Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

Royal Unibrew A/S (CPH:RBREW) presented its H1 2025 interim results on August 27, 2025, revealing solid performance despite weather-related challenges in key markets. The Danish beverage company’s stock has faced pressure in recent months, with shares trading at DKK 465, down from a 52-week high of DKK 592, reflecting broader market concerns following a disappointing Q1 performance earlier this year.

The H1 results demonstrate a significant improvement from Q1, when the company missed analyst expectations with EPS of $2.50 against forecasts of $2.76. This recovery suggests the company’s geographic diversification strategy is yielding results, even as consumer sentiment remains cautious across European markets.

Executive Summary

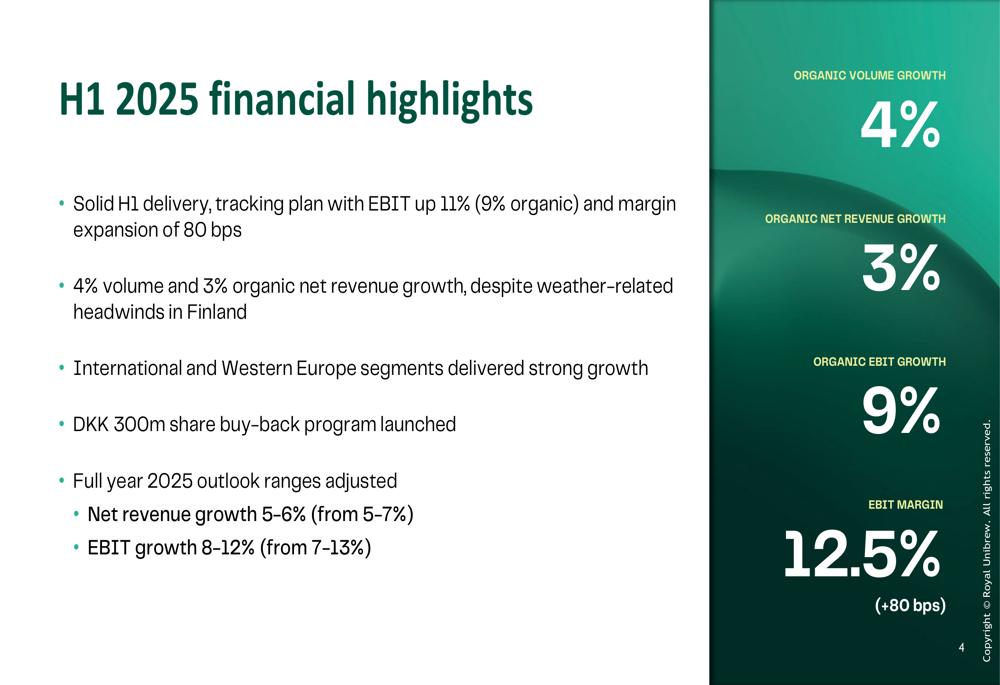

Royal Unibrew reported an 11% increase in EBIT for H1 2025, with organic EBIT growth of 9% and margin expansion of 80 basis points to 12.5%. The company achieved 4% volume growth and 3% organic net revenue growth, despite weather-related headwinds in Finland during May and June.

As shown in the following financial highlights slide, the company’s performance was driven by strong results in International and Western Europe segments, offsetting challenges in Northern Europe:

CEO Lars Jensen and CFO Lars Vestergaard emphasized the company’s operational improvements and efficiency gains as key drivers of the margin expansion. The management team has launched a DKK 300 million share buy-back program and adjusted the full-year 2025 outlook ranges, narrowing net revenue growth expectations to 5-6% (from 5-7%) and EBIT growth to 8-12% (from 7-13%).

Quarterly Performance Highlights

Royal Unibrew’s performance varied significantly across its three geographic segments, highlighting the value of the company’s diversified market approach.

