Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

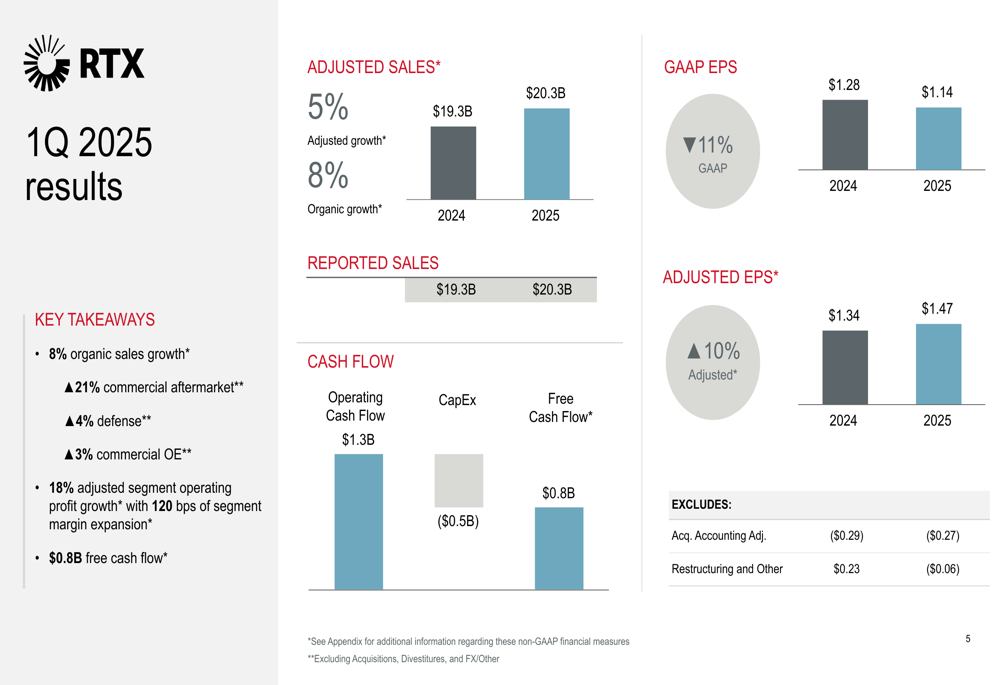

RTX Corporation (NYSE:RTX) released its first quarter 2025 earnings presentation on April 22, showing strong financial performance across all business segments despite emerging concerns about potential tariff impacts. The aerospace and defense giant reported 8% organic sales growth and significant margin expansion, continuing the positive momentum seen in its previous quarter.

The company’s stock reacted with slight volatility, trading down 2.15% to $126.12 at the previous close, following a strong 43.2% total return over the past year. RTX has maintained its 2025 outlook without incorporating potential tariff impacts, signaling confidence in its operational capabilities despite macroeconomic uncertainties.

