Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

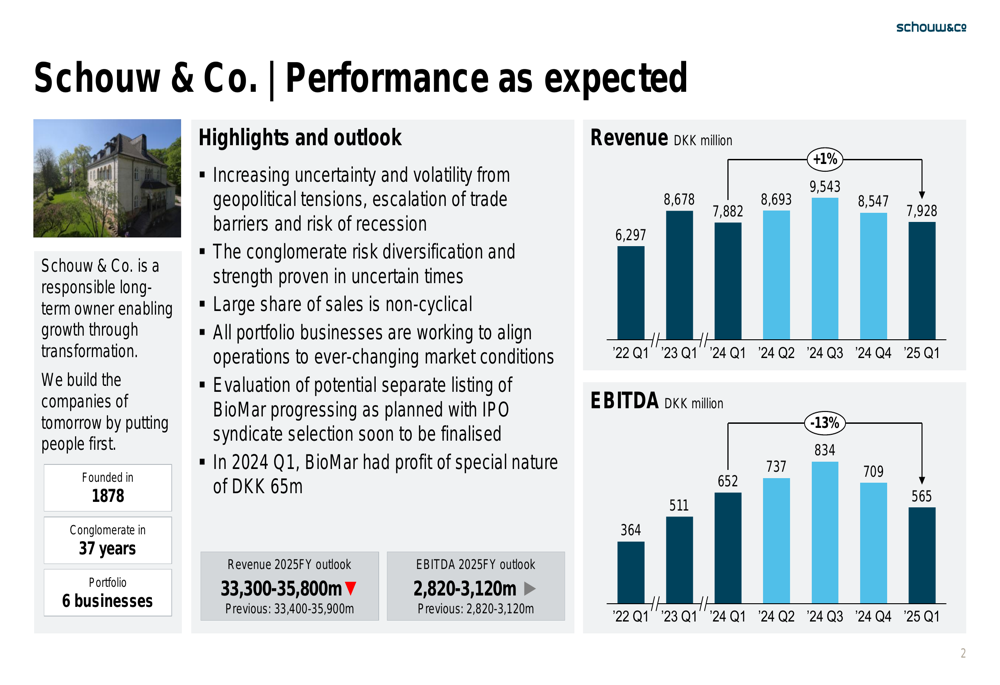

Schouw & Co. reported its Q1 2025 results on May 2, showing stable revenue but declining profitability across most of its business portfolio. The Danish industrial conglomerate posted revenue of 7.9 billion DKK, up 1% year-over-year, while EBITDA fell 13% to 565 million DKK. Despite the earnings decline, the company maintained its full-year guidance, describing the quarter as delivering "stable performance in a volatile environment."

Investors appeared less convinced by this characterization, with Schouw & Co. (CPH:SCHO) shares falling 4.3% following the earnings release, closing at 578 DKK.

Quarterly Performance Highlights

Schouw & Co.’s Q1 performance revealed significant variations across its business units, with some segments showing resilience while others faced considerable headwinds. The company emphasized its strength in uncertain times, highlighting a large share of non-cyclical sales and ongoing efforts to align operations with changing market conditions.

Revenue for the quarter reached 7,928 million DKK, representing a modest 1% increase compared to Q1 2024. However, EBITDA declined 13% to 565 million DKK, reflecting margin pressure across several business units.

