Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Saputo Inc . (TSX:SAP) presented its fourth quarter and year-end results for fiscal year 2025 on June 6, showing resilience in the face of continued market pressures. The Canadian dairy giant reported stable overall performance, with strong results in North America counterbalancing significant challenges in its International Sector, particularly in Argentina where currency devaluation issues impacted profitability.

The company’s stock closed at C$26.51 on June 5, 2025, up 0.34% ahead of the results announcement, and has traded between C$22.59 and C$32.15 over the past 52 weeks, indicating moderate investor confidence in the dairy processor’s performance amid volatile global dairy markets.

Quarterly Performance Highlights

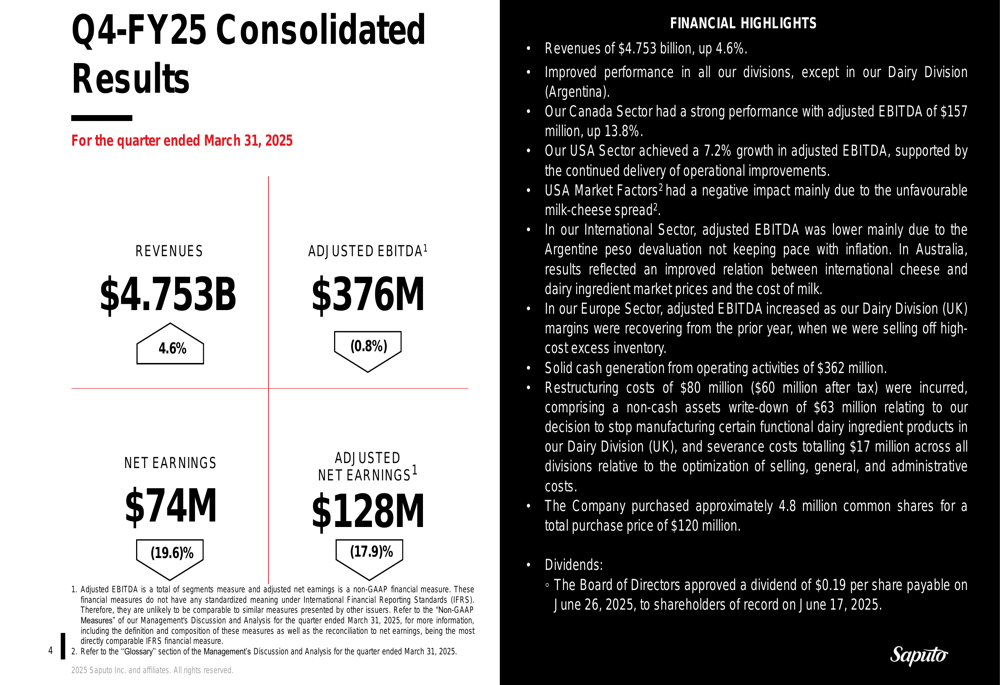

Saputo reported consolidated revenues of $4.753 billion for Q4 FY25, representing a 4.6% increase compared to the same period last year. However, adjusted EBITDA slightly decreased by 0.8% to $376 million, while net earnings fell more significantly by 19.6% to $74 million. Adjusted net earnings also declined by 17.9% to $128 million.

As shown in the following consolidated results:

Despite these mixed results, the company highlighted its solid cash generation from operating activities of $362 million and continued share repurchase program, having bought back approximately 4.8 million common shares for a total of $120 million during the quarter. The Board of Directors approved a dividend of $0.19 per share payable on June 26, 2025.

Detailed Financial Analysis by Sector

The company’s performance varied significantly across its geographical segments, with North American operations showing strength while international markets faced challenges.

Canada Sector

The Canada Sector delivered impressive results with revenues of $1.258 billion, up 5.5% compared to Q4-FY24, and adjusted EBITDA of $157 million, representing a robust 13.8% increase. The adjusted EBITDA margin stood at a healthy 12.5%. This strong performance was attributed to operational efficiencies, favorable product mix, higher sales volumes, and lower general and administrative costs.

