5 big analyst AI moves: Nvidia guidance warning; Snowflake, Palo Alto upgraded

Introduction & Market Context

Rayonier Advanced Materials (NYSE:RYAM) presented its second quarter 2025 financial results on August 6, revealing a challenging period for the specialty cellulose producer. The company reported an operating loss amid headwinds from tariffs, foreign exchange impacts, and operational challenges, leading to reduced full-year guidance. RYAM’s stock closed at $3.83 on August 5, near its 52-week low of $3.45, reflecting ongoing investor concerns following a disappointing first quarter.

The presentation positioned 2025 as a "trough year" with Q2 marking the low point, while outlining an ambitious transformation strategy aimed at returning to growth in 2026 and beyond. Management emphasized that current challenges are largely temporary, with plans to divest underperforming segments and focus on higher-margin cellulose specialties.

Quarterly Performance Highlights

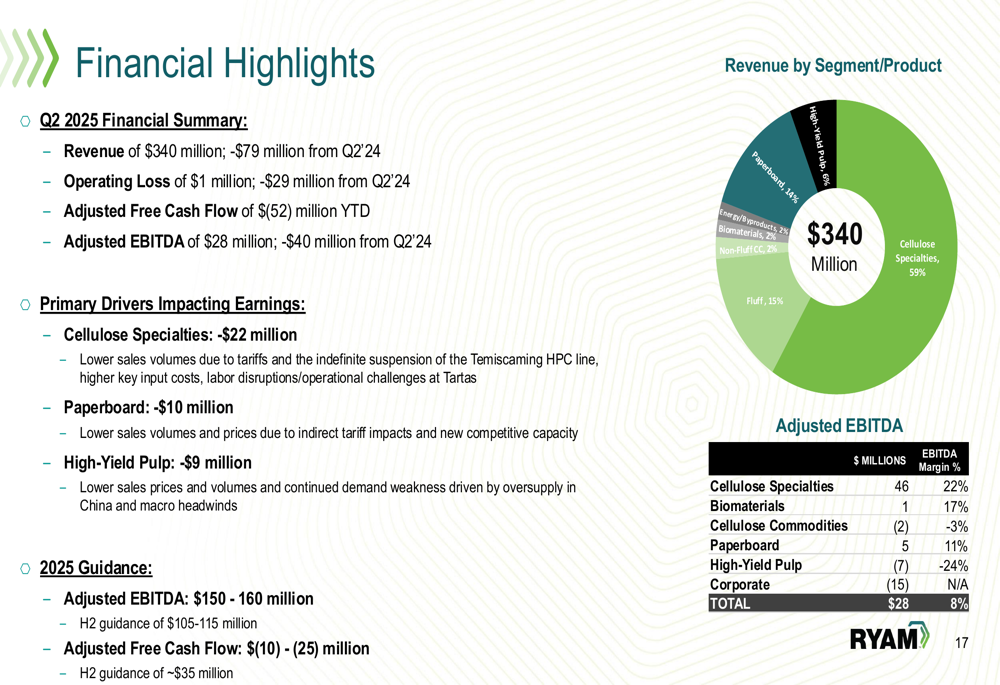

RYAM reported Q2 2025 revenue of $340 million, down $79 million from Q2 2024, with an operating loss of $1 million compared to an operating income of $28 million in the prior-year period. The company’s adjusted free cash flow stood at $(52) million year-to-date.

As shown in the following financial highlights from the presentation:

Performance varied significantly across business segments. Cellulose Specialties, which represents 59% of revenue, generated $208 million in sales with an operating income of $29 million and a healthy EBITDA margin of 22%. However, sales decreased $33 million due to lower volumes driven by tariff-related order pauses.

In contrast, High-Yield Pulp continued to struggle with a $(7) million operating loss and a negative EBITDA margin of (24)%, while Paperboard broke even at the operating income level with an 11% EBITDA margin.

