Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Sampo Group (HEL:SAMPO) presented its Q2 2025 results on August 6, showcasing strong performance across its insurance operations. The Finnish insurance giant, currently trading near its 52-week high of €71.52, reported significant growth in both premiums and underwriting profit, building on the positive momentum seen in Q1 2025.

The company’s shares closed at €71.18 on August 5, 2025, with the stock having gained approximately 24.5% over the past year, outperforming many European insurance peers. This performance comes amid a relatively stable Nordic insurance market, where Sampo has maintained disciplined underwriting despite competitive pressures.

Quarterly Performance Highlights

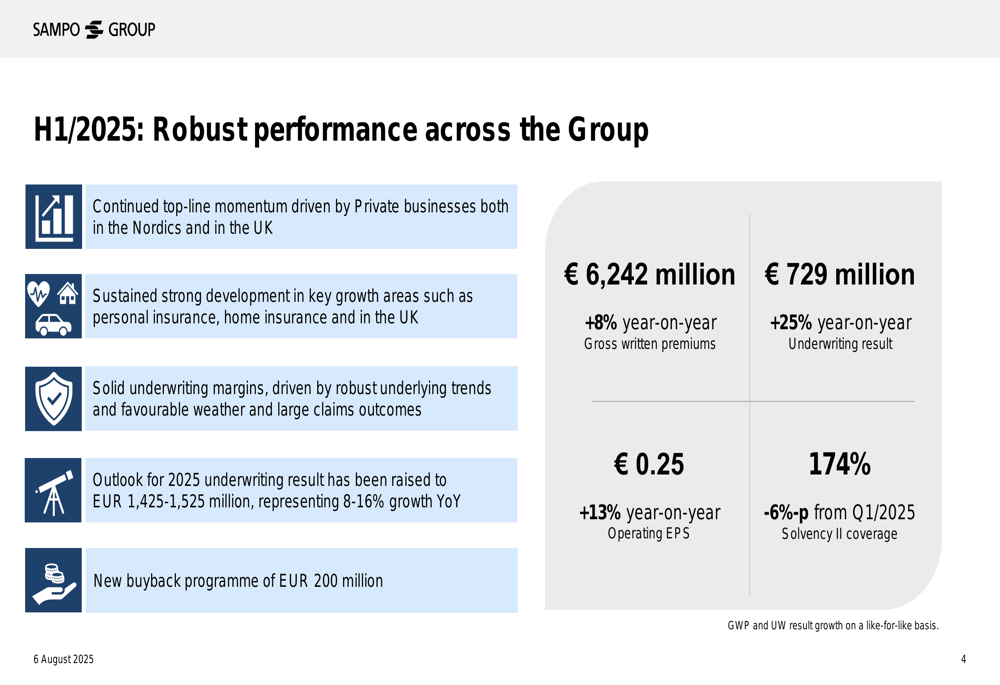

Sampo reported gross written premiums of €6,242 million for the first half of 2025, representing an 8% year-on-year increase. The company’s underwriting result showed even stronger growth, reaching €729 million, a 25% improvement compared to the same period last year.

