Gold prices slid below $4,000/oz amid profit-taking on Gaza ceasefire

Introduction & Market Context

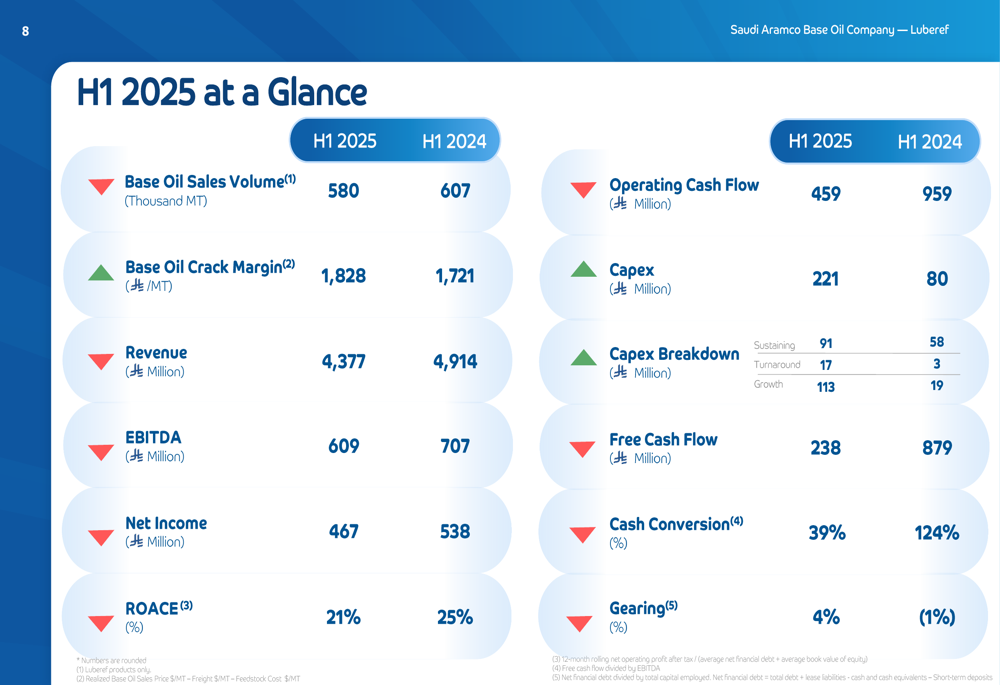

Saudi Aramco Base Oil Company JSC (TADAWUL:2223), also known as Luberef, presented its first half 2025 earnings results on August 4, 2025, revealing a 13% decline in net income despite improved crack margins. The company, which trades at SAR 93.40 per share, reported that lower base oil sales volumes were the primary driver behind the financial performance decline compared to the same period last year.

