Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Salesforce Inc (NYSE:CRM) presented its second quarter fiscal year 2026 earnings results on September 3, 2025, reporting 10% year-over-year revenue growth and raising its full-year operating margin and cash flow guidance. The company’s shares rose 1.36% to $256.30 in after-hours trading following the announcement.

Quarterly Performance Highlights

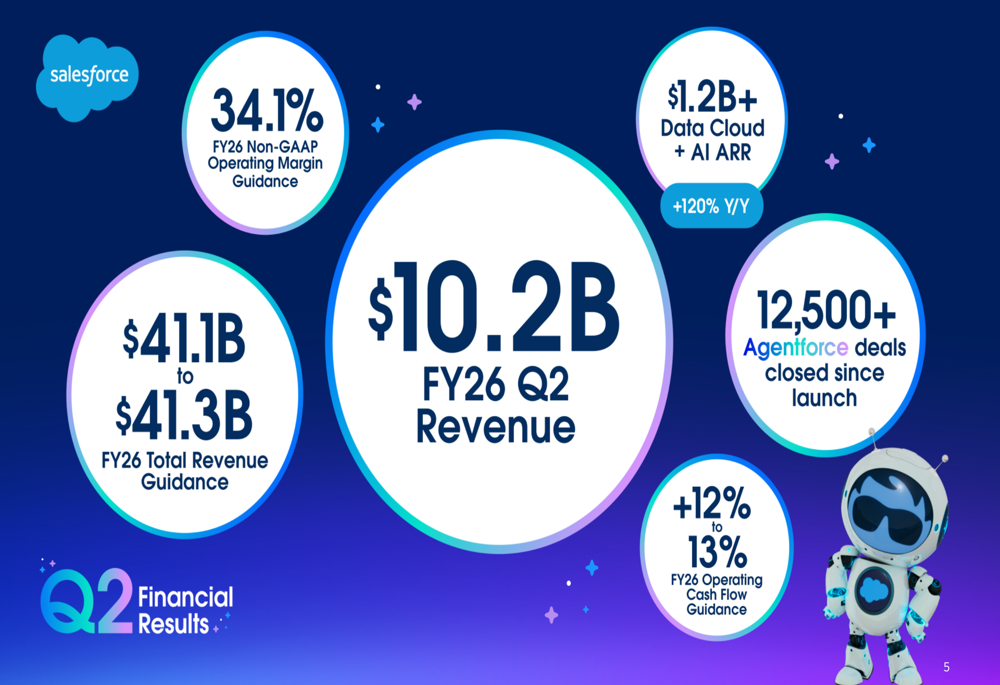

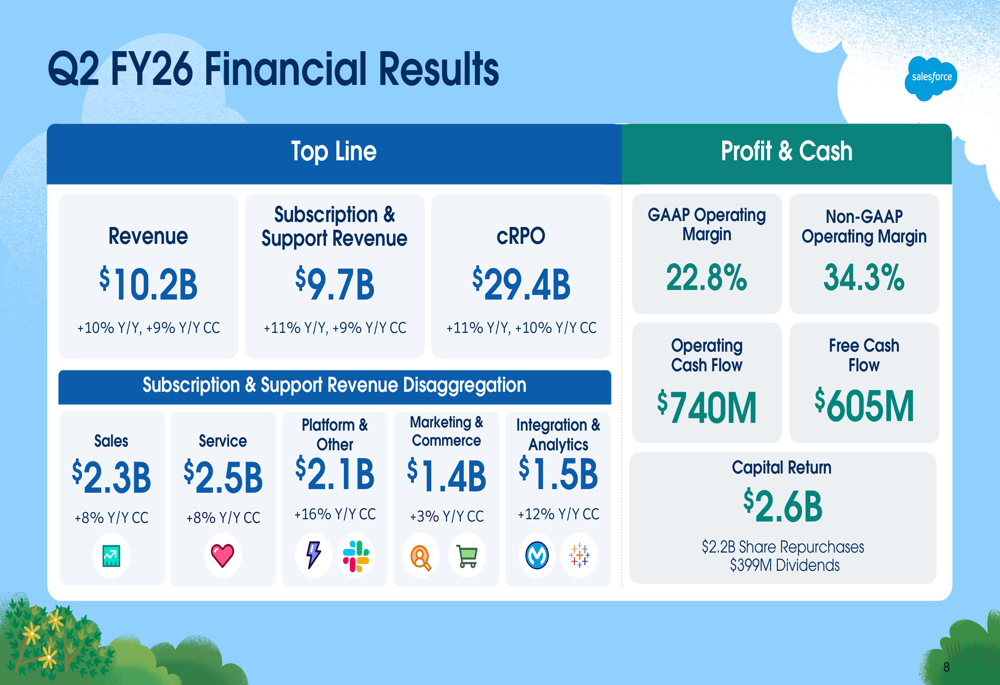

Salesforce reported Q2 FY26 revenue of $10.2 billion, representing a 10% increase year-over-year, or 9% in constant currency. The company’s subscription and support revenue, which accounts for the bulk of its business, grew to $9.7 billion, up 11% year-over-year or 9% in constant currency.

