Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Salmon Evolution Holding AS (SALME) presented its Q1 2025 results on May 13, highlighting record biomass growth as the land-based salmon producer continues its strategic expansion. The Norwegian company, which utilizes hybrid flow-through technology for sustainable salmon farming, is currently in a transitional phase as it scales operations while constructing its Phase 2 facility.

The company’s stock closed at 6.23 NOK on May 12, 2025, up 0.32% for the day, and has traded between 5.50 NOK and 8.25 NOK over the past 52 weeks.

Quarterly Performance Highlights

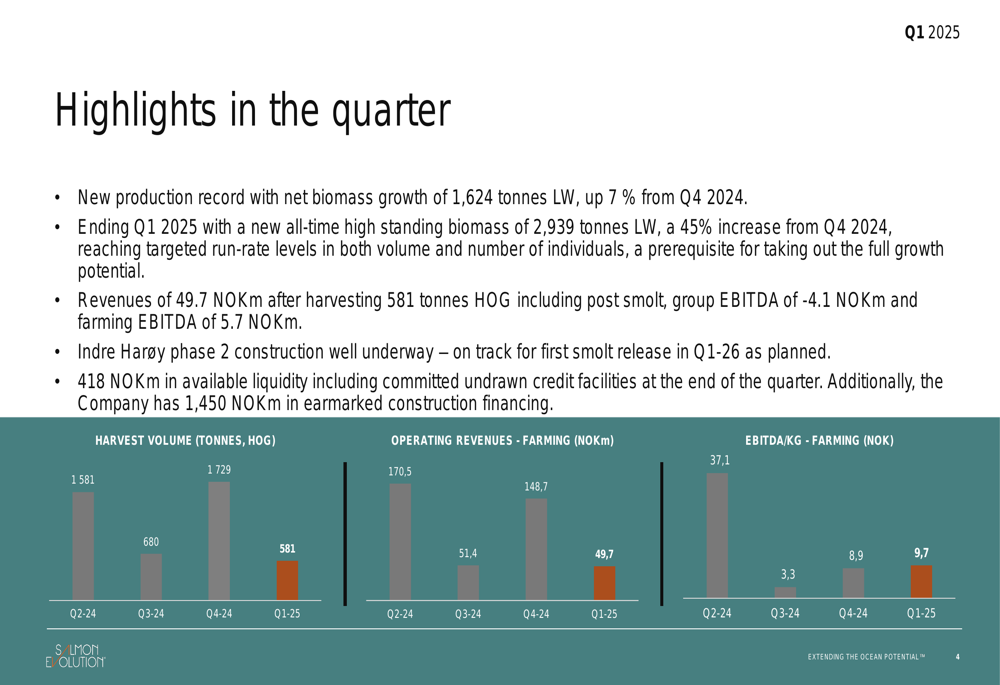

Salmon Evolution reported a new production record in Q1 2025, with net biomass growth reaching 1,624 tonnes (live weight), representing a 7% increase from Q4 2024. The company achieved an all-time high standing biomass of 2,939 tonnes, a substantial 45% increase from the previous quarter.

As shown in the following chart of key performance metrics:

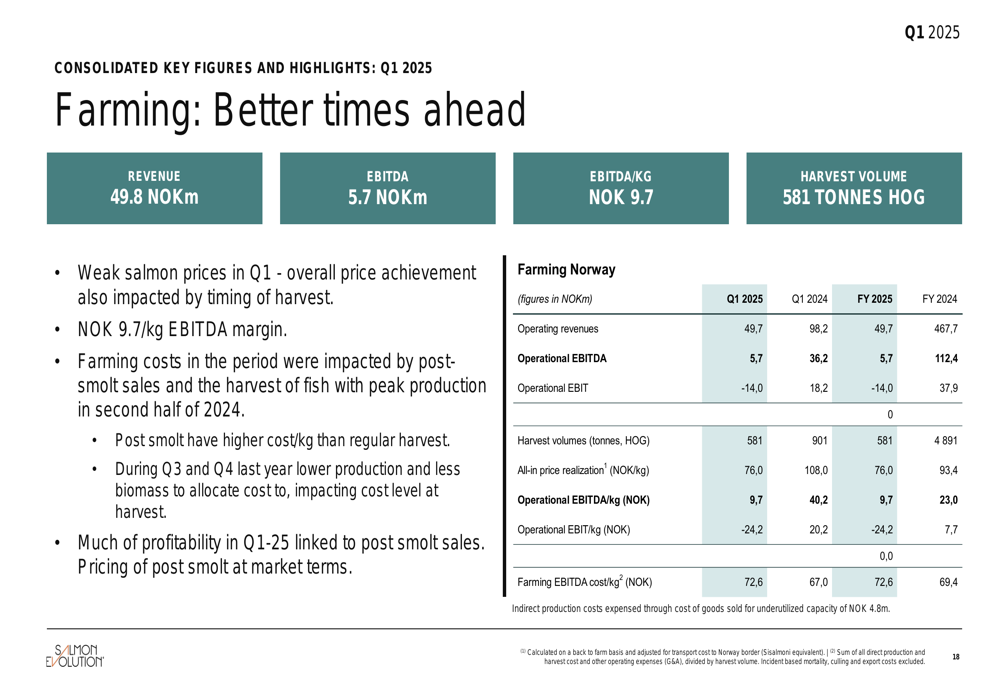

Despite these production achievements, revenue was limited to 49.7 million NOK after harvesting only 581 tonnes (head-on gutted), as the company prioritized biomass growth over harvest volumes. This strategic decision resulted in a positive Farming EBITDA of 5.7 million NOK but a Group EBITDA of -4.1 million NOK.

CEO Trond Håkon Schaug-Pettersen emphasized that the company has fully demonstrated its proof of concept after more than three years of industrial-scale operations, with continuous improvement in biological performance.

Operational Progress

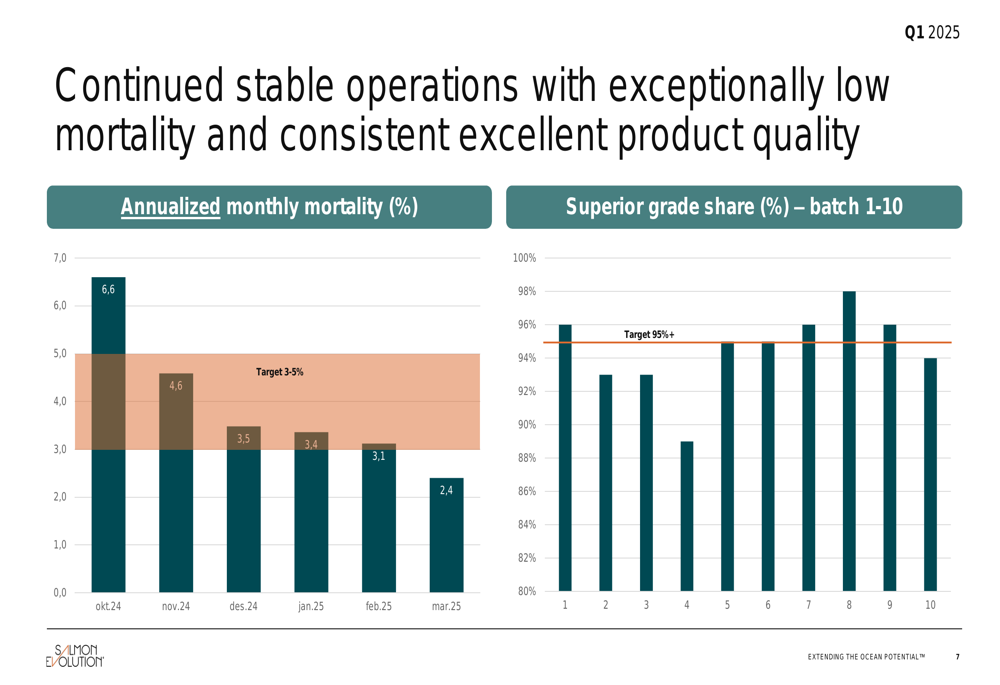

The presentation highlighted exceptionally strong biological performance, with mortality rates consistently declining to reach 2.4% in March 2025, well below the company’s target range of 3-5%. Product quality remains excellent, with superior grade share consistently meeting or exceeding the 95% target across harvested batches.