Quarterly Performance Highlights

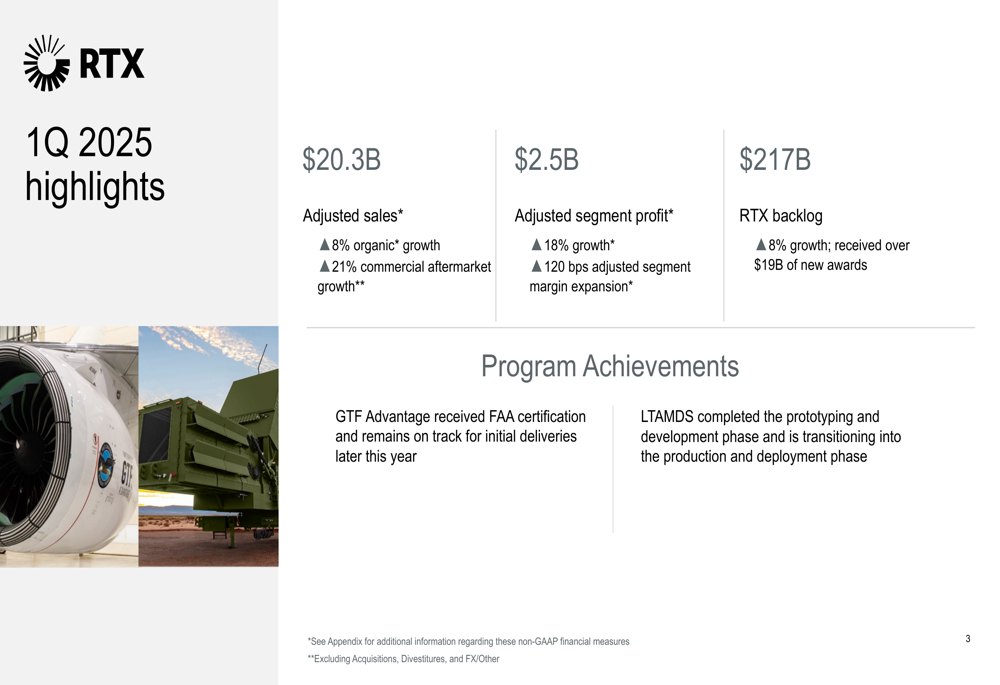

RTX delivered robust financial results for Q1 2025, with adjusted sales reaching $20.3 billion, representing 8% organic growth compared to the same period last year. The company’s adjusted segment profit grew by 18% to $2.5 billion, with a 120 basis point expansion in adjusted segment margins.

As shown in the following highlights slide, RTX secured over $19 billion in new awards during the quarter, contributing to an 8% growth in its backlog, which now stands at $217 billion:

Commercial aftermarket sales were particularly strong, growing 21% year-over-year, while defense sales increased by 4% and commercial original equipment (OE) sales rose by 3%. The company generated $0.8 billion in free cash flow during the quarter.

On the program front, RTX achieved two significant milestones: the GTF Advantage engine received FAA certification and remains on track for initial deliveries later this year, while the Lower Tier Air and Missile Defense Sensor (LTAMDS) completed its prototyping and development phase and is transitioning to production and deployment.

Segment Analysis

All three of RTX’s business segments contributed to the company’s strong performance in Q1 2025.