USA Sector

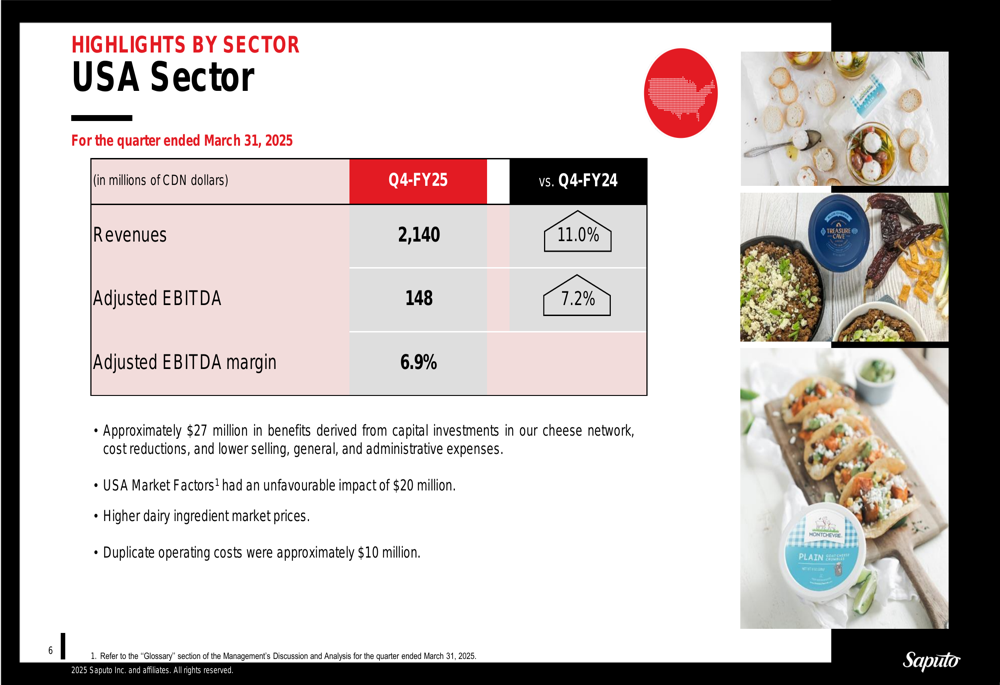

The USA Sector also performed well, with revenues increasing by 11.0% to $2.140 billion and adjusted EBITDA rising by 7.2% to $148 million. The company realized approximately $27 million in benefits from capital investments in its cheese network, cost reductions, and lower selling, general, and administrative expenses. However, these gains were partially offset by unfavorable USA Market Factors, which had a negative impact of $20 million, and duplicate operating costs of approximately $10 million.

International Sector

The International Sector faced significant headwinds, with revenues declining by 10.1% to $1.020 billion and adjusted EBITDA plummeting by 46.6% to $47 million. The adjusted EBITDA margin contracted to 4.6%. The poor performance was primarily attributed to challenges in Argentina, where peso devaluation did not keep pace with inflation, leading to higher production costs and reduced profitability from US dollar-denominated export sales.

Europe Sector

The Europe Sector showed strong recovery with revenues of $335 million, up 15.5%, and adjusted EBITDA of $24 million, representing a substantial 60.0% increase. The adjusted EBITDA margin improved to 7.2%. This favorable comparison to the previous fiscal year was largely due to selling excess inventory produced at higher milk prices through bulk cheese sales volumes.