Strategic Initiatives

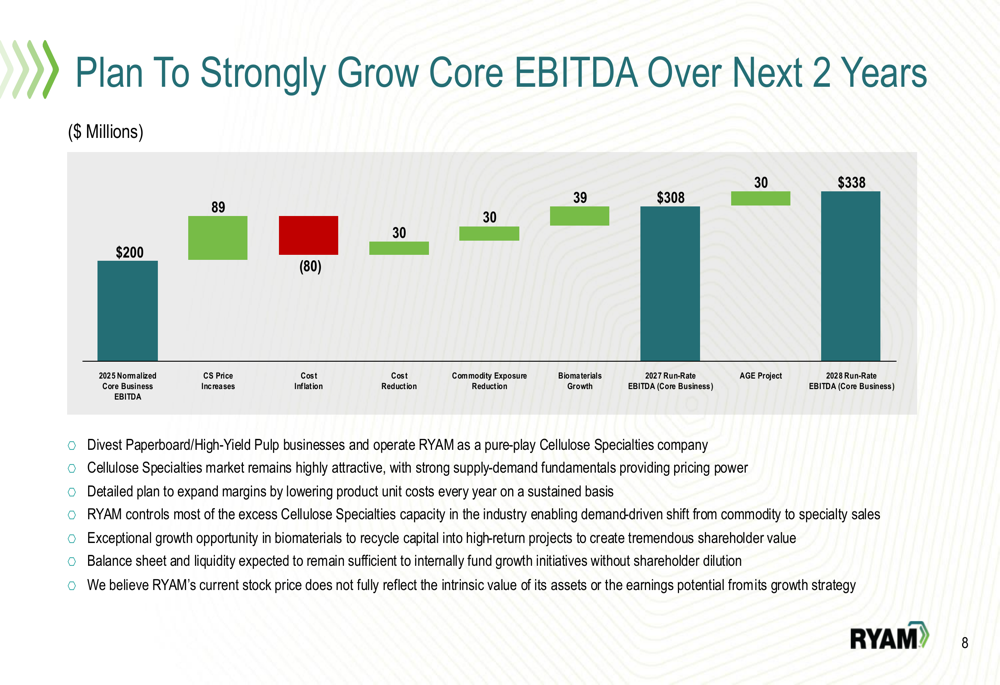

The presentation outlined RYAM’s path to recovery and growth, with a comprehensive plan to increase normalized core business EBITDA from $200 million in 2025 to approximately $338 million by 2028. This growth strategy is illustrated in the following waterfall chart:

Key drivers of this growth include Cellulose Specialties price increases (+$89 million), cost reduction initiatives (+$30 million), reduced commodity exposure (+$30 million), biomaterials growth (+$39 million), and the Altamaha Green Energy (AGE) project (+$30 million), partially offset by cost inflation (-$80 million).

A central element of RYAM’s strategy involves divesting its Paperboard and High-Yield Pulp businesses to operate as a pure-play Cellulose Specialties company. Management emphasized that the company’s balance sheet and liquidity remain sufficient to fund growth initiatives without shareholder dilution.

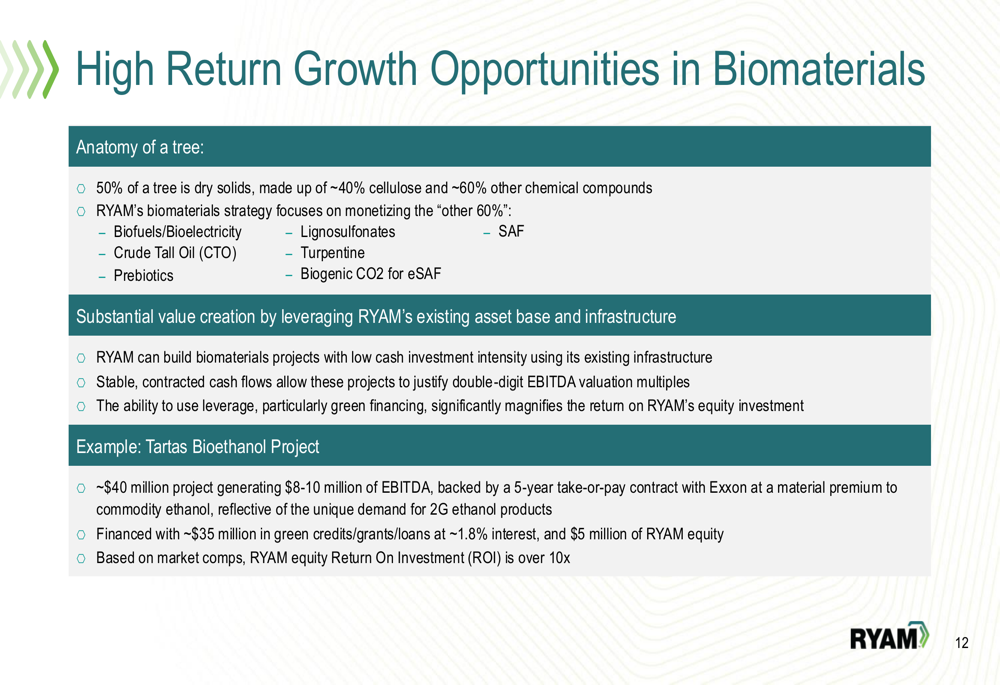

The company is also focusing on high-return opportunities in biomaterials, leveraging its existing infrastructure to monetize additional components of wood beyond cellulose. As shown in the following slide detailing these opportunities:

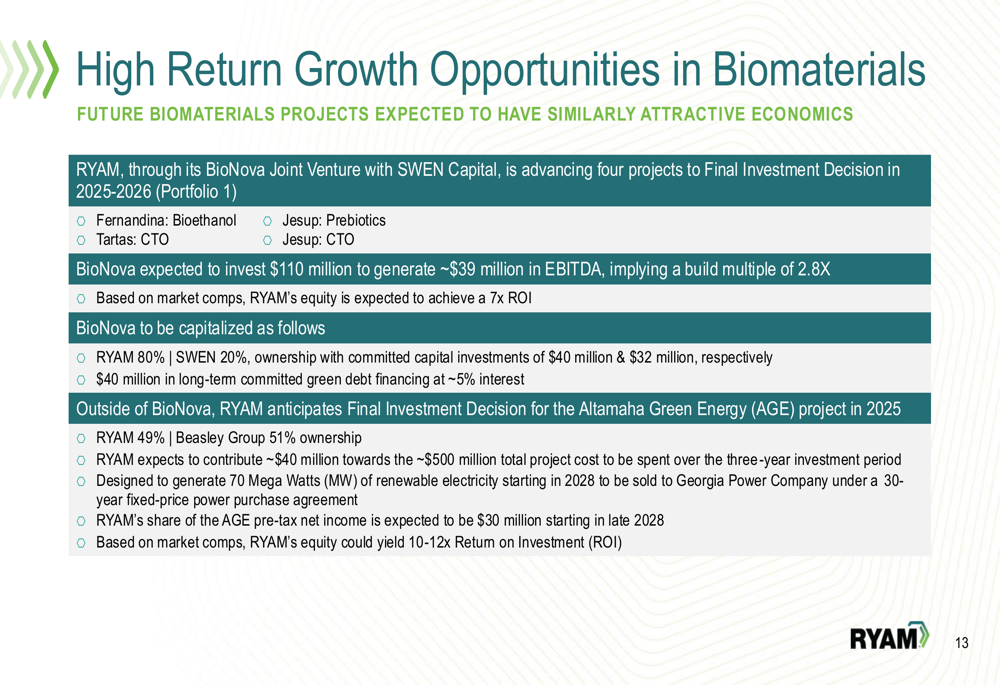

RYAM highlighted several biomaterials projects with attractive economics, including a partnership with SWEN Capital through their BioNova Joint Venture. These projects are expected to generate significant returns, as illustrated below:

Detailed Financial Analysis

The presentation acknowledged several challenges impacting 2025 performance, including a $21 million EBITDA headwind from tariffs, $18 million from extraordinary operational issues (including labor strikes and power outages), and $12 million in non-cash environmental charges. These factors contributed to the reduction in 2025 guidance, with adjusted EBITDA now expected at $150-160 million and adjusted free cash flow at $(10)-(25) million.

