Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

Sabra Health Care REIT (NYSE:WELL) Inc. (NASDAQ:SBRA) released its investor presentation on August 4, 2025, highlighting the company’s strategic positioning in healthcare real estate with a focus on skilled nursing facilities and senior housing. The presentation comes after Sabra reported solid Q1 2025 results, with EPS of $0.17 meeting analyst expectations and revenue of $183.54 million slightly exceeding forecasts.

The healthcare REIT, which closed at $18.29 on August 4 with a 0.77% gain, has positioned itself to capitalize on favorable demographic trends in the senior care market. With its stock trading between its 52-week range of $15.60 to $20.03, Sabra continues to execute its "Strategic, Disciplined, Opportunistic" approach to healthcare real estate investment.

Portfolio Strategy and Demographics

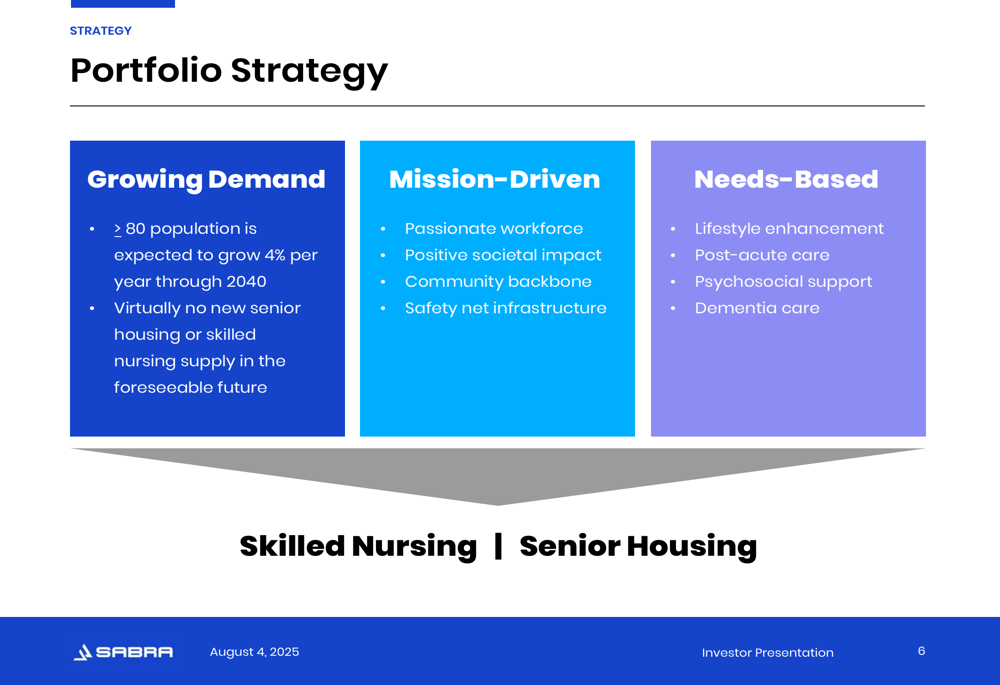

Sabra’s portfolio strategy centers on three key pillars: Growing Demand, Mission-Driven operations, and Needs-Based services. The company is strategically positioned to benefit from demographic tailwinds, with the 80+ population expected to grow by 4% annually through 2040.

As shown in the following portfolio strategy breakdown:

This demographic advantage is further reinforced by supply constraints in the skilled nursing sector. Since 2000, the 85+ population has grown by 60%, while skilled nursing beds have declined by 12%, creating a widening gap between supply and demand that supports Sabra’s investment thesis.

