Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Russel Metals Inc. (TSX:RUS) released its Q2 2025 earnings on August 8, followed by a September 2025 company update presentation that highlighted the company’s strong quarterly performance and ongoing strategic transformation. As one of North America’s largest metals service center operators, Russel maintains a leading position in Canada and a growing presence in the U.S. South and Midwest regions.

The company’s stock currently trades at $39.99, well above its 52-week low of $34.62 but below its high of $46.87, reflecting mixed investor sentiment despite solid operational performance. Following the Q2 earnings release, the stock experienced a 2.18% decline in after-hours trading, primarily due to revenue falling short of analyst expectations despite quarter-over-quarter growth.

Quarterly Performance Highlights

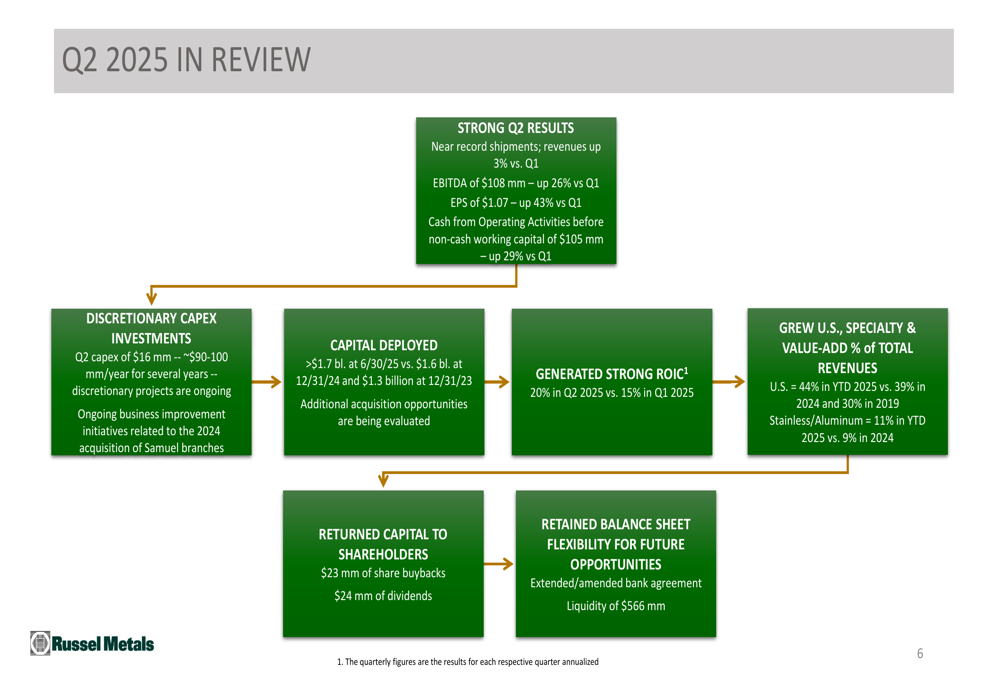

Russel Metals reported robust Q2 2025 results, achieving near-record shipments and demonstrating significant improvements across key financial metrics compared to the previous quarter.

As shown in the following quarterly performance summary:

The company posted revenues up 3% quarter-over-quarter, with EBITDA reaching $108 million, representing a 26% increase from Q1. Earnings per share climbed to $1.07, a substantial 43% improvement over the previous quarter, exceeding analyst expectations of $1.03. Cash from operating activities before non-cash working capital reached $105 million, up 29% from Q1.

These results reflect Russel’s operational efficiency and effective cost management, as evidenced by the 180 basis point improvement in gross margins noted in the earnings call. However, the company’s revenue of $1.21 billion fell short of the forecasted $1.25 billion, representing a 3.2% miss that likely contributed to the post-earnings stock decline.