"We delivered strong Q2 results while continuing to invest in our AI and data capabilities," said Marc Benioff, Chair and CEO of Salesforce, according to the presentation materials.

The standout performer in Salesforce’s portfolio was its Data Cloud and AI offerings, which reached an Annual Recurring Revenue (ARR) of over $1.2 billion, growing an impressive 120% year-over-year. The company also highlighted the success of its Agentforce product, closing more than 12,500 deals since its launch.

As shown in the following key financial results:

Detailed Financial Analysis

Breaking down the subscription and support revenue by cloud offering, Platform & Other showed the strongest growth at 16% year-over-year in constant currency, reaching $2.1 billion. Integration & Analytics grew 12% to $1.5 billion, while Sales and Service each grew 8% to $2.3 billion and $2.5 billion respectively. Marketing & Commerce showed the slowest growth at 3%, generating $1.4 billion in revenue.

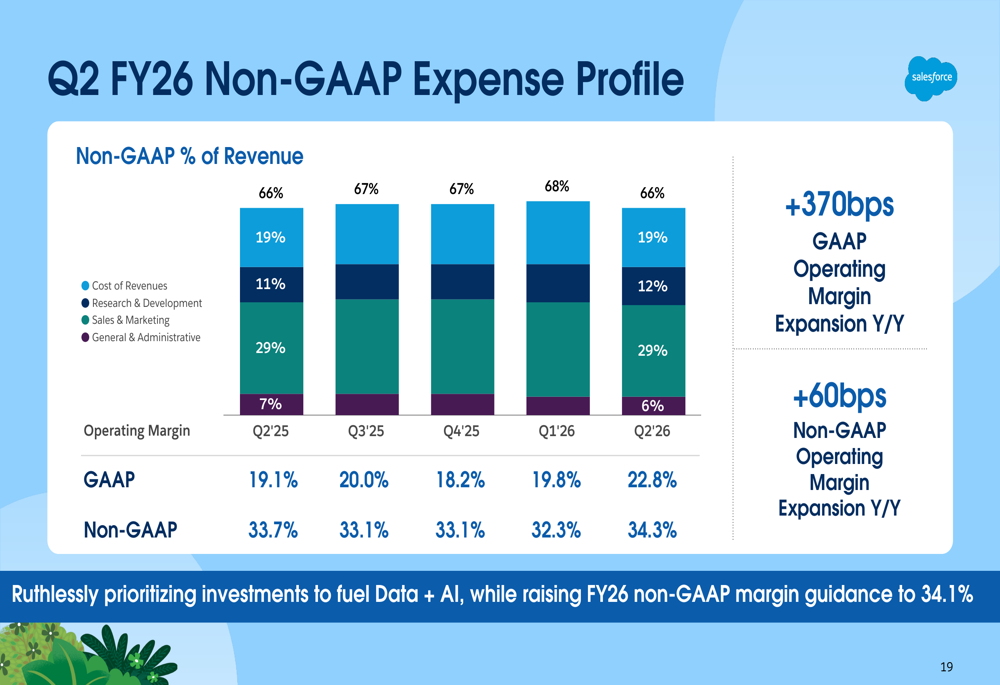

From a profitability standpoint, Salesforce achieved a non-GAAP operating margin of 34.3% in Q2, while GAAP operating margin stood at 22.8%. The company generated $740 million in operating cash flow and $605 million in free cash flow during the quarter.

The detailed breakdown of financial results shows Salesforce’s performance across all segments:

Geographically, the Americas region contributed $6.7 billion in revenue (9% growth in constant currency), while EMEA (Europe, Middle East, and Africa) added $2.4 billion (7% growth) and APAC (Asia-Pacific) delivered $1.1 billion (11% growth), making it the fastest-growing region.

