Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

SBC Medical Group Holdings Inc. (NASDAQ:SBC) presented its second quarter 2025 financial results on August 13, 2025, revealing significant challenges despite ongoing expansion efforts. The company’s stock reacted negatively in premarket trading, falling 7.49% to $4.20, following a 2.25% gain in the previous session.

The presentation comes as SBC continues to navigate a complex landscape in the aesthetic medicine market, balancing clinic expansion with business restructuring and fee structure revisions that have materially impacted financial performance.

Quarterly Performance Highlights

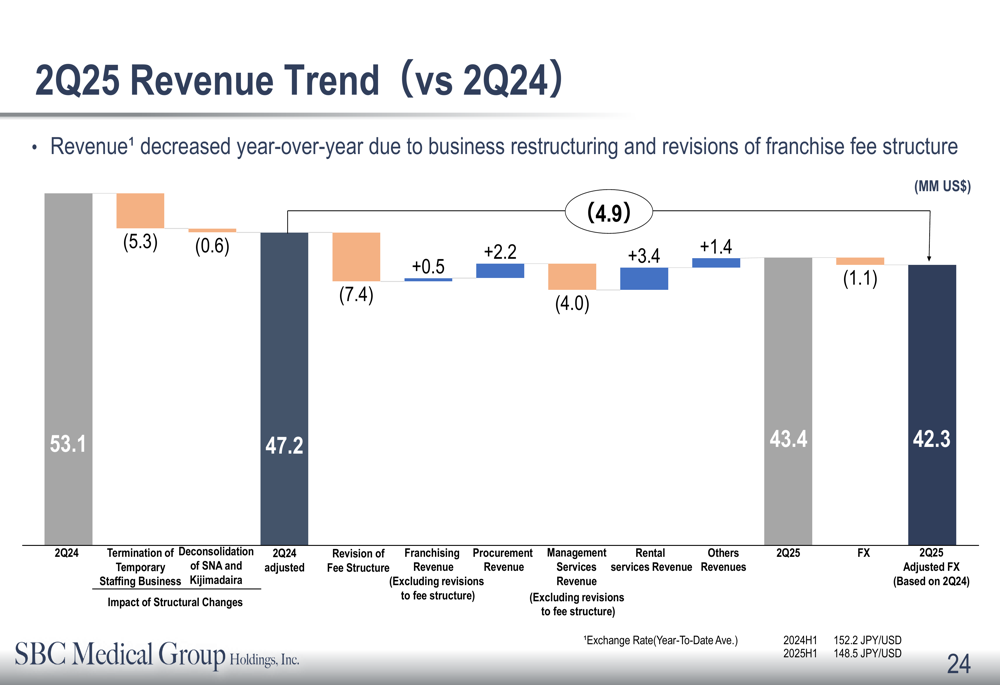

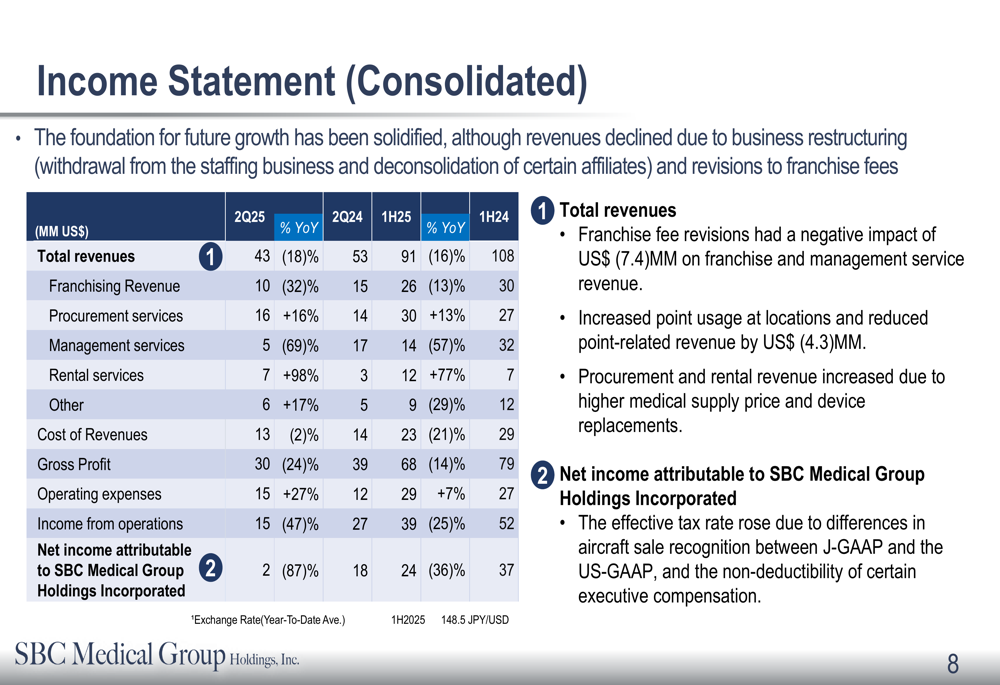

SBC reported a substantial decline in its second quarter 2025 financial results, with consolidated revenue falling 18% year-over-year to $43 million. More concerning was the 87% drop in net income attributable to SBC Medical Group Holdings, which plummeted to just $2 million.

