TSX up after index logs fresh record high close

Samsara Inc. (NYSE:IOT) presented its Q2 FY26 financial results on September 4, 2025, highlighting continued strong growth in annual recurring revenue (ARR) and improving profitability metrics. The connected operations cloud provider saw its stock decline 0.59% in after-hours trading following the presentation, despite beating previous guidance.

Quarterly Performance Highlights

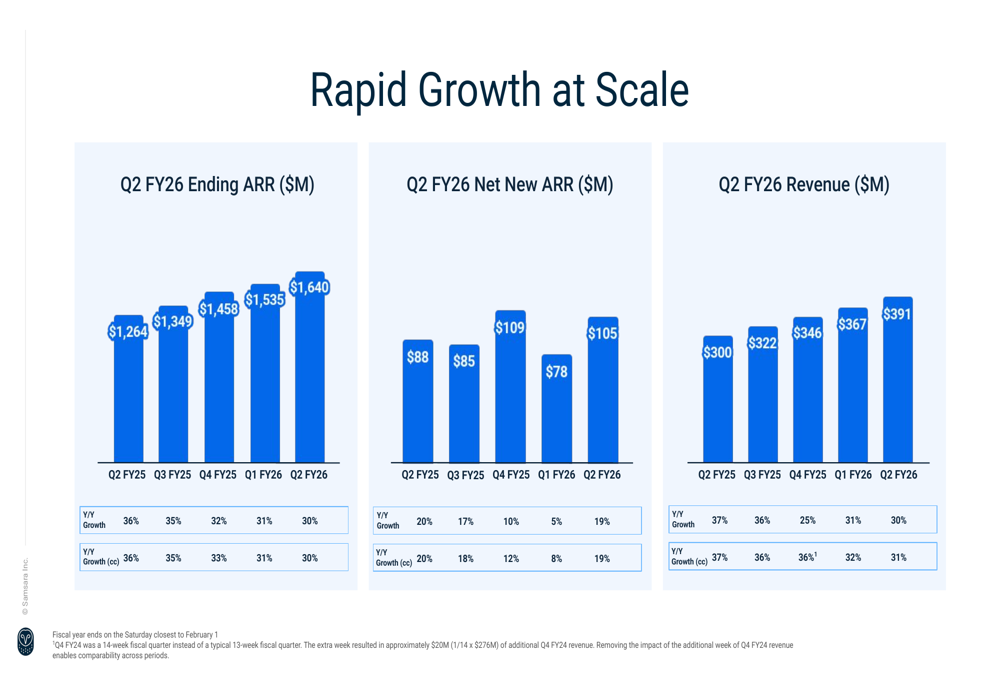

Samsara reported Q2 FY26 revenue of $391 million, representing 30% year-over-year growth and exceeding the company’s previous guidance midpoint by 5%. The company’s ARR reached $1.64 billion, also growing at 30% year-over-year.

"Our mission is to increase the safety, efficiency, and sustainability of the operations that power the global economy," Samsara stated in its presentation, highlighting the company’s focus on delivering tangible ROI for customers across various industries.

The company generated $44 million in adjusted free cash flow during the quarter, representing an 11% adjusted FCF margin, demonstrating Samsara’s improving capital efficiency.

As shown in the following chart of Samsara’s growth metrics:

Customer Growth and Expansion Strategy

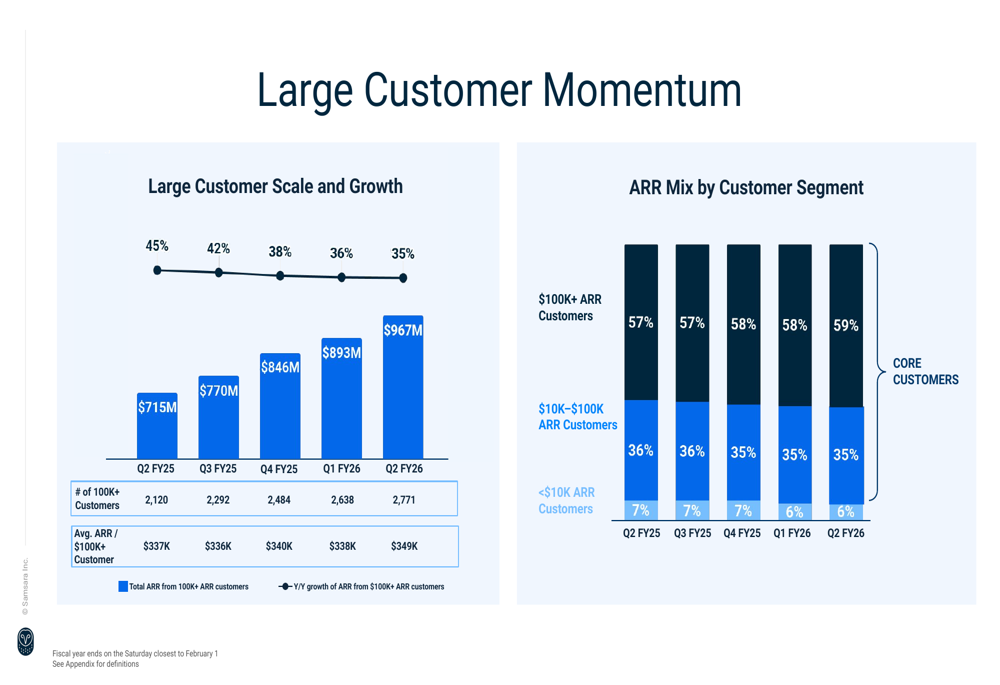

Samsara’s "land and expand" strategy continues to show strong results. The company added over 1,000 core customers for the fourth time in the last five quarters. Large customers remain a key driver of growth, with $100K+ ARR customers now numbering 2,771, and more than 20% of ARR coming from customers with $1M+ in ARR.

The company’s customer acquisition strategy shows depth across product offerings, with 9 of the top 10 new customer transactions including two or more products, and 8 of those including three or more products. On the expansion side, 15 of the top 25 customers expanded their relationships with Samsara during the quarter.

The following slide illustrates Samsara’s large customer momentum:

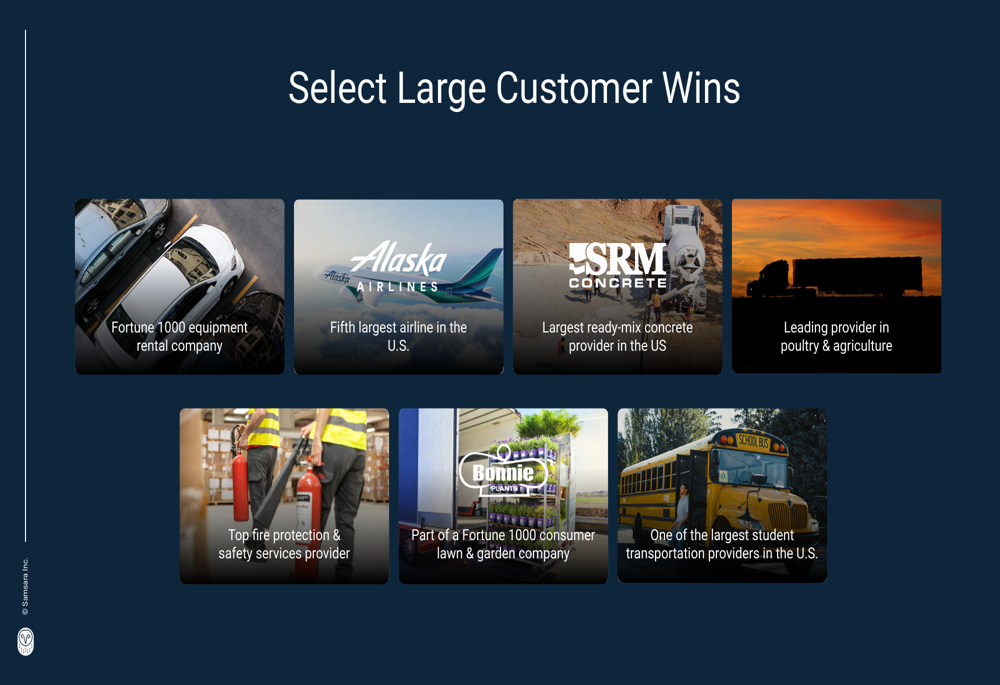

Samsara also highlighted several notable customer wins during the quarter, including Alaska Airlines, SRM Concrete (the largest ready-mix concrete provider in the U.S.), and several Fortune 1000 companies across different industries.

