Street Calls of the Week

Introduction & Market Context

Sanmina Corporation (NASDAQ:SANM) presented its Q3 fiscal 2025 financial results on July 28, 2025, showcasing strong performance that exceeded the company’s outlook across key metrics. The electronic manufacturing services provider reported a 10.9% year-over-year revenue increase amid continued demand across its diversified end markets. Despite the positive results, Sanmina’s stock closed at $98.58, down slightly by 0.24% on the day of the presentation.

The company highlighted its progress on the pending ZT Systems acquisition, which is expected to significantly expand Sanmina’s presence in the growing Data Center and AI infrastructure markets. This strategic move comes as global data center investments are projected to nearly triple by 2028.

Quarterly Performance Highlights

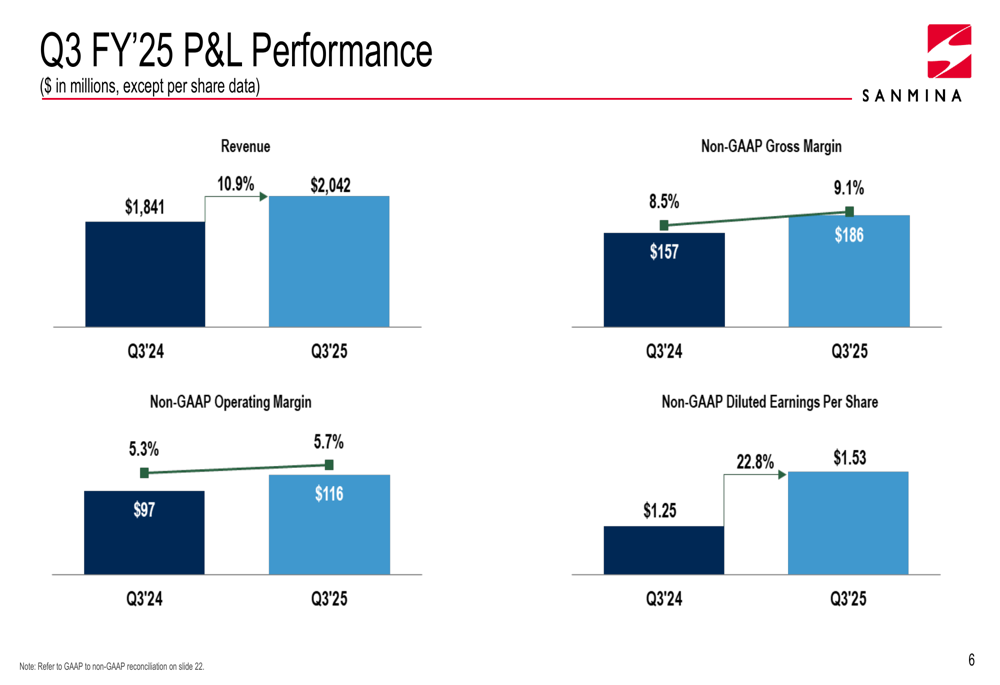

Sanmina reported Q3 fiscal 2025 revenue of $2.042 billion, exceeding its outlook range of $1.925-$2.025 billion and representing a 10.9% increase from $1.841 billion in the same quarter last year. The company’s non-GAAP gross margin reached 9.1%, surpassing the projected 8.6-9.0% range, while operating margin hit 5.7%, at the high end of the 5.4-5.8% outlook.

As shown in the following chart of quarterly financial performance:

Non-GAAP diluted earnings per share grew impressively by 22.8% year-over-year to $1.53, significantly exceeding the company’s outlook of $1.35-$1.45. This strong performance reflects what the company described as "solid operational execution" in a dynamic market environment.

