Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

RTX Corporation (NYSE:RTX) presented its second quarter 2025 earnings results on July 22, 2025, revealing strong operational performance across its business segments despite ongoing challenges from tariffs and recent tax legislation changes. The aerospace and defense giant reported significant organic growth but adjusted its earnings outlook downward, reflecting external pressures on its business.

In premarket trading, RTX shares were down 0.7% to $150.50, following the previous day’s close of $151.56, suggesting investors are weighing the company’s strong operational performance against its reduced earnings guidance.

Quarterly Performance Highlights

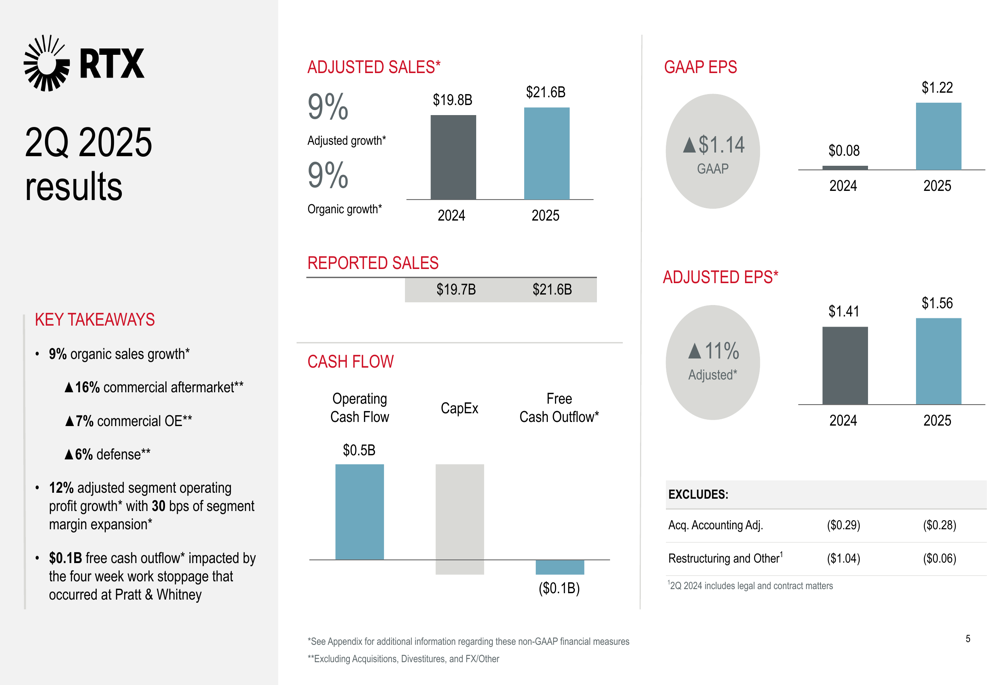

RTX reported adjusted sales of $21.6 billion for the second quarter, representing 9% organic growth compared to the same period last year. The company’s adjusted segment profit increased by 12% to $2.7 billion, with margin expansion of 30 basis points.

Commercial aftermarket business continued to be a standout performer with 16% growth, while commercial original equipment (OE) sales increased by 7%. Defense-related sales grew by 6%, demonstrating balanced growth across RTX’s portfolio.

As shown in the following comprehensive overview of Q2 results:

Despite the strong operational performance, RTX reported a free cash outflow of $0.1 billion for the quarter, which the company attributed to a four-week work stoppage at Pratt & Whitney. On a GAAP basis, earnings per share reached $1.22, while adjusted EPS came in at $1.56, representing an 11% increase from the prior year.

The company’s backlog grew to $236 billion, bolstered by Pratt & Whitney securing orders for over 1,000 GTF engines and Raytheon (NYSE:RTN) receiving more than $5 billion in integrated air and missile defense awards.