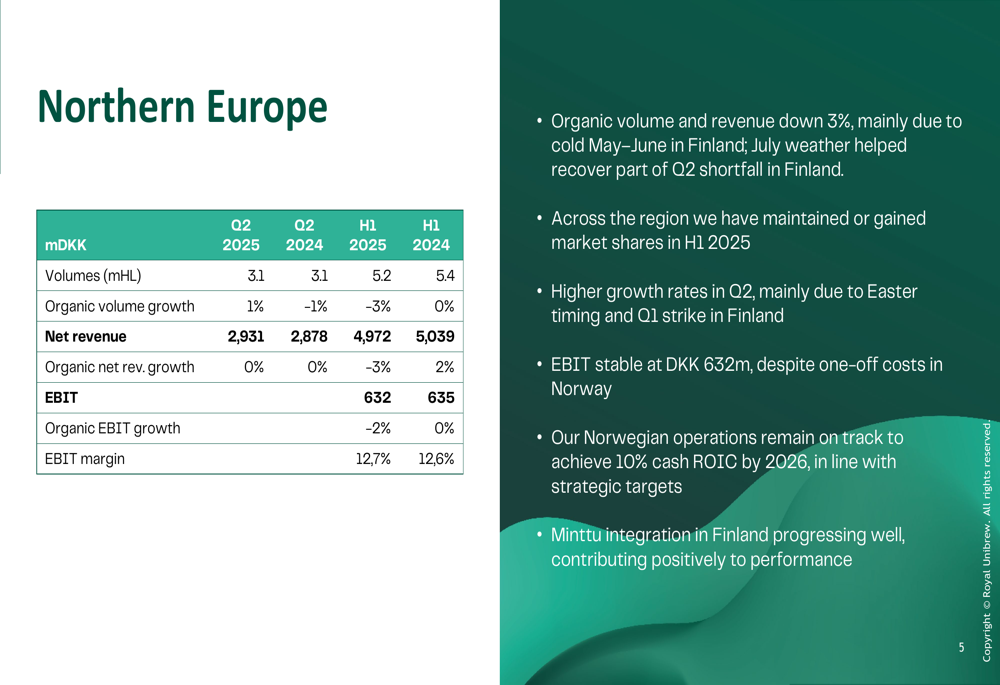

Northern Europe faced challenges with organic volume and revenue down 3%, primarily due to cold weather in Finland during May-June. However, the company maintained or gained market share across the region, and July weather helped recover part of the Q2 shortfall in Finland. EBIT remained stable at DKK 632 million despite one-off costs in Norway, and the Minttu integration in Finland is progressing well.

The regional breakdown for Northern Europe shows the impact of these challenges:

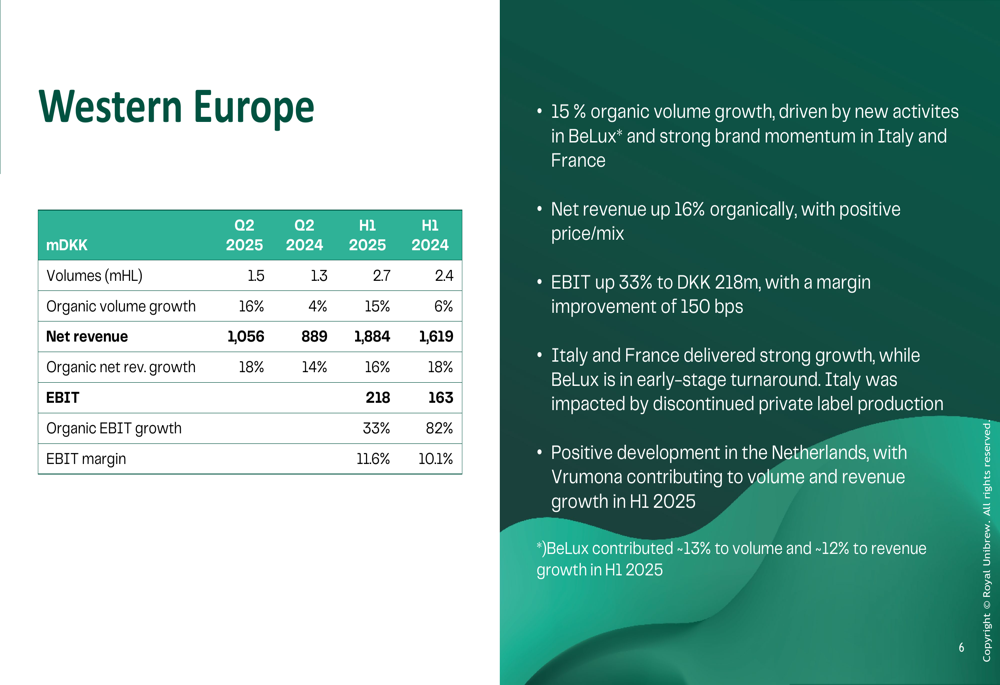

In contrast, Western Europe delivered exceptional results with 15% organic volume growth and 16% net revenue growth. EBIT increased by 33% to DKK 218 million, with margin improvement of 150 basis points to 11.6%. This strong performance was driven by new activities in BeLux and strong brand momentum in Italy and France, while the Netherlands contributed positively through the Vrumona business.

