Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

Saratoga Investment Corp (NYSE:SAR) presented its fiscal second quarter 2026 results on October 8, 2025, highlighting portfolio quality and consistent performance despite recent challenges. The business development company’s stock has been under pressure following its Q4 2025 earnings miss, with shares trading near $24.00 in after-hours trading, down 1.68% following the presentation and approaching its 52-week low of $21.10.

The presentation comes against a backdrop of mixed performance, as Saratoga missed analyst expectations in its previous quarter with an EPS of $0.56 versus the forecasted $0.7029, and revenue of $31.3 million against expectations of $33.29 million.

Quarterly Performance Highlights

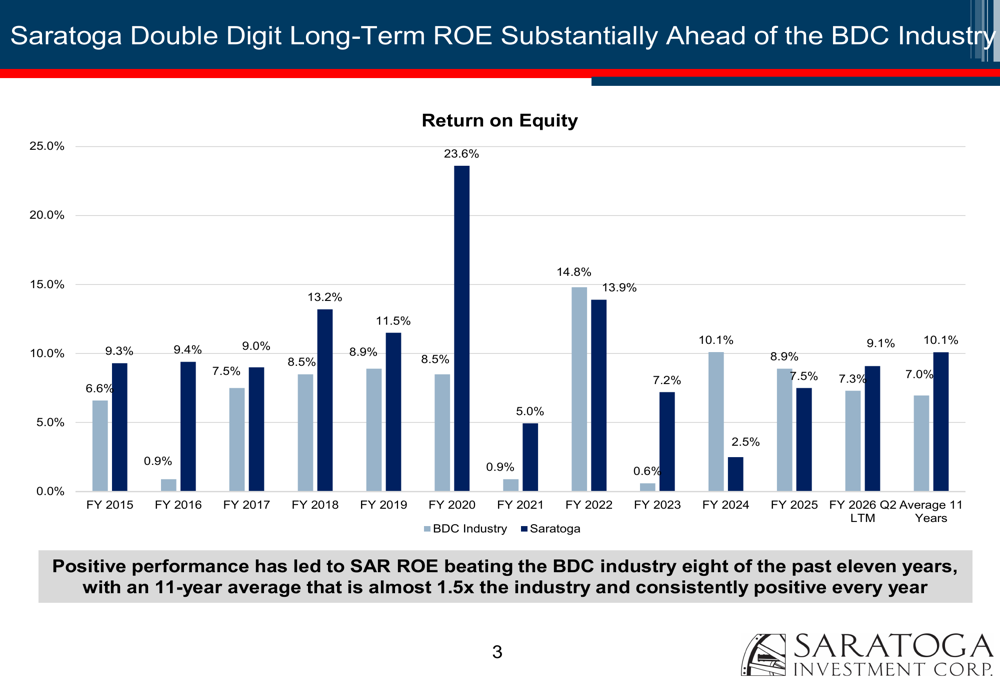

Saratoga reported continued strength in its investment portfolio quality with 99.7% of loan investments maintaining the highest internal rating. The company posted a last twelve months (LTM) return on equity of 9.1%, exceeding the industry average of 7.3%.

As shown in the following chart comparing Saratoga’s ROE to the BDC industry average, the company has consistently outperformed the sector over the long term:

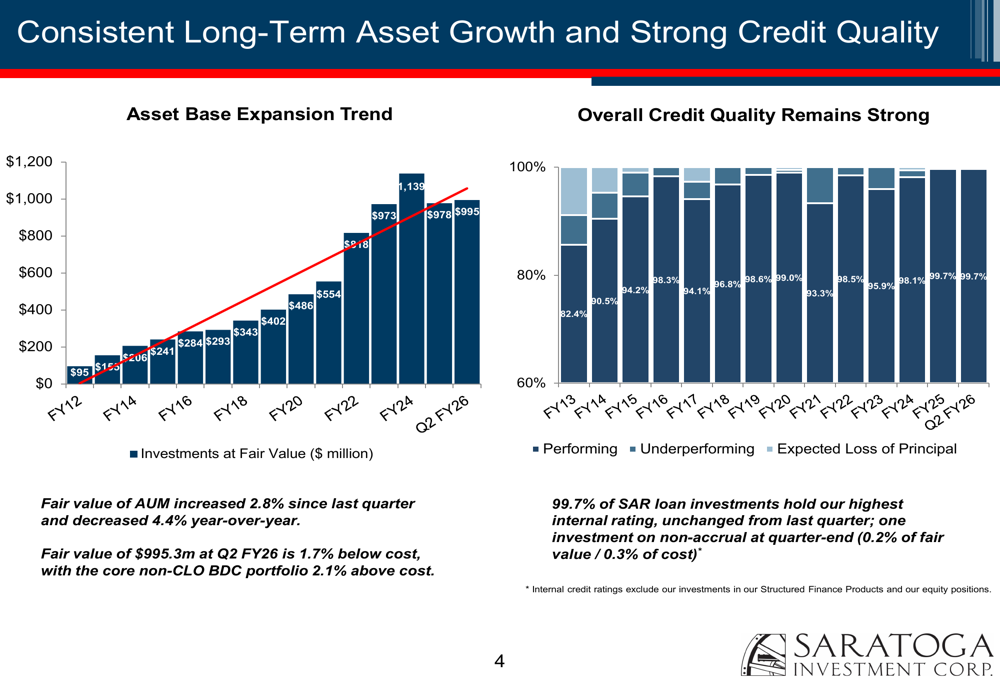

The company’s assets under management (AUM) reached $995.3 million, representing a 2.8% increase from the previous quarter. Saratoga also declared a quarterly dividend of $0.75 per share for the quarter ending November 30, 2025, maintaining its commitment to shareholder returns despite recent earnings volatility.

Net investment income (NII) for Q2 FY26 was $9.1 million, with NII per share decreasing from $0.66 in Q1 FY26 to $0.58 in Q2 FY26. This decline aligns with the challenges highlighted in the company’s recent earnings report, where adjusted NII per share had decreased by 40.4% year-over-year.

Portfolio Quality & Composition

Saratoga’s presentation emphasized its disciplined approach to credit quality, with only one investment on non-accrual at quarter-end, representing just 0.2% of fair value and 0.3% of cost. This quality-focused approach is illustrated in the company’s asset growth and credit quality chart:

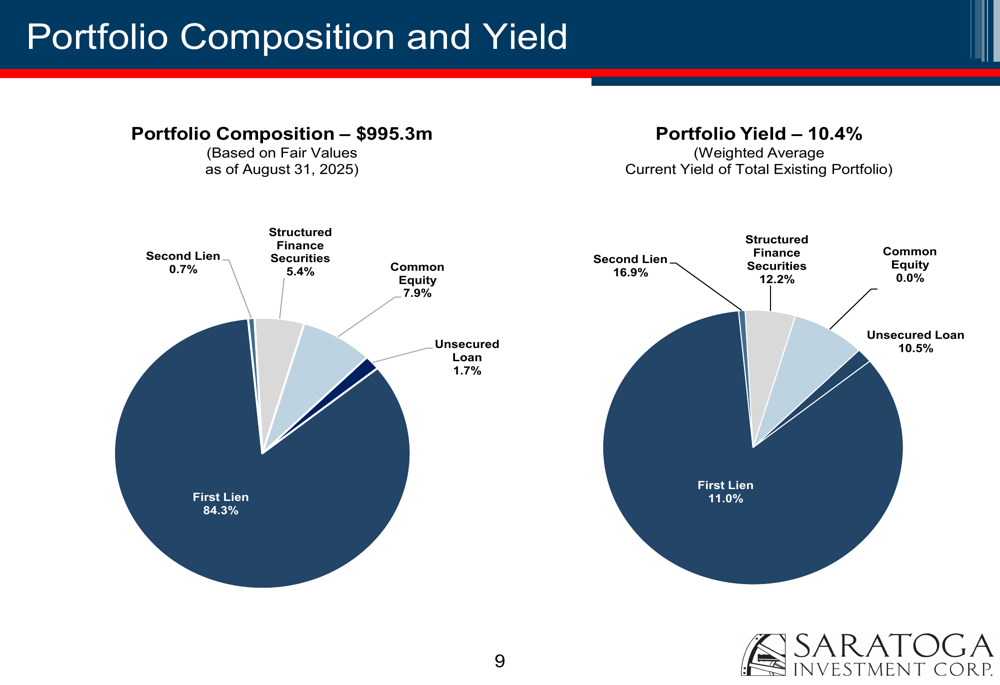

The portfolio composition remains heavily weighted toward first lien debt, providing greater security in uncertain economic conditions. As of August 31, 2025, the portfolio composition by fair value consisted of:

Saratoga maintains significant diversification across 39 distinct industries, with the largest exposures in Healthcare Services (9.7%), Structured Finance Securities (7.3%), and Consumer Services (6.0%). Geographically, investments are spread primarily across the Midwest (36.2%) and Southeast (20.7%), with additional allocations in the Northeast, West, and Southwest regions.

Growth Trajectory & NAV Performance

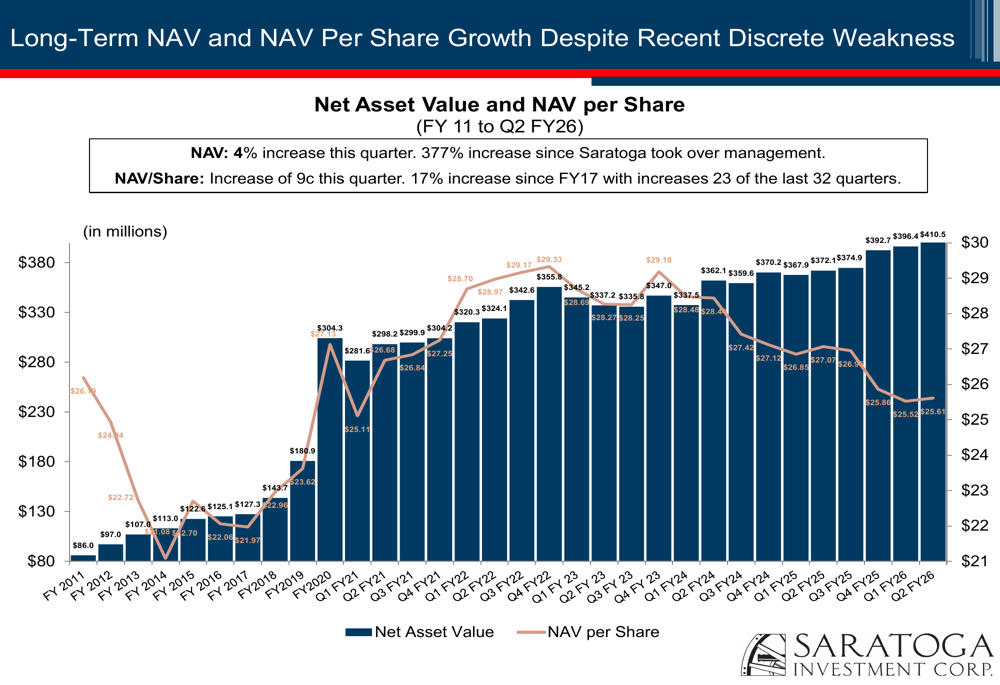

Despite recent earnings challenges, Saratoga has demonstrated consistent growth in Net Asset Value (NAV), which increased by 4% in the most recent quarter to $410.5 million. This represents a 377% increase since management took over the company. NAV per share also increased by $0.09 during the quarter to $25.61, marking growth in 23 of the last 32 quarters.

The following chart illustrates this long-term growth trajectory:

The company maintains strong liquidity with $406.8 million available at quarter-end, providing the ability to grow AUM by 41% without requiring new external financing. This positions Saratoga to capitalize on investment opportunities while maintaining financial flexibility in a challenging market environment.