Segment Performance Analysis

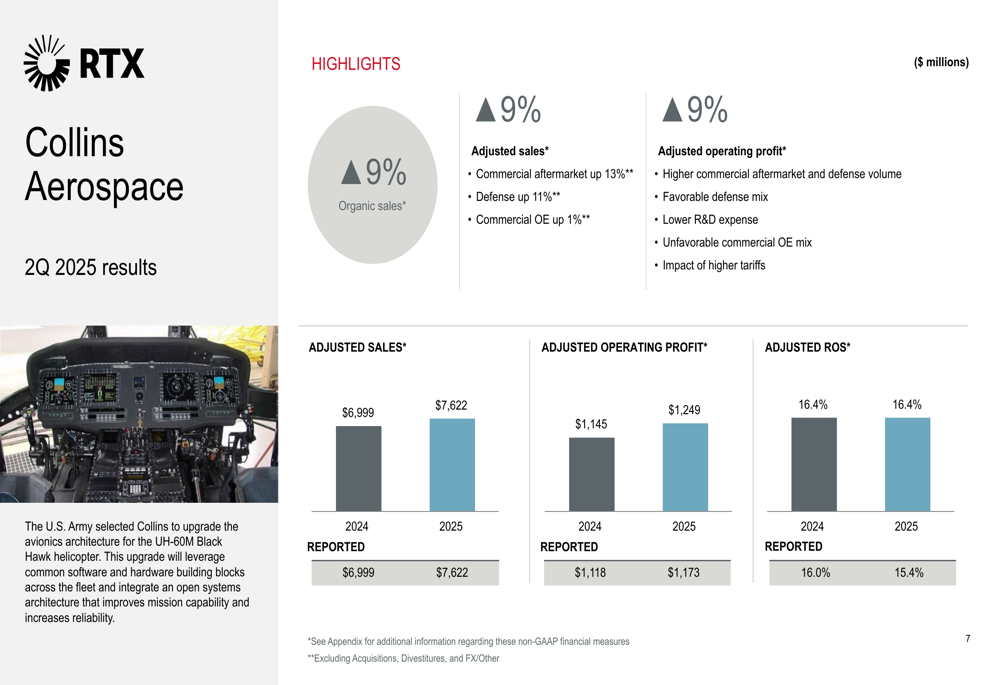

Collins Aerospace delivered adjusted sales of $7.62 billion, up 9% from the previous year, with commercial aftermarket sales increasing by 13% and defense sales up 11%. The segment’s adjusted operating profit also grew by 9% to $1.25 billion, maintaining its robust operating margin of 16.4%.

As illustrated in the Collins Aerospace results:

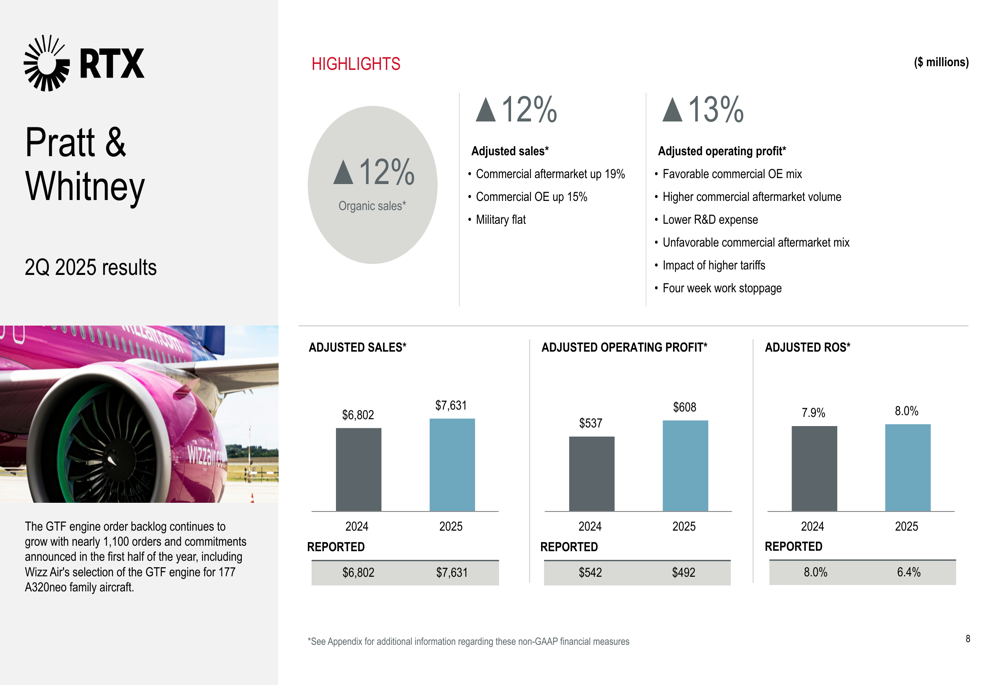

Pratt & Whitney demonstrated the strongest growth among RTX’s segments, with adjusted sales increasing by 12% to $7.63 billion. Commercial aftermarket sales surged by 19%, while commercial OE sales grew by 15%. The segment’s adjusted operating profit rose by 13% to $608 million, improving its operating margin to 8.0% from 7.9% in the prior year, despite the impact of a four-week work stoppage.

The following chart details Pratt & Whitney’s performance:

Raytheon’s adjusted sales increased by 6% to $7.0 billion, driven by higher volumes in land and air defense systems and naval programs. The segment achieved the most significant profit improvement with a 14% increase in adjusted operating profit to $809 million, expanding its operating margin by 80 basis points to 11.6%.

Strategic Initiatives

RTX highlighted several strategic priorities focused on execution, innovation, and leveraging its scale. The company reported that Pratt & Whitney’s PW1100 MRO output is on track for over 30% improvement year-over-year, while Raytheon is leveraging its CORE program to significantly increase output on GEM-T, Coyote, and AMRAAM systems.

On the innovation front, RTX announced partnerships with Shield AI to integrate AI-based capabilities into select products and with Kongsberg to co-develop GhostEye subcomponents. The company is also leveraging its proprietary data and AI platform to achieve a 30% reduction in avionics software development times.

Portfolio optimization continues with the announced divestiture of Collins’ Simmonds Precision Products business and the completed divestiture of Collins’ Actuation business, aligning with RTX’s strategy of focusing on core capabilities.

Updated Outlook & Guidance

RTX updated its full-year 2025 guidance, increasing its adjusted sales outlook to $84.75-$85.5 billion from the previous range of $83.0-$84.0 billion. The company also raised its organic sales growth projection to 6-7% from the previous 4-6%.

However, despite the stronger sales outlook, RTX reduced its adjusted EPS guidance to $5.80-$5.95 from the previous $6.00-$6.15, citing the expected impact of tariffs and changes associated with recently enacted tax legislation. The company maintained its free cash flow outlook at $7.0-$7.5 billion.

The following slide illustrates RTX’s updated 2025 outlook:

Market Reaction & Conclusion

The slight decline in RTX’s premarket trading suggests investors are processing the mixed guidance update, with strong operational performance and increased sales projections offset by reduced earnings expectations due to external factors.

This reaction follows a pattern seen after the company’s Q1 2025 results, when the stock fell 8.86% despite beating expectations. At that time, RTX had warned about potential tariff impacts of approximately $850 million annually, concerns that appear to be materializing in the current guidance adjustment.

RTX continues to demonstrate strong operational execution and robust demand across its aerospace and defense businesses. The company remains committed to its capital return plan, expecting to return $37 billion to shareholders from the merger through 2025, including an 8% dividend increase implemented in Q2 2025.

While external challenges from tariffs and tax changes are creating headwinds for earnings growth, RTX’s substantial backlog of $236 billion and continued strong demand in commercial aerospace and defense markets position the company for sustained long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.