Dollar rebounds despite Fed independence worries; euro slips

Introduction & Market Context

SANUWAVE Health Inc (SNWV) presented its first quarter fiscal year 2025 results on May 9, 2025, highlighting substantial revenue growth and a transition to profitability. The wound care technology company, currently trading at $28.55, has positioned itself to capitalize on the industry’s shift toward evidence-based medicine and reimbursement models.

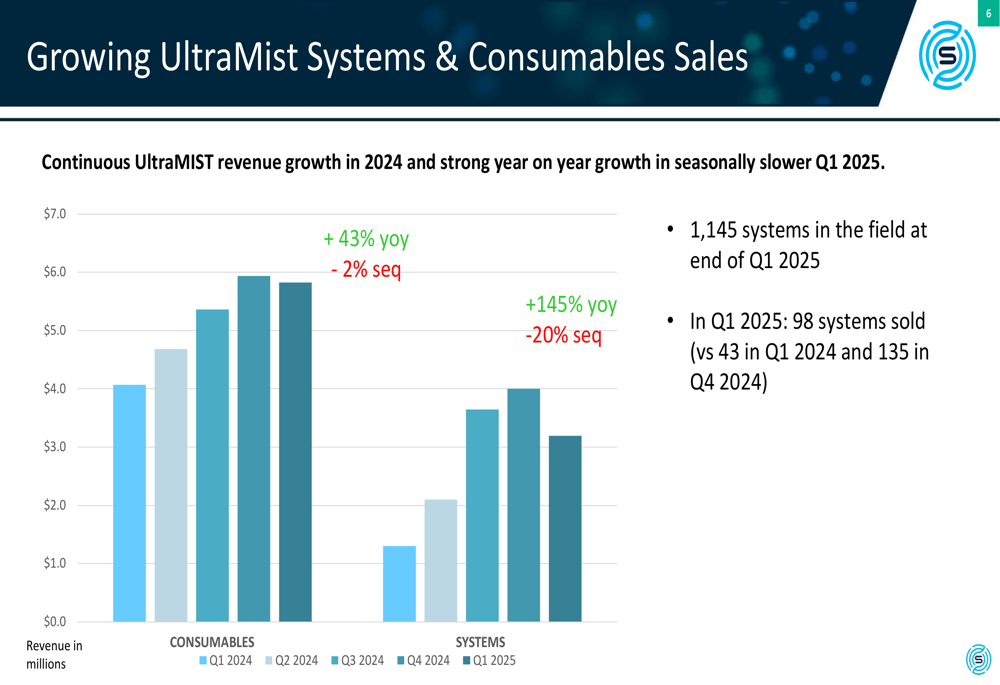

The company’s UltraMist system, which continues to gain market adoption, forms the cornerstone of SANUWAVE’s growth strategy in the competitive wound care market. With 1,145 systems now deployed in the field, the company is building a strong foundation for recurring revenue through consumables sales.