The Western Europe performance metrics demonstrate this segment’s strong contribution:

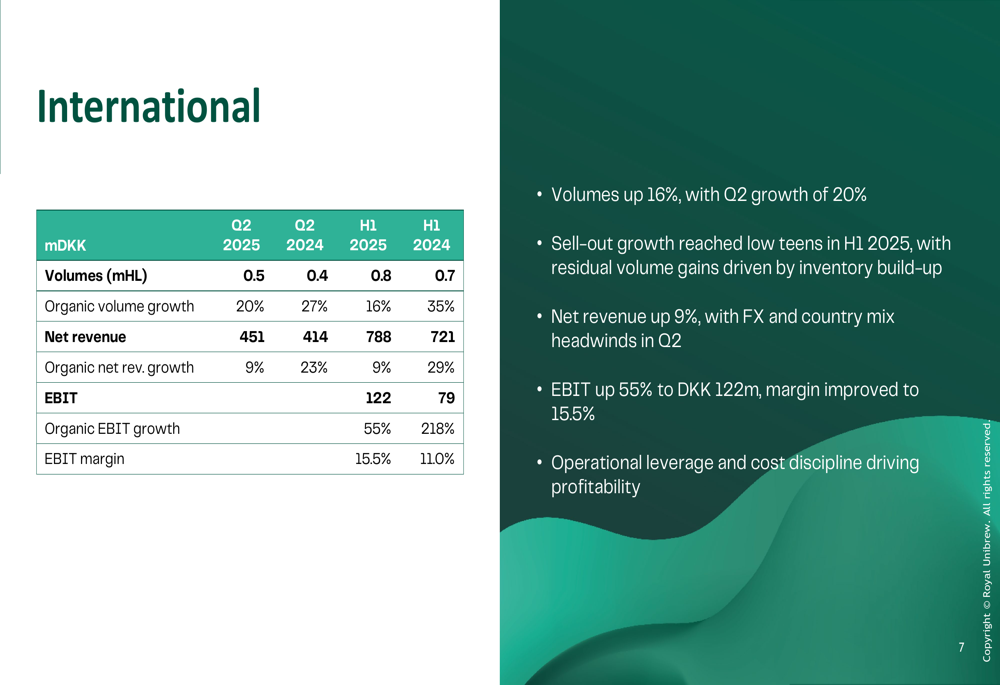

The International segment also showed robust growth with volumes up 16% and EBIT increasing by 55% to DKK 122 million. The EBIT margin improved significantly to 15.5% from 11.0% in H1 2024, driven by operational leverage and cost discipline. Net revenue grew by 9%, with some headwinds from foreign exchange and country mix in Q2.

The International segment’s performance is detailed in the following slide:

Detailed Financial Analysis

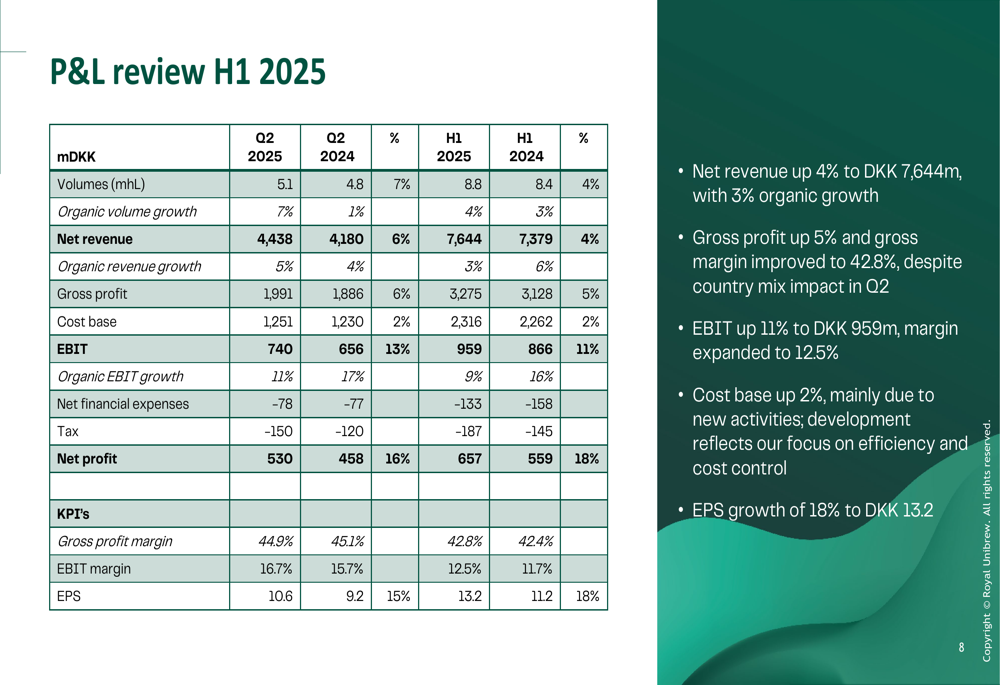

Royal Unibrew’s consolidated P&L shows strong improvement across key metrics, with net profit up 18% to DKK 657 million and EPS growing at the same rate to DKK 13.2. Gross profit increased by 5% to DKK 3,275 million, with gross margin improving to 42.8% despite country mix impact in Q2.

The company’s cost base increased by only 2%, primarily due to new activities, reflecting management’s focus on efficiency and cost control. This disciplined approach to costs contributed significantly to the EBIT margin expansion to 12.5%.

The comprehensive P&L review provides a detailed breakdown of the company’s financial performance:

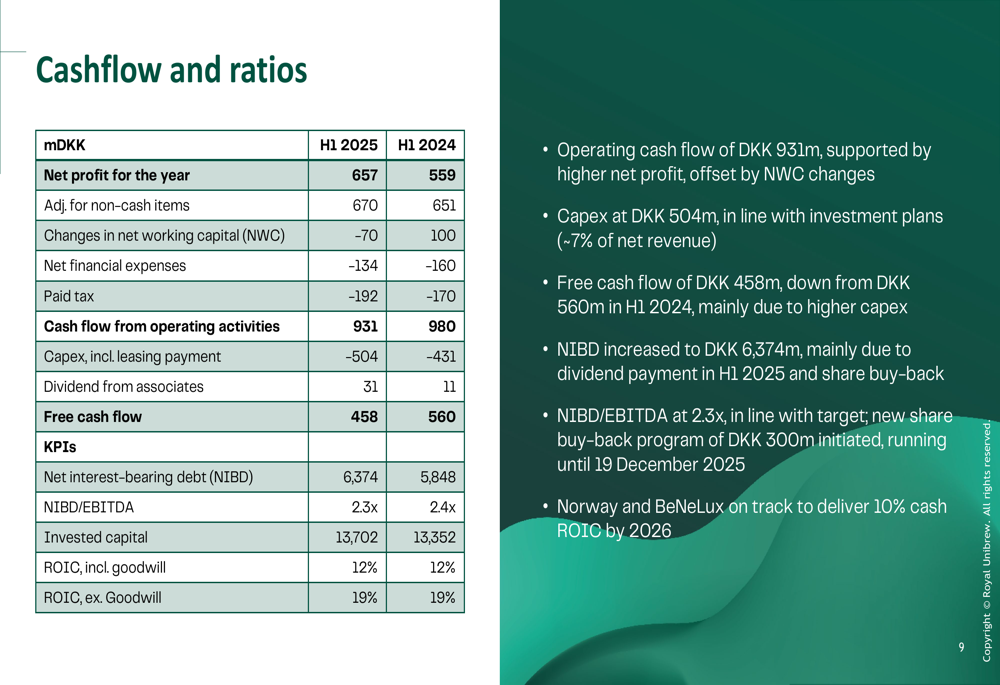

Cash flow from operating activities reached DKK 931 million, supported by higher net profit but offset by changes in net working capital. Capital expenditure increased to DKK 504 million, representing approximately 7% of net revenue and in line with the company’s investment plans. As a result, free cash flow decreased to DKK 458 million from DKK 560 million in H1 2024.

