NVIDIA expands Microsoft partnership with Blackwell GPUs for AI infrastructure

Introduction & Market Context

SCOR SE (EPA:SCR) released its third quarter 2025 results on October 31, 2025, reporting strong financial performance across all business segments despite an increasingly competitive reinsurance market. The global reinsurer maintained its disciplined underwriting approach while delivering substantial profitability improvements compared to the same period last year.

The company's stock has performed exceptionally well over the past year, delivering a 38.12% return, with a particularly impressive six-month gain of 51.66%. SCOR's shares closed at €27.82, near its 52-week high of €28.18, reflecting investor confidence in the company's strategic direction and financial results.

Quarterly Performance Highlights

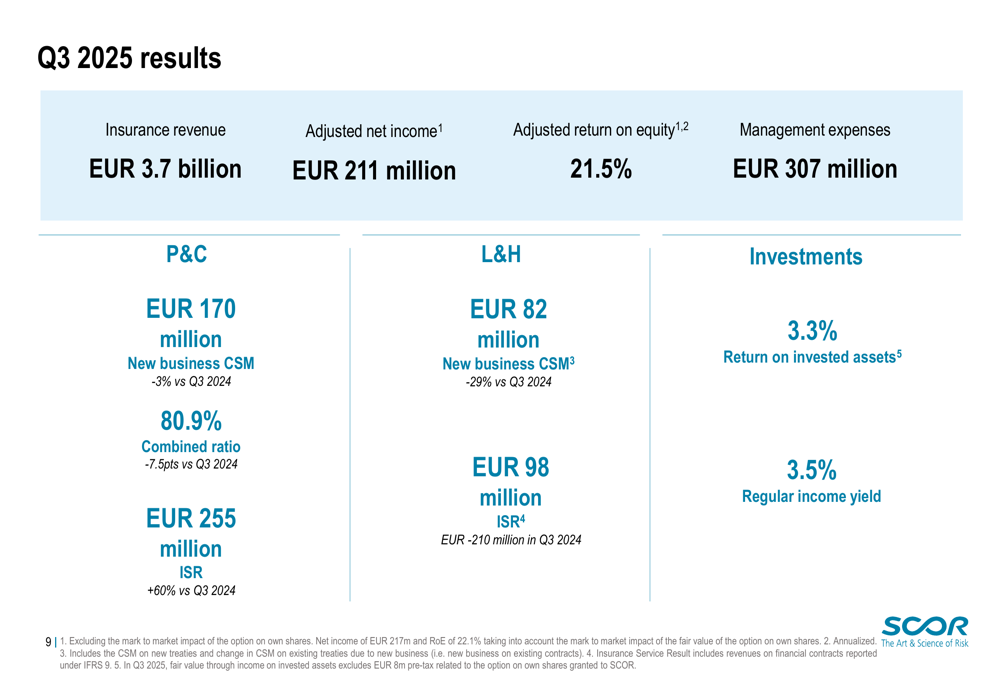

SCOR reported an adjusted net income of €211 million for Q3 2025, translating to an adjusted return on equity of 21.5%. This strong performance contributed to a nine-month adjusted net income of €631 million and a nine-month adjusted return on equity of 19.5%.

As shown in the following comprehensive overview of Q3 2025 results:

The company generated €3.7 billion in insurance revenue during the quarter while maintaining management expenses at €307 million. SCOR's diversified business model continues to demonstrate resilience, with strong contributions from both its Property & Casualty (P&C) and Life & Health (L&H) segments.

