Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

RXO Inc (NYSE:RXO) reported its second quarter 2025 results on August 7, 2025, showing sequential improvement from the challenging first quarter while continuing to navigate a soft freight market. The company’s stock was down 4.4% in premarket trading to $14.76, suggesting investors may have been looking for stronger results despite the progress made.

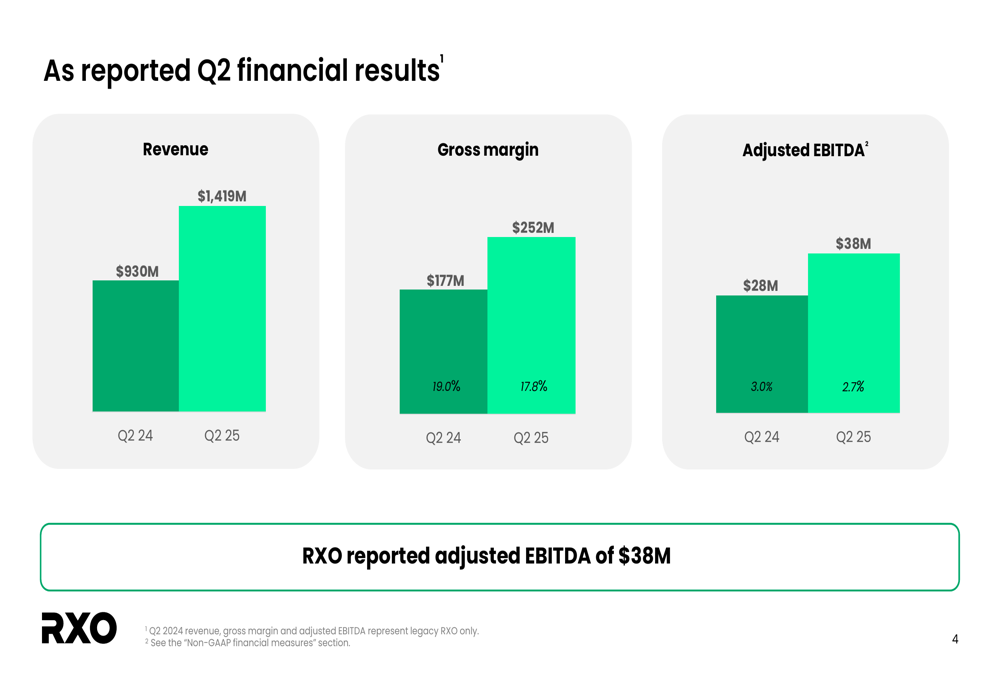

The freight brokerage company posted $1.42 billion in revenue for Q2, representing a substantial 52.6% increase from the $930 million reported in the same period last year, largely reflecting the impact of the Coyote Logistics acquisition.