Business Unit Analysis

BioMar: Volume Growth Offset by Margin Pressure

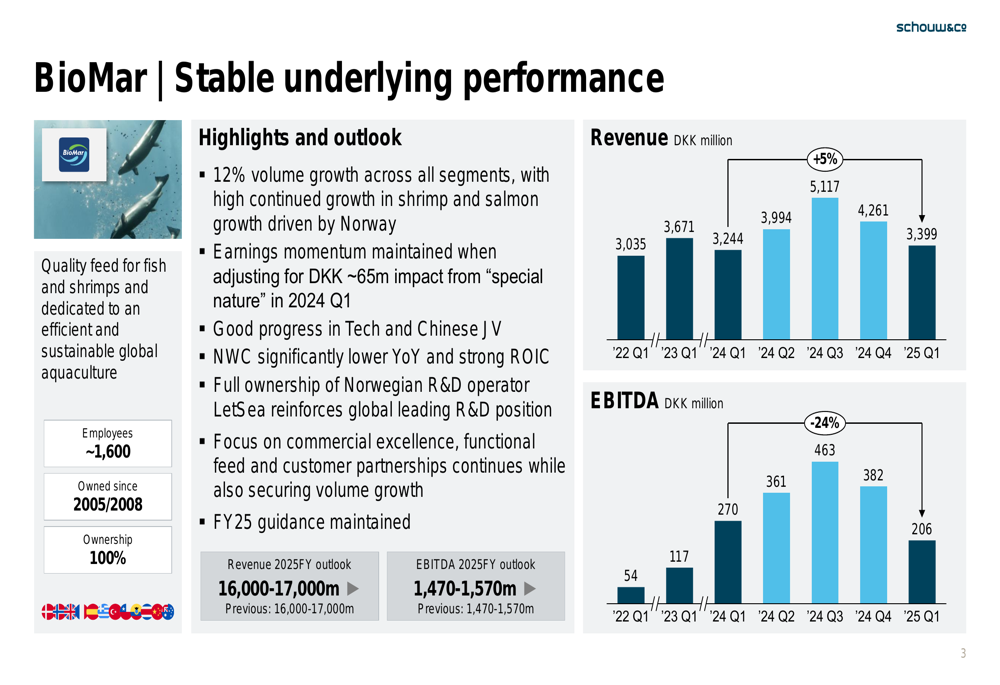

BioMar, Schouw’s fish feed division and largest business unit, delivered 12% volume growth across all segments, with revenue increasing 5% to 3,399 million DKK. Despite this growth, EBITDA fell 24% to 206 million DKK compared to Q1 2024.

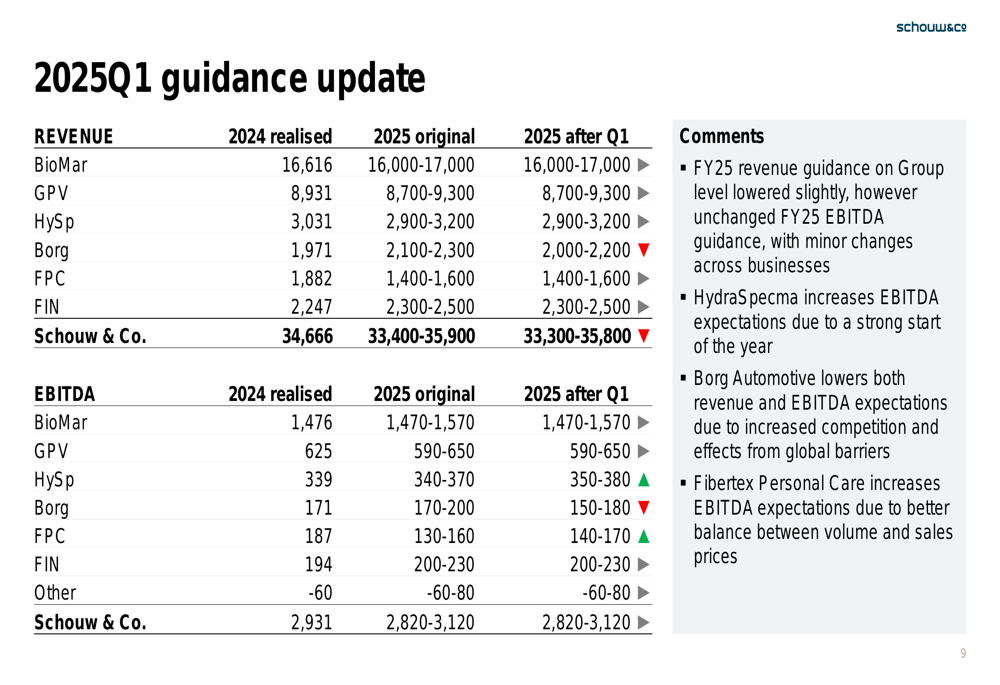

The company highlighted progress in its technology initiatives and Chinese joint venture, while maintaining its full-year guidance for BioMar with revenue of 16,000-17,000 million DKK and EBITDA of 1,470-1,570 million DKK. Notably, Schouw mentioned the potential for a separate listing of BioMar, though no specific timeline was provided.