The customer wins demonstrate Samsara’s broad market appeal:

International Expansion and Product Innovation

International markets are becoming an increasingly important growth driver for Samsara, with 15% of net new annual contract value (ACV) coming from non-U.S. geographies in Q2. The construction sector continued its strong contribution, marking the eighth consecutive quarter as the highest contributor to net new ACV mix.

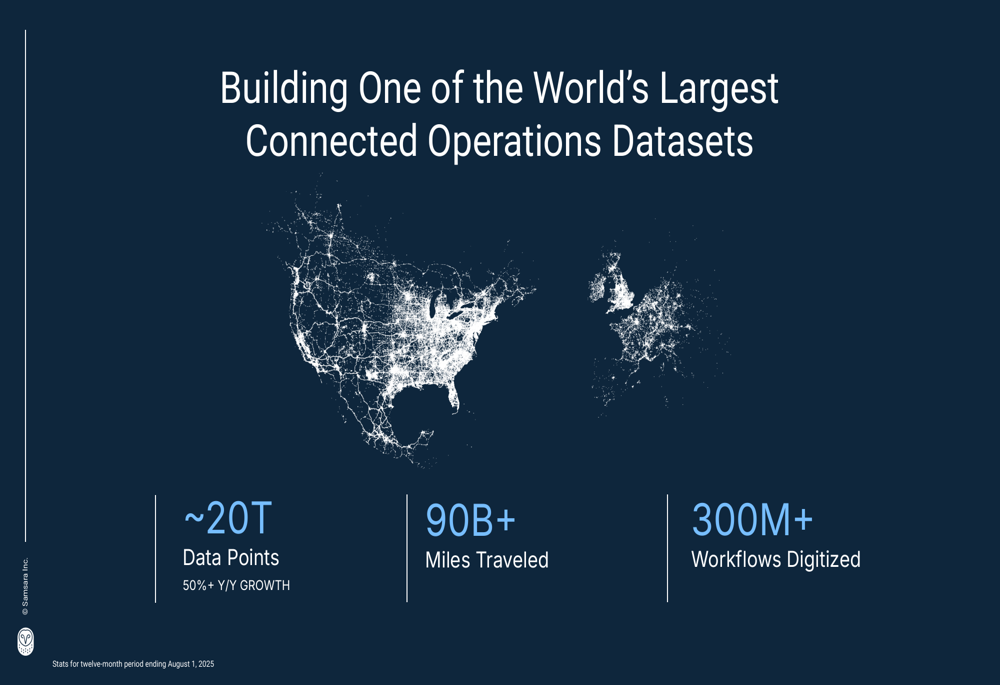

Samsara’s connected operations platform continues to process massive amounts of data, with approximately 20 trillion data points (growing over 50% year-over-year), 90+ billion miles traveled, and 300+ million workflows digitized in the twelve months ending August 1, 2025.

The scale of Samsara’s data operations is visualized here:

Product innovation remains a priority, with 8% of net new ACV coming from products launched within the last year. The company announced several new products at its BEYOND 2.5 event, including AI Multicam, Commercial Navigation, Connected Asset Maintenance, and Route Planning.