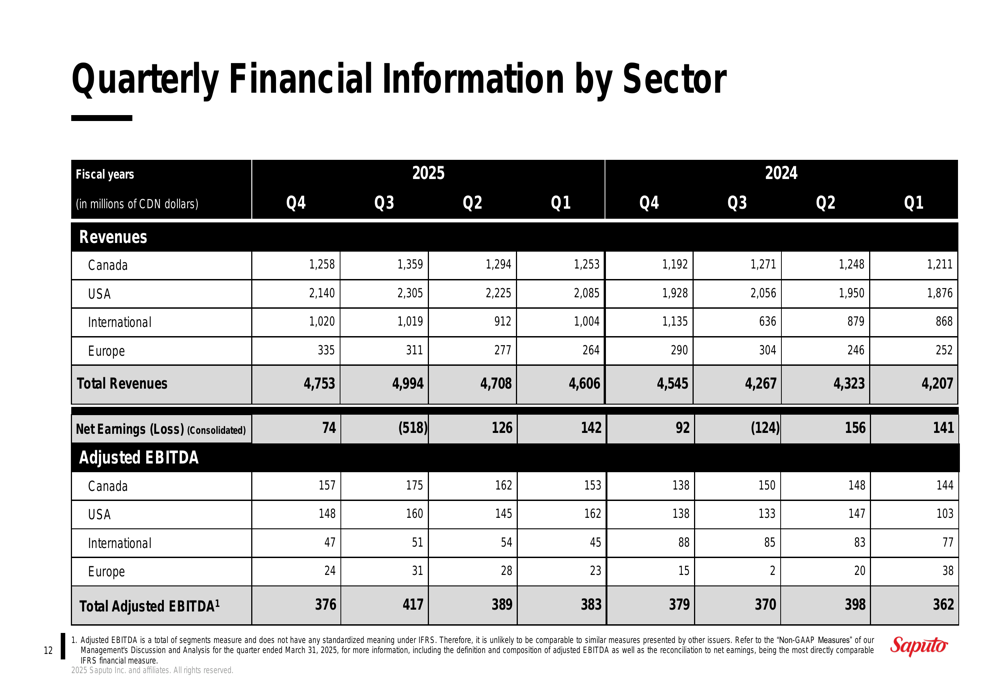

The quarterly financial information across all sectors provides a comprehensive view of the company’s performance over the past two fiscal years:

Forward-Looking Statements

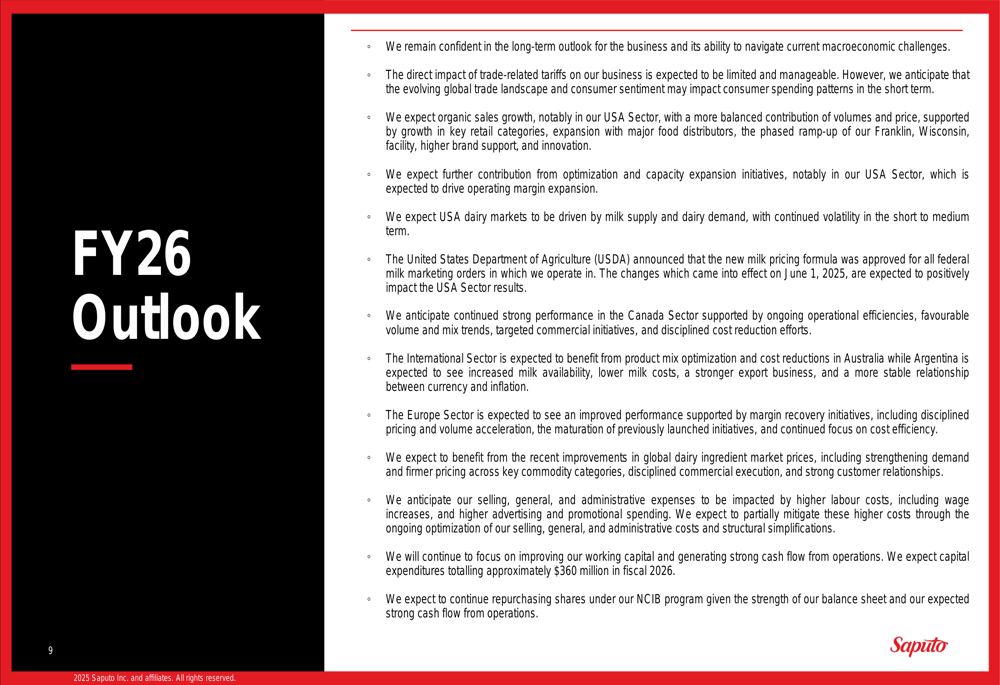

Looking ahead to fiscal year 2026, Saputo expressed confidence in its long-term outlook despite acknowledging continued market challenges. The company expects limited impact from trade-related tariffs and anticipates organic sales growth in the USA Sector, with further contributions from optimization and capacity expansion initiatives.

For the Canada Sector, Saputo expects continued strong performance, while the International Sector should benefit from product mix optimization and cost reductions in Australia, along with a more stable relationship between currency and inflation in Argentina. The Europe Sector is projected to show improved performance, benefiting from improvements in global dairy ingredient market prices.

The company plans capital expenditures of approximately $360 million in fiscal 2026 and will continue its share repurchase program under the NCIB (Normal Course Issuer Bid).

Strategic Initiatives

Throughout the presentation, Saputo emphasized its focus on disciplined cost containment efforts and the positive contributions from strategic initiatives. In the USA Sector, the company highlighted approximately $27 million of savings and benefits derived from capital investments in its cheese network, cost reductions, and lower selling, general, and administrative expenses.

The company also noted the strong performance of its focus brands in a highly competitive environment, suggesting that its brand strategy is yielding positive results despite market pressures. Additionally, Saputo’s efforts to improve working capital and generate strong cash flow remain key priorities for fiscal 2026.

Compared to the first quarter of fiscal 2025, when the company reported strong financial results with consolidated revenues of $4.6 billion and adjusted EBITDA of $383 million, the fourth quarter shows some deterioration in profitability, particularly in the International Sector. However, the continued strength in North American operations and the recovery in Europe provide a counterbalance to these challenges as the company enters fiscal year 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.