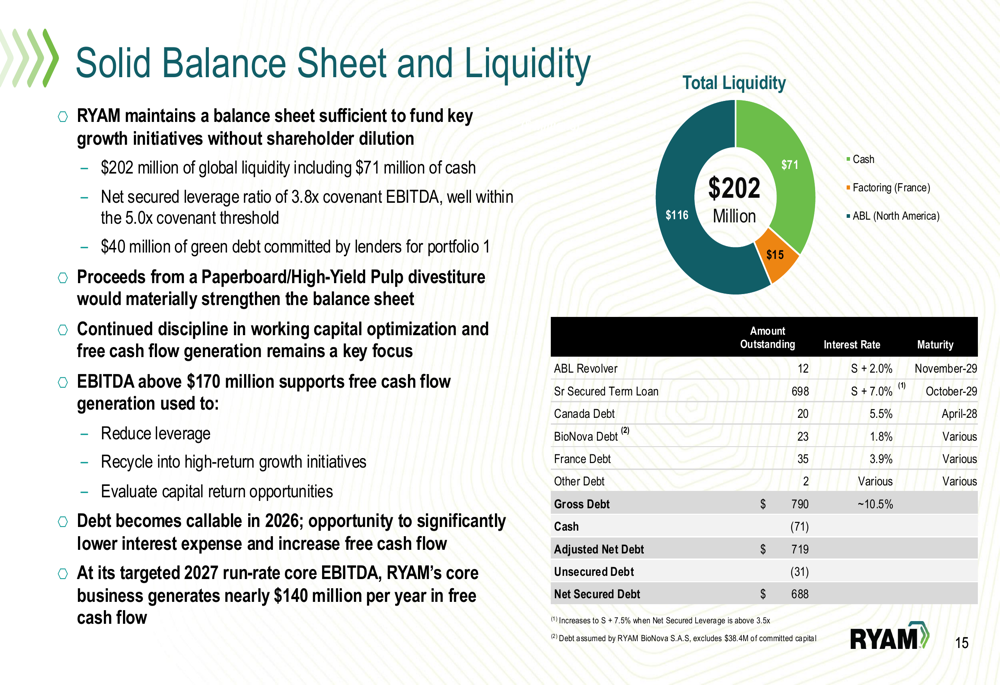

Despite these challenges, RYAM maintains a solid balance sheet with $202 million in global liquidity, including $71 million in cash, as shown in the following liquidity breakdown:

The company expects stronger performance in the second half of 2025, with projected EBITDA of $105-115 million and adjusted free cash flow of approximately $35 million.

This guidance represents a further reduction from the $175-185 million EBITDA outlook provided after Q1 results, indicating continued deterioration in the company’s near-term prospects.

Forward-Looking Statements

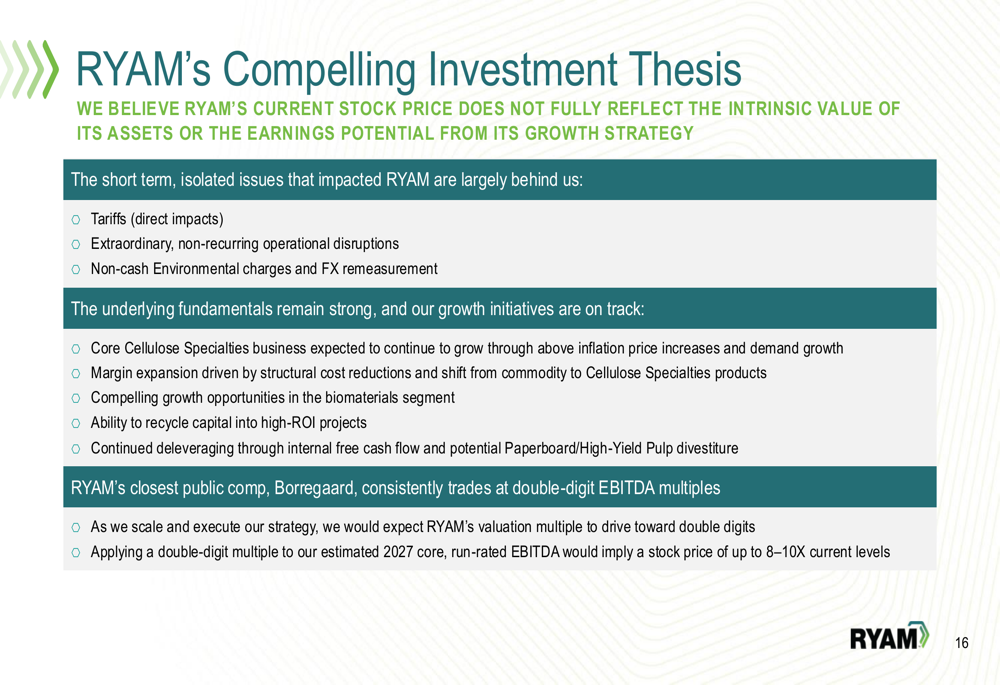

RYAM’s presentation emphasized that the company’s current stock price does not reflect its intrinsic value or earnings potential. Management noted that RYAM’s closest public competitor, Borregaard, consistently trades at double-digit EBITDA multiples, suggesting significant upside potential as the company executes its transformation plan.

The company’s compelling investment thesis highlights that many of the issues impacting performance are temporary and largely behind them:

Looking ahead, RYAM plans to restore profitability at its Temiscaming facility with the goal of pursuing a divestiture in 2026. The company also expects to benefit from growing Cellulose Specialties markets, with analysts forecasting growth of 45,000 MT in 2026 and 35,000 MT in 2027.

Management expressed confidence in capturing this growth through requalification of Cellulose Specialties production from Temiscaming to other sites and additional sales of Ethers and other CS products, projecting approximately $30 million of cumulative incremental EBITDA by 2027.

While RYAM faces significant near-term challenges, the presentation outlined a clear strategy for transformation and growth that could position the company for improved performance in 2026 and beyond. Investors will be watching closely to see if management can execute on these plans and reverse the stock’s downward trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.