Functional Brands closes $8 million private placement and completes Nasdaq listing

Introduction & Market Context

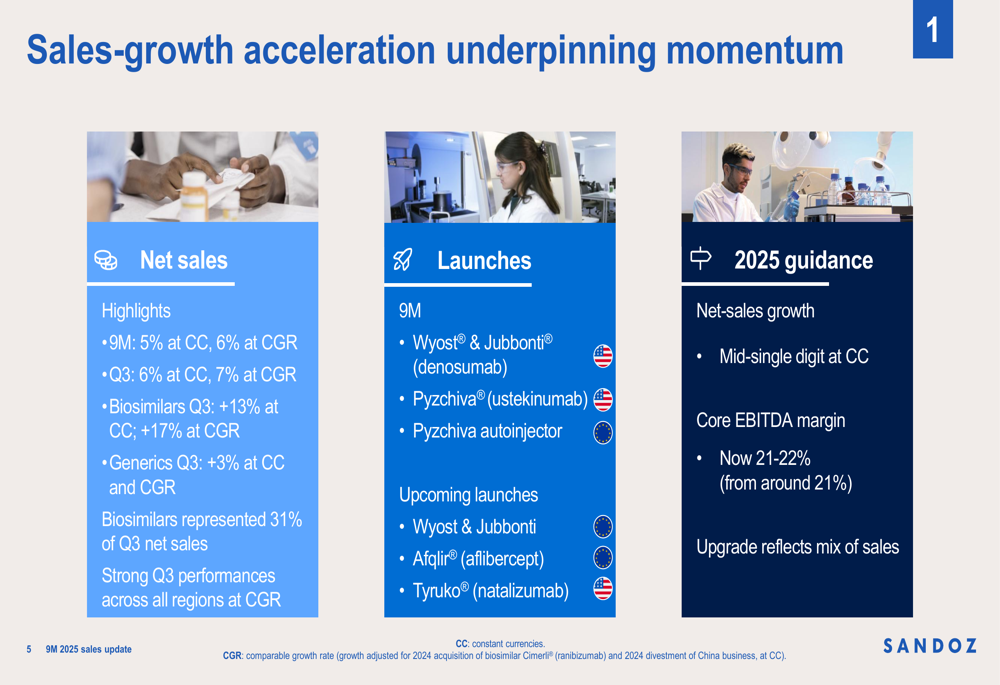

Sandoz Group AG (SWX:SDZ) reported accelerating sales growth in its Q3 2025 presentation, driven largely by its expanding biosimilars business. The company achieved 6% growth at constant currencies (CC) and 7% at comparable growth rate (CGR) for the quarter, marking its 16th consecutive quarter of growth. Sandoz shares have gained 41.6% over the past six months and are currently trading near $50.70, close to their 52-week high of $52.88.

The company’s strategic pivot toward higher-margin biosimilars continues to bear fruit, with this segment now constituting 31% of Q3 net sales, up from 29% in the same period last year. This improved sales mix has allowed Sandoz to upgrade its full-year core EBITDA margin guidance.