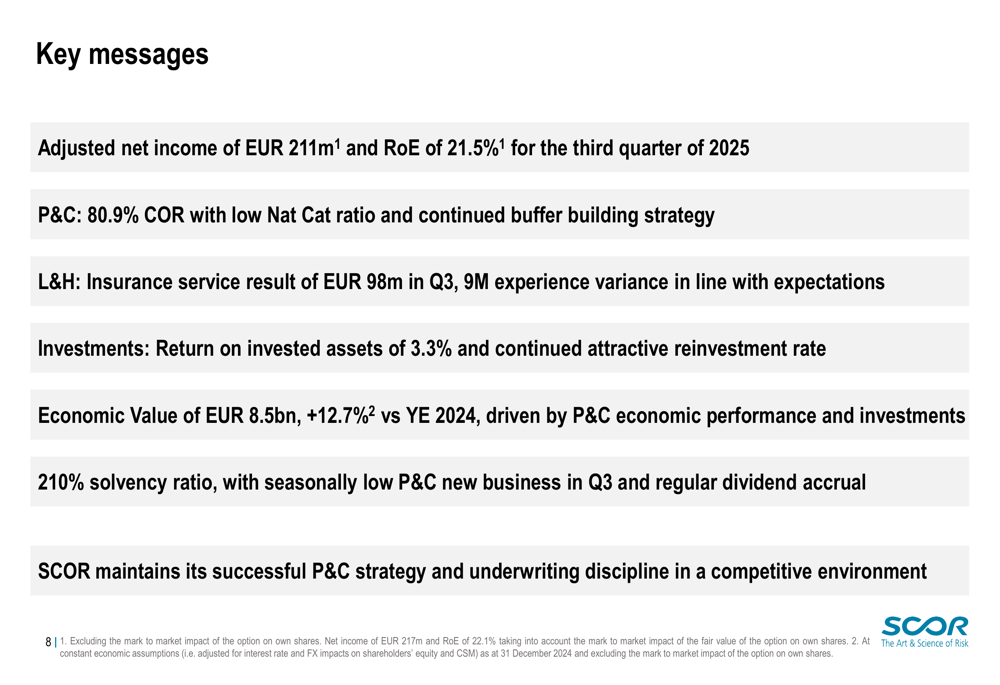

The key messages from SCOR's Q3 presentation highlight the company's strategic focus and achievements:

P&C Business Performance

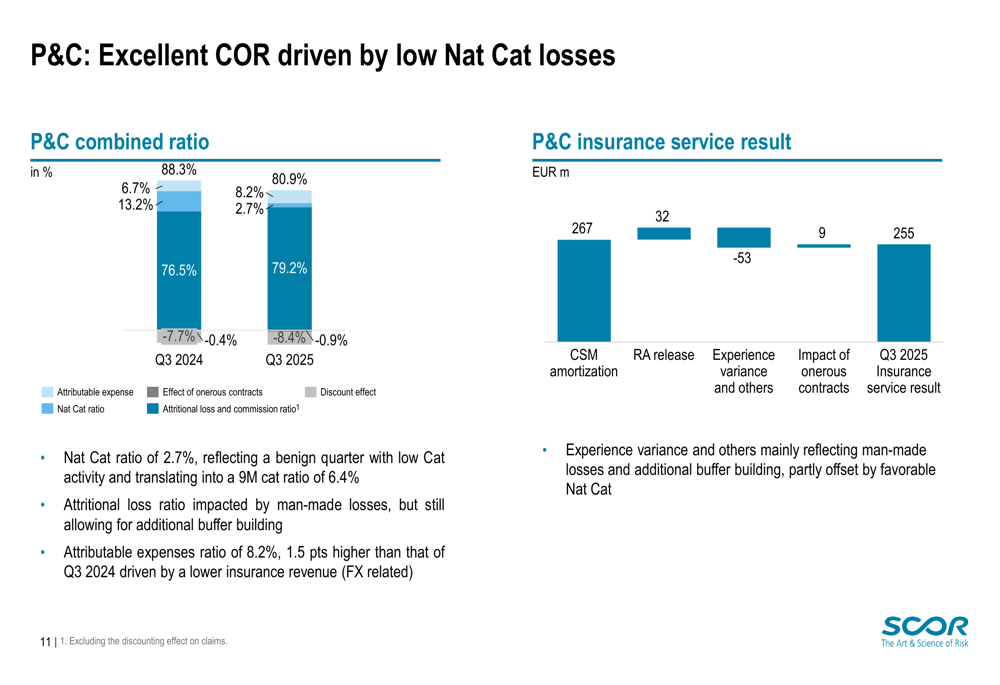

SCOR's P&C business delivered exceptional results in Q3 2025, with a combined ratio of 80.9%, a significant improvement from 88.3% in Q3 2024. This improvement was largely driven by a benign natural catastrophe environment, with the nat cat ratio dropping to just 2.7% from 13.2% in the same period last year.

