Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Salmon Evolution Holding AS (OB:SALME) released its Q2 2025 operational update on July 8, 2025, revealing significant improvements in harvest volumes and continued growth in standing biomass. The company’s stock closed at NOK 6.25 on July 7, up 1.3% ahead of the presentation.

The land-based salmon producer continues to show progress in its operational metrics following its Q1 2025 results, which had shown promising biomass growth despite challenging market conditions. This operational update provides insight into the company’s production efficiency and scale as it moves toward its targeted annual harvest volume of 5,800 to 6,200 tonnes for 2025.

Quarterly Performance Highlights

Salmon Evolution reported a substantial increase in harvest volume for Q2 2025, reaching 1,232 tonnes HOG (head-on gutted), which represents a 112% increase from the 581 tonnes reported in Q1. The company maintained a high superior share of 95%, indicating consistent quality in its production.

The company’s biomass production showed stability with 1,604 tonnes LW (live weight) produced during Q2, representing a slight 1% decrease from Q1’s 1,624 tonnes. However, Salmon Evolution noted that underlying biomass production exceeded 1,700 tonnes LW during the quarter.

As shown in the following chart of biomass production and standing biomass:

Standing biomass reached 3,043 tonnes LW by the end of Q2, exceeding the company’s target range of 2,900-3,000 tonnes LW. This represents a continued improvement from the 2,939 tonnes reported at the end of Q1 2025 and positions the company well for increased harvest volumes in upcoming quarters.

The company highlighted stable operations throughout the quarter, with two smolt groups stocked and the farm now fully stocked. Production reached an all-time high toward the end of Q2, suggesting positive momentum heading into the second half of the year.

Detailed Financial Analysis

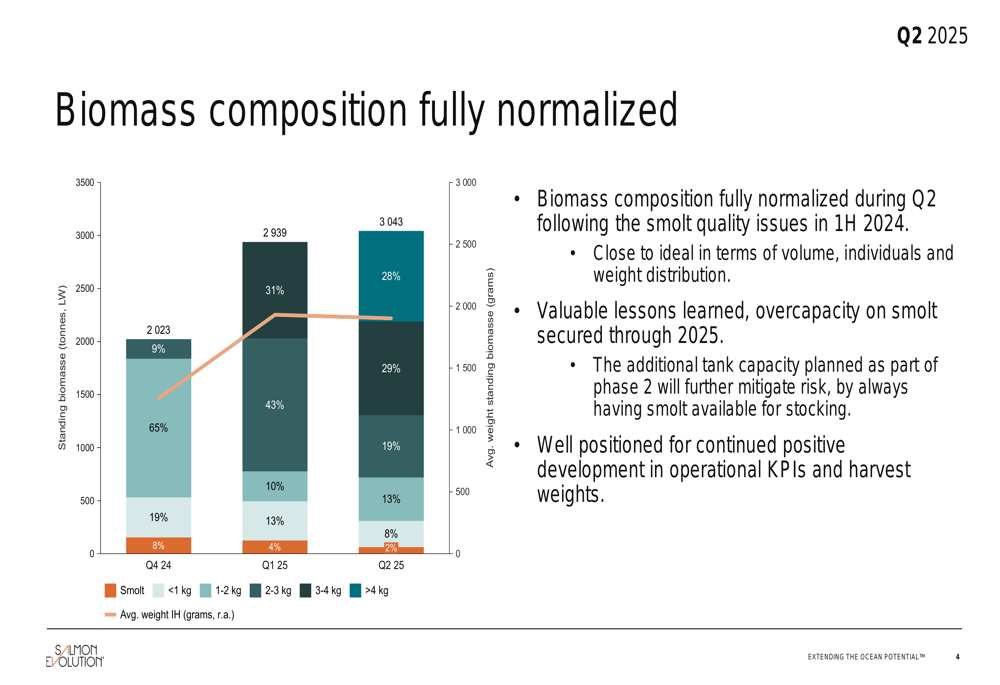

Salmon Evolution’s biomass composition has fully normalized during Q2, with a balanced distribution across different weight categories. This normalization is crucial for consistent production and harvest planning.

The following chart illustrates the biomass composition across different weight categories:

The normalized distribution shows 28% of biomass in the smolt category, 8% under 1 kg, 29% between 1-2 kg, 19% between 2-3 kg, 13% between 3-4 kg, and 2% above 4 kg. This balanced distribution represents a significant improvement from previous quarters and indicates operational maturity.

The company reported an all-in price realization of approximately NOK 72/kg on harvested fish during Q2. While this metric wasn’t directly comparable to figures in the Q1 earnings report, it provides insight into the company’s revenue potential from its current harvest.

The following chart details harvest volumes and weights across recent quarters:

The average harvest weight for Q2 2025 was 2.9 kg HOG, showing an improvement from the 2.3 kg reported in Q1 but still below the 3.8 kg achieved in Q4 2024. The company indicated that both harvest volumes and weights are set to increase from Q3 onward, suggesting further operational improvements.

Forward-Looking Statements

Salmon Evolution appears well-positioned for continued growth in the second half of 2025. The company noted that valuable lessons have been learned from its operations, and it has secured overcapacity on smolt, which should support future production targets.

The normalized biomass composition and increased standing biomass provide a solid foundation for the company to achieve its annual harvest target of 5,800-6,200 tonnes. The expected increase in harvest volumes and weights from Q3 onward aligns with statements made during the Q1 earnings call, where CEO Trun Hakons Geertpataschen expressed that the company was at an "inflection point" with Phase Two expansion nearing completion.

Salmon Evolution will present its complete Q2 2025 results on August 19, 2025, which will provide more detailed financial information and likely include updates on the company’s expansion plans, including the Phase Two construction and potential international growth opportunities in North America and Korea that were mentioned in previous communications.

The operational improvements demonstrated in this update support the company’s earlier assertions that cost improvements would materialize in the second half of 2025, potentially moving the company closer to consistent profitability after reporting an operational EBITDA loss of NOK 4.1 million in Q1.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.