Net interest-bearing debt increased to DKK 6,374 million, mainly due to dividend payments and share buybacks, with the NIBD/EBITDA ratio at 2.3x, in line with the company’s target. Return on invested capital remained stable at 12% including goodwill and 19% excluding goodwill.

The cash flow and financial ratios are detailed in the following slide:

Strategic Initiatives

Royal Unibrew’s business strategy focuses on differentiated approaches for different market types, as outlined in their strategic framework:

The company is pursuing a three-pronged market strategy:

1. Fueling momentum in growth markets: International, Italy, and France

2. Building momentum in new markets: Norway, Netherlands, and BeLux

3. Optimizing developed markets: Denmark, Finland, and Baltics

This strategic approach appears to be delivering results, with strong performance in growth and new markets offsetting challenges in developed markets. The company reported that Norway and BeNeLux operations are on track to deliver 10% cash ROIC by 2026, in line with strategic targets.

Management emphasized continued focus on operational efficiency, optimized resource use, and cost discipline as key priorities, alongside advancing the sustainability agenda and delivering on long-term financial targets.

Forward-Looking Statements

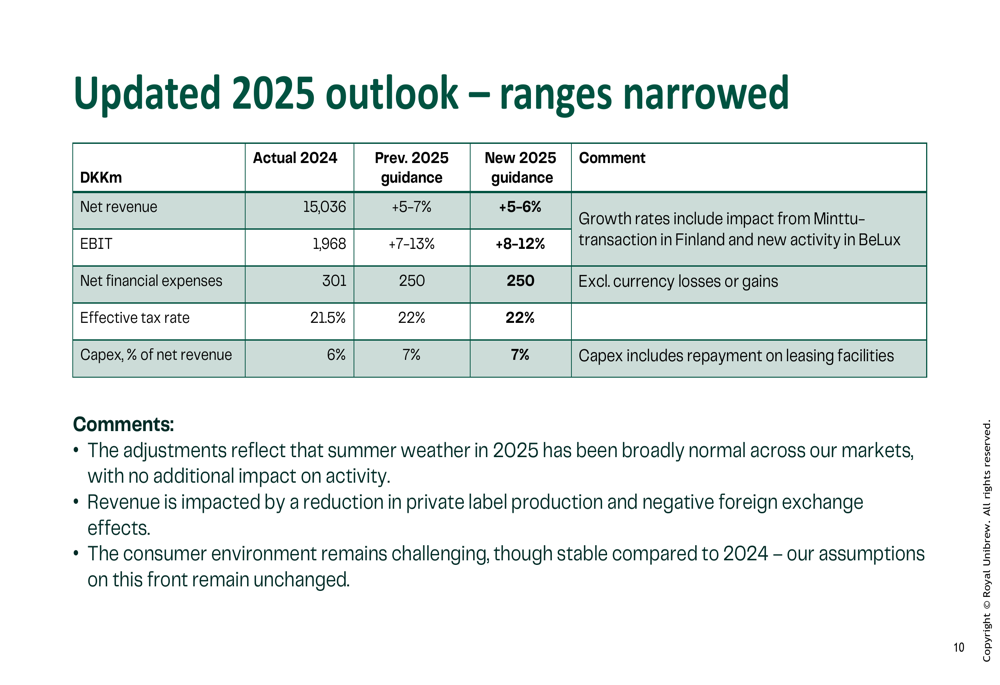

Royal Unibrew has narrowed its full-year 2025 guidance ranges, reflecting increased certainty about performance expectations. The company now projects net revenue growth of 5-6% (previously 5-7%) and EBIT growth of 8-12% (previously 7-13%).

The updated outlook is presented in the following slide:

Management noted that the adjustments reflect normal summer weather conditions across markets with no additional impact on activity. Revenue projections are impacted by a reduction in private label production and negative foreign exchange effects. The consumer environment remains challenging but stable compared to 2024.

The company maintains its long-term commitment to yearly organic EBIT growth of 6-8%, double-digit EPS growth, and improving ROIC. Capital expenditure is expected to remain at approximately 7% of net revenue, with an effective tax rate of around 22%.

Despite the narrowed guidance and recent stock price pressure, Royal Unibrew’s H1 2025 results demonstrate the resilience of its business model and the effectiveness of its geographic diversification strategy in navigating challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.