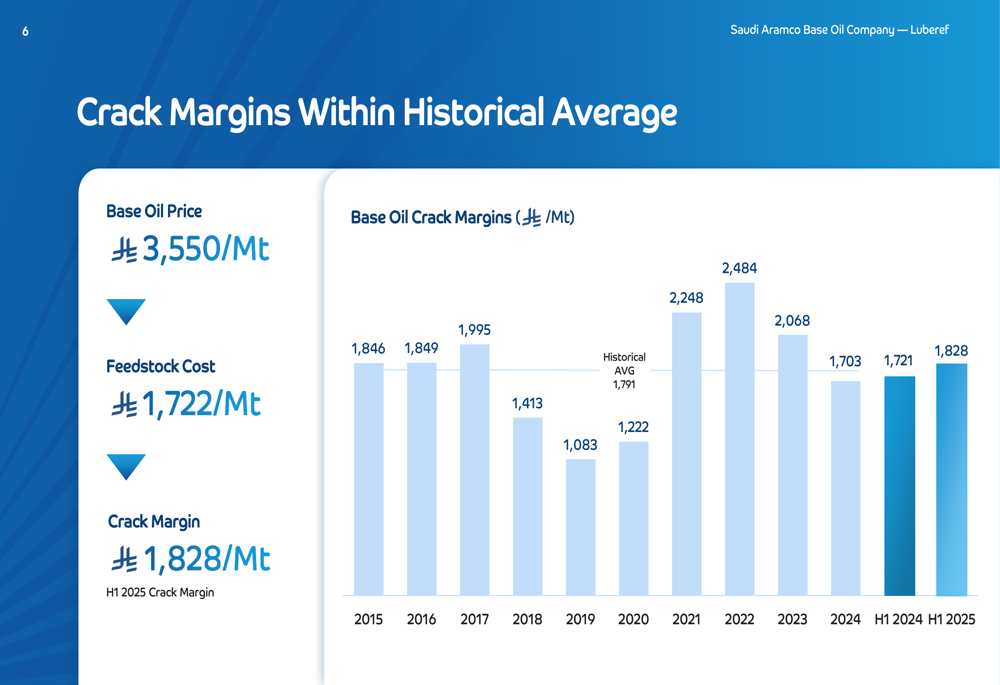

Luberef’s presentation highlighted that while base oil crack margins improved year-over-year to SAR 1,828/Mt (above the historical average of SAR 1,791/Mt), the company faced headwinds from reduced sales volumes and operational challenges, including an unplanned shutdown and scheduled turnaround.

Executive Summary

Luberef reported net income of SAR 467 million for H1 2025, down from SAR 538 million in H1 2024. Revenue declined to SAR 4,377 million from SAR 4,914 million in the prior-year period. The company maintained its dividend commitment, announcing a distribution of SAR 168 million for H1 2025 performance despite the earnings decline.

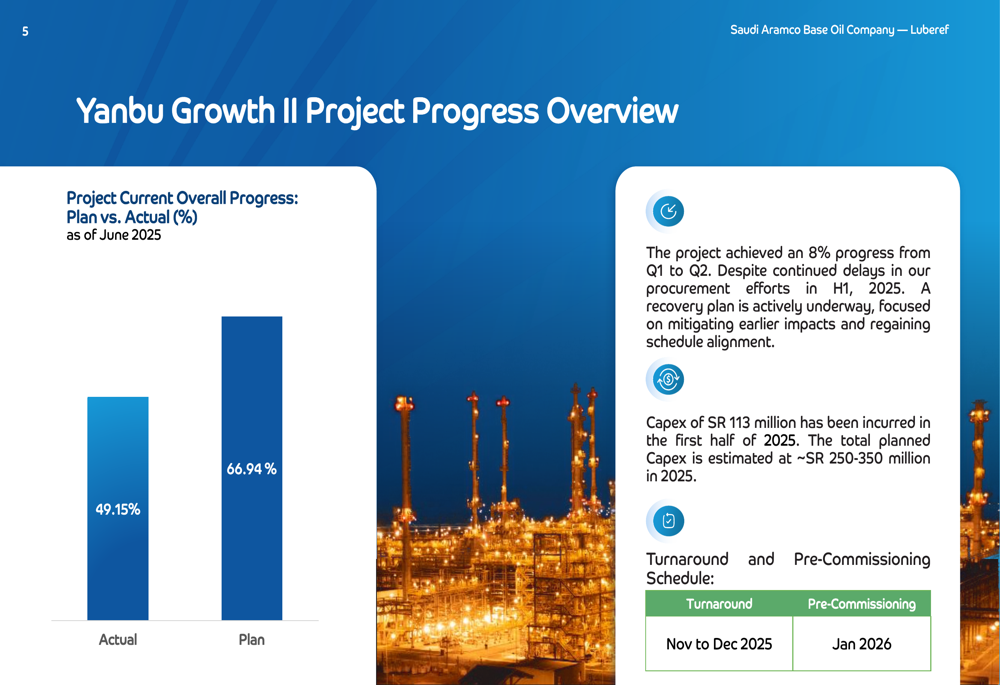

The company’s Yanbu Growth II project, a key strategic initiative, is behind schedule at 49.15% completion versus the planned 66.94%. Management indicated a recovery plan is underway, with total planned capital expenditure for this project estimated at SAR 250-350 million for 2025.

As shown in the following financial overview from the presentation:

Quarterly Performance Highlights

Luberef’s operational performance remained strong from a safety and reliability perspective, with a Total Recordable Incident Rate (TRIR) of 0.0 for more than five years and mechanical availability of 98.4%. However, base oil sales volume declined to 580 thousand metric tons in H1 2025 compared to 607 thousand metric tons in H1 2024.