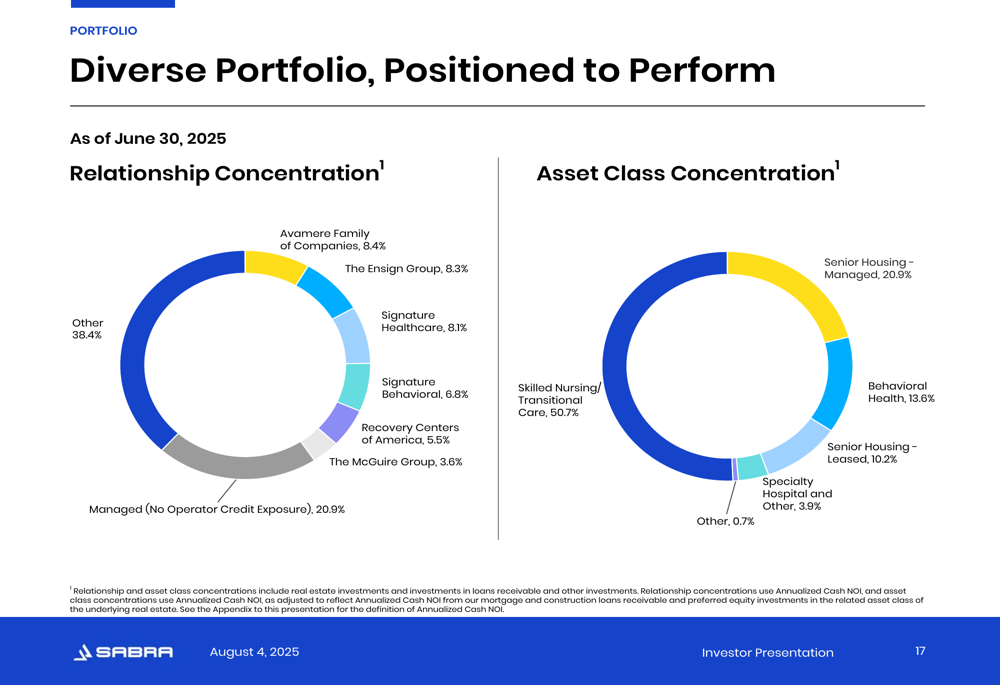

The company’s portfolio as of June 30, 2025, includes 392 investments across 58 relationships with a weighted average remaining lease term of 7 years. Occupancy rates remain strong at 83% for skilled nursing/transitional care, 90% for leased senior housing, and 78% for behavioral health/hospitals/other facilities.

The following chart illustrates Sabra’s diverse portfolio by relationship concentration and asset class:

2025 Financial Guidance and Performance

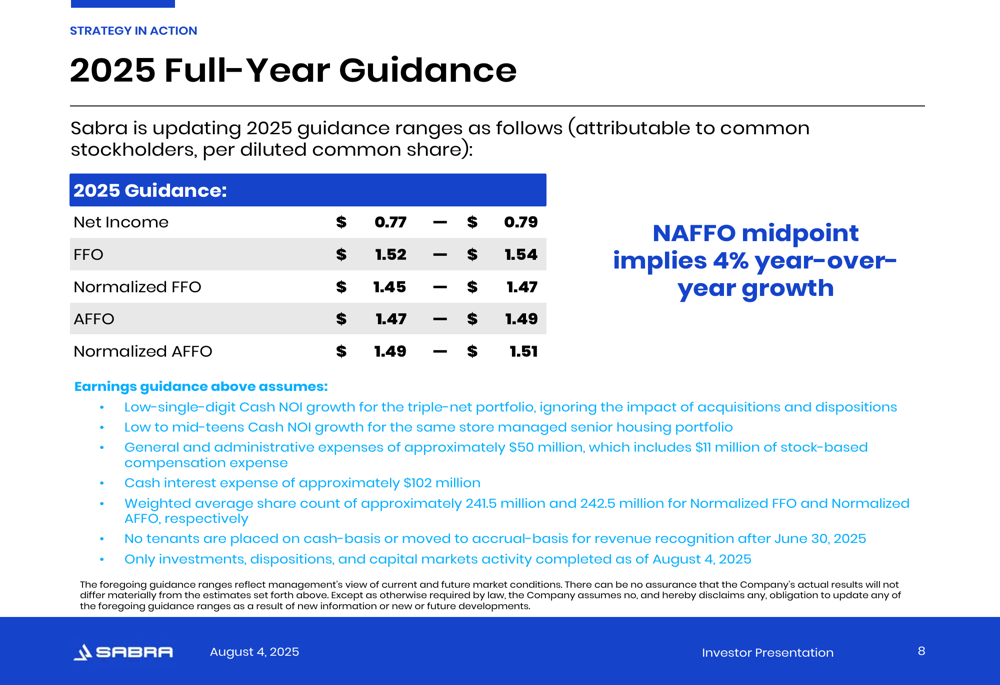

Sabra has provided full-year 2025 guidance that projects continued growth across key financial metrics. The company expects normalized AFFO per diluted common share of $1.49-$1.51, representing a 4% year-over-year growth at the midpoint.

The detailed financial guidance is presented in the following table:

This guidance aligns with the company’s Q1 2025 performance, where normalized FFO per share increased to $0.35 from $0.34 in Q1 2024, and normalized AFFO per share rose to $0.37 from $0.35 in the same period last year.

The company’s assumptions include low-single-digit Cash NOI growth for triple-net properties and low to mid-teens Cash NOI growth for senior housing, consistent with statements made during their Q1 earnings call where management highlighted "strong performance in its senior housing and skilled nursing segments."

