Sana Biotechnology stock higher after Eric Jackson touts 100-bagger potential

Introduction & Market Context

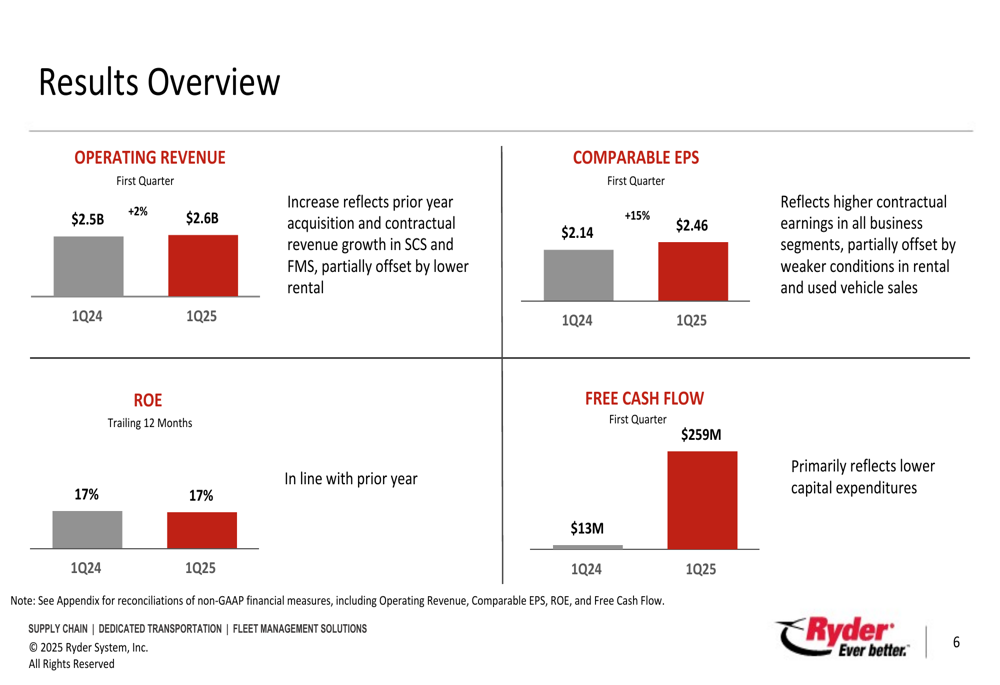

Ryder System Inc (NYSE:R) presented its first quarter 2025 earnings results on April 23, 2025, highlighting a 15% increase in comparable earnings per share despite ongoing challenges in the freight market. The logistics and transportation company reported operating revenue of $2.6 billion, up 2% from the prior year, while maintaining a return on equity of 17%.

The company’s stock has experienced volatility following the earnings release, with premarket trading showing a 2.16% decline after gaining 2.82% in the previous session. Ryder’s shares have traded between $116.58 and $171.78 over the past 52 weeks.

Quarterly Performance Highlights

Ryder’s comparable EPS reached $2.46 in Q1 2025, up from $2.14 in the same period last year, while free cash flow surged to $259 million compared to just $13 million in Q1 2024. This significant improvement in cash flow primarily resulted from reduced capital expenditures.

As shown in the following overview of Q1 results, the company maintained steady performance across key metrics despite market headwinds:

The company’s performance varied across its three business segments. Fleet Management Solutions (FMS) saw modest 1% growth in operating revenue to $1.3 billion, but earnings before tax declined 6% to $94 million. This decrease primarily reflected weaker rental demand and lower used vehicle sales gains, partially offset by improved ChoiceLease performance.