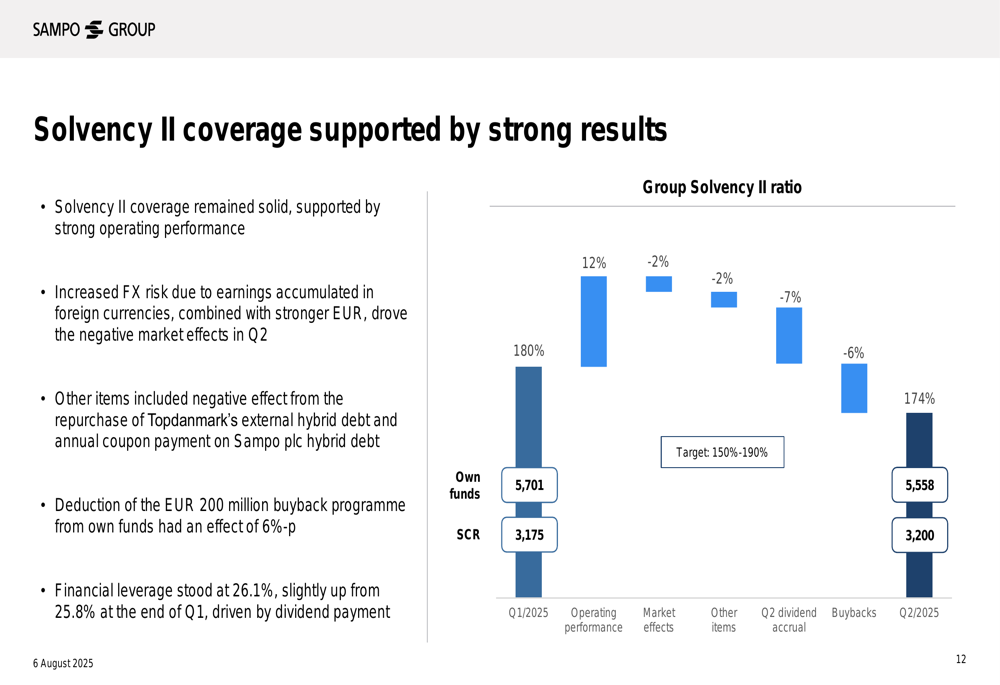

As shown in the following performance highlights chart, operating earnings per share increased by 13% year-on-year to €0.25, while the company maintained a solid Solvency II coverage ratio of 174%, though this represents a 6 percentage point decrease from Q1 2025:

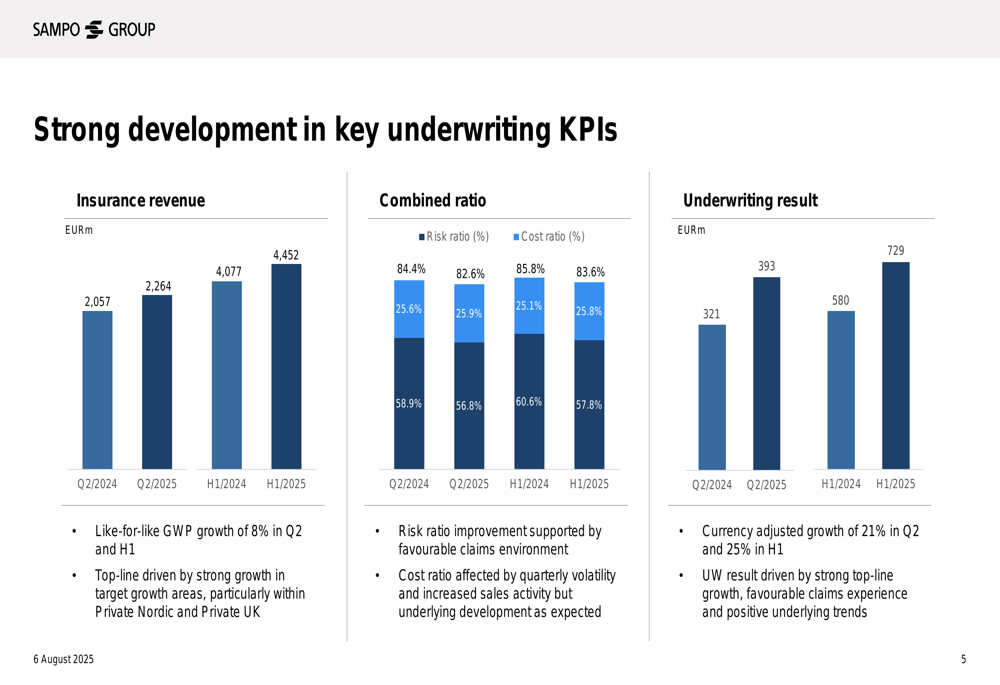

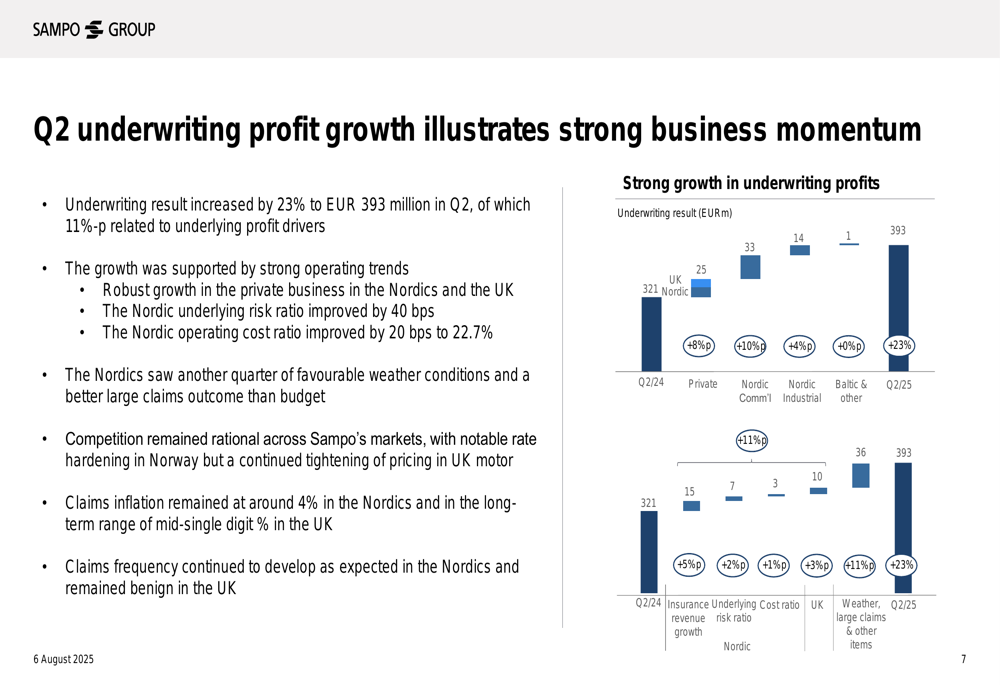

The company’s underwriting performance showed consistent improvement across key metrics. Insurance revenue grew to €2,264 million in Q2 2025, up from €2,057 million in Q2 2024, while the combined ratio improved with the risk ratio decreasing from 58.9% to 56.8% year-on-year in Q2:

Claims inflation has remained stable at around 4%, and the claims frequency developed as expected, contributing to the strong underwriting result. The company noted that the risk ratio improvement was supported by a favorable claims environment, while the cost ratio was affected by quarterly volatility and increased sales activity.

Segment Performance Analysis

All major business segments contributed to Sampo’s strong performance, with particularly robust results in the Private Nordic and Private UK divisions.