Quarterly Performance Highlights

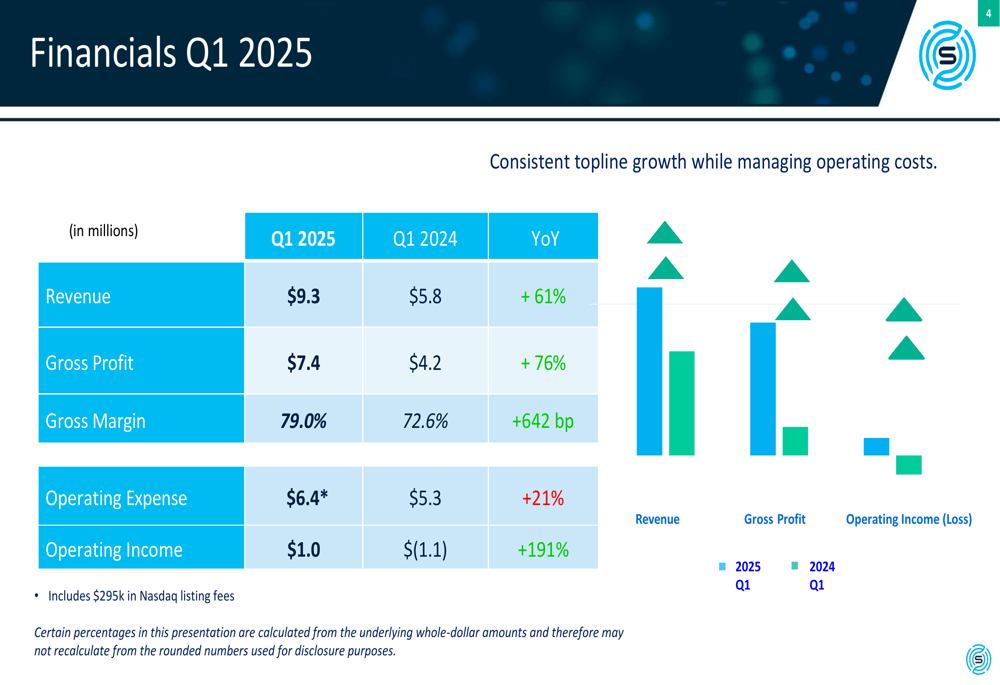

SANUWAVE reported impressive financial results for Q1 2025, with revenue reaching $9.3 million, a 61% increase compared to $5.8 million in the same period last year. More significantly, the company achieved operating income of $1.0 million, representing a 191% improvement from the $1.1 million operating loss recorded in Q1 2024.

As shown in the following chart detailing the company’s quarterly performance metrics, gross profit increased by 76% year-over-year to $7.4 million, while gross margin expanded by 642 basis points to 79.0%:

Operating expenses increased by 21% year-over-year to $6.4 million, which included $295,000 in Nasdaq listing fees. Despite this increase, the company’s expense growth remained well below its revenue growth rate, demonstrating improving operational efficiency and scale.

Detailed Financial Analysis

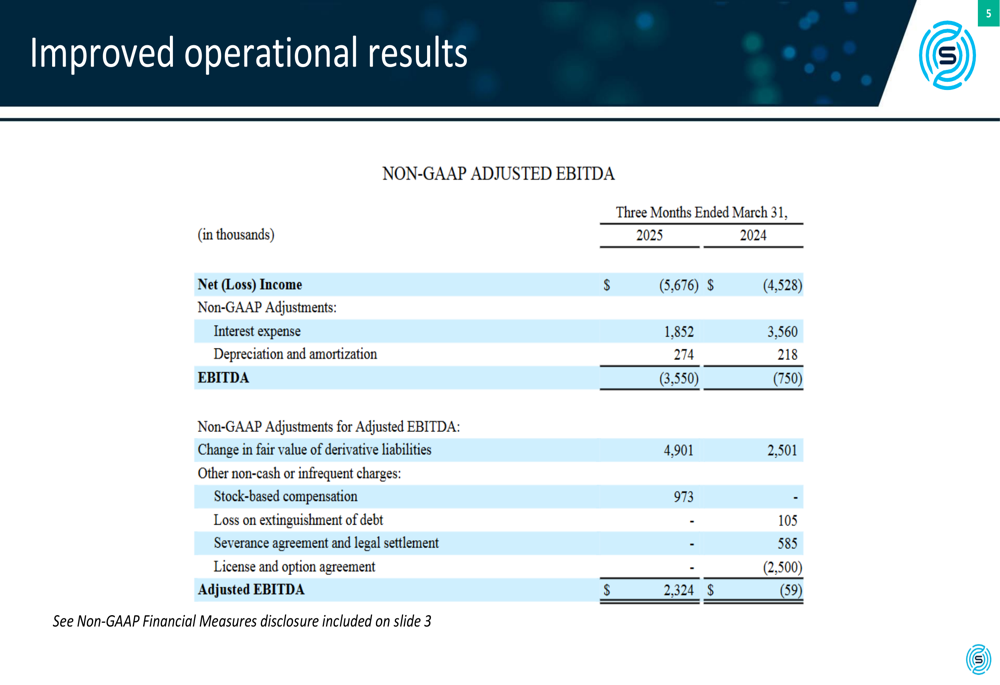

The company’s improved operational results are further illustrated in its reconciliation of net loss to adjusted EBITDA. For Q1 2025, SANUWAVE reported adjusted EBITDA of $2.32 million, a significant improvement from the negative $59,000 reported in Q1 2024.