Quarterly Performance Highlights

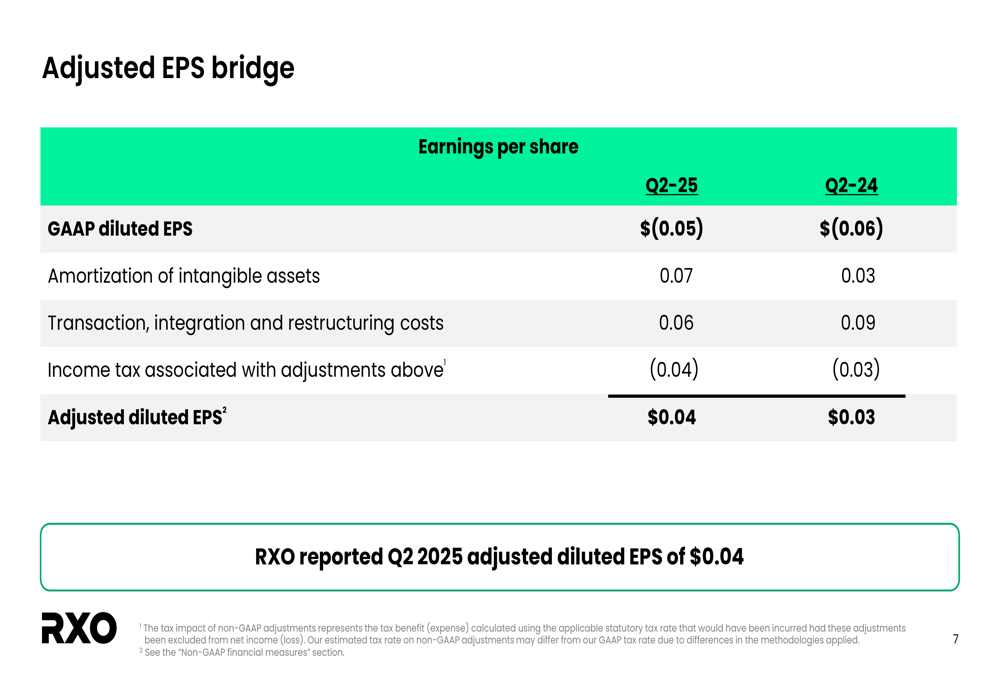

RXO reported adjusted EBITDA of $38 million in Q2 2025, up from $28 million in Q2 2024, though the margin decreased slightly from 3.0% to 2.7%. The company also posted adjusted diluted earnings per share of $0.04, compared to $0.03 in the prior-year period.

As shown in the following chart of quarterly financial results:

Gross margin increased to $252 million from $177 million year-over-year, though as a percentage of revenue it decreased from 19.0% to 17.8%. This reflects the ongoing margin pressure in the freight market despite the company’s efforts to improve profitability.

The company highlighted several key achievements in the quarter, including improved truckload profitability, initial purchased transportation benefits from coverage migration, brokerage volume growth driven by less-than-truckload (LTL), continued momentum in complementary services led by Last Mile, and strong adjusted free cash flow conversion.

Segment Performance

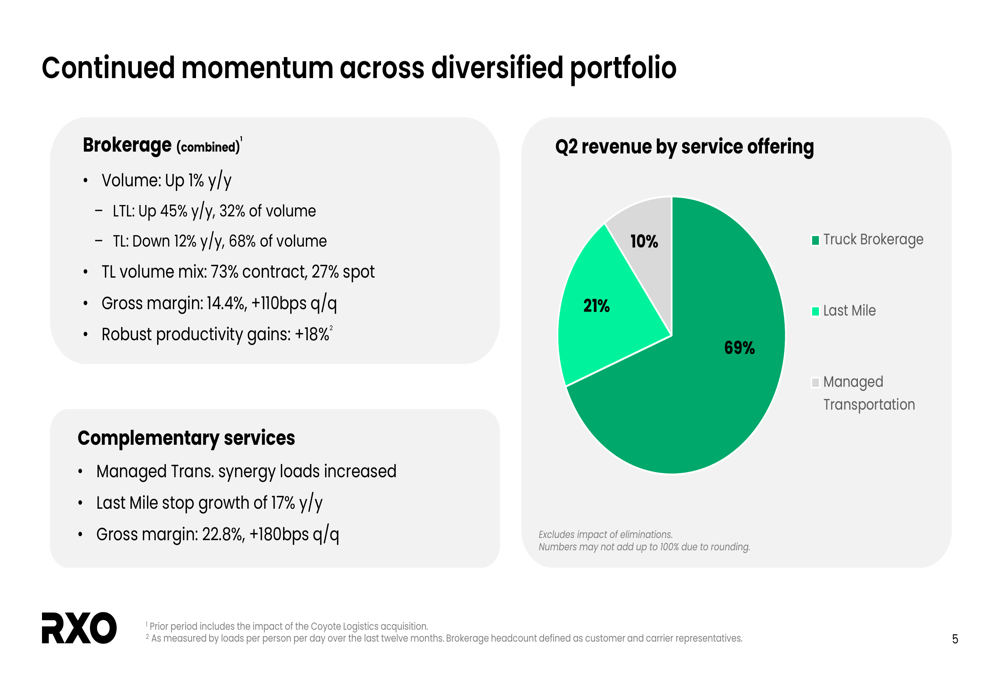

RXO’s revenue diversification across service offerings shows the company’s balanced approach to the transportation market. Truck brokerage remains the dominant segment at 69% of revenue, with Last Mile at 21% and Managed Transportation at 10%, as illustrated in this breakdown:

In the brokerage segment, overall volume increased 1% year-over-year, with LTL volume surging 45% while truckload (TL) volume declined 12%. The company’s truckload mix remains heavily weighted toward contract business at 73% versus 27% spot market exposure.