The following chart illustrates the combined ratio improvement and its components:

Despite the competitive market environment, SCOR maintained its strategic growth in P&C, focusing on preferred lines of business. The company generated €170 million in new business CSM (Contractual Service Margin), slightly down from €175 million in Q3 2024, partly due to adverse foreign exchange effects of €10 million.

P&C insurance revenue grew by 3.1% at constant exchange rates, driven primarily by growth in reinsurance, particularly in alternative solutions and specialty lines. The P&C segment delivered a strong insurance service result of €255 million, a 60% increase compared to Q3 2024.

L&H Business Performance

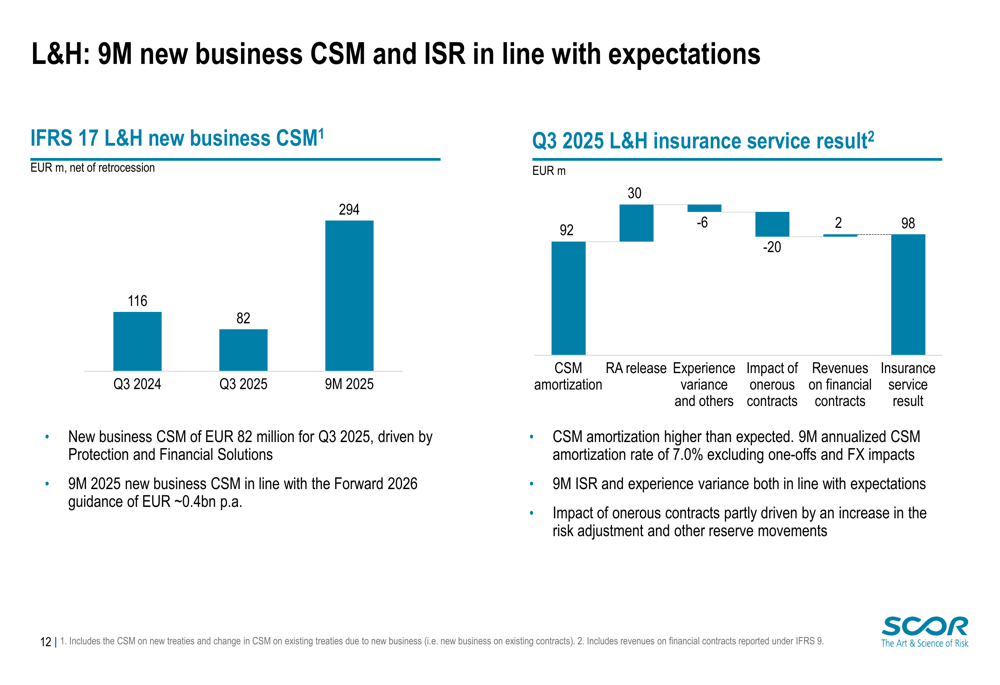

The Life & Health segment showed significant improvement compared to the previous year. The L&H insurance service result reached €98 million in Q3 2025, a substantial recovery from a €210 million loss in Q3 2024. This improvement reflects SCOR's successful management of its L&H portfolio.

The following chart provides details on L&H new business and insurance service result:

New business CSM in the L&H segment amounted to €82 million for Q3 2025, driven by Protection and Financial Solutions. While this represents a 29% decrease compared to Q3 2024, the nine-month new business CSM of €294 million remains in line with SCOR's Forward 2026 guidance of approximately €400 million per annum.