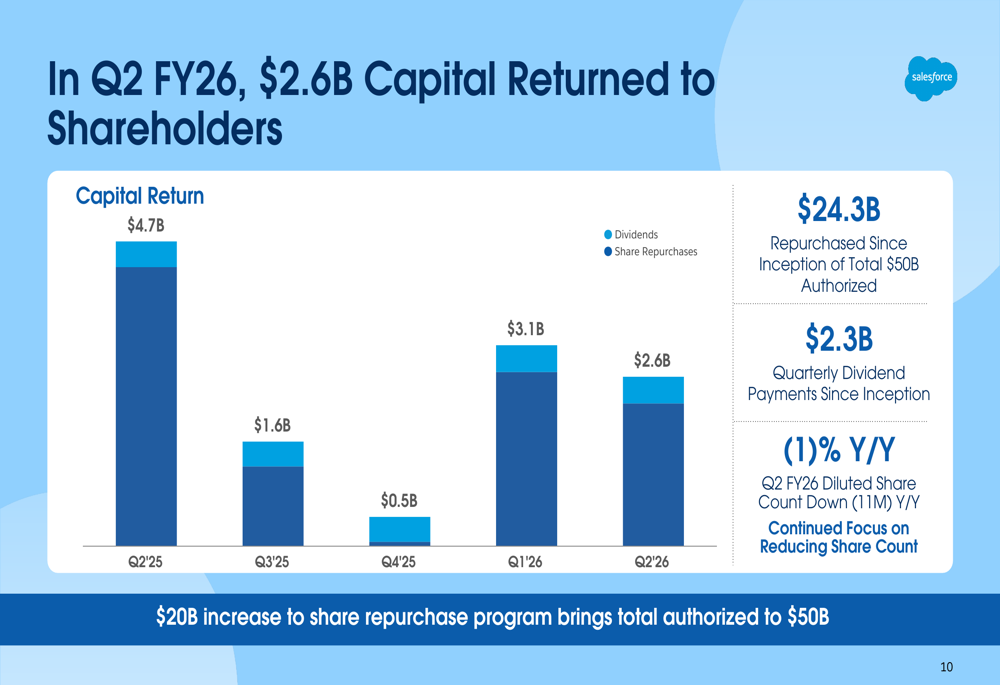

Salesforce continued its robust capital return program, returning $2.6 billion to shareholders in Q2, comprising $2.2 billion in share repurchases and $399 million in dividends. The company has now repurchased $24.3 billion of shares since the inception of its $50 billion authorization program.

The following chart illustrates Salesforce’s consistent capital return to shareholders:

Strategic Initiatives

Salesforce emphasized its position as "Customer Zero" for the Agentic Enterprise, showcasing how it deploys its own AI and automation technologies internally before offering them to customers. The company highlighted that its help.salesforce.com platform now handles 1.4 million conversations and supports seven languages, demonstrating the scalability of its AI solutions.

The presentation featured logos of prominent customers adopting Salesforce’s agentic enterprise solutions, including Dell Technologies, FedEx, Marriott Bonvoy, Anthropic, Reddit, and Under Armour, underscoring the company’s broad market penetration across industries.

Robin Washington, President and Chief Operating and Financial Officer, noted that the company is "ruthlessly prioritizing investments to fuel Data + AI," while simultaneously improving margins. This strategic balance between growth investments and profitability appears to be resonating with investors, as reflected in the after-hours stock movement.