The company’s EBITDA fell to SAR 609 million from SAR 707 million in H1 2024, while Return on Average Capital Employed (ROACE) decreased to 21% from 25%. Operating cash flow saw a significant decline to SAR 459 million from SAR 959 million in the prior-year period.

Capital expenditure increased substantially to SAR 221 million in H1 2025 from SAR 80 million in H1 2024, driven primarily by growth initiatives and turnaround activities. This higher capex, combined with lower operating cash flow, resulted in free cash flow of SAR 238 million, down from SAR 879 million in H1 2024.

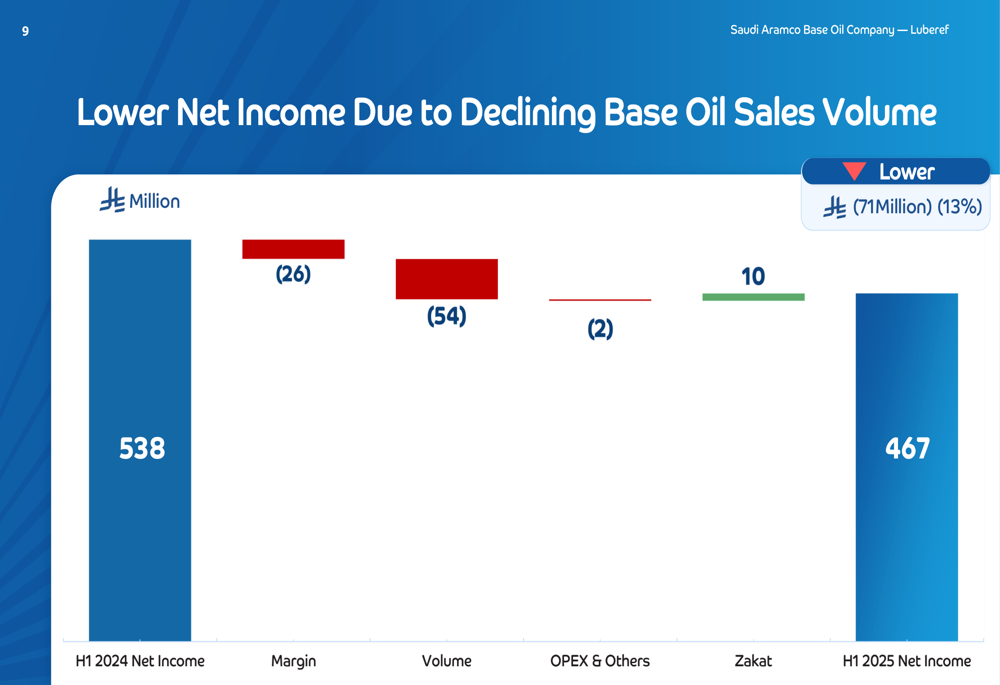

The following waterfall chart illustrates the factors contributing to the net income decline:

Detailed Financial Analysis

Luberef’s financial performance deterioration was primarily driven by volume declines, which negatively impacted net income by SAR 54 million. Margin decreases contributed an additional SAR 26 million to the earnings decline. These factors were slightly offset by a SAR 10 million positive impact from Zakat (Islamic tax).