Quarterly Performance Highlights

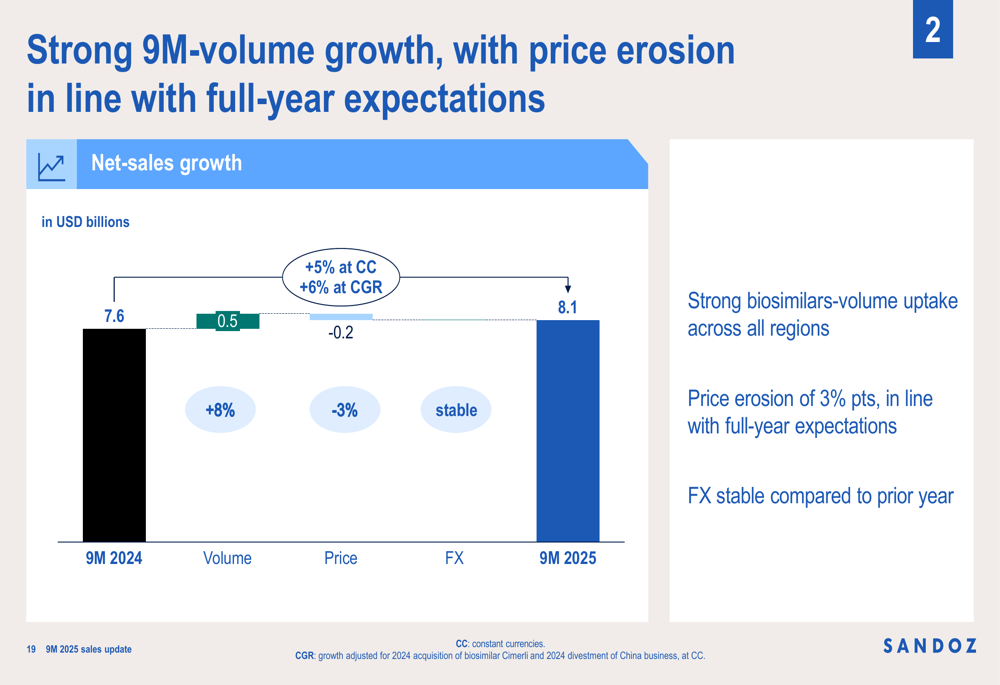

Sandoz reported Q3 2025 net sales of $2.8 billion, up from $2.6 billion in Q3 2024. The 6% constant currency growth reflects strong volume increases of 8%, partially offset by price erosion of 3%, which the company notes is in line with full-year expectations.

As shown in the following chart of sales growth and business mix:

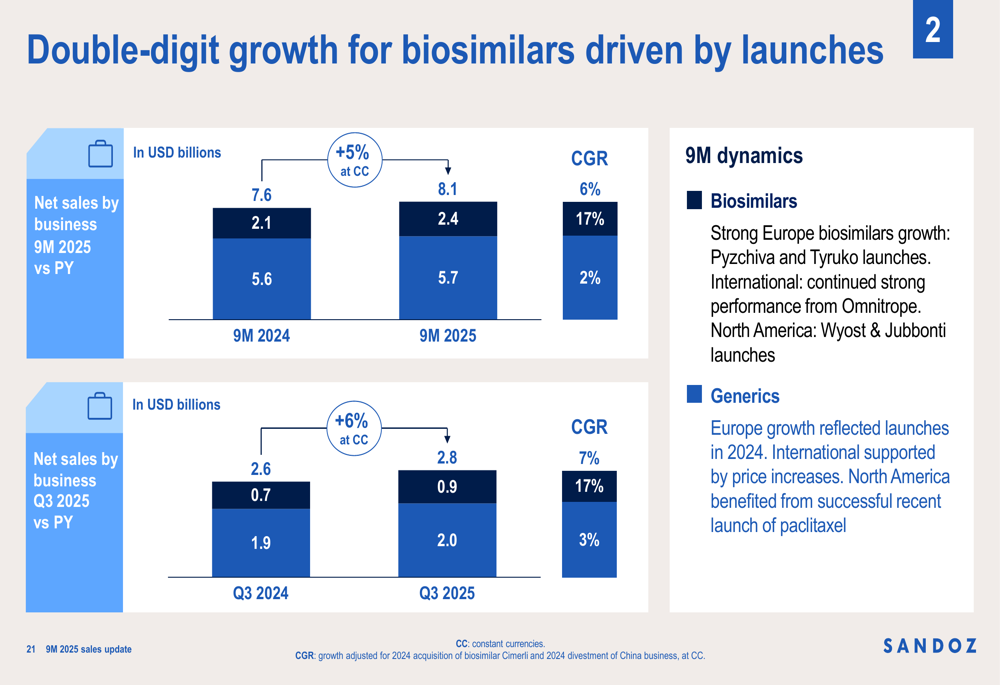

Biosimilars were the standout performer, with Q3 sales growing 13% at constant currency and 17% at comparable growth rate. The generics business, while more mature, still delivered 3% growth in the quarter. This performance continues the company’s acceleration throughout 2025, with quarterly growth rates of 3% in Q1, 5% in Q2, and now 6% in Q3.

The components of Sandoz’s sales growth clearly illustrate the volume-driven nature of their performance:

Biosimilars Growth Strategy

Biosimilars now represent nearly a third of Sandoz’s business, with the segment contributing $0.9 billion to Q3 sales compared to $0.7 billion in the prior year. This 17% comparable growth rate significantly outpaces the generics business and is reshaping Sandoz’s profit profile.

The company’s biosimilars growth is being fueled by several key product launches, including Pyzchiva (ustekinumab) in the US, which includes a first commercially available autoinjector in Europe, and Wyost & Jubbonti (denosumab), which were the first denosumab biosimilars in the US market.

The following chart breaks down the performance of biosimilars versus generics:

CEO Richard Saynor emphasized during the earnings call that the company is "making excellent progress on our biosimilar launches" and views biosimilars as "a global market, not just a U.S. market." This global approach is evident in Sandoz’s launch strategy, with additional rollouts of Afqlir (aflibercept) and Tyruko (natalizumab) anticipated in Q4.