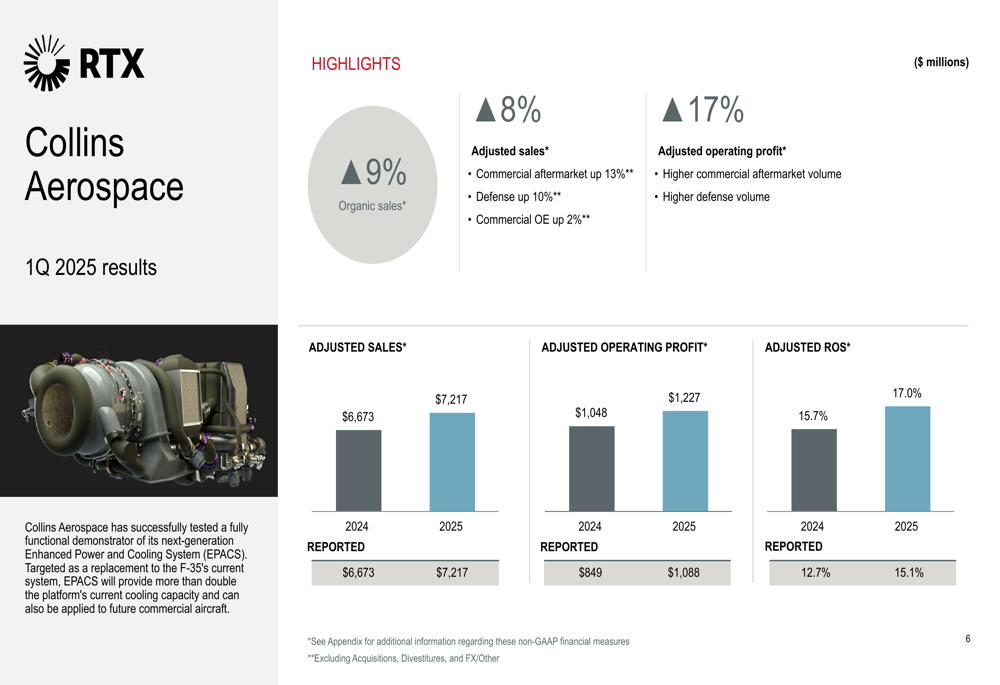

Collins Aerospace reported 9% organic sales growth, with adjusted sales up 8%. The segment’s commercial aftermarket sales increased by 13%, defense sales grew by 10%, and commercial OE sales rose by 2%. Adjusted operating profit improved by 17%, primarily due to higher commercial aftermarket and defense volumes.

As shown in the following segment results slide, Collins Aerospace delivered solid margin improvement:

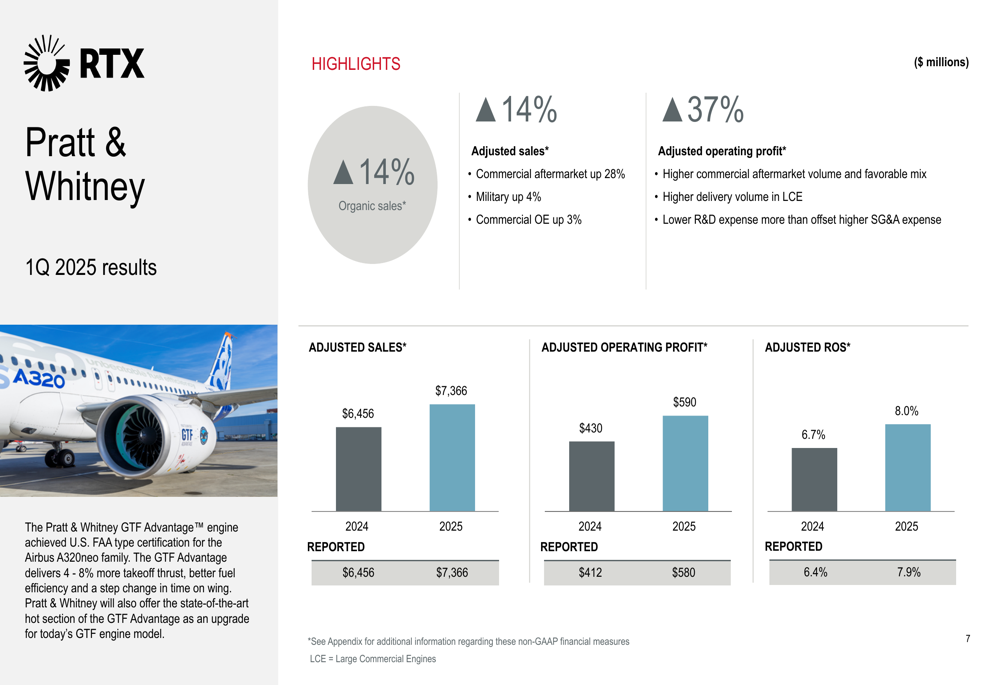

Pratt & Whitney demonstrated even stronger growth, with organic sales up 14% and adjusted sales also increasing by 14%. The segment’s commercial aftermarket sales surged by 28%, while military sales grew by 4% and commercial OE sales increased by 3%. Adjusted operating profit jumped by 37%, driven by higher commercial aftermarket volume, favorable mix, higher delivery volume, and lower R&D expenses.

The following slide illustrates Pratt & Whitney’s exceptional performance:

Raytheon (NYSE:RTN)’s results were more modest but still positive, with organic sales up 2% while adjusted sales decreased by 5% due to the Cybersecurity divestiture. Higher volumes on land and air defense systems were partially offset by lower volumes on air and space defense systems. Despite the sales decline, adjusted operating profit increased by 8%, reflecting favorable mix and improved net productivity.