GPV: Navigating Soft Electronics Demand

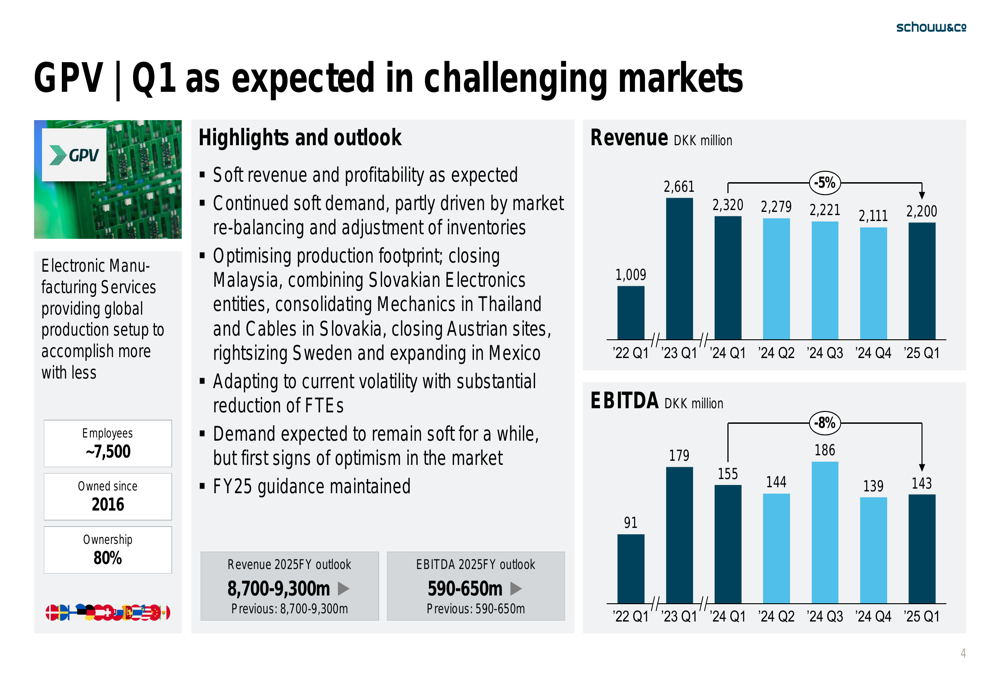

GPV, the electronics manufacturing services division, reported results "as expected in challenging markets" with revenue declining 5% to 2,200 million DKK and EBITDA falling 8% to 143 million DKK. The company cited continued soft demand and is focusing on optimizing its production footprint to adapt to current market volatility.

The presentation noted that demand is expected to remain soft, though GPV maintained its full-year guidance with revenue of 8,700-9,300 million DKK and EBITDA of 590-650 million DKK. The earnings call transcript revealed additional context, mentioning one-off costs of 40 million DKK anticipated in June 2025 related to GPV’s ERP system implementation.