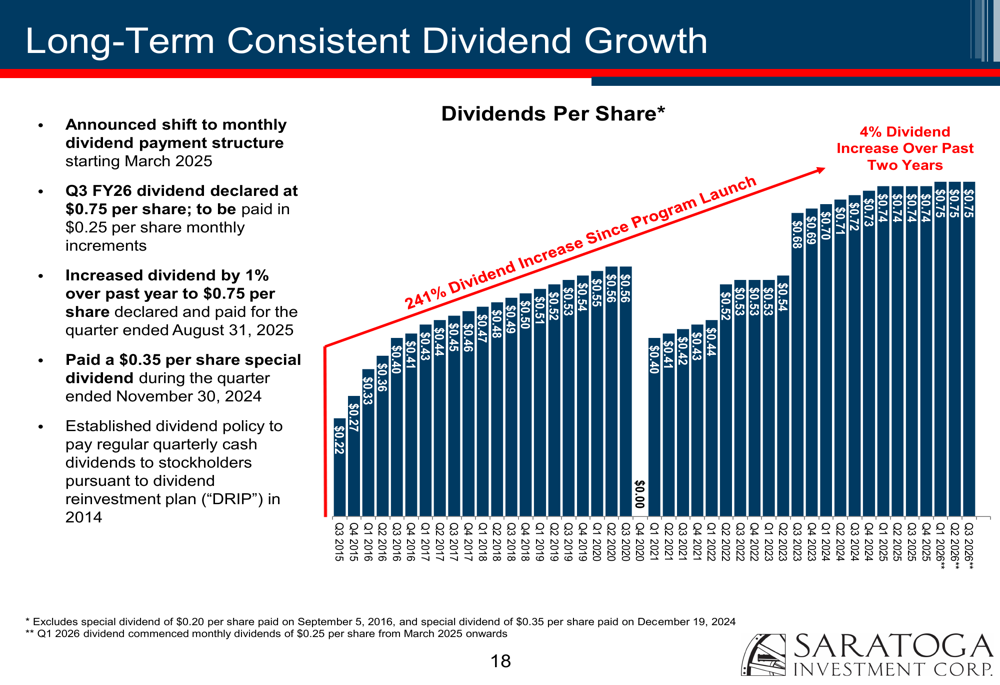

Dividend Strategy & Shareholder Returns

Saratoga has maintained a consistent dividend growth strategy, increasing its dividend by 4% over the past two years. The quarterly dividend has grown from $0.22 in Q3 2015 to the current $0.75 per share, as illustrated in the following chart:

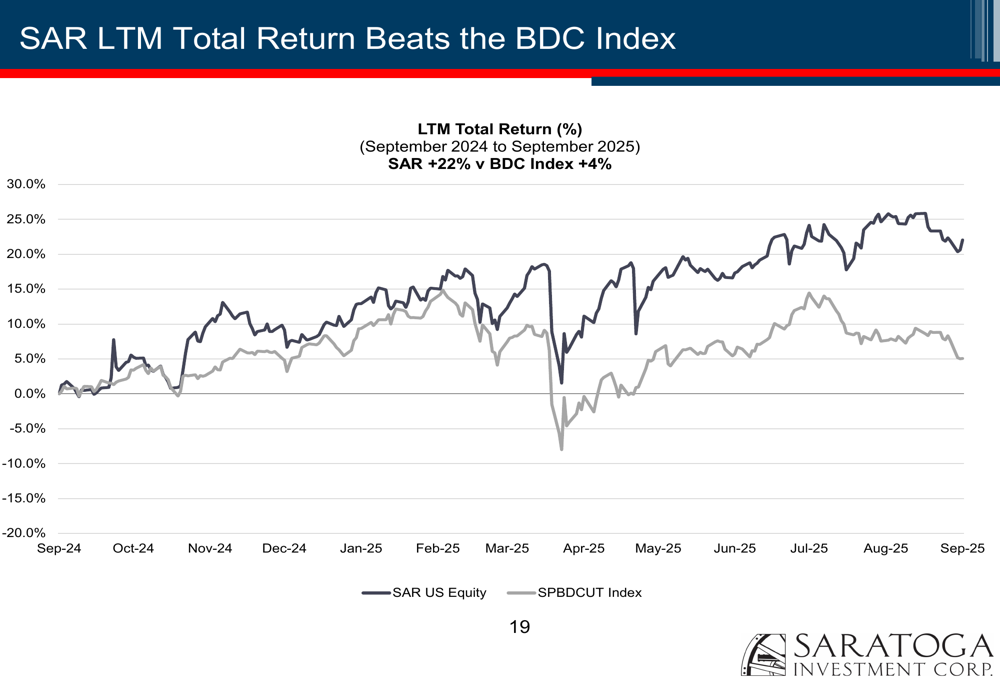

In terms of total returns, Saratoga has outperformed the BDC index by 22% on an LTM basis. The company’s long-term performance remains strong with total returns of 146% over five years, 38% over three years, and 22% over one year.

Forward Outlook & Challenges

While Saratoga’s presentation emphasized portfolio strength and long-term performance, the company faces several challenges highlighted in its recent earnings call. These include economic uncertainties, lower middle market deal volumes, and a disconnect between buyer and seller expectations in the current market environment.

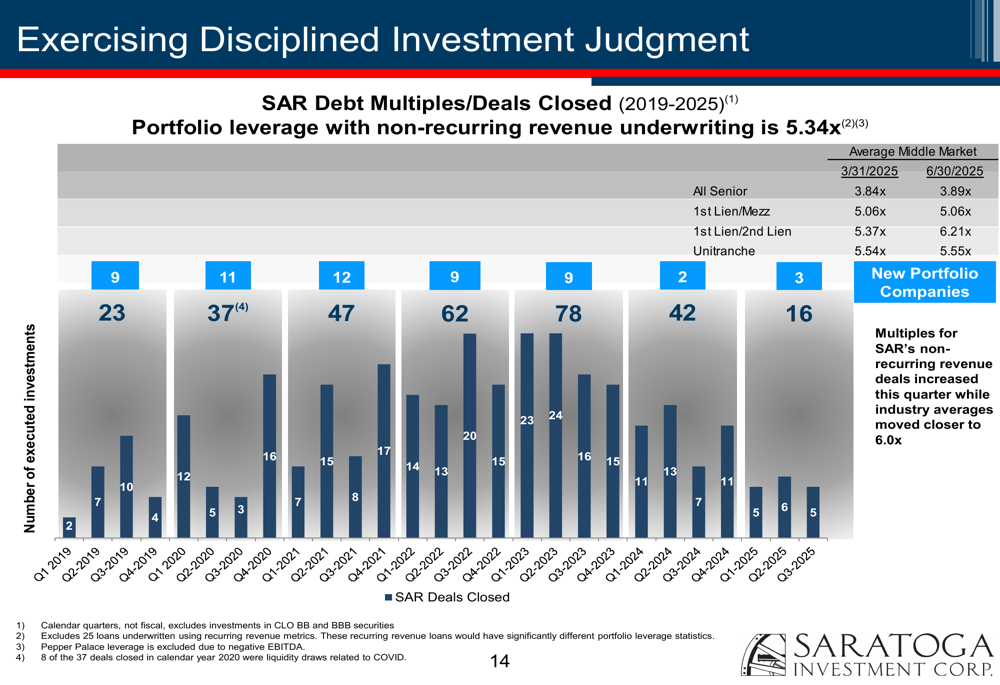

The company’s leverage strategy and underwriting approach remain focused on maintaining portfolio quality while pursuing growth opportunities. Saratoga’s portfolio leverage with non-recurring revenue underwriting stands at 5.34x, reflecting its disciplined approach to deal structuring:

CEO Christian Oberbeck previously stated that "Saratoga continues to be favorably situated for potential future economic opportunities as well as challenges," reflecting cautious optimism despite recent performance issues. The company’s objectives include expanding its asset base without sacrificing credit quality, a balance that will be crucial as Saratoga navigates current market headwinds.

The contrast between Saratoga’s strong long-term performance metrics and recent earnings challenges suggests that investors will be closely watching whether the company can maintain its portfolio quality while addressing the factors that led to its recent underperformance relative to expectations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.