Tariff Environment

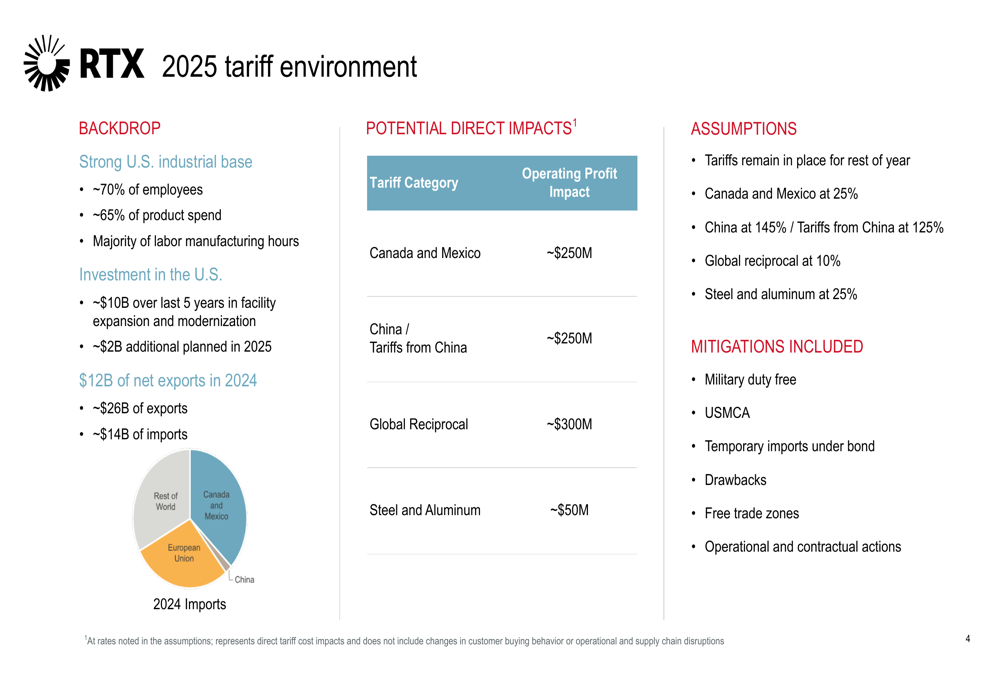

A notable aspect of RTX’s Q1 presentation was its detailed assessment of potential tariff impacts. The company identified approximately $850 million in potential direct impacts across various tariff categories, including Canada and Mexico (~$250M), China (~$250M), Global Reciprocal (~$300M), and Steel and Aluminum (~$50M).

The following slide outlines RTX’s tariff environment analysis:

RTX emphasized its strong U.S. industrial base, with approximately 70% of employees and 65% of product spend in the United States. The company has invested approximately $10 billion over 5 years in U.S. facility expansion, with about $2 billion planned for 2025. RTX also highlighted its positive trade balance, with $12 billion in net exports in 2024 ($26 billion in exports versus $14 billion in imports).

The company has identified several mitigations for potential tariff impacts, including military duty exemptions, USMCA provisions, temporary imports under bond, drawbacks, free trade zones, and various operational and contractual actions.

Detailed Financial Analysis

RTX’s Q1 2025 financial results showed a divergence between GAAP and adjusted figures. GAAP EPS declined by 11% to $1.14 compared to $1.28 in Q1 2024, while adjusted EPS increased by 10% to $1.47 from $1.34 in the prior-year period.

The following slide provides a comprehensive view of the company’s Q1 2025 results:

Free cash flow for the quarter was $0.8 billion, derived from $1.3 billion in operating cash flow minus $0.5 billion in capital expenditures. The company’s cash flow reconciliation shows net income of $1,625 million, with depreciation and amortization adding $1,052 million, offset by a $1,246 million change in working capital and $126 million in other adjustments.

Engine shipments showed solid growth across all categories. In Q1 2025, RTX shipped 51 Military engines (compared to 43 in Q1 2024), 250 Large Commercial engines (versus 232 in Q1 2024), and 518 Pratt & Whitney Canada engines (up from 496 in Q1 2024).

