Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Schrödinger Inc. (NASDAQ:SDGR) presented its second quarter 2025 financial results on August 6, 2025, highlighting continued revenue growth across its software and drug discovery segments. The computational chemistry company reported total revenue of $54.8 million, representing a 16% year-over-year increase, while maintaining its full-year guidance.

The company’s stock closed at $19.64 on August 6, down 1.58% for the day, with aftermarket trading showing a further decline of 0.71%. This performance comes amid a challenging period for the stock, which has fallen significantly from its post-Q1 earnings level of $24.50 earlier this year.

Quarterly Performance Highlights

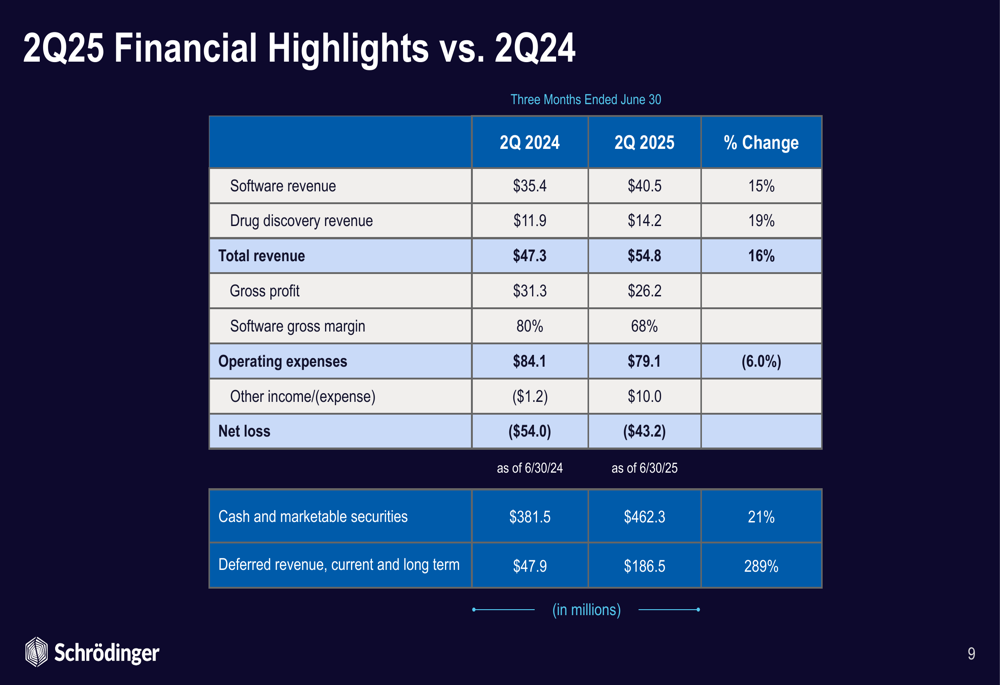

Schrödinger reported software revenue of $40.5 million for Q2 2025, a 15% increase compared to the same period last year. Drug discovery revenue reached $14.2 million, growing 19% year-over-year. The company’s total revenue of $54.8 million represents a 16% increase from Q2 2024, though this marks a slowdown from the 63% growth reported in Q1 2025.

As shown in the following quarterly financial comparison:

The company improved its net loss position to $43.2 million from $54.0 million in the prior year period, while reducing operating expenses by 6% to $79.1 million. Gross profit increased to $31.3 million, though software gross margin declined to 68% from 80% in Q2 2024.

Schrödinger’s cash position remains strong with $462.3 million in cash and marketable securities, a 21% increase from Q2 2024, though down from the $512 million reported at the end of Q1 2025. Notably, deferred revenue increased substantially to $186.5 million, a 289% jump from the prior year, suggesting strong future revenue recognition potential.