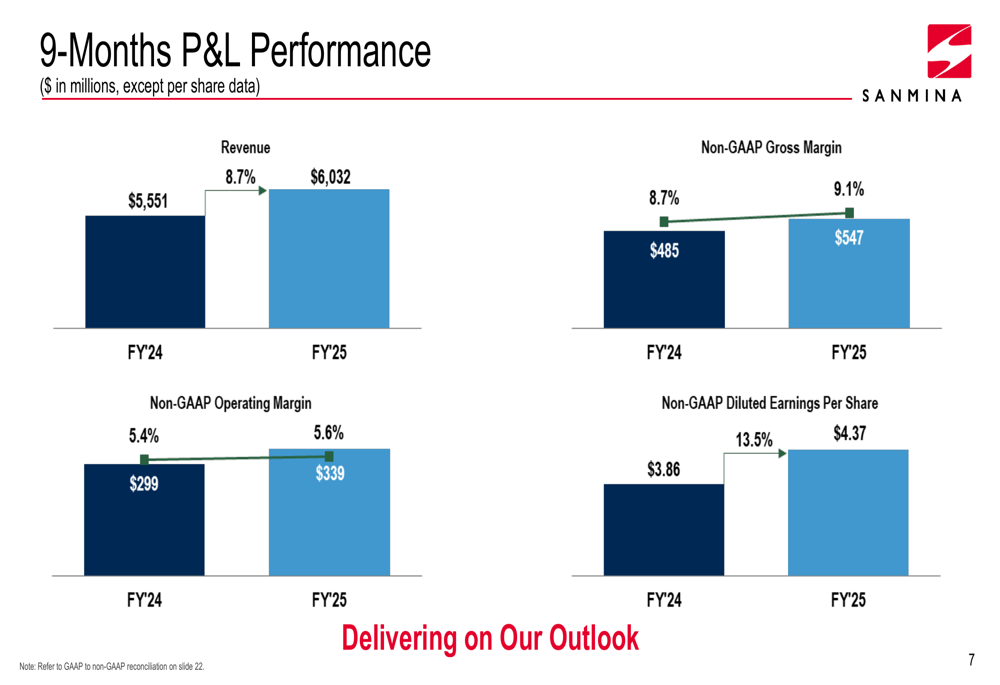

The nine-month year-to-date results also showed consistent growth, with revenue up 8.7% to $6.032 billion and non-GAAP diluted EPS increasing by 13.5% to $4.37 compared to the same period in fiscal 2024.

The company’s year-to-date performance is illustrated in this chart:

Detailed Financial Analysis

Sanmina’s performance varied across its two main business segments. The Integrated Manufacturing Solutions (IMS) segment generated $1.648 billion in revenue, up from $1.478 billion in Q3 FY’24, while maintaining a relatively stable gross margin of 7.5% compared to 7.6% last year. The Components, Products and Services (CPS) segment saw revenue increase to $422 million from $388 million, with a significant gross margin improvement from 11.5% to 14.7%.

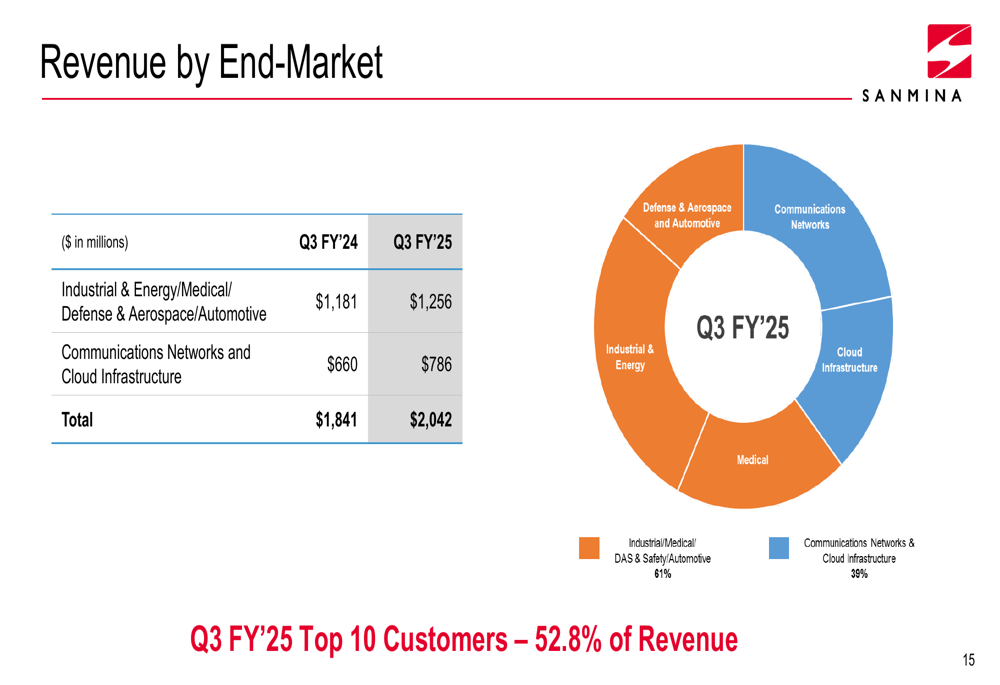

The company’s revenue diversification across end markets continues to provide stability. As shown in the following breakdown:

Industrial, Energy, Medical (TASE:BLWV), Defense, Aerospace, and Automotive sectors collectively contributed 61% of revenue ($1.256 billion), while Communications Networks and Cloud Infrastructure accounted for 39% ($786 million). The company noted that its top 10 customers represented 52.8% of total revenue.

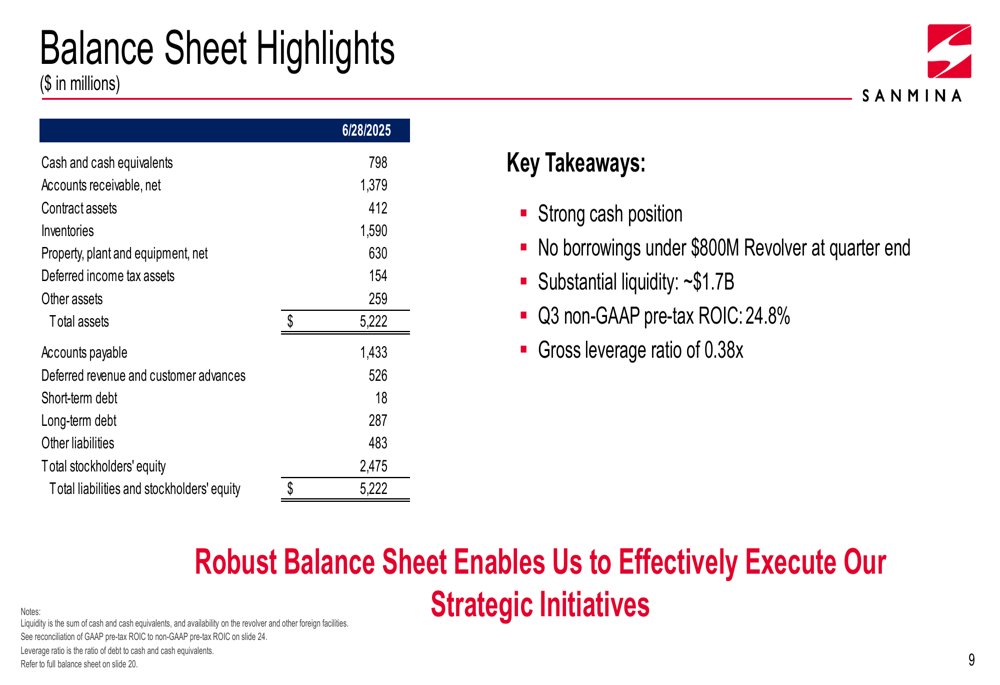

Sanmina maintained a robust balance sheet with $798 million in cash and cash equivalents and minimal debt ($18 million short-term, $287 million long-term). The company’s non-GAAP pre-tax return on invested capital reached an impressive 24.8%, with a low gross leverage ratio of 0.38x.

The key balance sheet metrics are summarized here:

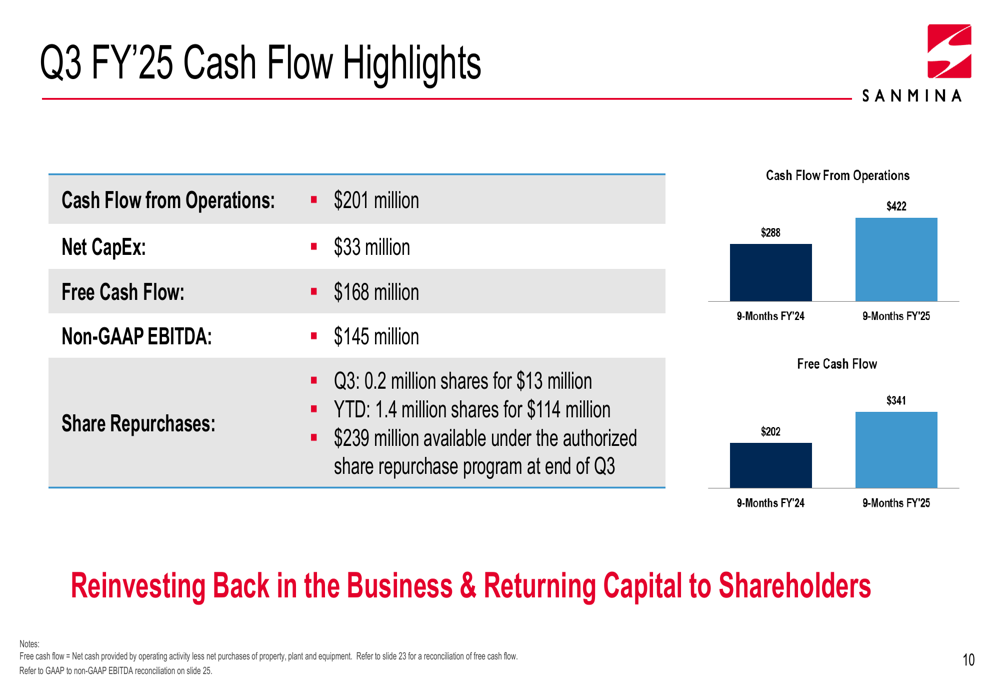

Cash flow generation remained strong, with $201 million in cash flow from operations and $168 million in free cash flow during Q3. Year-to-date free cash flow reached $341 million, a significant improvement from $202 million in the same period last year. The company continued its share repurchase program, buying back 0.2 million shares for $13 million during the quarter and 1.4 million shares for $114 million year-to-date.

The cash flow performance is illustrated in this chart:

Strategic Initiatives

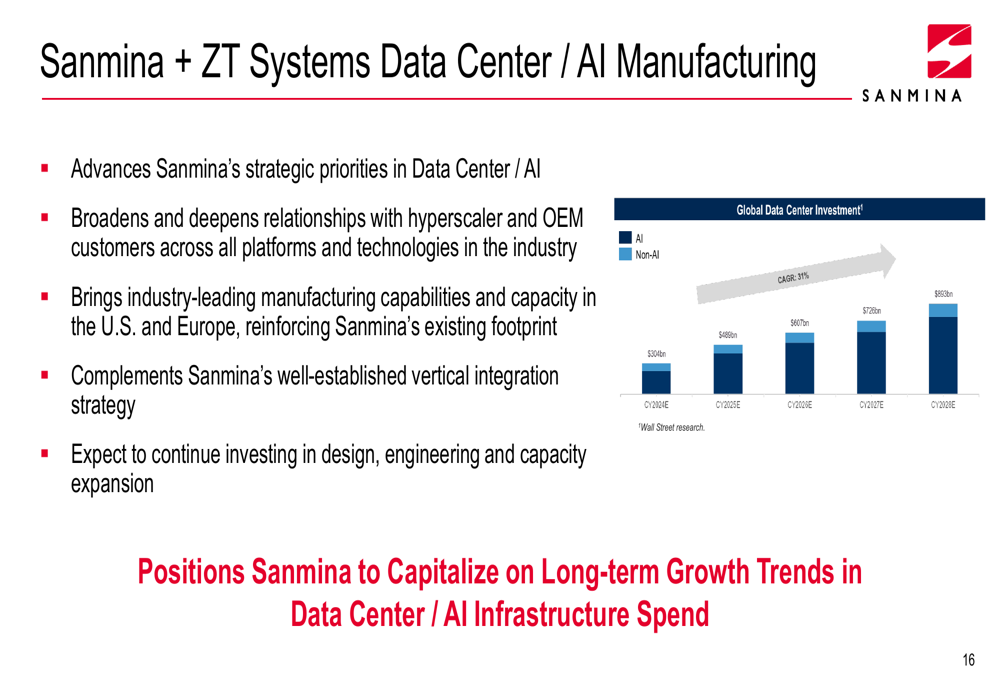

A significant focus of the presentation was the pending acquisition of ZT Systems’ Data Center/AI Manufacturing business, which Sanmina expects to close near the end of calendar year 2025. The company reported that all regulatory filings are proceeding according to plan, with bridge financing in place and permanent debt financing on track.