Regional Performance

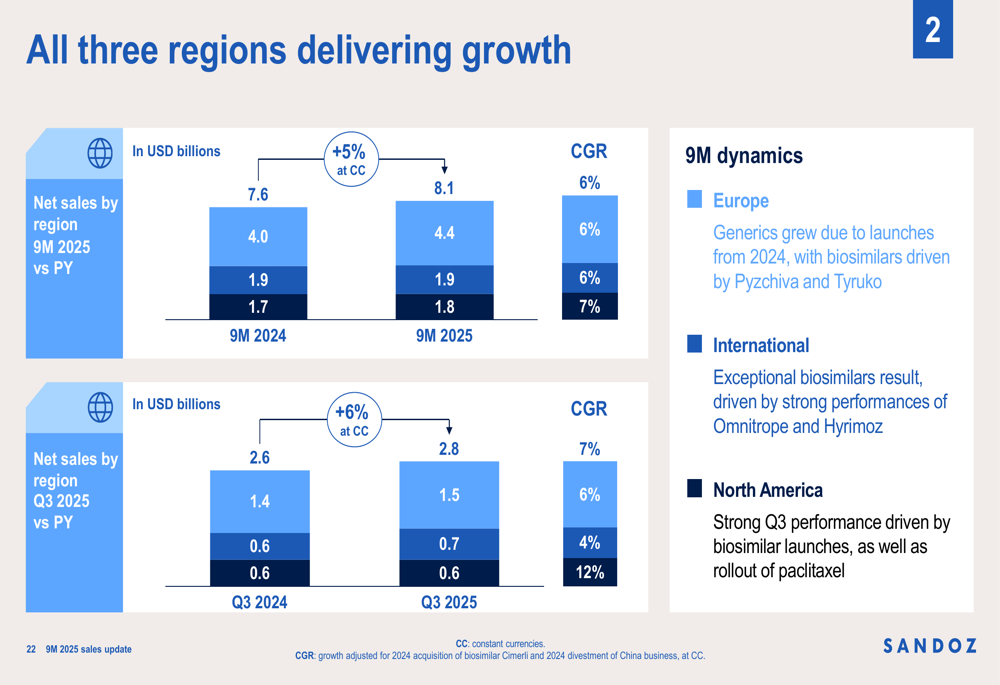

All regions delivered growth in Q3, with Europe showing particularly strong performance at 12% CGR. North America grew at 4% CGR, while International markets expanded by 6% CGR.

Europe’s exceptional performance was driven by the launches of Pyzchiva and Tyruko, while North America benefited from the successful launches of Wyost & Jubbonti and paclitaxel. The International segment saw continued strong performance from established products like Omnitrope and Hyrimoz.

The regional breakdown of sales performance shows:

Generics Momentum

While biosimilars are growing faster, generics remain the core of Sandoz’s business, representing 69% of Q3 sales. The company launched 115 medicines in the first nine months of 2025, with 280 launches across markets.

Key generic launches included lisdexamfetamine in the US, which is gaining encouraging market share and targeting an originator market of $2.8 billion, and rivaroxaban in Germany, where Sandoz achieved a first-to-market position targeting an originator market of $957 million.