The revenue decline was attributed to business restructuring and revisions to the franchise fee structure, as illustrated in the following breakdown:

Operating expenses increased 27% year-over-year, further pressuring profitability. Income from operations fell 47% compared to the same period last year, as shown in the consolidated income statement:

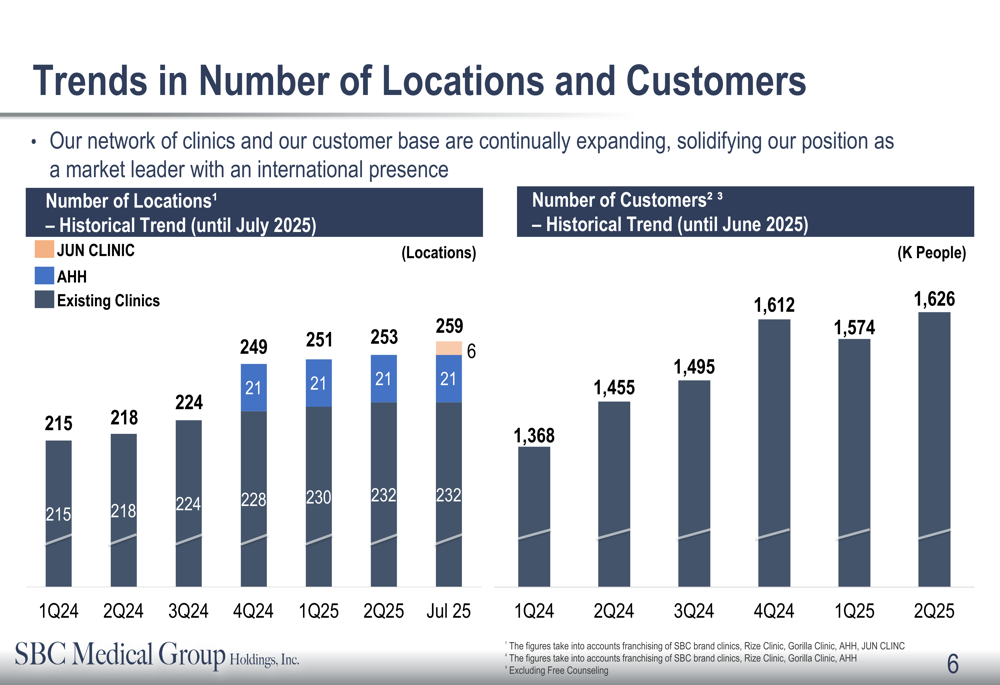

Despite these challenges, SBC continued to expand its franchise network, reaching 259 locations by July 2025, representing a 16% increase year-over-year. Customer numbers also grew to 6.31 million total visits (2.00 million unique customers), showing 14% and 10% growth respectively.

The following chart illustrates the company’s consistent location growth trajectory:

Strategic Initiatives

SBC is pursuing several strategic initiatives across different business segments to counter current headwinds. In aesthetic dermatology, the company is implementing a multi-brand strategy to capture a diversifying customer base, accelerating its shift from general surgery to specialized dermatology in response to changing market preferences.