This strategic acquisition is expected to add $5-6 billion in net revenue on a run-rate basis and potentially double Sanmina’s total revenue within three years. Management anticipates the deal will be accretive to non-GAAP EPS in the first year after closing, with further accretion expected as growth and synergies materialize.

The strategic rationale and market opportunity for the ZT Systems acquisition is shown here:

Sanmina emphasized that this acquisition advances its strategic priorities in the Data Center/AI space, broadens relationships with hyperscaler and OEM customers, and brings industry-leading manufacturing capabilities in the U.S. and Europe. The company plans to continue investing in design, engineering, and capacity expansion to capitalize on the projected growth in global data center investment, which is expected to increase from approximately $304 billion to $893 billion between 2024 and 2028.

The company also highlighted its end-to-end solutions for the Data Center/AI market, encompassing architecture design, firmware and software engineering, electro-mechanical systems, test validation, regulatory certification, and build-to-order/configure-to-order fulfillment capabilities.

Forward-Looking Statements

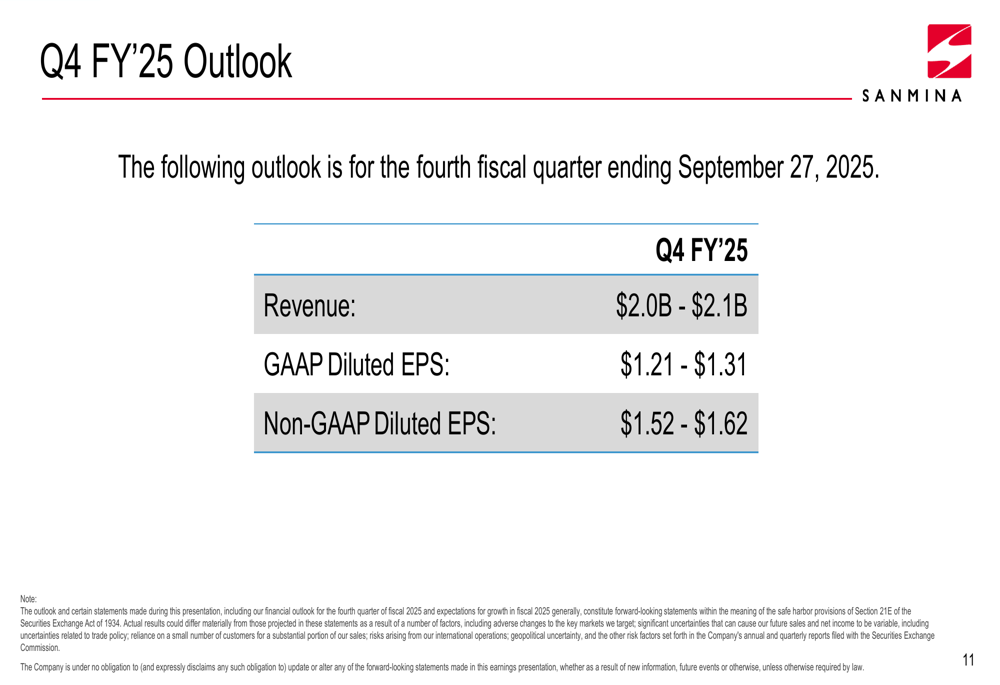

For the fourth quarter of fiscal 2025 ending September 27, 2025, Sanmina provided the following outlook:

The company expects Q4 revenue between $2.0-$2.1 billion and non-GAAP diluted EPS of $1.52-$1.62. Management indicated that this outlook aligns with achieving their fiscal 2025 growth and profitability objectives.

Looking further ahead, Sanmina expressed optimism about fiscal 2026, citing new program wins and demand improvements as drivers for continued growth. The company aims to maintain a net leverage ratio of 1.0x to 2.0x over time following the ZT Systems acquisition, which would be in line with industry peers.

In the presentation summary, CEO Jure Sola stated the company is "Excited About the Opportunities Ahead," particularly highlighting the strategic importance of the ZT Systems acquisition in positioning Sanmina to capitalize on long-term growth trends in Data Center/AI infrastructure spending.

With consistent execution across financial metrics, strategic advancement in high-growth markets, and a strong balance sheet to support future initiatives, Sanmina appears well-positioned to continue its growth trajectory through the remainder of fiscal 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.