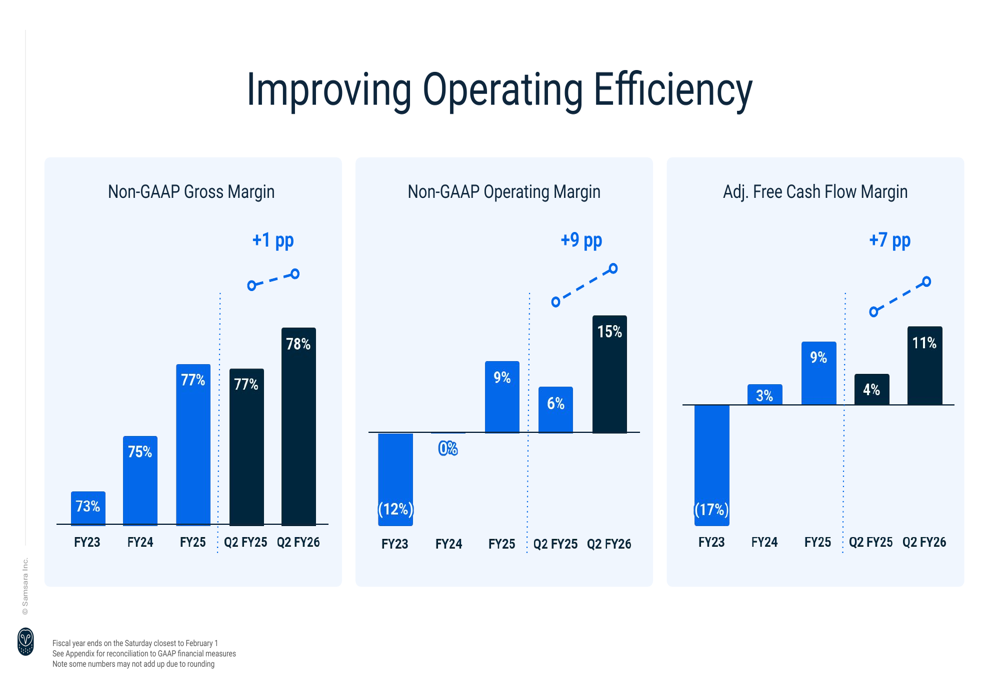

Improving Operating Efficiency

One of the most notable aspects of Samsara’s Q2 results was the continued improvement in operating efficiency. The company reported a non-GAAP gross margin of 78% for Q2 FY26, up from 73% in FY23. More impressively, non-GAAP operating margin reached 15% in Q2 FY26, a dramatic improvement from -12% in FY23.

The following chart illustrates Samsara’s margin improvements:

These improvements align with the company’s Q1 FY26 performance, where it reported a record non-GAAP gross margin of 79% and a non-GAAP operating margin of 14%. The slight quarter-over-quarter decrease in gross margin from 79% to 78% was offset by the improvement in operating margin from 14% to 15%.