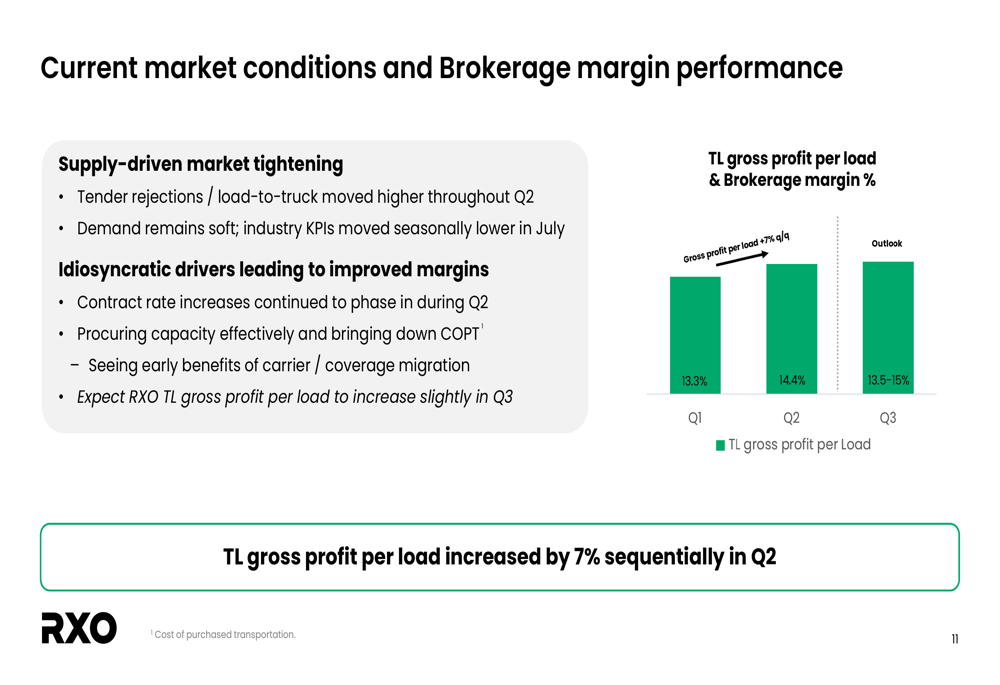

Truckload revenue per load increased 3% year-over-year, marking the third consecutive quarter of year-over-year growth. More importantly, TL gross profit per load increased 7% sequentially in Q2, representing the largest percentage increase in three years.

The following chart illustrates the company’s brokerage margin performance and outlook:

RXO noted that market conditions showed supply-driven tightening during Q2, with tender rejections and load-to-truck ratios moving higher throughout the quarter. However, demand remains soft, and industry key performance indicators moved seasonally lower in July.