2025 Outlook

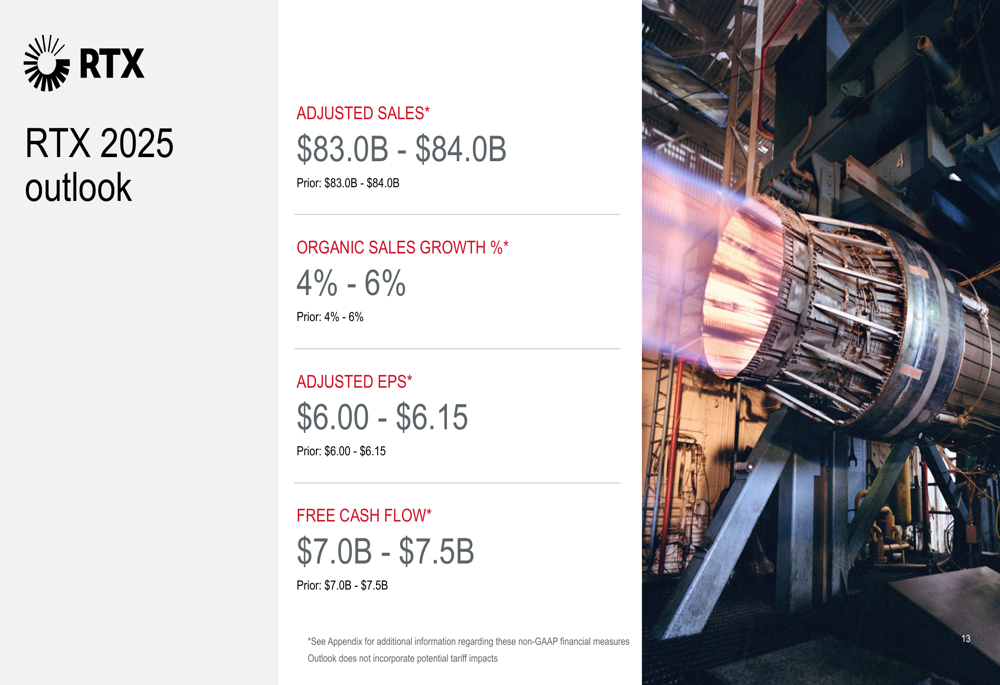

Despite the potential tariff impacts, RTX maintained its full-year 2025 guidance, which does not incorporate these tariff concerns. The company expects adjusted sales of $83.0-$84.0 billion, representing 4-6% organic sales growth.

The following slide outlines RTX’s 2025 outlook:

RTX projects adjusted EPS of $6.00-$6.15 and free cash flow of $7.0-$7.5 billion for the full year. This outlook aligns with the company’s previous guidance provided in its Q4 2024 earnings call, where management projected 4-6% organic sales growth for 2025.

By segment, Collins Aerospace is expected to deliver mid-single-digit organic sales growth, Pratt & Whitney is projected to achieve high-single-digit growth, and Raytheon is forecast to generate mid-single-digit organic growth. All three segments are expected to contribute to margin expansion.

Key Takeaways

RTX’s Q1 2025 presentation emphasized four key takeaways: strong first-quarter financial results, a 2025 outlook that doesn’t incorporate potential tariff impacts, positioning to respond to a changing environment, and operational progress on strategic priorities.

As illustrated in the following key takeaways slide, the company remains confident in its ability to navigate potential challenges:

The company’s strong backlog of $217 billion, including significant growth in international defense orders, provides visibility into future revenue streams. RTX’s focus on operational excellence and strategic initiatives, such as the GTF Advantage certification and LTAMDS transition to production, positions it well for continued growth despite macroeconomic uncertainties.

In the context of RTX’s Q4 2024 performance, where the company reported adjusted EPS of $1.54 (beating forecasts of $1.38) and revenue of $21.62 billion (exceeding expectations of $20.53 billion), the Q1 2025 results demonstrate continued execution of the company’s growth strategy and operational improvements across all business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.