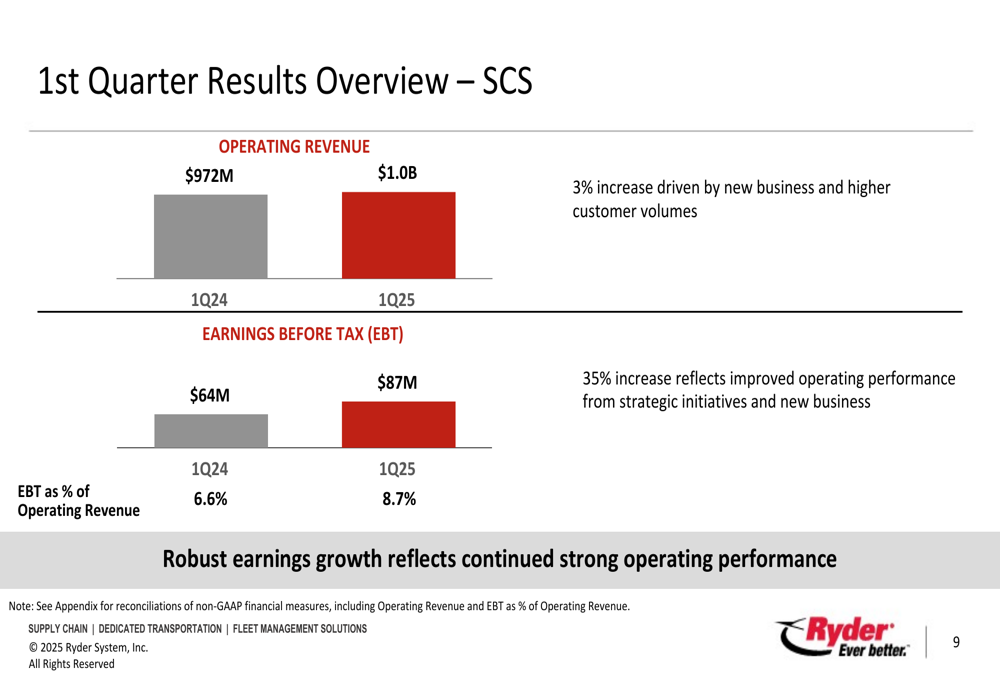

Supply Chain Solutions (SCS) delivered strong results with operating revenue increasing 3% to $1.0 billion and earnings before tax surging 35% to $87 million. The robust earnings growth demonstrates the strength of Ryder’s contractual business model in this segment:

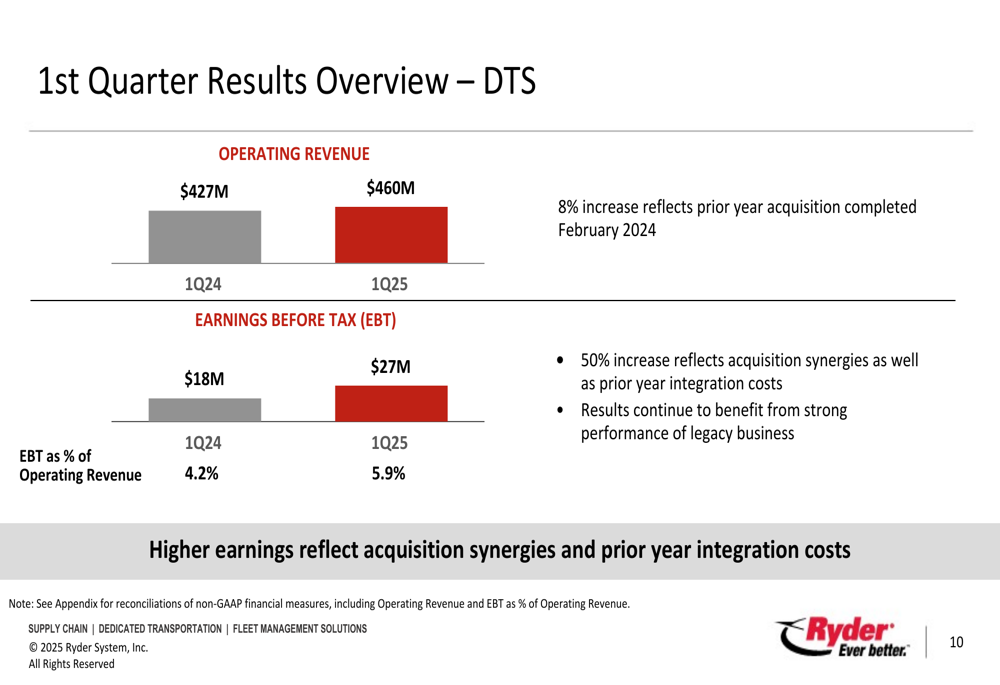

Dedicated Transportation Solutions (DTS) showed the strongest growth among all segments, with operating revenue up 8% to $460 million and earnings before tax increasing 50% to $27 million. This impressive performance was driven by acquisition synergies and strong performance in the legacy business:

Strategic Initiatives

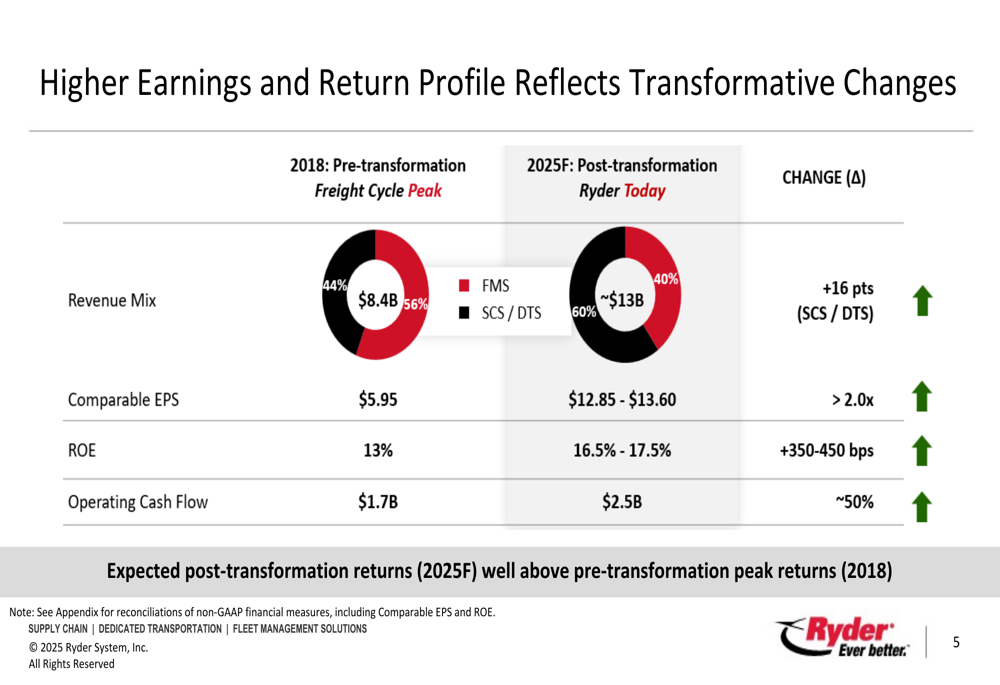

Ryder’s ongoing business transformation continues to yield benefits, with the company highlighting how its evolved business model has improved financial performance compared to previous cycles. The presentation emphasized that expected post-transformation returns in 2025 are significantly higher than pre-transformation peak returns in 2018:

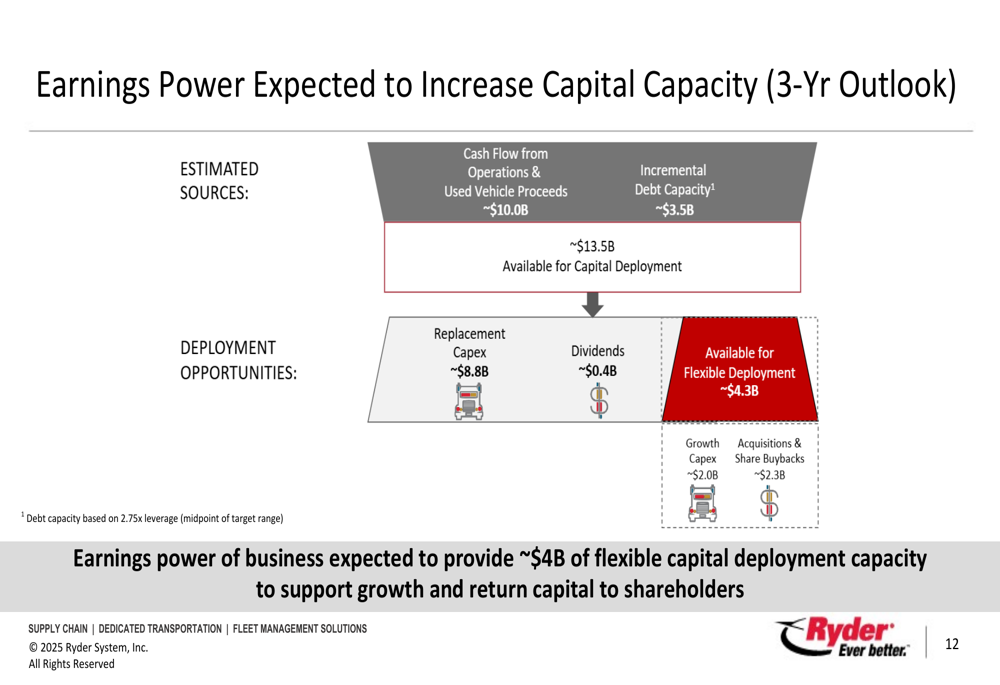

A key component of Ryder’s strategy involves optimizing capital allocation to support both growth initiatives and shareholder returns. The company projects approximately $13.5 billion in capital deployment capacity over a three-year period, with $4.3 billion available for flexible deployment:

In the first quarter, Ryder returned $202 million to shareholders through buybacks and dividends, demonstrating its commitment to shareholder value while maintaining investment in strategic growth areas.

Used Vehicle Sales Performance

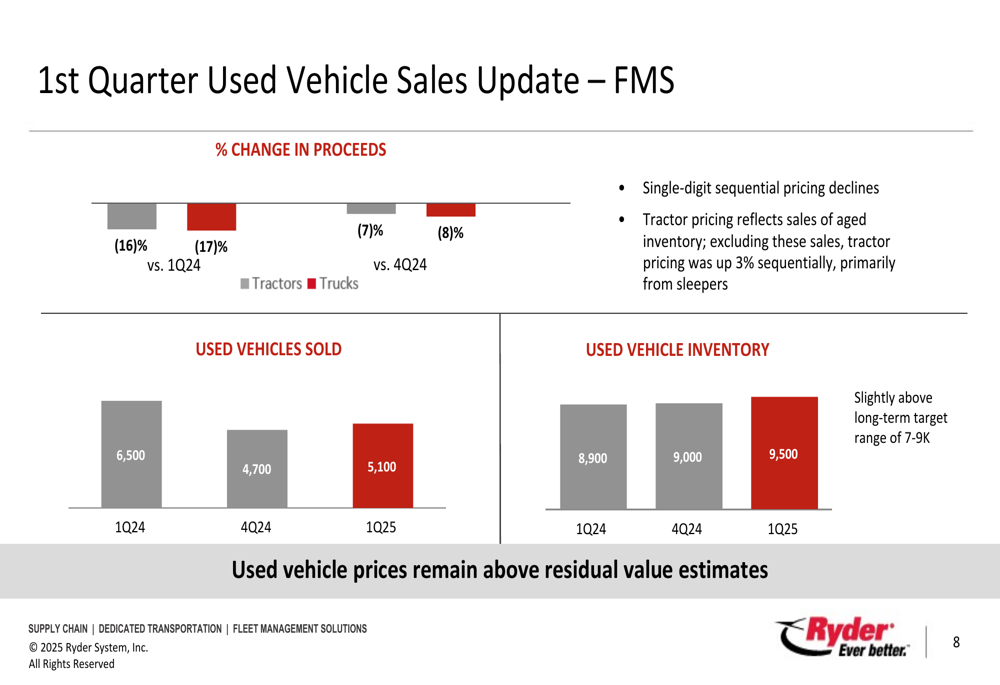

Used vehicle sales, an important component of Ryder’s FMS segment, showed weakness in the quarter with pricing down significantly year-over-year. Tractor proceeds decreased 16% compared to Q1 2024 and 7% sequentially, while truck proceeds fell 17% year-over-year and 8% sequentially:

The company noted that used vehicle inventory increased to 9,500 units, slightly above its long-term target range of 7,000-9,000 units. Despite the pricing pressure, Ryder emphasized that used vehicle prices remain above residual value estimates, providing a buffer against further deterioration.