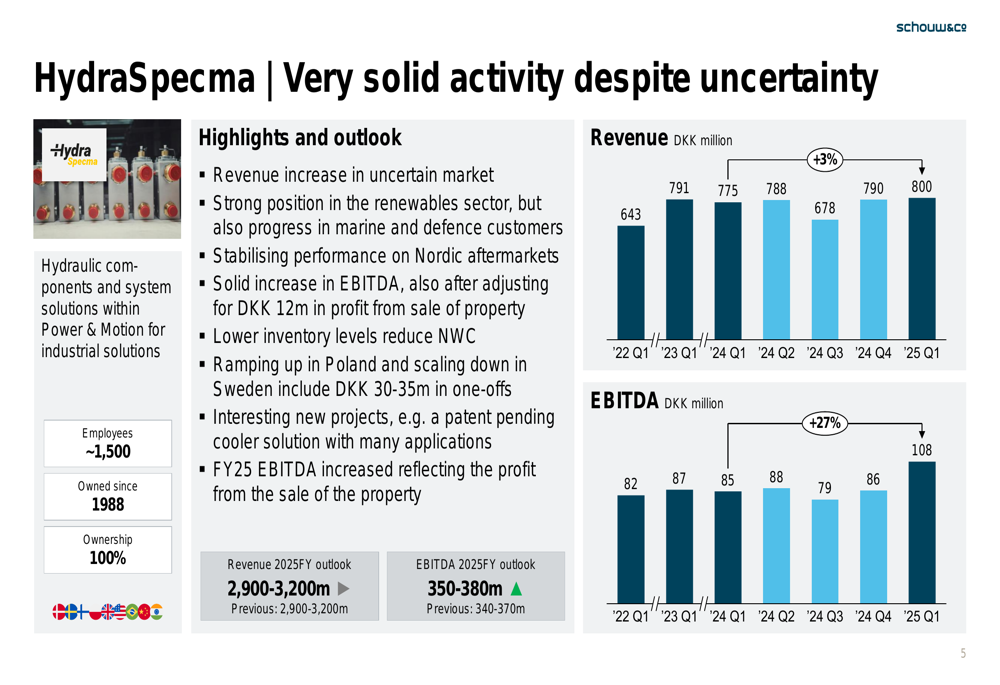

HydraSpecma: The Portfolio’s Bright Spot

HydraSpecma emerged as the standout performer in Schouw’s portfolio, delivering "very solid activity despite uncertainty." The hydraulic solutions provider increased revenue by 3% to 800 million DKK while achieving impressive EBITDA growth of 27% to 108 million DKK.

The company cited a strong position in renewables, stabilizing Nordic aftermarkets, and lower inventory levels as key factors in its performance. Following this strong quarter, Schouw raised HydraSpecma’s full-year EBITDA guidance to 350-380 million DKK, up from the previous 340-370 million DKK.