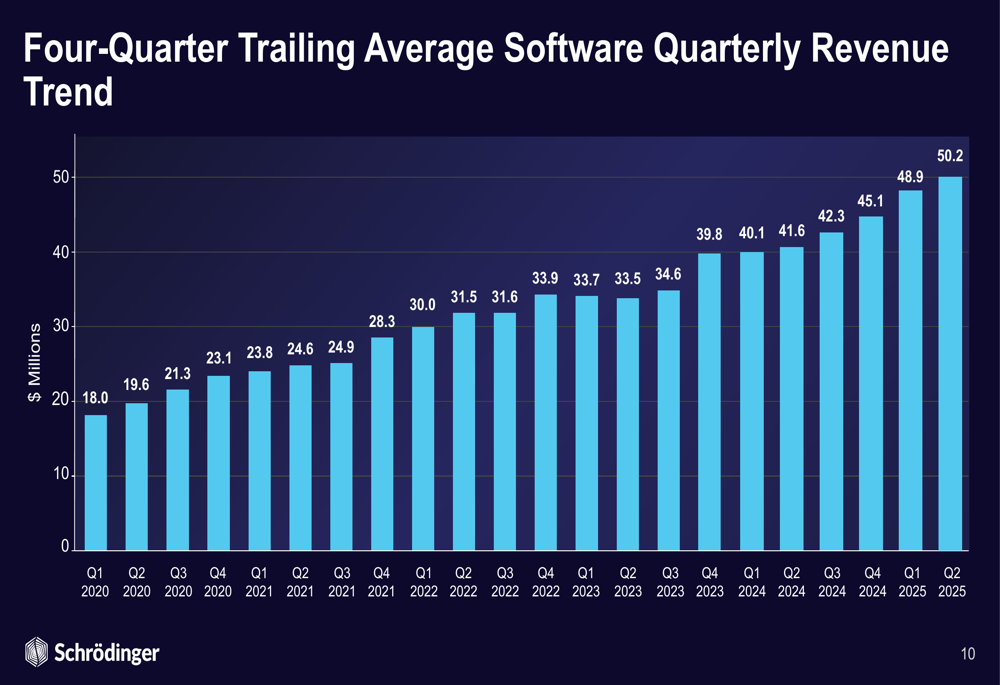

The company’s four-quarter trailing average software revenue continues to show consistent growth:

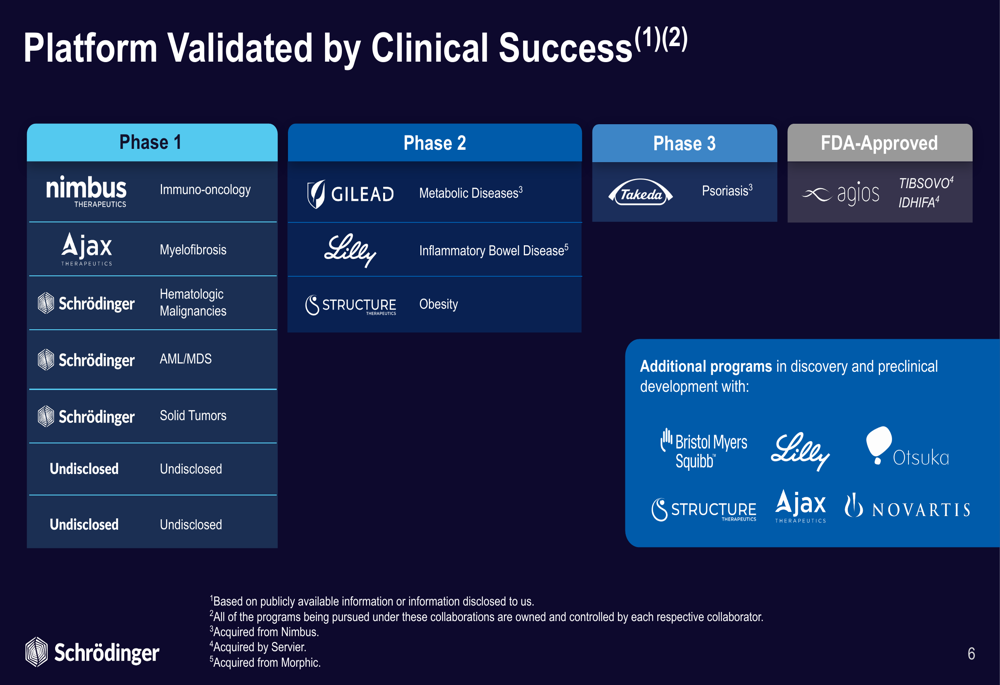

Platform Validation and Pipeline Progress

Schrödinger emphasized the clinical validation of its computational platform through multiple collaborations with major pharmaceutical companies. The company’s technology has contributed to programs across various development stages, including FDA-approved products.