Forward-Looking Statements

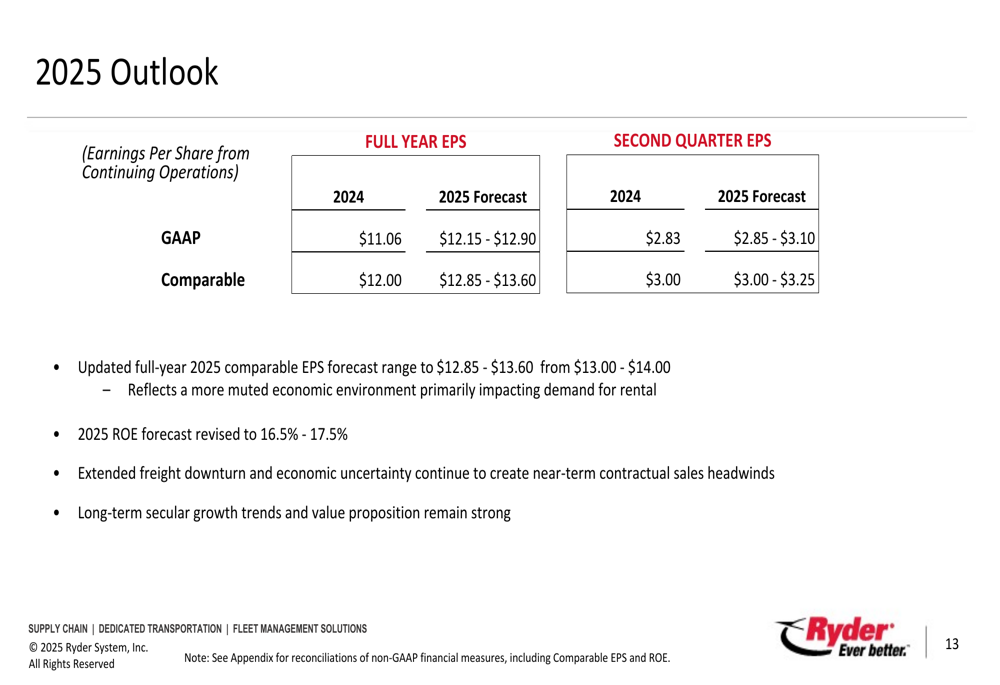

Ryder updated its full-year 2025 comparable EPS forecast range to $12.85-$13.60, down from the previous guidance of $13.00-$14.00, citing a more muted economic environment primarily impacting demand for rental services. The company also revised its 2025 ROE forecast to 16.5%-17.5%:

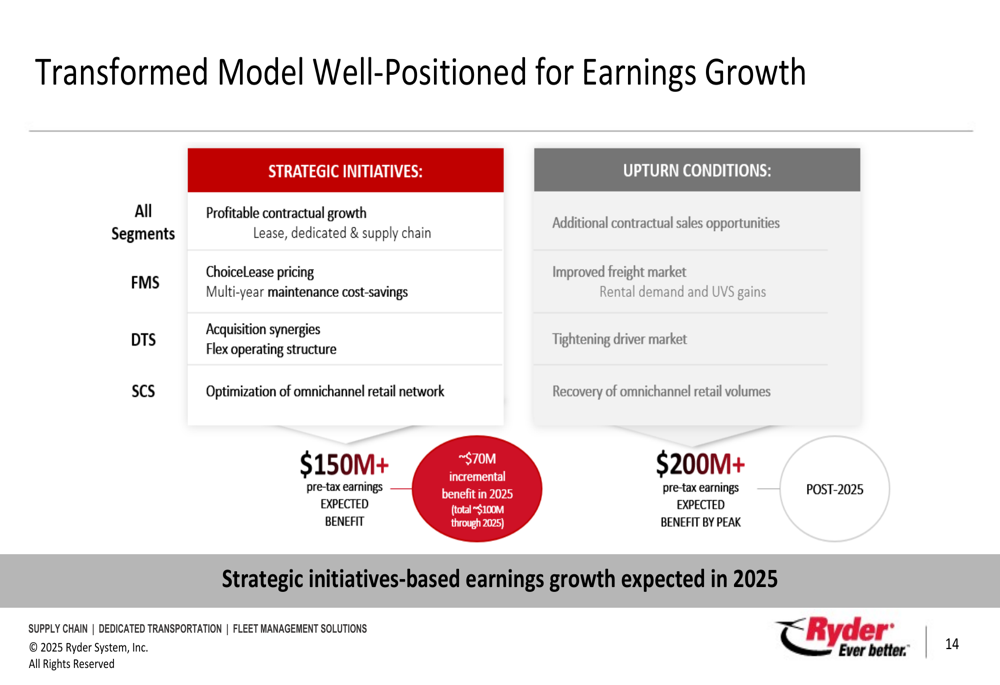

Despite near-term challenges, Ryder remains confident in its long-term growth prospects, highlighting several strategic initiatives expected to deliver over $150 million in pre-tax earnings benefits:

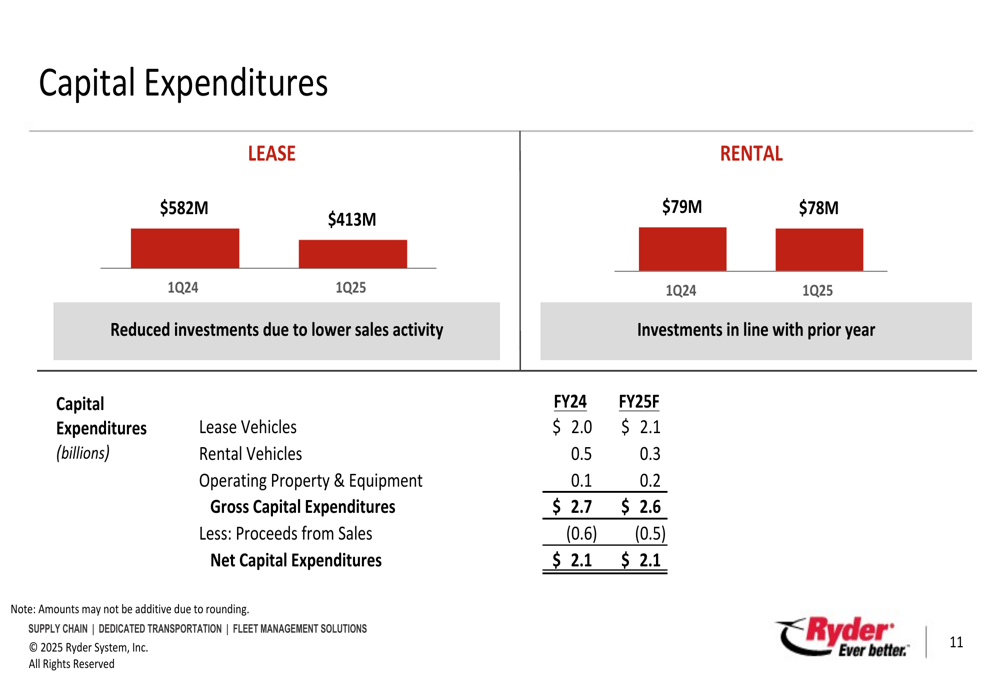

Capital Expenditure and Cash Flow

Ryder has adjusted its capital expenditure plans for 2025, with gross capital expenditures projected at $2.6 billion, down from $2.7 billion in 2024. The company increased its full-year 2025 free cash flow guidance to $375-$475 million, up from the previous range, primarily due to reduced capital spending:

This improved cash flow outlook provides Ryder with additional flexibility to pursue growth opportunities and return capital to shareholders through its established dividend and share repurchase programs.

Conclusion

Ryder’s Q1 2025 results demonstrate the resilience of its transformed business model, with strong performance in contractual segments offsetting weakness in more cyclical areas like rental and used vehicle sales. While the company has modestly reduced its full-year guidance due to economic uncertainties, its strategic initiatives and focus on high-margin contractual business continue to support solid financial performance.

The company’s ability to generate substantial free cash flow even during an extended freight downturn highlights the success of its business transformation efforts. As Ryder continues to execute its balanced growth strategy, it remains well-positioned to deliver long-term shareholder value despite near-term market challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.