Balance Sheet and Credit Metrics

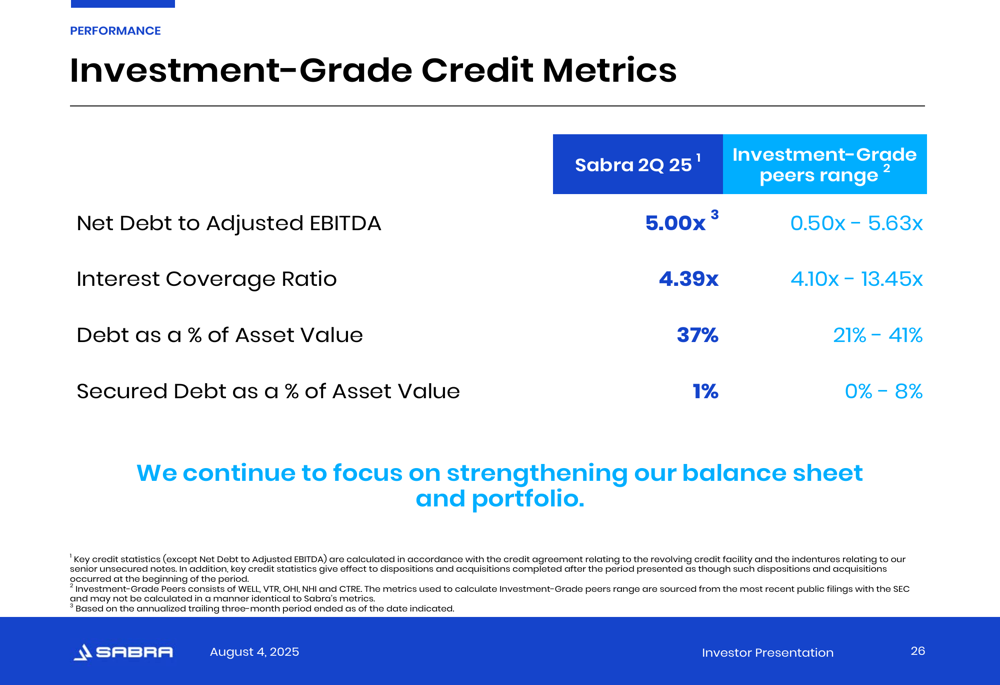

Sabra maintains a strong balance sheet with investment-grade credit metrics. As of June 30, 2025, the company reported a weighted average debt maturity of nearly 5 years with no material debt maturities until 2028. The weighted average effective interest rate stands at 4.04%, with ample liquidity of approximately $1.2 billion.

The company’s key credit metrics compared to investment-grade peers are illustrated in the following chart:

Sabra’s consolidated enterprise value of $6.7 billion consists of 64% common equity value, 18% fixed rate bonds, 15% hedged term loans, 2% line of credit, and 1% secured debt. This capital structure supports the company’s strategy of maintaining balance sheet flexibility while pursuing strategic growth opportunities.

CFO Michael Costa emphasized this approach, stating: "Our strong balance sheet and ready access to capital allows us to thoughtfully finance investment opportunities and drive value for our shareholders."