The following slide illustrates the breadth of clinical programs enabled by Schrödinger’s platform:

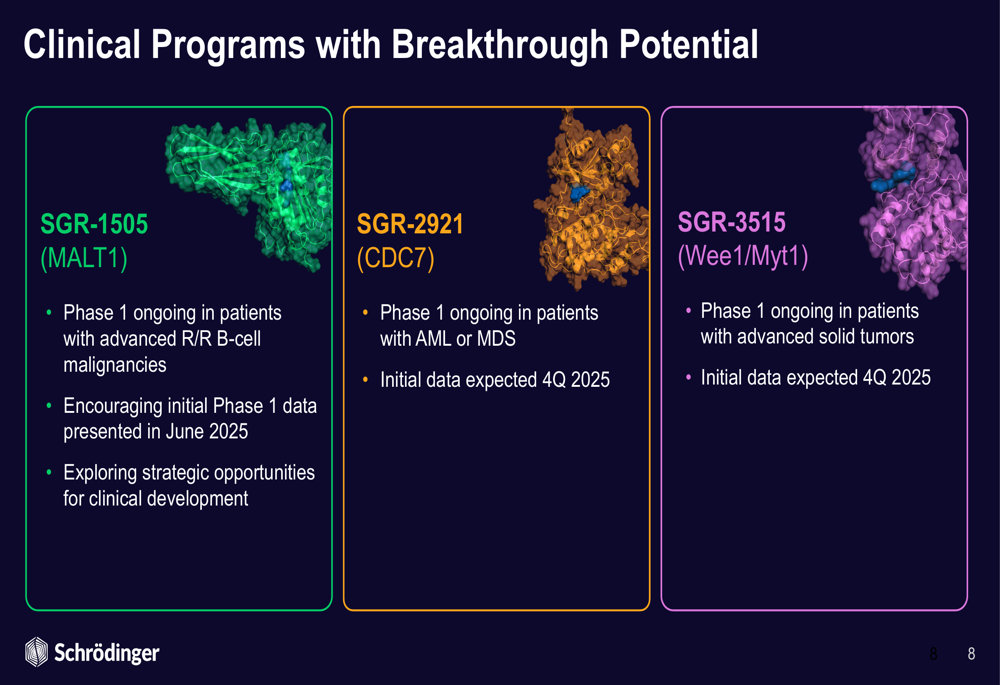

In its proprietary pipeline, Schrödinger highlighted three key clinical programs:

1. SGR-1505 (MALT1 inhibitor): Phase 1 ongoing in advanced R/R B-cell malignancies with encouraging initial data presented in June 2025. The company is exploring strategic opportunities for clinical development.

2. SGR-2921 (CDC7 inhibitor): Phase 1 ongoing in patients with AML or MDS with initial data expected in Q4 2025.

3. SGR-3515 (Wee1/Myt1 inhibitor): Phase 1 ongoing in patients with advanced solid tumors with initial data expected in Q4 2025.

These programs demonstrate the company’s breakthrough potential in oncology:

Strategic Initiatives and Technology Advancements

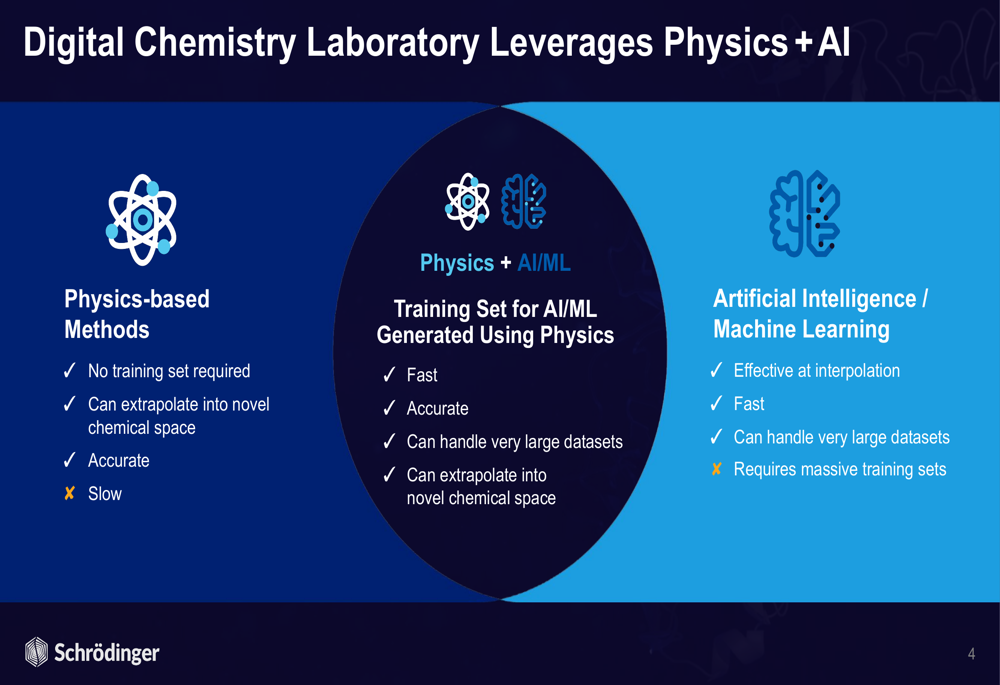

Schrödinger continues to differentiate itself through its unique approach of combining physics-based methods with artificial intelligence and machine learning. This hybrid approach allows the company to maintain advantages in accuracy while improving speed and scalability.

