United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

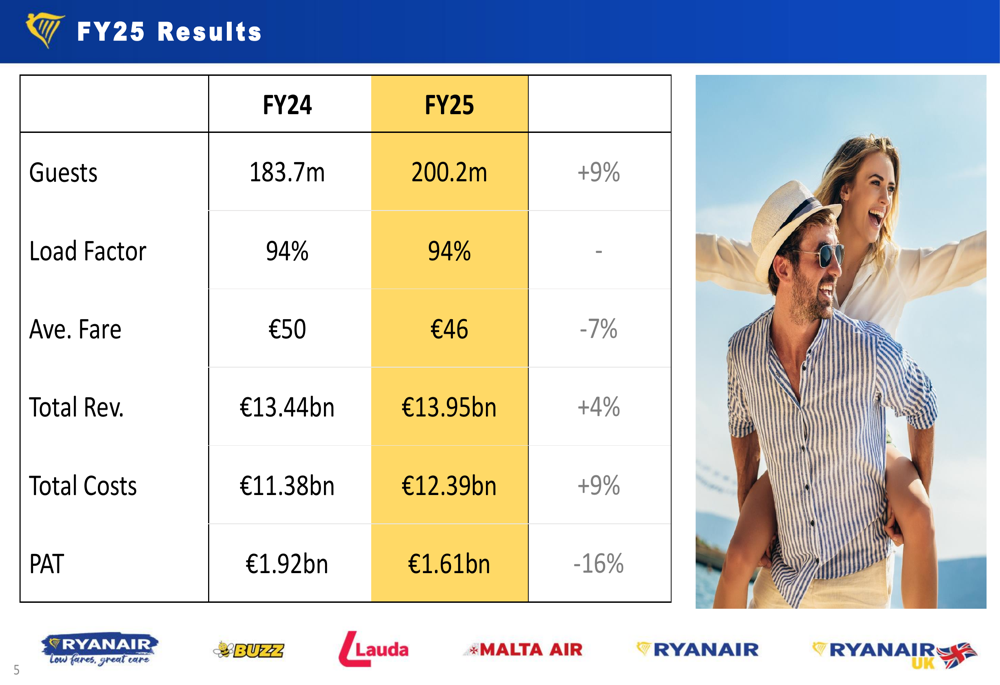

Ryanair Holdings (NASDAQ:RYAAY) (LON:RYA) presented its fiscal year 2025 results on May 19, 2025, revealing a mixed performance characterized by strong passenger growth but declining profitability. The Irish low-cost carrier reported a 16% drop in profit after tax despite carrying a record 200.2 million passengers during the year. Ryanair shares have declined 5.3% over the past week, closing at $21.78 before the presentation.

Quarterly Performance Highlights

Ryanair achieved a 9% increase in passenger numbers to 200.2 million in FY25, becoming the first European airline to carry 200 million guests in a single year. However, this growth was accompanied by a 7% decline in average fares to €46, reflecting competitive pricing pressures across European routes.

Total (EPA:TTEF) revenue increased by 4% to €13.95 billion, but this was outpaced by a 9% rise in total costs to €12.39 billion. As a result, profit after tax fell 16% to €1.61 billion. Load factor remained steady at 94% throughout the fiscal year.

As shown in the following financial results summary:

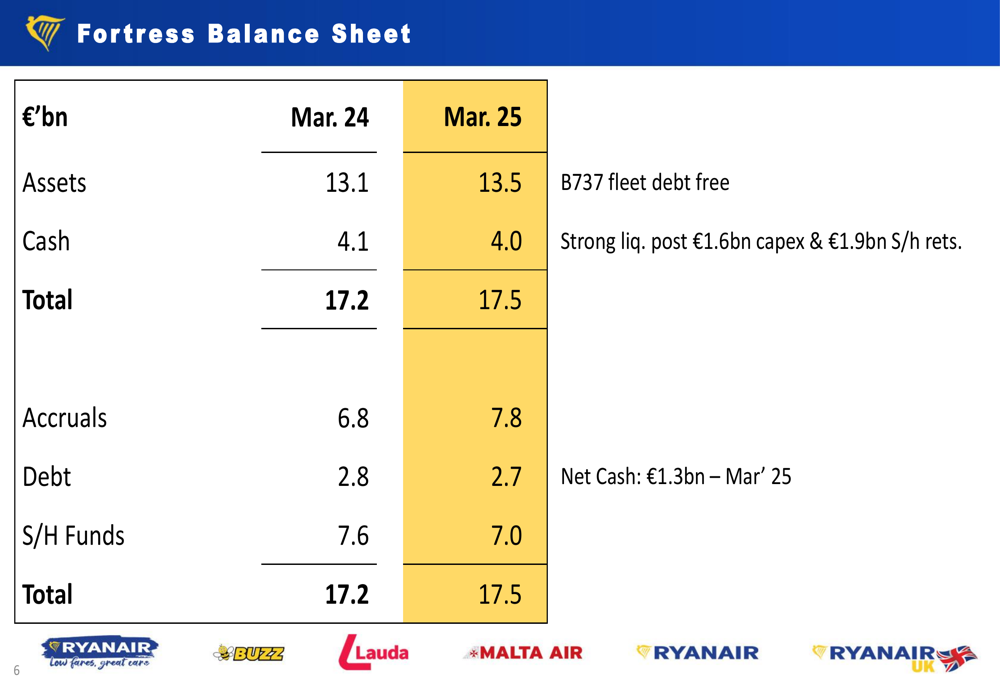

Fortress Balance Sheet

Despite the profit decline, Ryanair maintained a strong financial position with €4.0 billion in cash as of March 2025, only slightly down from €4.1 billion the previous year. The company’s total assets increased from €17.2 billion to €17.5 billion, while shareholder funds decreased from €7.6 billion to €7.0 billion, reflecting capital returns to shareholders.

The airline emphasized its debt-free Boeing (NYSE:BA) 737 fleet and reported a net cash position of €1.3 billion as of March 2025, positioning it well to navigate potential market uncertainties.

The company’s balance sheet strength is illustrated in this financial summary:

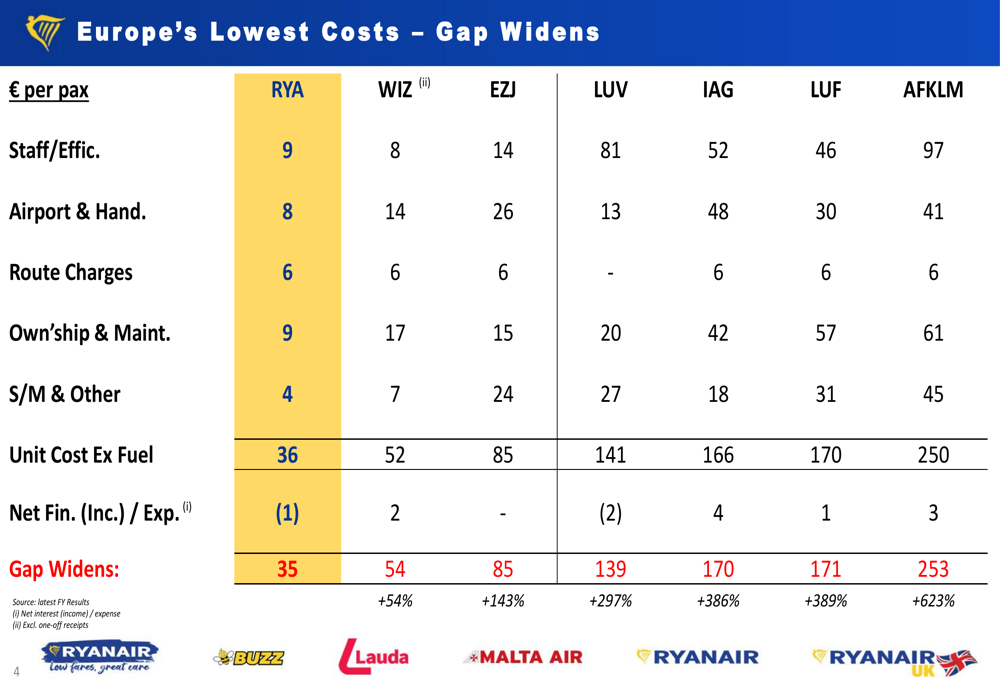

Competitive Industry Position

Ryanair continues to emphasize its position as Europe’s lowest-cost airline, with a widening cost gap compared to competitors. According to the presentation, Ryanair’s unit cost excluding fuel stands at €36 per passenger, significantly lower than Wizz Air (€52), easyJet (LON:EZJ) (€85), and legacy carriers like IAG (€166) and Air France-KLM (€250).