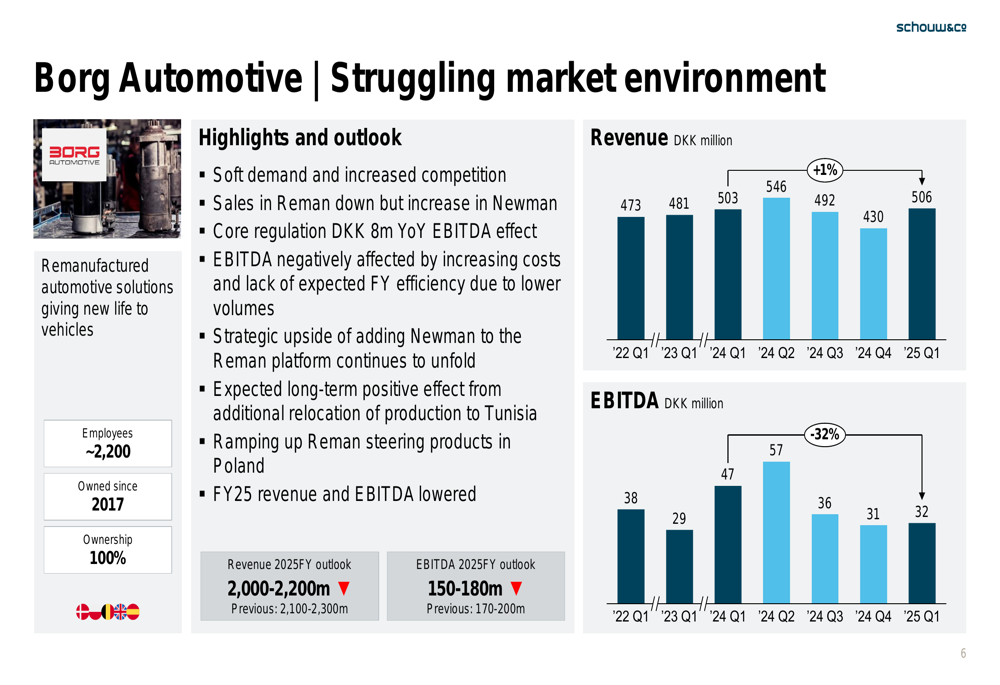

Borg Automotive: Facing Significant Headwinds

Borg Automotive experienced the most challenging quarter among Schouw’s businesses, described as operating in a "struggling market environment." While revenue increased marginally by 1% to 506 million DKK, EBITDA plummeted 32% to 32 million DKK.

The company cited soft demand, declining sales in its remanufacturing segment, and regulatory effects as factors behind the disappointing performance. In response, Schouw lowered Borg’s full-year revenue guidance to 2,000-2,200 million DKK (from 2,100-2,300 million DKK) and reduced EBITDA expectations to 150-180 million DKK (from 170-200 million DKK).

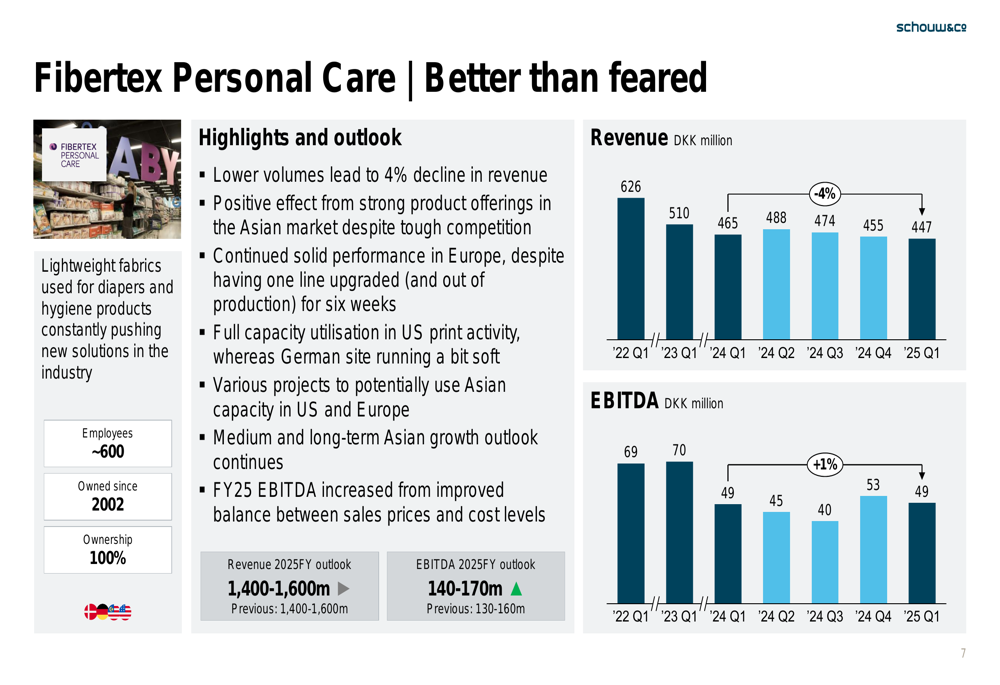

Fibertex Personal Care: Exceeding Low Expectations

Fibertex Personal Care performed "better than feared" despite a 4% revenue decline to 447 million DKK. EBITDA remained stable with a 1% increase to 49 million DKK, as the company benefited from strong product offerings in Asia and solid performance in Europe.

The presentation highlighted full capacity utilization in the US and projects to leverage Asian capacity for US markets. Based on this performance, Schouw increased Fibertex Personal Care’s full-year EBITDA guidance to 140-170 million DKK, up from the previous 130-160 million DKK.