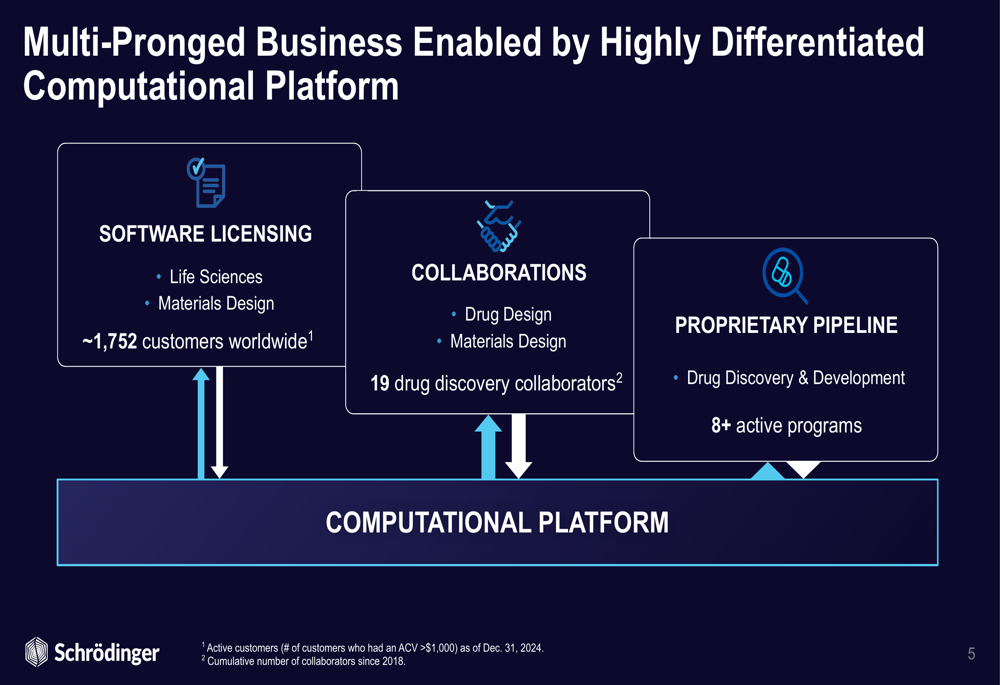

The company’s computational platform serves as the foundation for its multi-pronged business model:

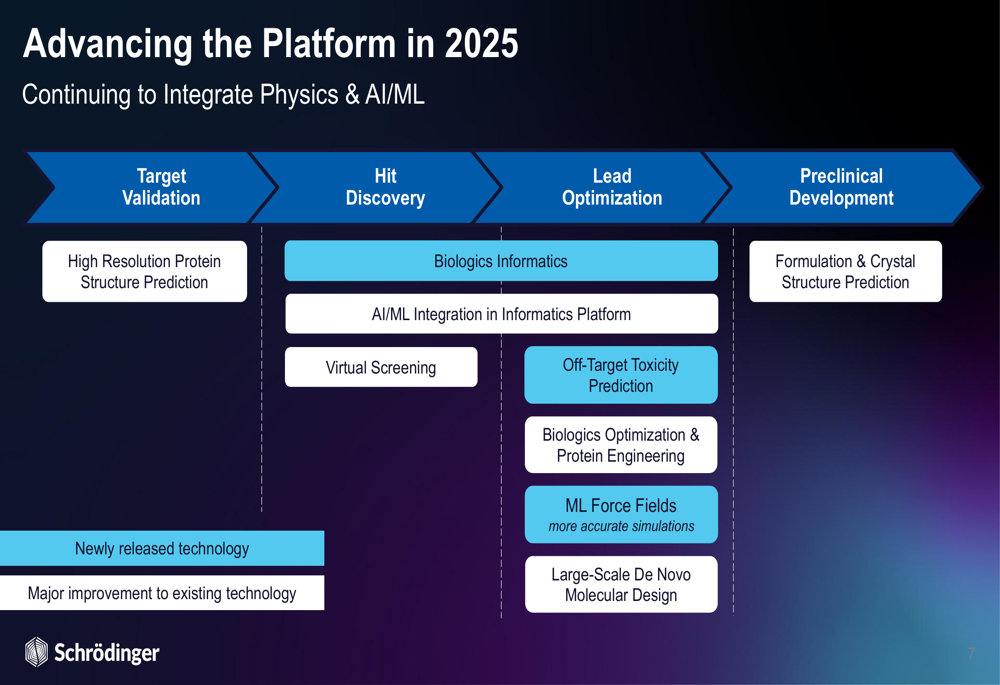

Schrödinger is advancing its platform in 2025 with several technological improvements, including high-resolution protein structure prediction, biologics informatics, AI/ML integration, and large-scale de novo molecular design:

The company’s approach to integrating physics with AI/ML provides distinct advantages over purely AI-driven or purely physics-based methods:

Financial Outlook and Guidance

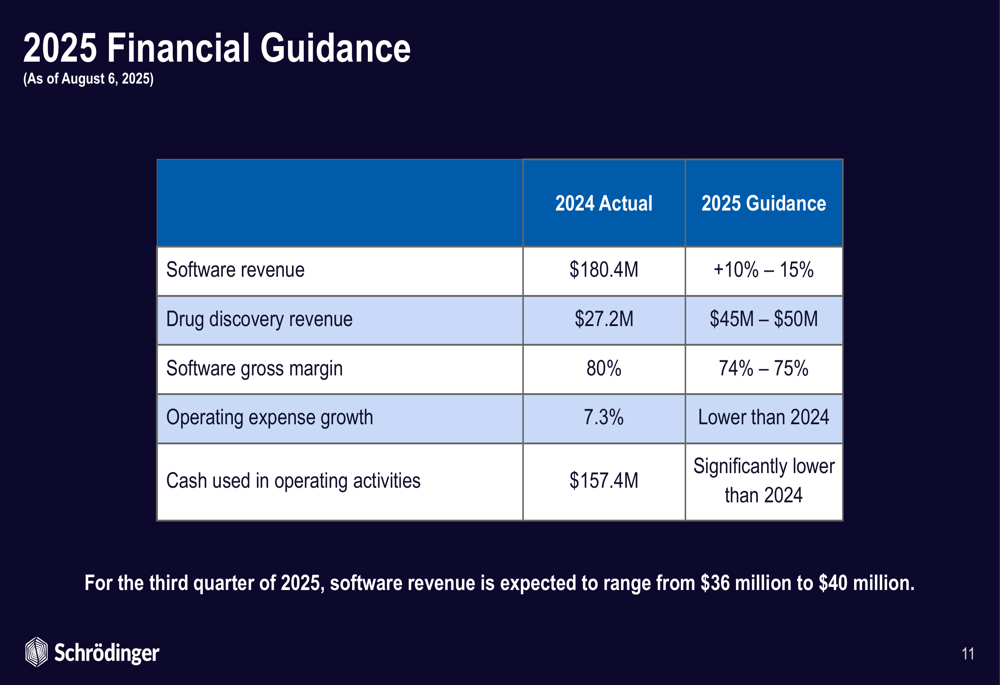

Schrödinger maintained its full-year 2025 financial guidance, projecting software revenue growth of 10-15% compared to 2024’s $180.4 million, and drug discovery revenue of $45-50 million. The company expects software gross margin to be 74-75%, down from 80% in 2024, while operating expense growth is projected to be lower than the 7.3% seen in 2024.

For the third quarter of 2025, Schrödinger expects software revenue to range from $36 million to $40 million.

The detailed financial guidance is presented below:

The company outlined several strategic priorities for the remainder of 2025, including increasing customer adoption of its computational platform, delivering planned platform enhancements, presenting initial Phase 1 clinical data for SGR-2921 and SGR-3515 in Q4 2025, and advancing its proprietary and collaborative discovery portfolio.

While Schrödinger continues to show revenue growth and platform advancement, investors will be closely watching the upcoming clinical data readouts in Q4 2025, which could significantly impact the company’s valuation and strategic direction. The substantial increase in deferred revenue suggests strong future revenue potential, but the sequential decline in software revenue from Q1 to Q2 and the year-over-year decrease in software gross margin may raise questions about scalability and profitability in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.