Technology Integration Progress

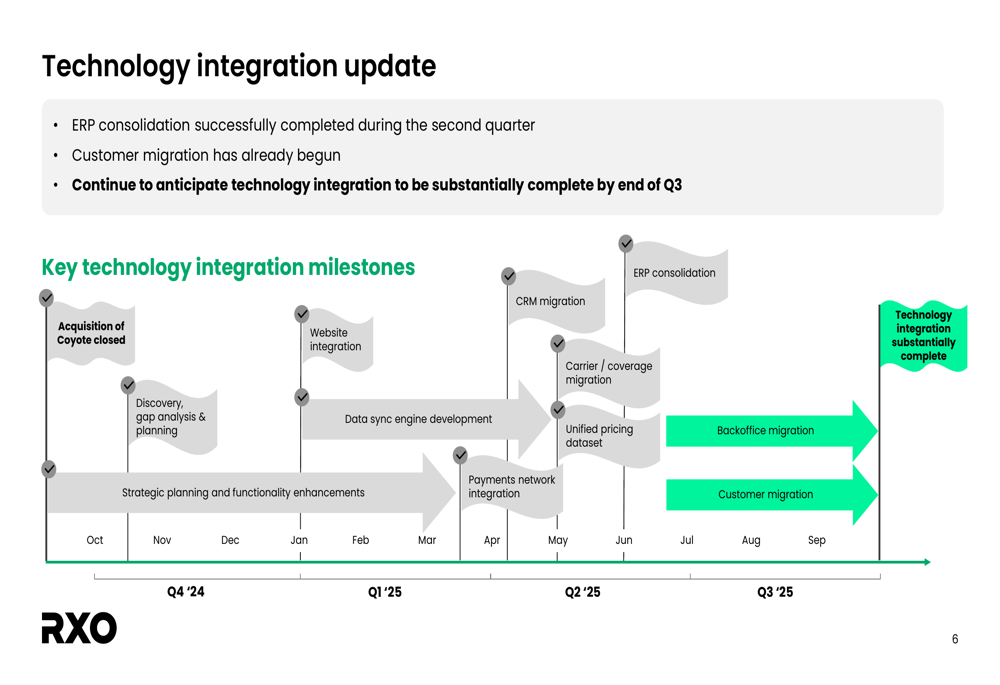

A significant focus for RXO has been the integration of Coyote Logistics, with technology integration being a critical component. The company successfully completed ERP consolidation during the second quarter and has already begun customer migration.

The technology integration timeline shows substantial progress with several key milestones achieved:

RXO continues to anticipate that technology integration will be substantially complete by the end of Q3 2025, which should enable further operational efficiencies and synergies.

Financial Position & Cash Flow

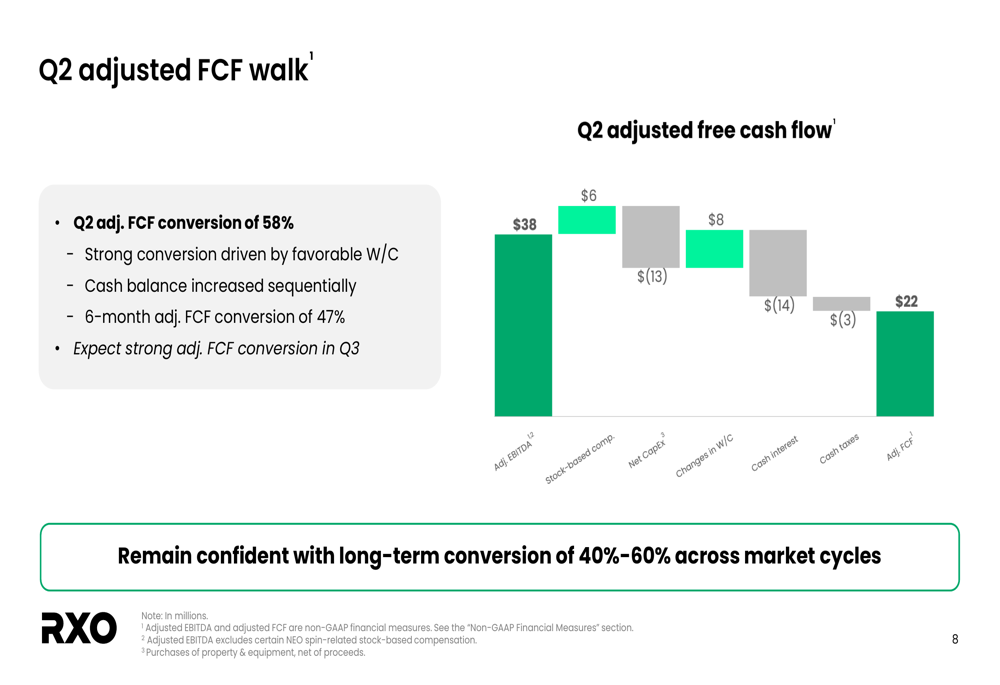

The company reported strong adjusted free cash flow conversion of 58% in Q2, driven by favorable working capital. The cash balance increased sequentially, and the six-month adjusted free cash flow conversion stood at 47%.