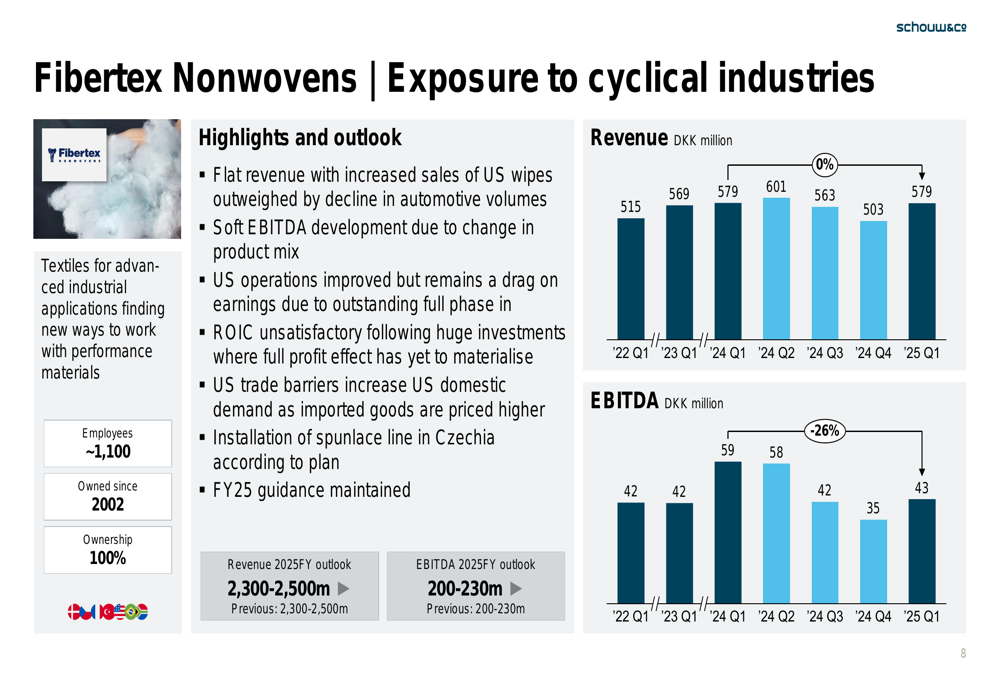

Fibertex Nonwovens: Cyclical Exposure Weighs on Results

Fibertex Nonwovens maintained flat revenue at 579 million DKK but saw EBITDA decline 26% to 43 million DKK, reflecting its "exposure to cyclical industries." The company reported improved US operations but cited unsatisfactory return on invested capital and US trade barriers as ongoing challenges.

Despite these headwinds, Schouw maintained Fibertex Nonwovens’ full-year guidance with revenue of 2,300-2,500 million DKK and EBITDA of 200-230 million DKK, noting the installation of a new spunlace production line in Czechia as a strategic investment.

Strategic Initiatives and Outlook

Schouw & Co. maintained its overall full-year guidance despite the Q1 EBITDA decline, projecting group revenue of 33,300-35,800 million DKK and EBITDA of 2,820-3,120 million DKK. This confidence suggests management expects improved performance in subsequent quarters.

The potential separate listing of BioMar represents a significant strategic development that could reshape Schouw’s portfolio. Additionally, the company highlighted several strategic initiatives across its businesses, including BioMar’s acquisition of full ownership of LetSea (a Norwegian R&D facility), HydraSpecma’s expansion in Poland, and Fibertex Nonwovens’ investment in new production capacity.

During the earnings call, executives emphasized strong customer relationships and innovation as key strengths, stating: "We are seeing very strong positions and long relations with our key customers globally." However, they also acknowledged the volatile business environment affecting the automotive and electronics sectors, with soft demand expected to persist through the first half of 2025.

The maintenance of full-year guidance despite Q1 underperformance and a 4.3% stock price decline suggests investors remain cautious about Schouw’s ability to overcome current market challenges and deliver on its financial targets for 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.