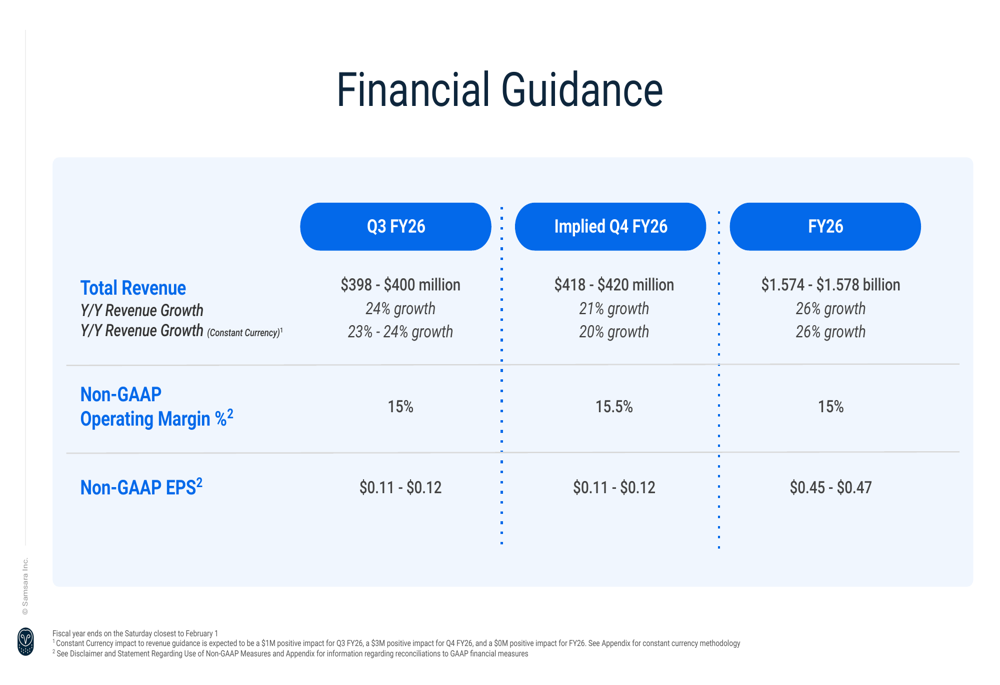

Forward Guidance and Outlook

Looking ahead, Samsara provided guidance for Q3 FY26 and the full fiscal year. For Q3, the company expects revenue between $398-400 million, representing 24% year-over-year growth, with a non-GAAP operating margin of 15%.

For the full FY26, Samsara raised its revenue guidance to $1.574-1.578 billion, representing 26% growth. This represents an increase from the previous guidance provided after Q1 results.

The company’s detailed financial guidance is shown here:

It’s worth noting that while Samsara continues to show strong growth, the projected 24% revenue growth for Q3 FY26 represents a slight deceleration from the 30% growth achieved in Q2. However, the company’s maintained operating margin guidance of 15% suggests confidence in its ability to balance growth and profitability.

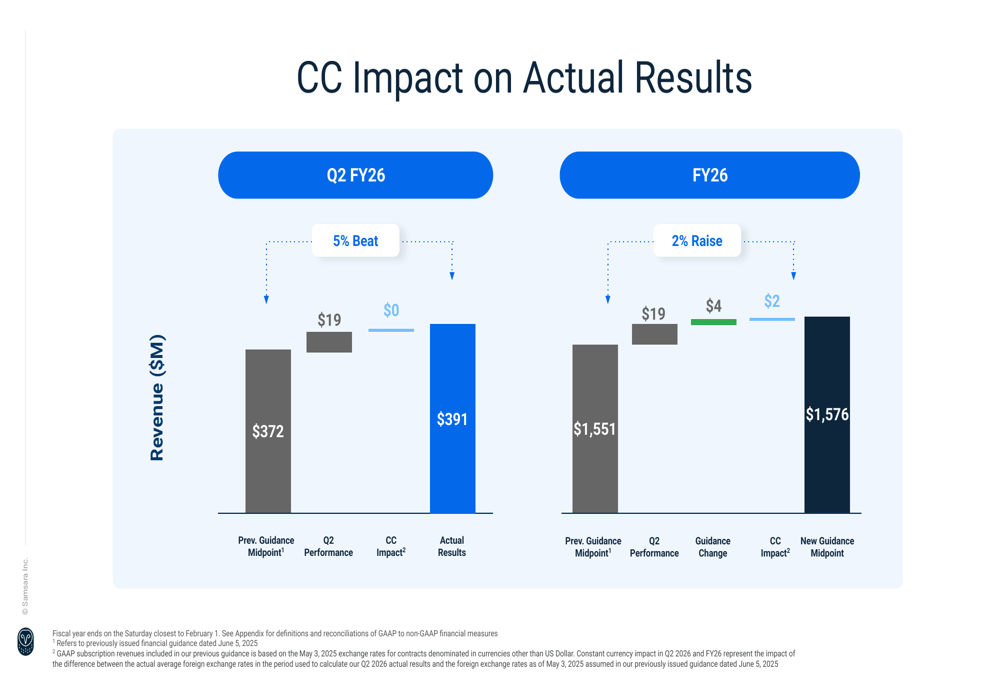

Samsara also provided insight into currency impacts on its results, noting that constant currency had a minimal impact on Q2 performance, with the company’s outperformance primarily driven by underlying business strength:

With its expanding product portfolio, growing customer base, and improving profitability metrics, Samsara appears well-positioned to continue its growth trajectory in the connected operations cloud market. The company’s focus on delivering tangible ROI for customers across diverse industries, combined with its international expansion efforts and product innovation, provides multiple avenues for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.