The following chart illustrates the company’s improving mortality rates and consistent product quality:

Management explained that the deliberate focus on biomass growth and optimizing biomass composition resulted in temporarily reduced harvest volumes. The company has updated its 2025 harvest guidance to 5,800-6,200 tonnes HOG, including post-smolt.

"We’re entering the second quarter with significantly better biomass composition, and we expect harvest weights to improve from Q2 onward," noted CFO Trond Vadset Veibust during the presentation.

Strategic Expansion

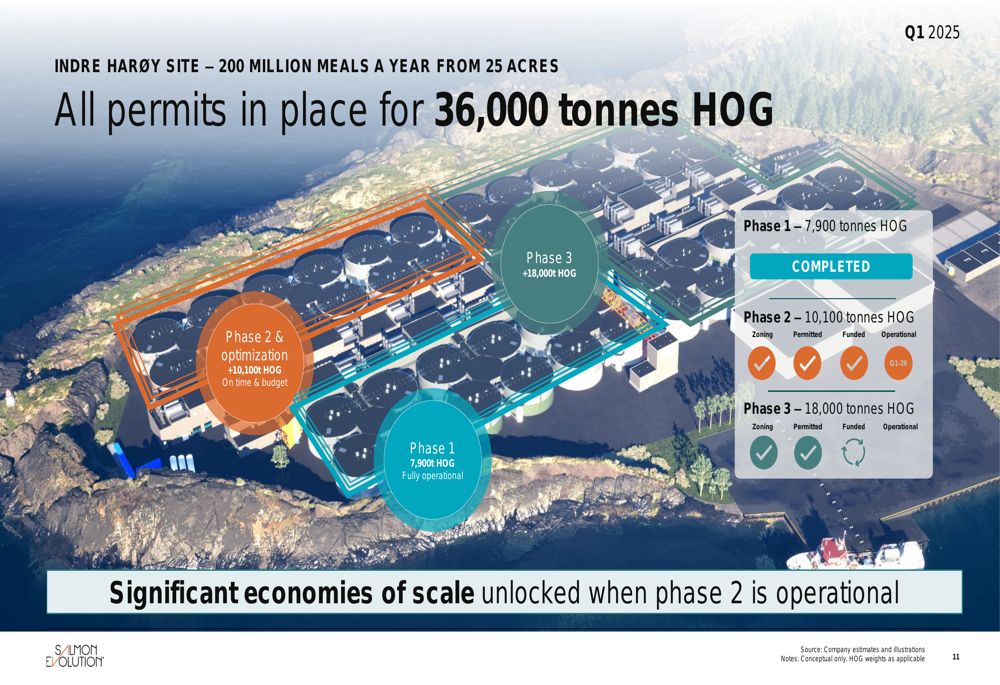

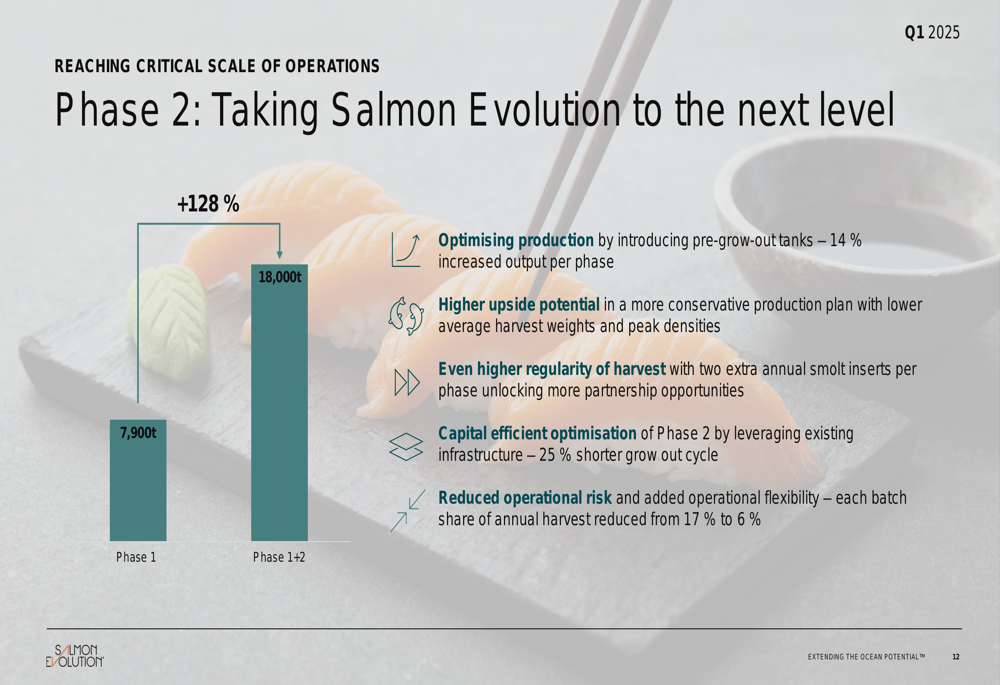

A central focus of the presentation was Salmon Evolution’s Phase 2 expansion at the Indre Harøy site, which is progressing on schedule and within budget. The expansion will increase production capacity by 128%, from the current 7,900 tonnes to 18,000 tonnes HOG upon completion.

The company’s phased development approach is illustrated in this expansion plan:

Phase 2 construction is well underway with approximately 130-140 workers on-site. Concrete works for the first four tanks were completed in Q1, with process installations set to begin soon. The company remains on track for first smolt release in Q1 2026 and first harvest in Q4 2026.

The Phase 2 expansion offers several strategic benefits, as illustrated below:

Beyond Phase 2, Salmon Evolution holds permits for up to 36,000 tonnes HOG at the Indre Harøy site, providing significant long-term growth potential. The company is also exploring opportunities in North America and continuing its project in South Korea, though with a measured approach.

Financial Analysis

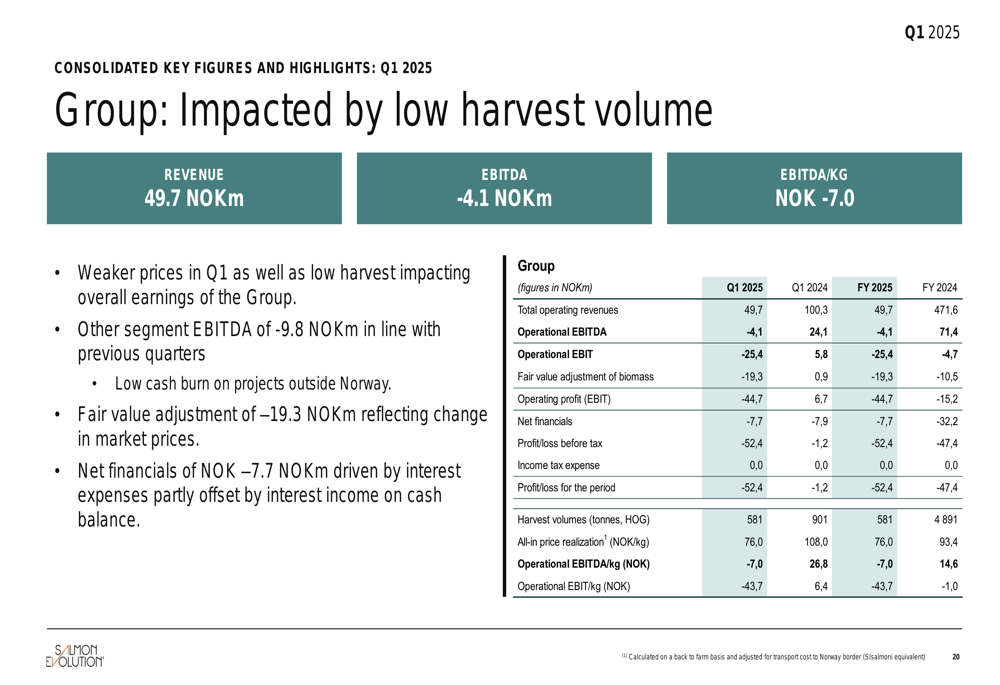

The financial results for Q1 2025 reflect the company’s current focus on growth over immediate profitability. While farming operations generated positive EBITDA of 5.7 million NOK (9.7 NOK/kg), the group’s overall EBITDA was negative at -4.1 million NOK.

