cost control. This balanced approach has been central to Royal Caribbean’s business strategy.

Royal Caribbean reaffirmed its mission to "deliver the best vacation experiences responsibly," underscoring the company’s commitment to both customer satisfaction and sustainable operations.

Financial Analysis

Royal Caribbean’s strong Q1 performance and improved full-year outlook reflect the company’s operational excellence and effective financial management. The 35% growth in adjusted EPS significantly outpaces the industry average and demonstrates the company’s ability to leverage its scale and brand strength.

The 5.6% increase in net yields indicates strong pricing power and demand for cruise vacations, while the minimal 0.1% growth in NCCx highlights effective cost management. The combination resulted in an adjusted EBITDA margin of 35.1%, representing a substantial improvement in profitability.

Operating cash flow reached $1.6 billion in Q1, providing the company with ample liquidity to fund its growth initiatives and further strengthen its balance sheet. The upgrade to investment grade by S&P marks an important milestone in Royal Caribbean’s financial recovery following the challenges faced by the cruise industry in recent years.

The company’s raised guidance for 2025 suggests management’s confidence in sustaining this momentum throughout the year, despite potential macroeconomic headwinds. With a strong booking position and effective yield management, Royal Caribbean appears well-positioned to deliver on its ambitious growth targets.

The stock’s premarket gain of 3.56% to $224 reflects investor optimism about the company’s performance and outlook. At this level, Royal Caribbean shares are trading well above their 52-week low of $130.08, though still below their 52-week high of $277.08, suggesting potential upside if the company continues to execute on its strategic initiatives and financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.