The following waterfall chart illustrates how RXO converted its adjusted EBITDA to free cash flow:

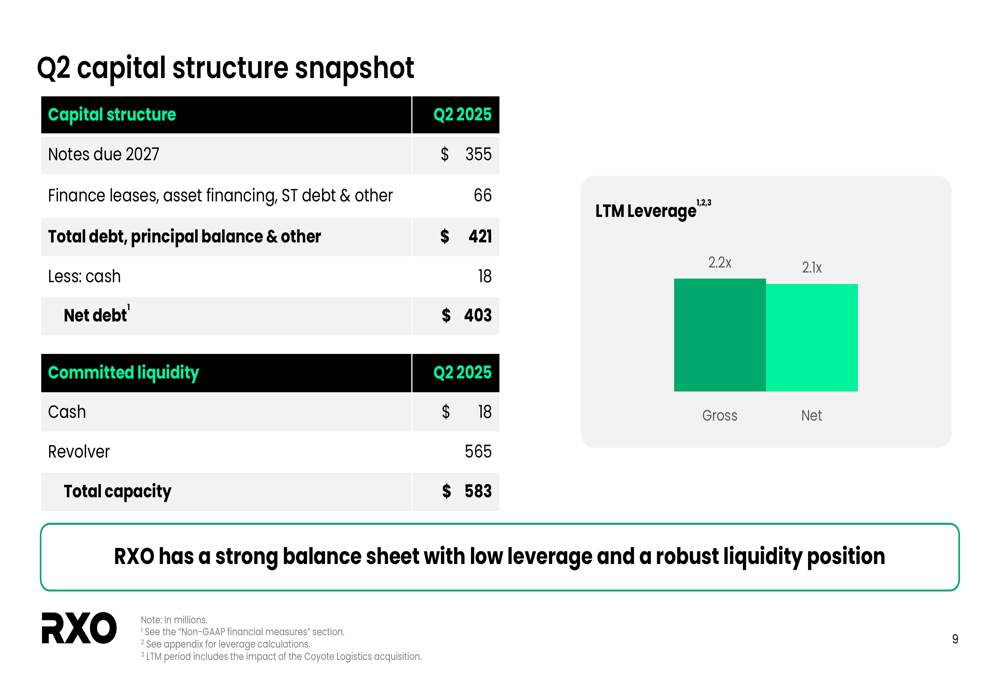

RXO maintains a strong balance sheet with low leverage and robust liquidity. The company’s net debt stood at $403 million with LTM leverage of 2.2x gross and 2.1x net. Total (EPA:TTEF) liquidity was $583 million, consisting of $18 million in cash and $565 million available on its revolving credit facility.

The capital structure snapshot provides a clear picture of RXO’s financial position:

Outlook & Guidance

Looking ahead to Q3 2025, RXO provided adjusted EBITDA guidance of $33-$43 million. The company expects brokerage volume to be approximately flat year-over-year, with brokerage gross margin projected between 13.5% and 15.0%.

For the full year 2025, RXO provided several modeling assumptions, including capital expenditures of $65-$75 million, depreciation of $65-$75 million, amortization of intangibles of $45-$50 million, and net interest expense of $32-$36 million. The company expects restructuring, transaction, and integration expenses to decrease significantly in the second half compared to the first half of the year.

RXO also outlined its balanced capital allocation strategy, focusing on organic growth, share repurchases through its $125 million program, and opportunistic M&A complementary to the company’s strategy.

The adjusted EPS bridge provides insight into how RXO’s earnings are calculated:

Despite ongoing challenges in the freight market, RXO’s Q2 results show sequential improvement from Q1, with the company making progress on integration milestones while maintaining a focus on profitability improvement and cash flow generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.