The following slide details the farming segment’s performance:

Management noted that weak salmon prices in Q1 and the timing of harvest impacted overall price achievement. Farming costs in the period were also affected by post-smolt sales and the harvest of fish with peak production in the second half of 2024.

The group’s consolidated financial performance, shown below, reflects the impact of low harvest volumes:

Cash flow from operations was -6.6 million NOK, primarily due to the 45% increase in standing biomass during the quarter. The company reported 418 million NOK in available liquidity, including committed undrawn credit facilities, plus an additional 1,450 million NOK in earmarked construction financing for Phase 2.

Forward-Looking Statements

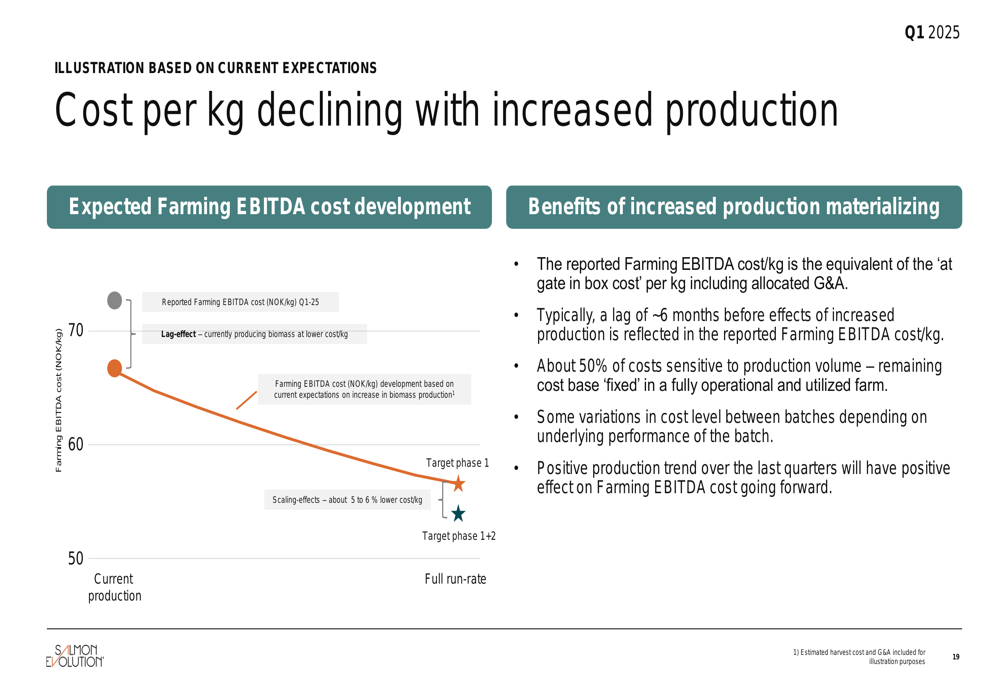

Salmon Evolution emphasized its cost leadership strategy, projecting declining costs per kg as production scales. The company expects Farming EBITDA cost/kg to decrease from 56.0 NOK at Phase 1 (8,000 tonnes) to 50.0 NOK at full capacity (36,000 tonnes).

This cost reduction trajectory is illustrated in the following graph:

Management positioned the company as being in the "sweet spot" with four key elements: a proven platform with demonstrated biological and technical performance; completion of the heavy lifting to reach critical mass; transition from capital expenditure to cash flow generation; and significant growth potential with licenses for 36,000 tonnes HOG.

The strategic positioning is visualized in this conceptual diagram:

"We have fully demonstrated our proof of concept after more than three years of operations," said CEO Schaug-Pettersen. "With Phase 2 on track and our biomass at record levels, we’re well-positioned to deliver on our growth strategy and move toward significant cash flow generation."

Salmon Evolution will release its Q2 2025 results on August 19, with an operational update expected in early July.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.