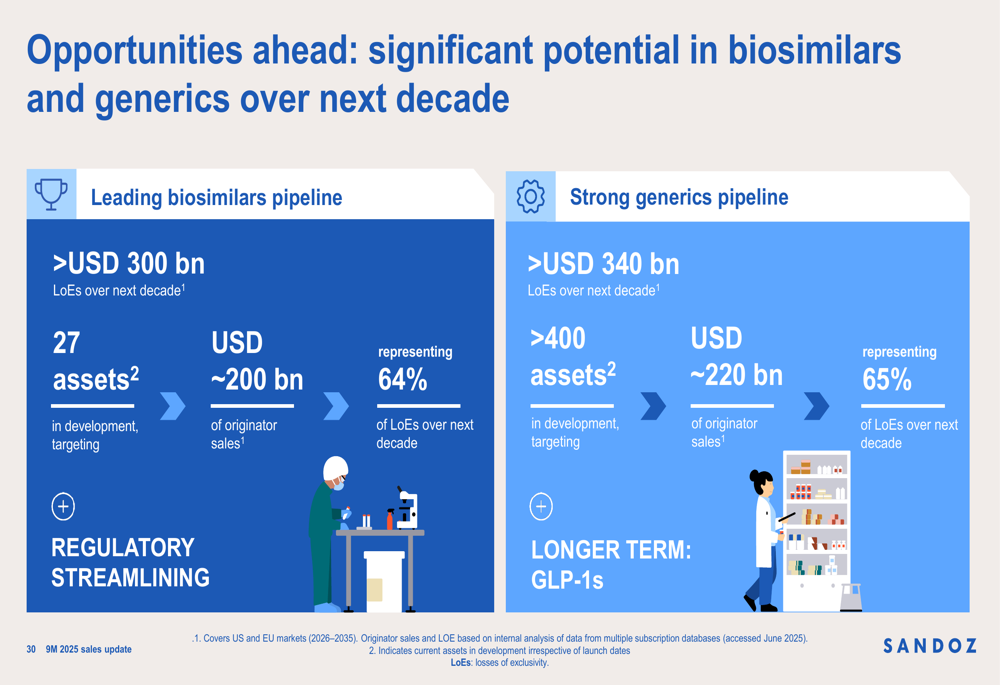

The company maintains a robust generics pipeline with over 400 assets in development targeting approximately $220 billion of originator sales, representing 65% of loss of exclusivity (LoE) opportunities over the next decade.

Forward-Looking Statements

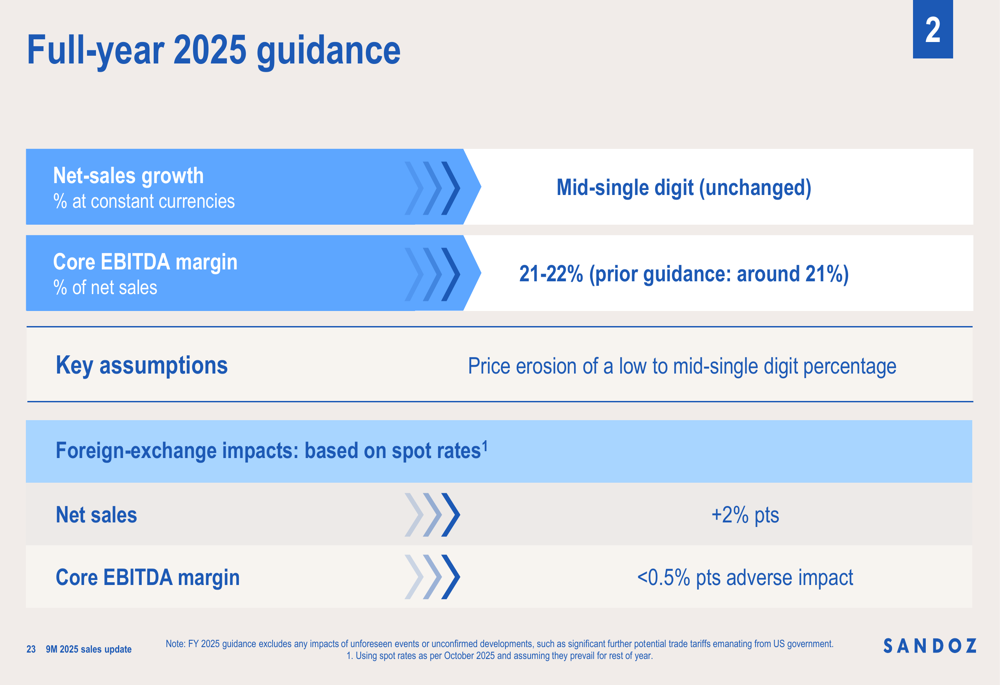

Based on its strong performance, Sandoz has upgraded its full-year 2025 guidance. While maintaining its mid-single-digit net sales growth projection at constant currencies, the company has raised its core EBITDA margin guidance to 21-22% from its previous guidance of around 21%.

The updated guidance reflects:

Looking further ahead, Sandoz highlighted significant potential in both its biosimilars and generics pipelines. The company has 27 biosimilar assets in development targeting approximately $200 billion of originator sales, representing 64% of loss of exclusivity opportunities over the next decade.

The company expects price erosion to remain in the low to mid-single digit percentage range, consistent with the 3% experienced in the first nine months of 2025. Foreign exchange impacts, based on current spot rates, are expected to contribute approximately 2 percentage points to net sales growth, with less than a 0.5 percentage point adverse impact on core EBITDA margin.

With its robust pipeline and increasing contribution from higher-margin biosimilars, Sandoz appears well-positioned to maintain its growth trajectory through 2025 and beyond, though the company will need to continue managing price erosion and increasing competition, particularly in the European biosimilars market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.