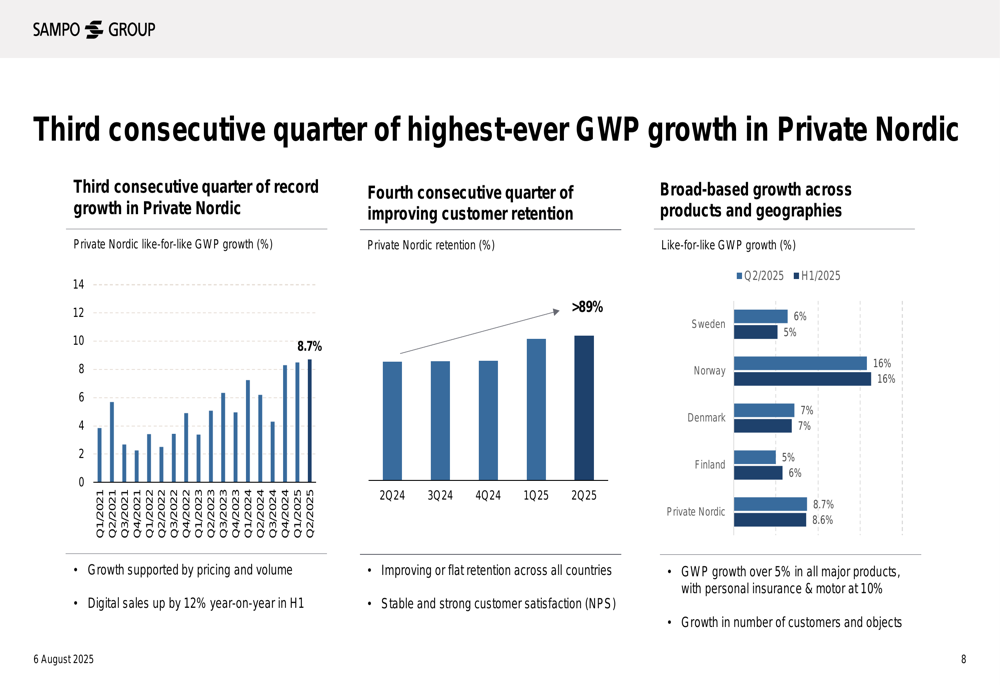

The Private Nordic segment reported an 8.6% increase in gross written premiums to €2,181 million, with the underwriting result growing by 24% to €337 million. The combined ratio improved from 85% to 82.7%. This segment benefited from the highest-ever GWP growth, supported by pricing and volume increases, with digital sales up 12% year-on-year in H1:

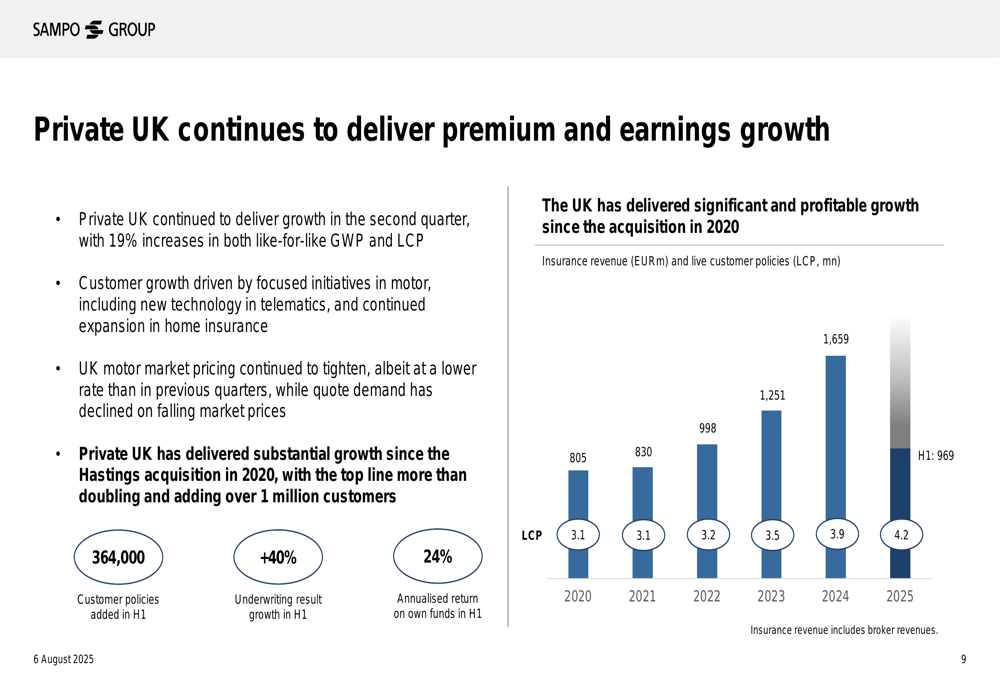

The Private UK segment showed even stronger growth, with gross written premiums increasing by 19% to €1,479 million and the underwriting result surging by 40% to €112 million. The combined ratio improved from 89.6% to 88.4%. This growth was driven by both policy count growth and increased average premiums, particularly in the motor and home insurance segments:

Nordic Commercial also performed well, with gross written premiums up 5.5% to €1,707 million and the underwriting result increasing by 15% to €185 million. The combined ratio improved from 84.7% to 83.0%. The growth was driven by successful renewals with rate increases, and the company reported that more SME customers were moved online, with SME GWP growth of 6%.