Strategic Initiatives & Business Transformation

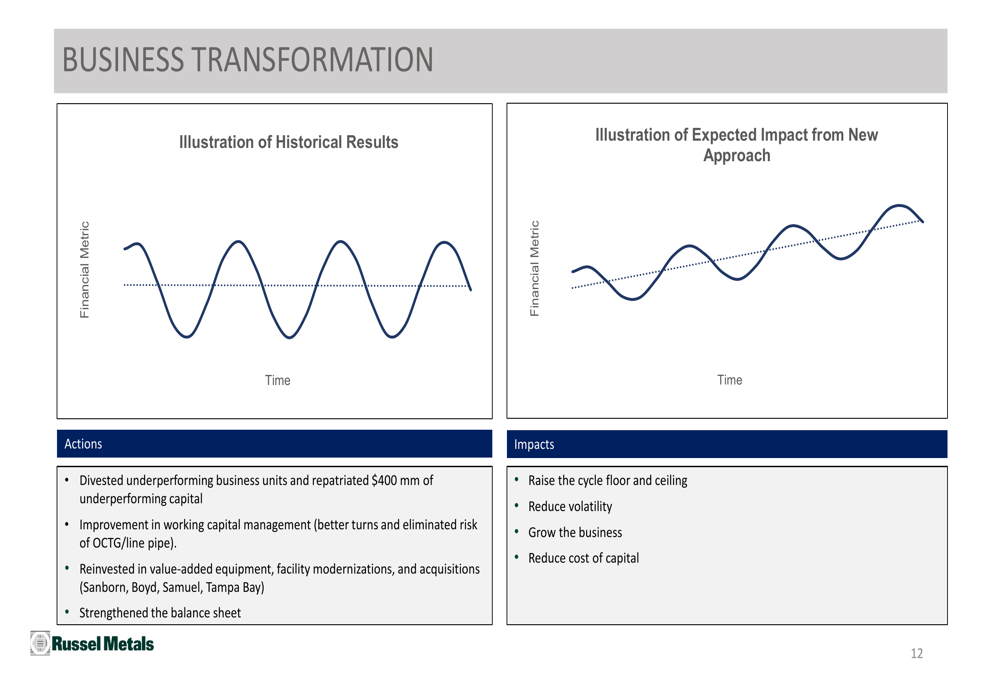

Russel Metals continues to execute its strategic transformation aimed at reducing business cyclicality and improving returns through diversification and value-added services.

The company’s transformation strategy is illustrated in the following chart:

Key initiatives include divesting underperforming business units, improving working capital management, and strategically reinvesting in value-added equipment and acquisitions. These efforts are expected to raise both the floor and ceiling of the business cycle while reducing volatility, ultimately leading to more consistent performance and potentially a lower cost of capital.

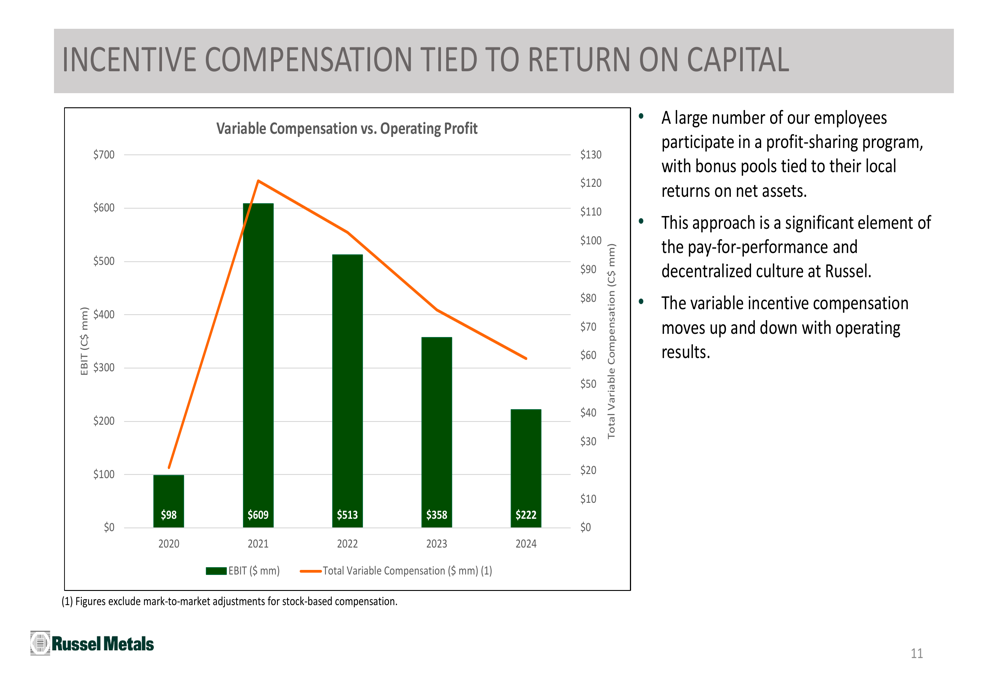

The company’s incentive structure aligns employee compensation with shareholder interests by tying bonuses to local returns on net assets, as demonstrated in this compensation chart:

This alignment has proven effective, with variable compensation tracking closely with operating profit. In 2024, the company reported EBIT of C$222 million and total variable compensation of C$41 million, demonstrating the direct relationship between performance and rewards.