The following table provides a detailed breakdown of the company’s EBITDA reconciliation, showing the various adjustments made to arrive at the adjusted EBITDA figure:

While the company still reported a net loss of $5.68 million for the quarter, this was primarily due to non-cash items, particularly a $4.9 million change in fair value of derivative liabilities. Interest expense decreased significantly year-over-year from $3.56 million to $1.85 million, reflecting improvements in the company’s capital structure.

Strategic Initiatives & Market Position

SANUWAVE’s growth strategy centers around expanding its UltraMist system installations and driving recurring revenue through consumables. The company has shown consistent growth in both segments throughout 2024 and into Q1 2025.

As illustrated in the following chart, both systems and consumables sales have demonstrated strong year-over-year growth, despite Q1 typically being a seasonally slower quarter:

System sales nearly tripled in Q1 2025, with 98 units sold compared to 43 in Q1 2024, representing a 145% year-over-year increase. While this represents a 20% sequential decline from Q4 2024’s 135 units, the company attributed this to normal seasonal patterns.

Consumables revenue, which provides a recurring revenue stream from the installed base, grew 43% year-over-year, with only a modest 2% sequential decline from Q4 2024, demonstrating the stability of this revenue segment.

Forward-Looking Statements

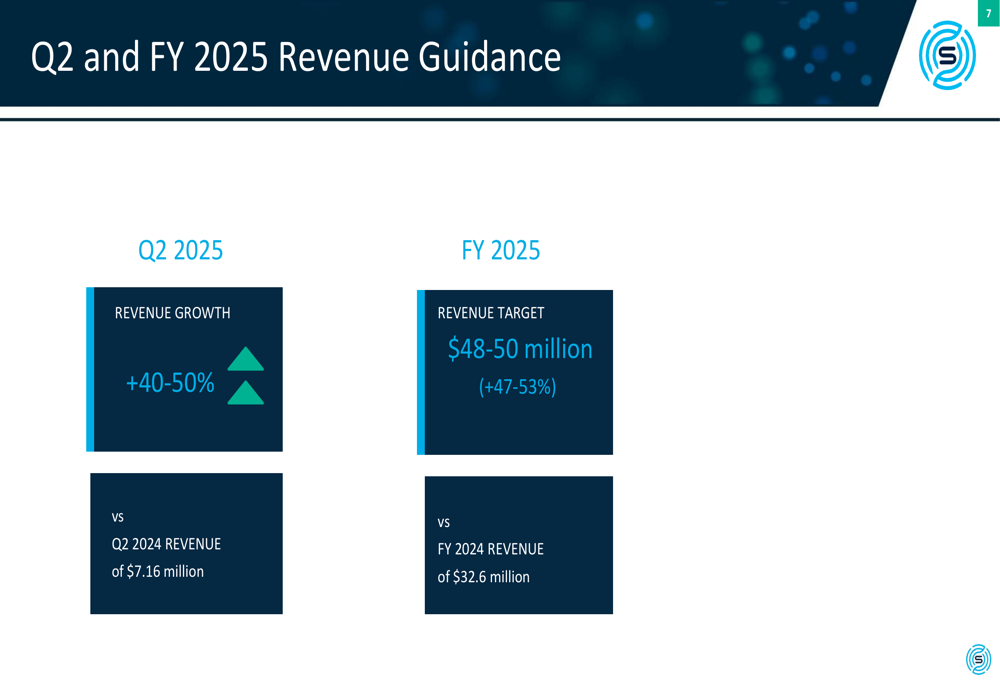

SANUWAVE provided optimistic guidance for both Q2 and the full fiscal year 2025. For the second quarter, the company expects revenue growth of 40-50% compared to Q2 2024’s $7.16 million. For the full year, SANUWAVE is targeting revenue of $48-50 million, representing growth of 47-53% over FY 2024’s $32.6 million.

The following slide outlines the company’s revenue guidance:

Management highlighted several factors supporting their positive outlook, including the ongoing shift in wound care toward evidence-based medicine and reimbursement models that align incentives for patients, payors, and providers.

The company’s strategic position is summarized in the following slide, emphasizing its approved products, strong IP protection, established reimbursement, focused sales force, expanded manufacturing capacity, and capital-light business model:

With its focus on "Rapid, Profitable Growth," SANUWAVE appears well-positioned to continue its positive momentum through 2025, leveraging its expanding installed base and improving operational efficiency to drive further margin expansion and profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.