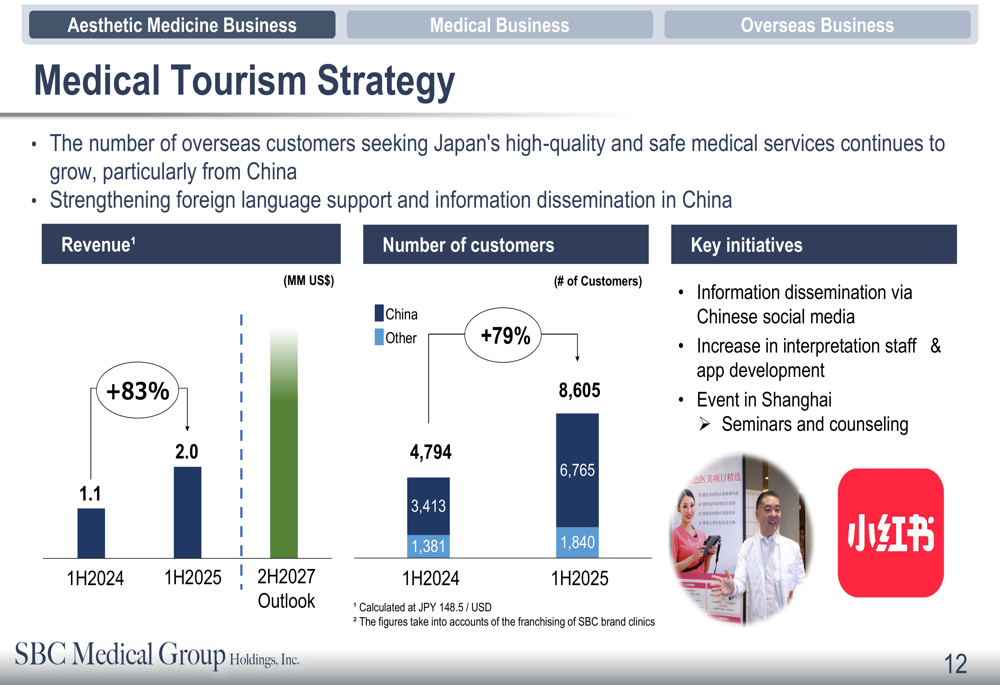

The company highlighted its expansion into medical tourism, particularly targeting Chinese customers, which has shown promising results with 83% revenue growth and 79% customer growth:

SBC is also expanding its medical business into orthopedics, fertility treatment/gynecology, and alopecia treatment, opening new clinics in Yokohama and Ikebukuro during the first half of 2025.

For its overseas business, SBC is strengthening its presence in the United States and Singapore, appointing key personnel including Dr. Steven R. Cohen as Advisor and hiring Stephen Rodgers to support U.S. operations.