Financial Position & Capital Allocation

Russel Metals maintains a strong financial position with significant liquidity and a conservative capital structure, providing flexibility for both organic growth and strategic acquisitions.

As of June 30, 2025, the company reported liquidity of $566 million and a net debt to invested capital ratio of just 6%. In March 2025, Russel issued $300 million of investment-grade term debt at a 4.423% interest rate and extended its bank facility in April 2025, further strengthening its financial foundation.

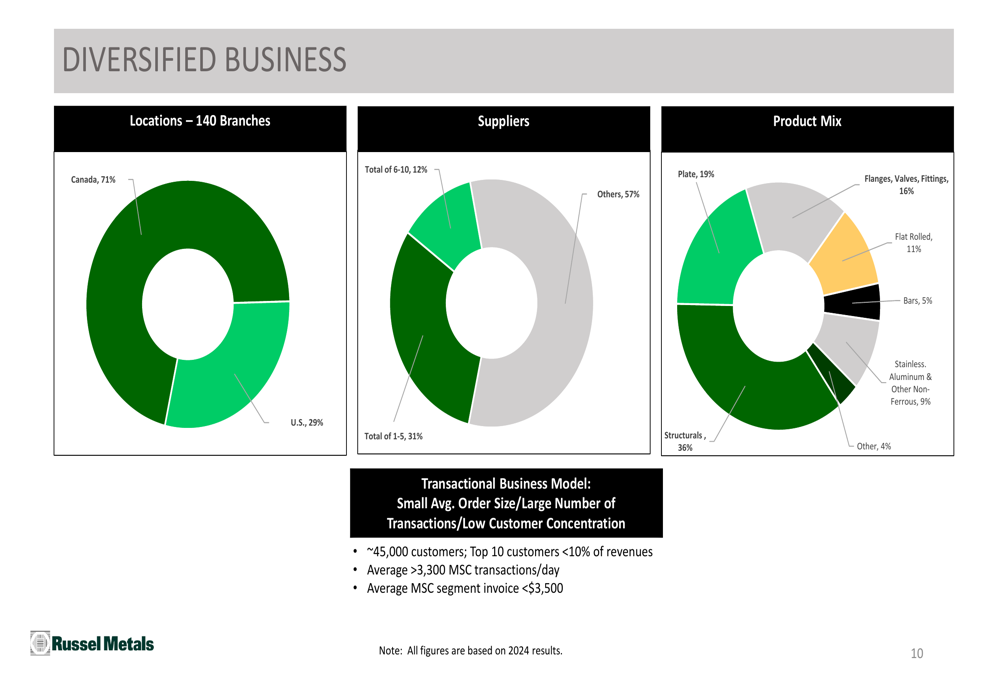

The company’s diversified business model spans multiple geographies, products, and customer segments, reducing concentration risk and enhancing stability:

With 140 branches (71% in Canada and 29% in the U.S.), Russel serves approximately 45,000 customers, with its top 10 customers representing less than 10% of total revenues. This diversification extends to its product mix, which includes structurals (36%), plate (19%), and flanges, valves, and fittings (16%), among other products.

The company’s 2024 revenue of $4.3 billion was distributed across three segments: Metals Service Centers (67%), Energy Field Stores (23%), and Steel Distributors (9%). During the earnings call, management highlighted the growing contribution from non-ferrous metals, which now represent 11% of revenues, and the continued expansion in the U.S. market, which accounts for 44% of year-to-date revenues.

Forward-Looking Statements

Looking ahead, Russel Metals projects stable demand for Q3 2025, though management acknowledged potential seasonal slowdowns during the earnings call. The company continues to explore merger and acquisition opportunities, with executives noting a strong pipeline and significant "dry powder" for opportunistic deals.

Management anticipates potential capital optimization of $30-50 million from the recent Samuels acquisition and remains focused on expanding its non-ferrous metals portfolio. Analyst guidance for upcoming quarters includes EPS forecasts ranging from $0.55 to $0.70 and revenue projections between $817.47 million and $914.78 million.

Key challenges identified include supply chain disruptions, tariff uncertainties, and potential impacts from agricultural sector struggles. During the earnings call, executives emphasized the company’s adaptability in sourcing materials and pricing strategies to navigate these challenges, with CEO Marty Djarowski noting, "We’re pretty adaptable of where we’re sourcing from and how we’re sourcing material."

With its strong financial position, diversified business model, and strategic transformation initiatives, Russel Metals appears well-positioned to navigate market uncertainties while pursuing both organic growth and strategic acquisitions in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.