Competitive Positioning and Valuation

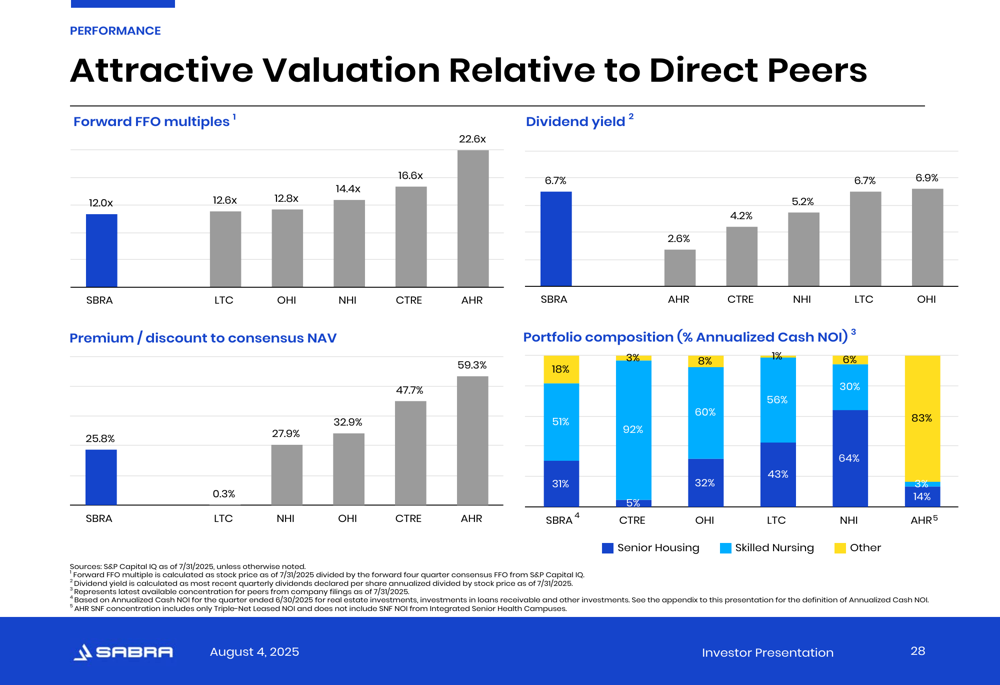

Sabra presents an attractive valuation relative to its direct peers in the healthcare REIT sector. The company trades at a forward FFO multiple of 12.0x and offers a dividend yield of 6.7%, both lower than its peer group average.

The comparative valuation metrics are illustrated in the following chart:

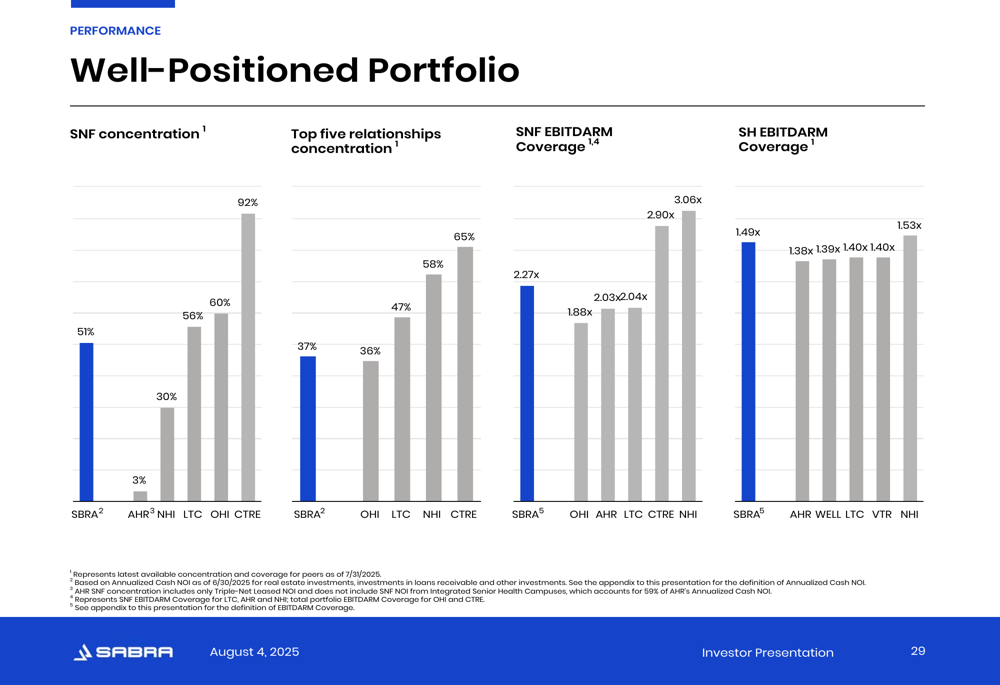

While Sabra has a higher concentration in skilled nursing facilities (51% of portfolio) compared to peers, it maintains competitive EBITDARM coverage ratios. The company’s skilled nursing EBITDARM coverage of 2.27x is lower than some peers, but its senior housing EBITDARM coverage of 1.49x exceeds the peer group average.

The following chart shows Sabra’s portfolio positioning relative to peers:

Forward-Looking Statements

Sabra’s management remains optimistic about future growth opportunities driven by favorable reimbursement trends and demographic tailwinds. Medicare rates have grown from $544 in January 2012 to $720 in January 2025 (2.1% CAGR), while Medicaid rates have increased from $179 to $312 over the same period (4.2% CAGR).

The Centers for Medicare & Medicaid Services recently finalized a 3.2% Medicare increase, and Medicaid rates are expected to see a 5% average increase in the top five states where Sabra operates. These reimbursement trends, combined with the company’s strategic focus on quality operators, position Sabra for continued growth.

CEO Rick Matros emphasized the importance of operational excellence, stating: "We know what happens inside our buildings matters most." This focus on quality care aligns with the company’s investment strategy of partnering with operators who provide skillful and compassionate care.

During the Q1 earnings call, management noted a "very robust pipeline of deals," while maintaining a cautious approach to growth. The presentation reinforces this disciplined strategy, focusing on unique, accretive investments that leverage Sabra’s operational and asset management expertise.

With its strategic portfolio positioning, strong balance sheet, and favorable demographic trends, Sabra Healthcare REIT appears well-positioned to deliver on its 2025 financial guidance and create long-term value for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.