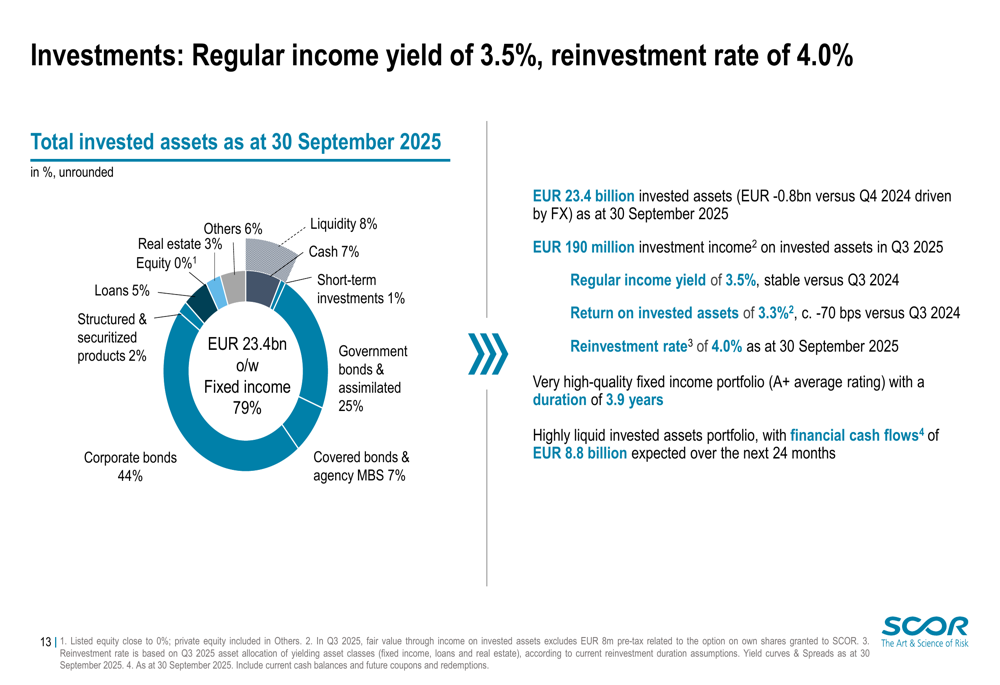

Investment Performance

SCOR maintained a solid investment performance in Q3 2025, with a return on invested assets of 3.3% and a regular income yield of 3.5%. The company's investment portfolio remains high-quality and liquid, with an average rating of A+ and a duration of 3.9 years.

As illustrated in the following asset allocation breakdown:

The company's total invested assets amounted to €23.4 billion as of September 30, 2025, a decrease of €0.8 billion compared to Q4 2024, primarily due to foreign exchange effects. The reinvestment rate stood at an attractive 4.0%, providing a positive outlook for future investment income.

SCOR's liquidity position remains strong, with cash and cash equivalents of €2.2 billion at the end of September 2025. Operating cash flows reached €1.0 billion in the first nine months of 2025, reflecting strong premium inflows and lower large claims payments in the P&C segment, as well as improved cash flows in the L&H segment.