The following chart illustrates how these segments contributed to the overall 23% increase in underwriting profit in Q2 2025:

Strategic Initiatives and Outlook

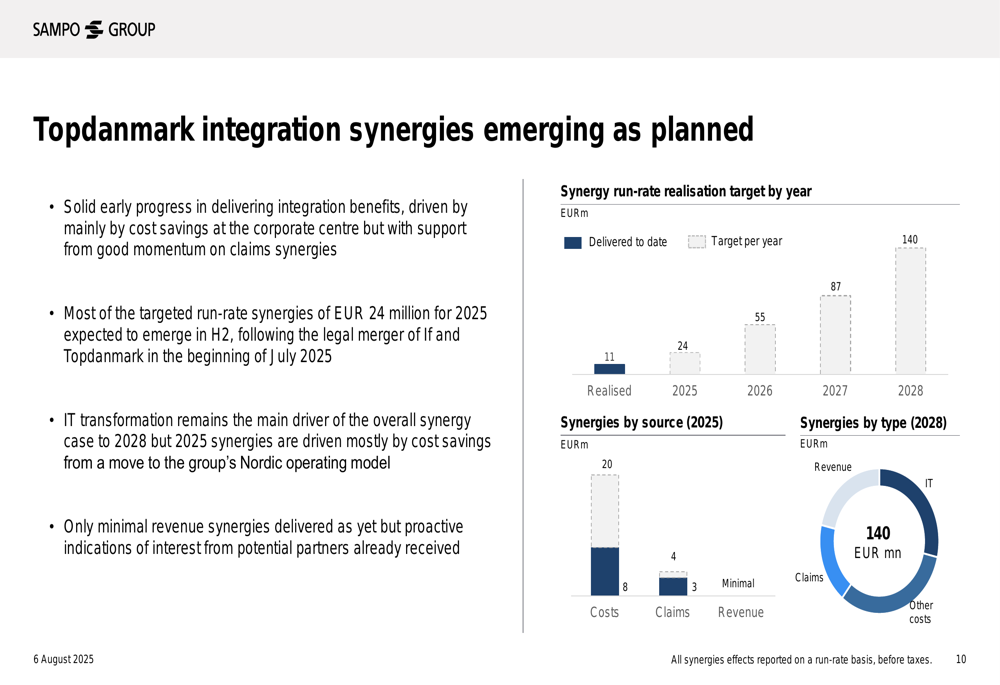

Sampo highlighted several strategic initiatives that are supporting its growth trajectory. The integration of Topdanmark is progressing as planned, with solid early progress in delivering integration benefits, primarily through cost savings at the corporate center:

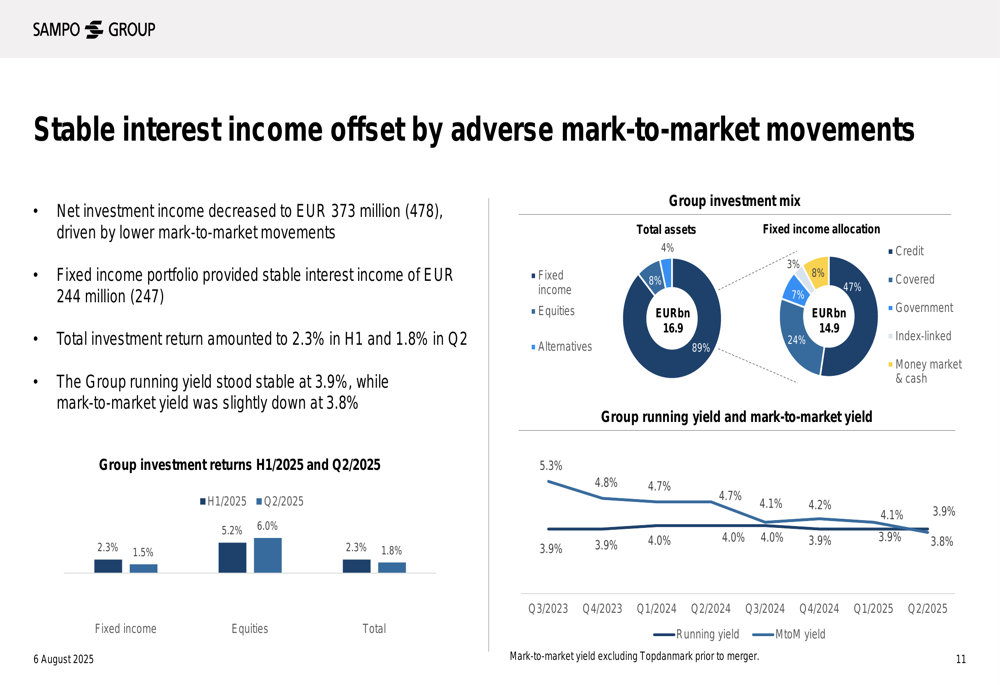

The company’s investment portfolio provided stable income despite adverse mark-to-market movements. Net investment income decreased to €373 million, while the fixed income portfolio provided stable interest income of €244 million. The total investment return amounted to 2.3% in H1 and 1.8% in Q2:

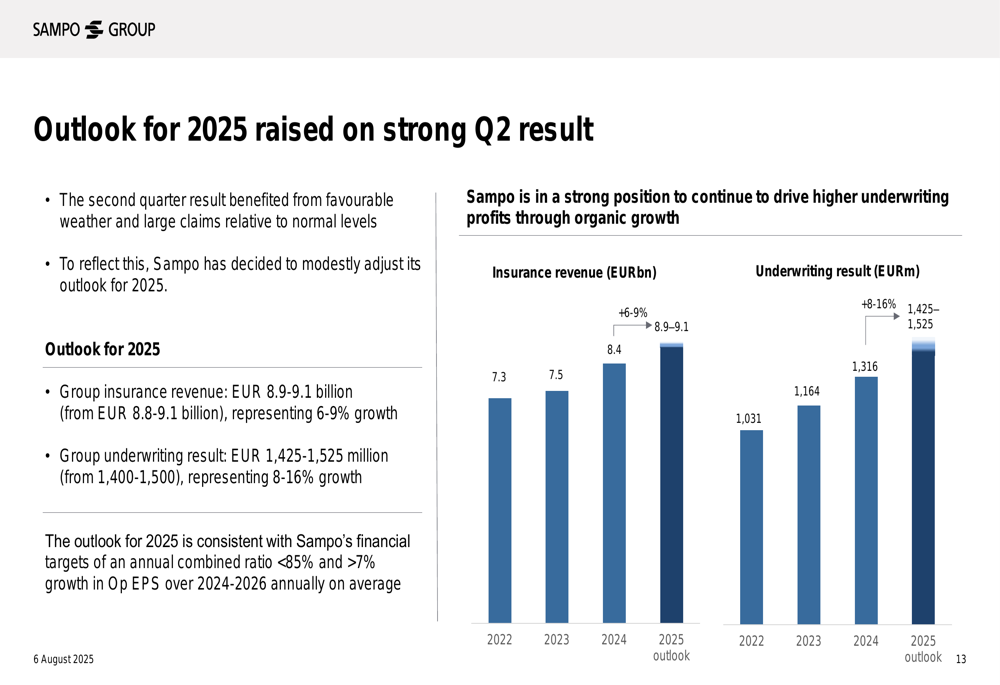

Based on the strong first-half performance, Sampo raised its outlook for 2025. The company now expects group insurance revenue of €8.9-9.1 billion and a group underwriting result of €1,425-1,525 million, representing 8-16% growth year-on-year:

This updated guidance is slightly higher than the €8.8-9.1 billion revenue outlook provided after Q1 2025, reflecting continued confidence in the company’s growth trajectory.