Financial Position & Capital Strategy

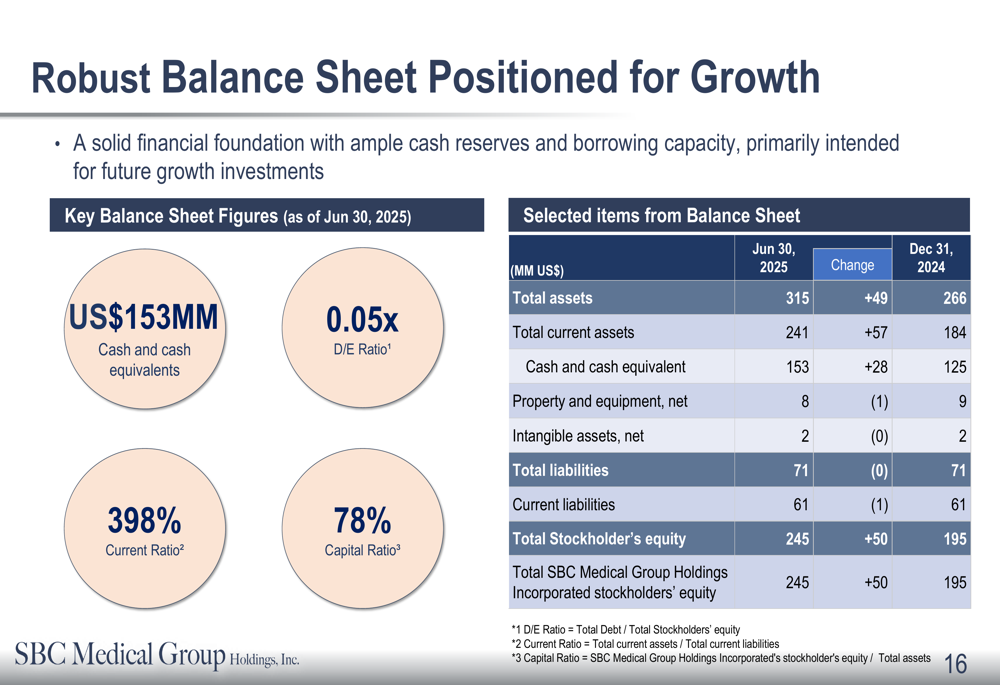

Despite operational challenges, SBC maintains a robust balance sheet with $153 million in cash and cash equivalents, a low debt-to-equity ratio of 0.05x, and a strong capital ratio of 78%. This financial strength provides a buffer as the company navigates its current challenges.

The following slide highlights key balance sheet metrics:

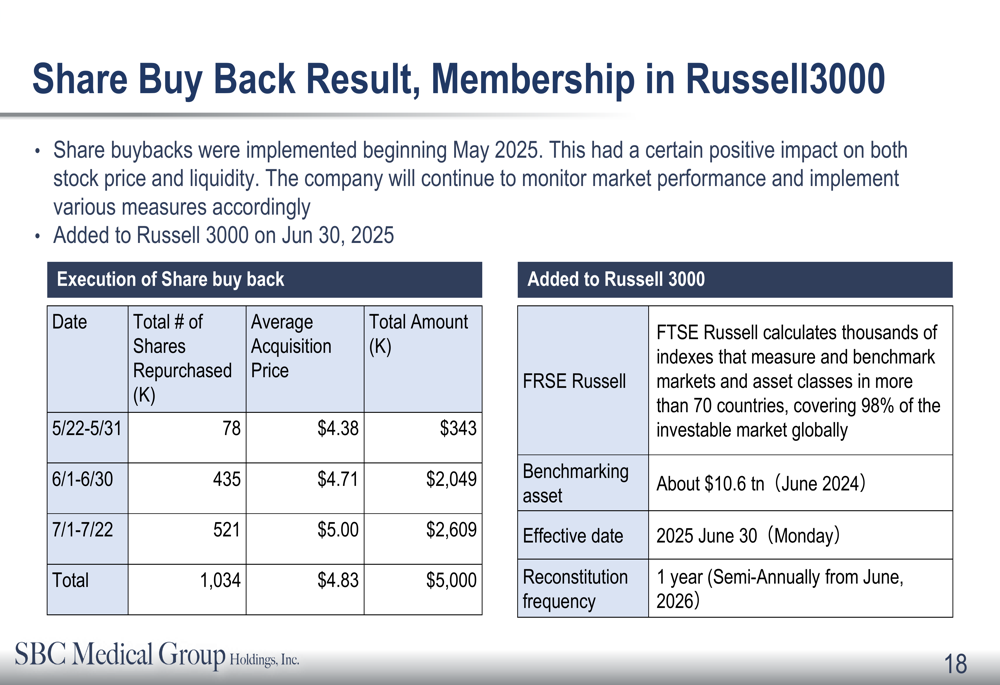

SBC completed a share buyback program, repurchasing 1,034,000 shares at an average price of $4.83. The company was also added to the Russell 3000 index on June 30, 2025, potentially improving its visibility among institutional investors.

However, the company acknowledged challenges with share liquidity, noting that low trading volume makes it difficult for many institutional investors to participate in the stock.