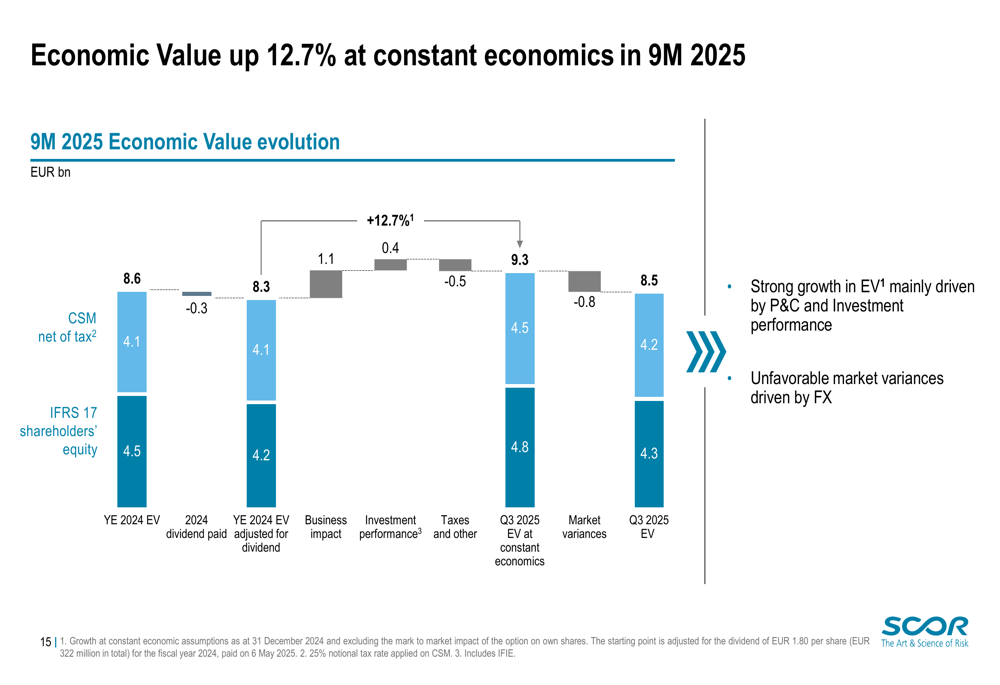

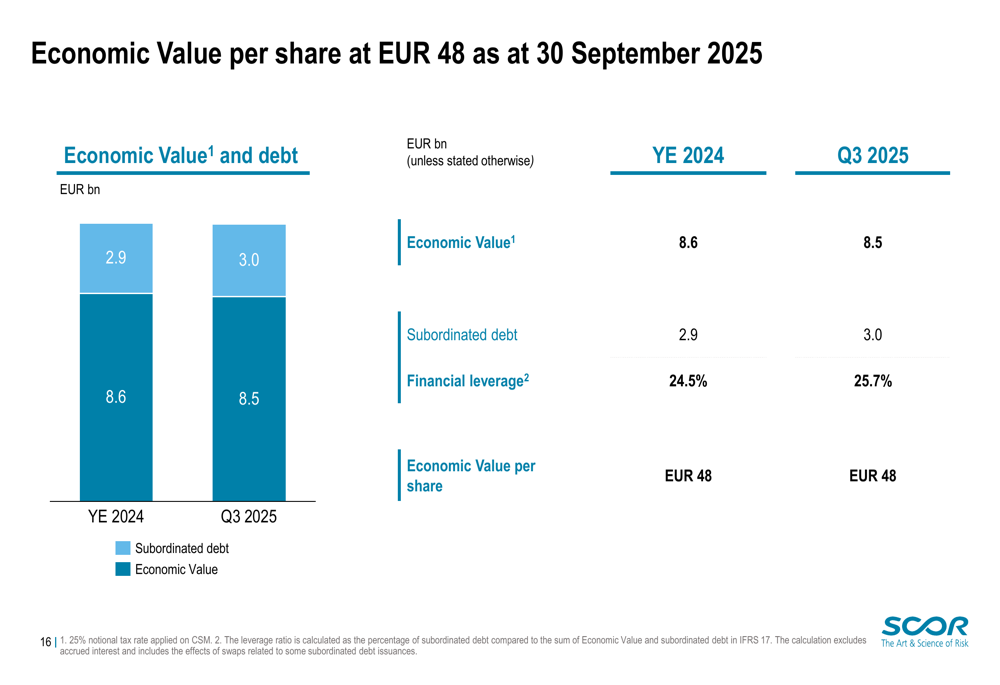

Economic Value and Solvency

SCOR's economic value grew by 12.7% at constant economics in the first nine months of 2025, reaching €8.5 billion. This growth was primarily driven by strong P&C and investment performance, partially offset by unfavorable foreign exchange effects.

The following chart illustrates the evolution of SCOR's economic value:

The company's economic value per share remained stable at €48, while the solvency ratio stood at a robust 210%, well within SCOR's optimal range of 185%-220%. This strong capital position provides the company with flexibility to pursue strategic opportunities while maintaining financial resilience.

Forward-Looking Statements

SCOR remains committed to its successful P&C strategy and underwriting discipline in an increasingly competitive environment. The company continues to focus on profitable and diversifying lines of business, with a clear emphasis on risk-adjusted returns.

For the L&H segment, SCOR targets an insurance service result of approximately €400 million per annum, in line with its Forward 2026 guidance. The investment strategy remains focused on maintaining a high-quality, liquid portfolio while capitalizing on attractive reinvestment opportunities.

As CEO Thierry Léger emphasized during the earnings call, "We are here for the long term and support our clients when they need us." He also highlighted the company's disciplined approach to capital deployment, stating, "We will stay focused on fundamentals and deploy capital where risk-adjusted returns are adequate."

Despite market challenges, including increasing competition, climate-related risks, geopolitical tensions, and cyber threats, SCOR's diversified business model and strong financial position provide a solid foundation for continued performance. The company's focus on disciplined underwriting and strategic growth initiatives positions it well to navigate the evolving reinsurance landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.