Capital Position and Shareholder Returns

Sampo maintained a solid capital position, with a Solvency II coverage ratio of 174% as of Q2 2025, down from 180% in Q1 2025 but still comfortably within the company’s target range of 150-190%:

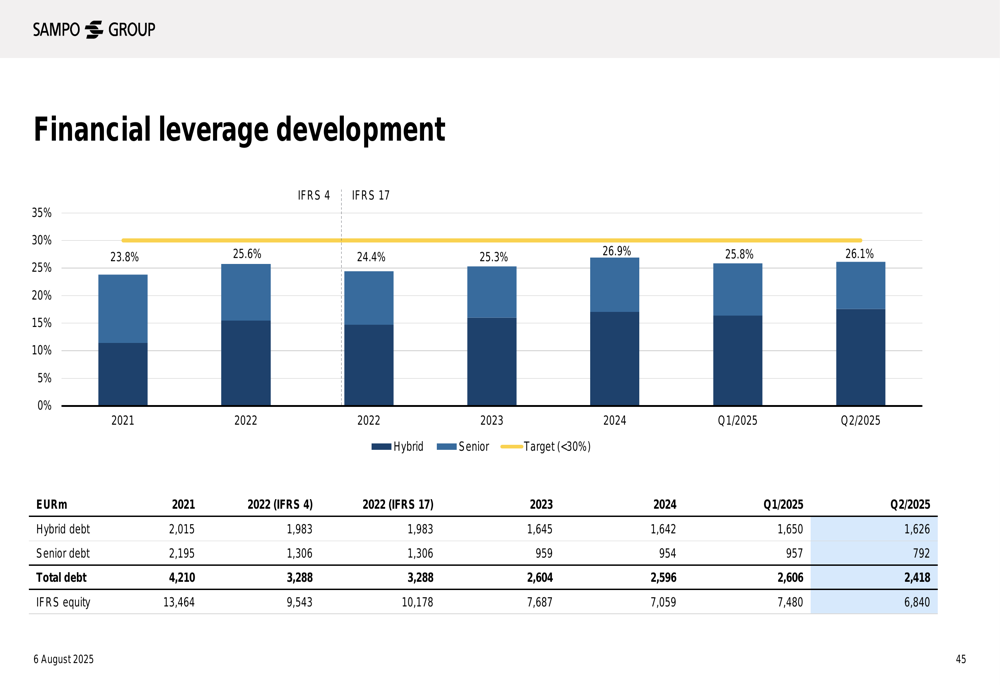

The company attributed the slight decrease in solvency to increased FX risk due to earnings accumulated in foreign currencies. Despite this, Sampo’s financial leverage remained well within its target of under 30%, as illustrated in the following chart:

In a move that underscores confidence in its financial strength, Sampo announced a new share buyback program of €200 million. This follows the company’s consistent approach to capital management and shareholder returns over recent years.

Forward-Looking Statements

Looking ahead, Sampo appears well-positioned to continue its growth trajectory, particularly in its target growth areas of Private Nordic and Private UK. The company’s focus on digital transformation and operational efficiency, combined with disciplined underwriting, should support continued improvement in underwriting results.

However, potential challenges include maintaining pricing discipline in competitive markets and managing the impact of inflation, which although stable at around 4%, remains a factor to monitor. The company’s increased FX risk due to earnings accumulated in foreign currencies also bears watching.

Overall, Sampo’s Q2 2025 presentation paints a picture of a company executing well on its strategic priorities, with strong growth across key segments and a positive outlook for the remainder of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.