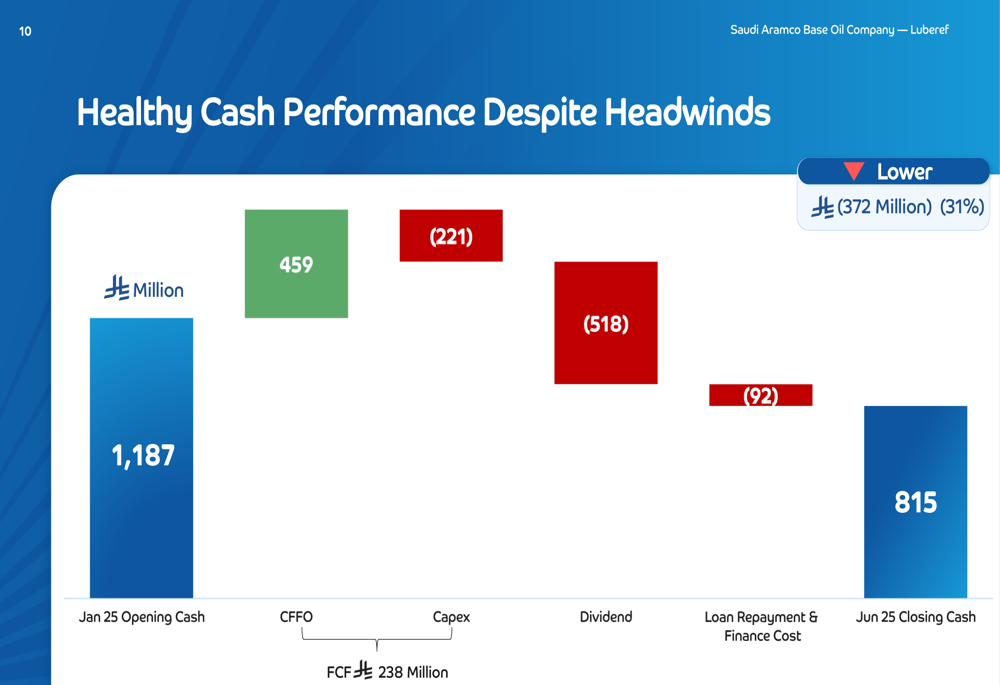

The company’s cash position remained relatively healthy despite the headwinds. Starting with SAR 1,187 million in January 2025, operating activities contributed SAR 459 million, while capital expenditures consumed SAR 221 million. Dividend payments of SAR 518 million and loan repayments plus finance costs of SAR 92 million resulted in a closing cash position of SAR 815 million in June 2025.

This cash flow performance is illustrated in the following chart:

The company’s base oil crack margins have remained relatively stable compared to historical averages. As shown in the following historical margin chart, H1 2025’s margin of SAR 1,828/Mt is slightly above the historical average of SAR 1,791/Mt:

Strategic Initiatives & Growth Projects

The Yanbu Growth II project remains a key strategic focus for Luberef despite falling behind schedule. The company reported 49.15% actual progress versus 66.94% planned progress as of June 2025. Management cited procurement delays as the primary reason for the schedule slippage but indicated a recovery plan is in place.

The project timeline shows turnaround activities scheduled for November to December 2025, with pre-commissioning expected in January 2026. The company has incurred SAR 113 million in capital expenditure for this project in H1 2025, with total planned capex estimated at SAR 250-350 million for the full year.

The following slide provides details on the Yanbu Growth II project progress:

Luberef’s long-term strategy includes unlocking future value from the Yanbu facility, with potential to produce 1.3 million metric tons of products from the Vacuum Distillation Unit and Hydrocracker Unit, and an additional 0.3 million metric tons from the Propane De Asphalting Unit and Furfural Unit. However, the company notes that realizing this potential depends on securing additional feedstock and completing the Growth II project.