Forward-Looking Statements

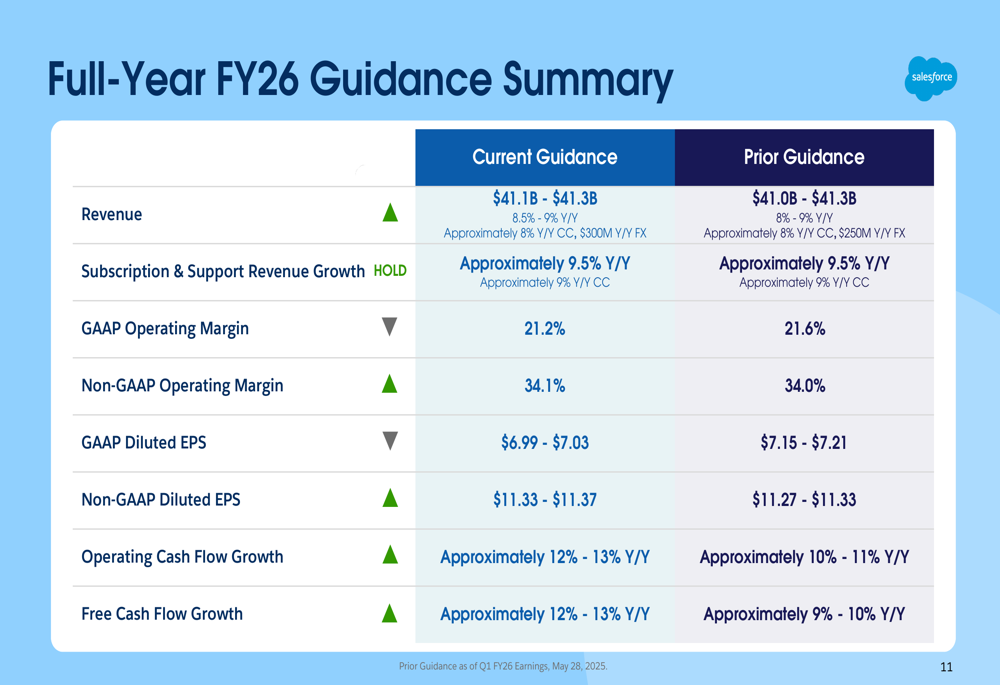

Salesforce updated its full-year FY26 guidance, slightly narrowing its revenue projection to $41.1-$41.3 billion (8.5%-9% year-over-year growth) from the previous $41.0-$41.3 billion. The company raised its non-GAAP operating margin guidance to 34.1% from 34.0%, and significantly increased its operating cash flow growth guidance to approximately 12%-13% year-over-year from the previous 10%-11%.

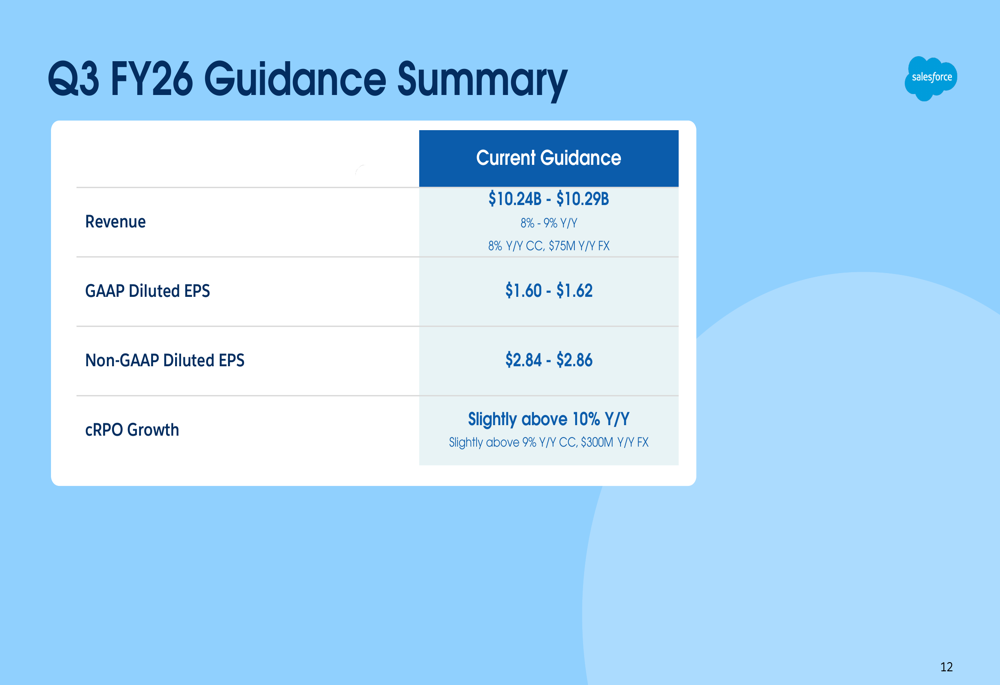

For Q3 FY26, Salesforce expects revenue between $10.24-$10.29 billion (8%-9% year-over-year growth), GAAP diluted EPS of $1.60-$1.62, and non-GAAP diluted EPS of $2.84-$2.86. The company also projects Current Remaining Performance Obligation (CRPO) growth to be slightly above 10% year-over-year.

The full-year guidance summary shows Salesforce’s updated projections across key metrics:

For the upcoming quarter, Salesforce provided the following guidance:

The company’s non-GAAP expense profile reveals its disciplined approach to cost management while investing in growth areas:

Salesforce’s Q2 FY26 results demonstrate the company’s continued momentum in cloud services, particularly in AI and data solutions. With strong revenue growth, margin expansion, and increased guidance for operating cash flow, Salesforce appears well-positioned to capitalize on enterprise digital transformation trends while delivering value to shareholders through its capital return program.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.