This cost advantage is visualized in the following comparative analysis:

The airline maintains Europe’s most extensive low-cost network with 93 bases across 233 airports in 37 countries. Its summer 2025 fleet consists of 618 aircraft, including 181 fuel-efficient "Gamechanger" Boeing 737s.

Strategic Initiatives

Boeing Delays and Fleet Expansion

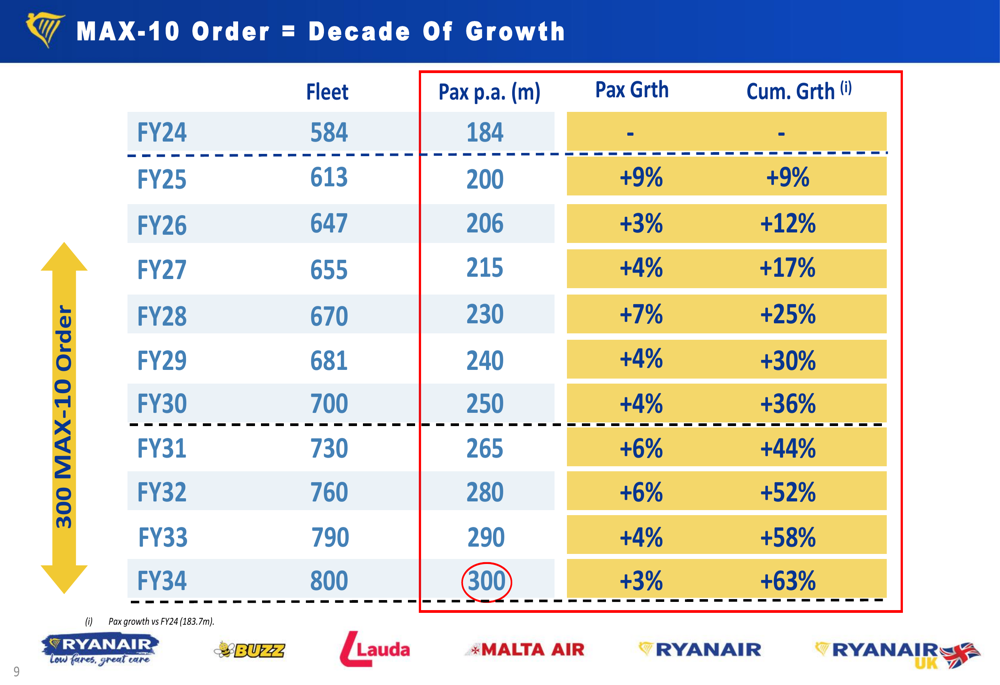

Ryanair addressed ongoing Boeing delivery delays, noting they are "getting better" but still impacting growth plans. The airline expects slower passenger growth of just 3% in FY26 (to 206 million) due to these delays. However, management reported that Boeing’s quality and delivery performance is improving, with efforts underway to accelerate the delivery of 29 "Gamechanger" aircraft for summer 2026.

The company’s long-term fleet plan remains ambitious, with an order for 300 Boeing MAX-10 aircraft that will support growth to 300 million passengers annually by FY34. Boeing expects MAX-10 certification in late 2025, with Ryanair’s first 15 MAX-10s scheduled for delivery in spring 2027.