Forward-Looking Statements

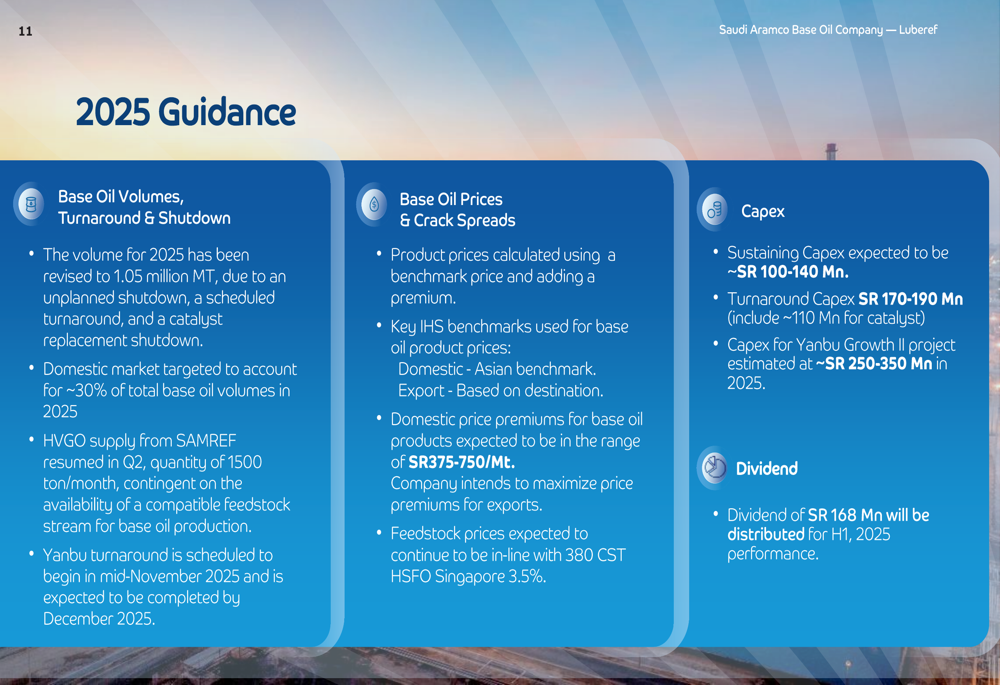

Luberef provided guidance for the full year 2025, revising its volume forecast to 1.05 million metric tons due to an unplanned shutdown, scheduled turnaround, and catalyst replacement. The company is targeting the domestic market to represent approximately 30% of sales.

Management indicated that HVGO supply from SAMREF has resumed at 1,500 tons per month, dependent on available feedstock. The Yanbu turnaround is scheduled for mid-November to end of December 2025.

Capital expenditure guidance for 2025 includes:

- Sustaining Capex: ~SAR 100-140 million

- Turnaround Capex: SAR 170-190 million (including SAR 110 million for catalyst)

- Growth Capex (Yanbu Growth II): ~SAR 250-350 million

The following guidance slide provides additional details on the company’s outlook:

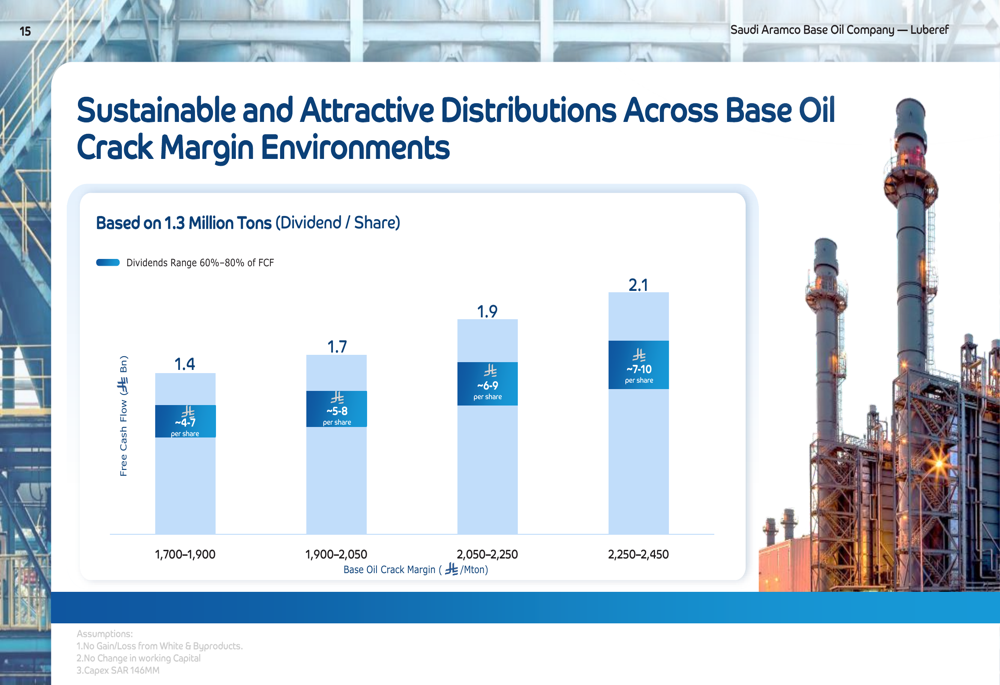

Looking further ahead, Luberef presented a model for sustainable distributions across various base oil crack margin environments, assuming 1.3 million tons of production. The company projects dividends ranging from 60%-80% of Free Cash Flow, with potential dividends per share ranging from SAR 4-7 at crack margins of 1,700-1,900 to SAR 7-10 at crack margins of 2,250-2,450.

Despite the current challenges, Luberef’s management remains focused on long-term growth initiatives while maintaining dividend distributions to shareholders. The company’s ability to navigate the current operational challenges while progressing on strategic projects will be crucial for its performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.