Forward-Looking Statements

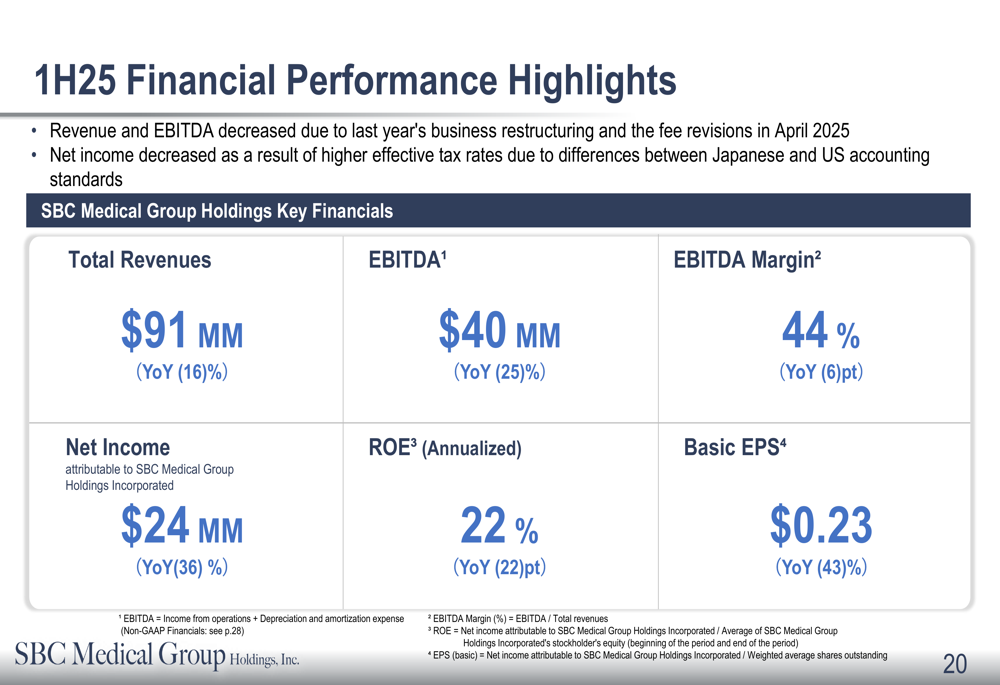

For the first half of 2025, SBC reported mixed results with total revenue of $91 million (up 16% year-over-year) but declining EBITDA of $40 million (down 25%) and net income of $24 million (down 36%).

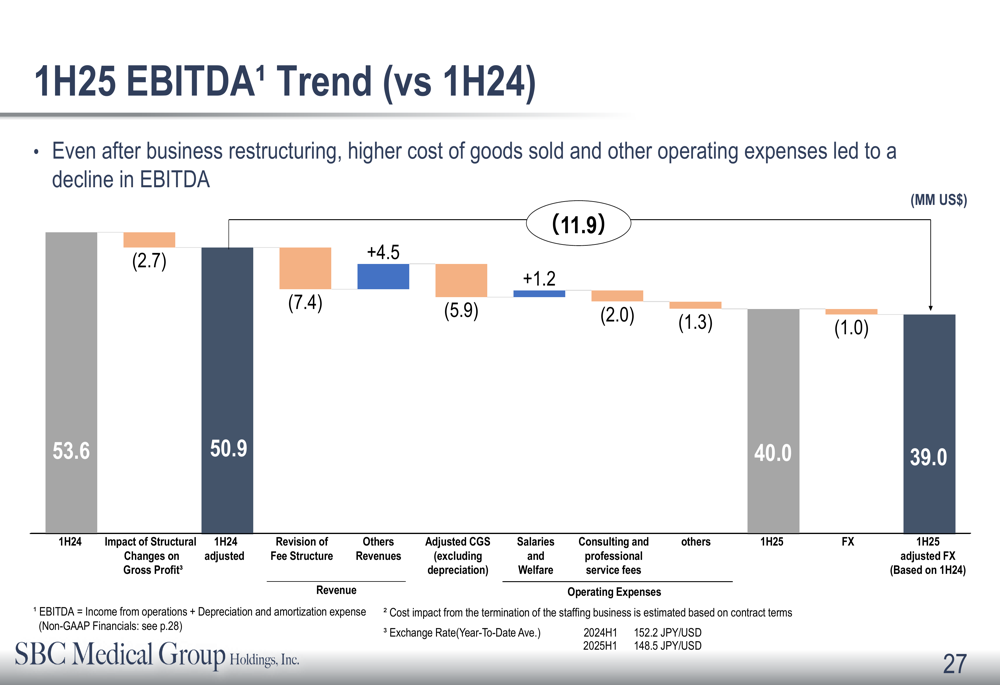

The EBITDA decline was primarily attributed to increased cost of goods sold and other operating expenses, as shown in this analysis:

Looking ahead, SBC appears focused on improving operational efficiency while continuing its expansion strategy. The company’s strong balance sheet provides financial flexibility to weather current challenges while pursuing growth opportunities across its various business segments.

However, investors should note the significant deterioration in profitability metrics and consider whether the company’s strategic initiatives will be sufficient to reverse these trends in upcoming quarters. The premarket stock decline suggests the market remains skeptical about SBC’s near-term prospects despite its long-term strategic vision.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.