The following chart illustrates Ryanair’s projected fleet and passenger growth through FY34:

Fuel Hedging Strategy

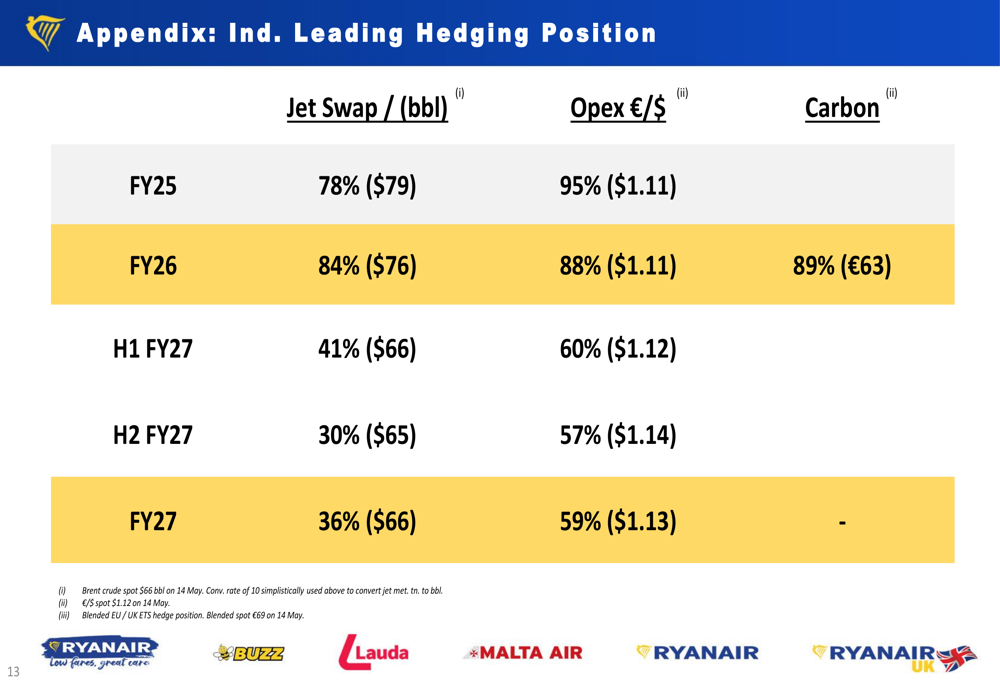

Ryanair highlighted its industry-leading hedging position, which provides significant protection against fuel price volatility. For FY25, the airline has hedged 78% of its jet fuel requirements at $79 per barrel, while FY26 is 84% hedged at $76 per barrel. The company has also begun hedging FY27, with 36% coverage at an advantageous $66 per barrel.

This comprehensive hedging strategy is detailed in the following table:

Shareholder Returns

Despite the profit decline, Ryanair continues to return capital to shareholders. The company bought back and canceled 77 million shares in FY25 at an average price of €19.10, representing 36% of issued share capital bought back since 2008. A new €750 million share buyback program is set to begin in May 2025.

Additionally, Ryanair paid a €400 million dividend in 2024 and plans to pay €480 million in 2025, subject to AGM approval. Management noted that Boeing delivery delays are actually boosting shareholder returns in the near term as capital expenditure is reduced.

Environmental Sustainability

Ryanair emphasized its environmental credentials, highlighting its position as the #1 large-cap airline for ESG according to Sustainalytics. The company also received an A rating from MSCI and A- from CDP.

The airline has committed to reducing CO2 emissions to approximately 50g per passenger/kilometer by 2031, a 27% reduction that has been validated by the Science Based Targets initiative (SBTi). This will be achieved through investments in fuel-efficient aircraft, including the "Gamechanger" and MAX-10 models, as well as new winglets that reduce fuel consumption by 1.5% and noise by 6%.

The company’s ESG credentials are summarized in this slide:

Forward-Looking Statements

For FY26, Ryanair expects traffic growth to slow to 3% (206 million passengers) due to Boeing delivery delays. Management reported strong summer 2025 demand across its network, with a particularly strong Q1 expected due to Easter timing and weak prior-year comparisons.

The airline cautiously expects to recover most, but not all, of the 7% fare decline experienced in FY25. However, management warned that an economic downturn due to tariffs could impact demand and fares. The company anticipates modest unit cost inflation from higher air traffic control and environmental costs, partially offset by lower fuel costs due to favorable hedging positions.

While Ryanair stated it was too early to provide meaningful profit guidance for FY26, it emphasized that its lowest-cost model, competitive fares, and strong balance sheet position it as a long-term winner by 2030.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.