Street Calls of the Week

Introduction & Market Context

Scotts Miracle-Gro Company (NYSE:SMG) released its second quarter fiscal 2025 earnings presentation on April 30, showing mixed results as the company navigates a challenging sales environment while making progress on margin recovery initiatives. Despite reporting improved profitability metrics, SMG shares fell 7.54% on the day, closing at $49.50, reflecting investor concerns about the sales decline.

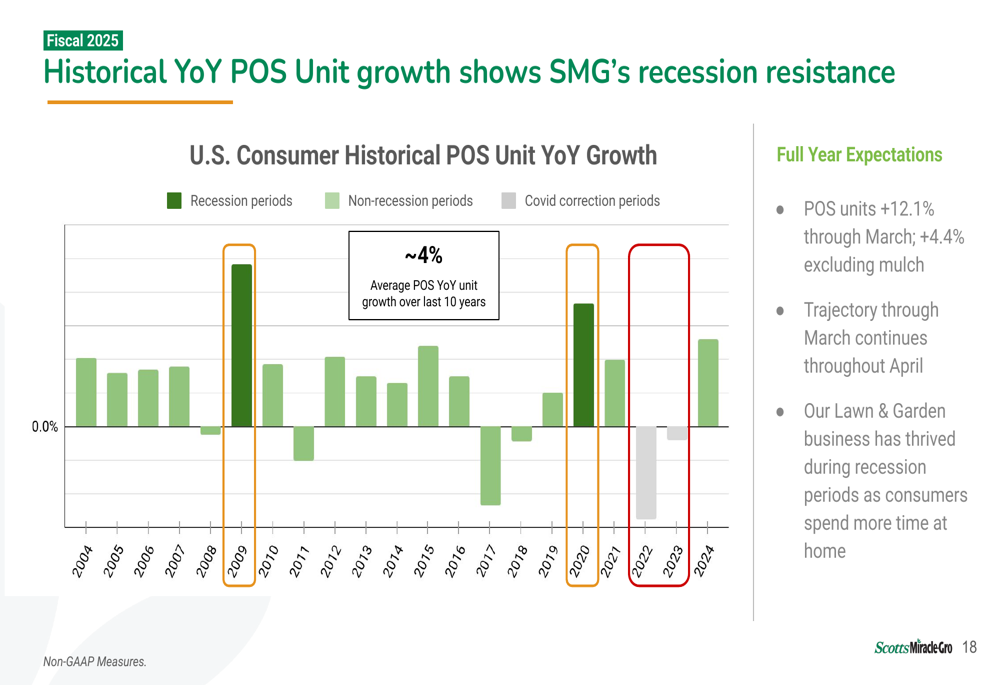

The company’s presentation highlighted its strategic focus on strengthening margins and the balance sheet while investing in brand development, even as total net sales decreased 7% compared to the same period last year. The results come as the lawn and garden industry continues to show resilience, with point-of-sale (POS) unit growth of 12.1% through March (4.4% excluding mulch).

Quarterly Performance Highlights

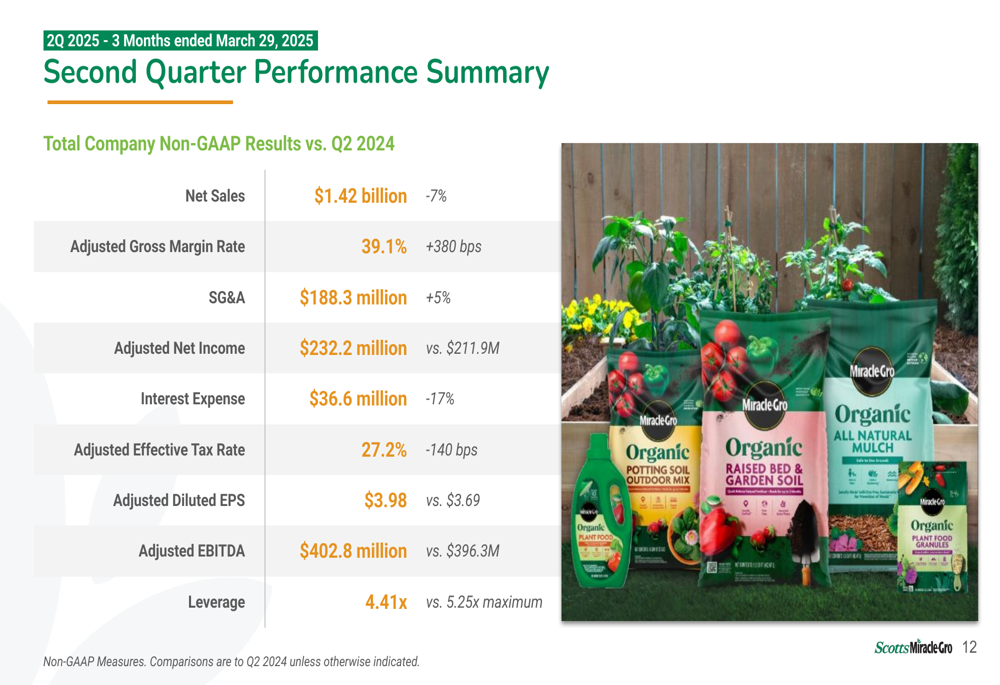

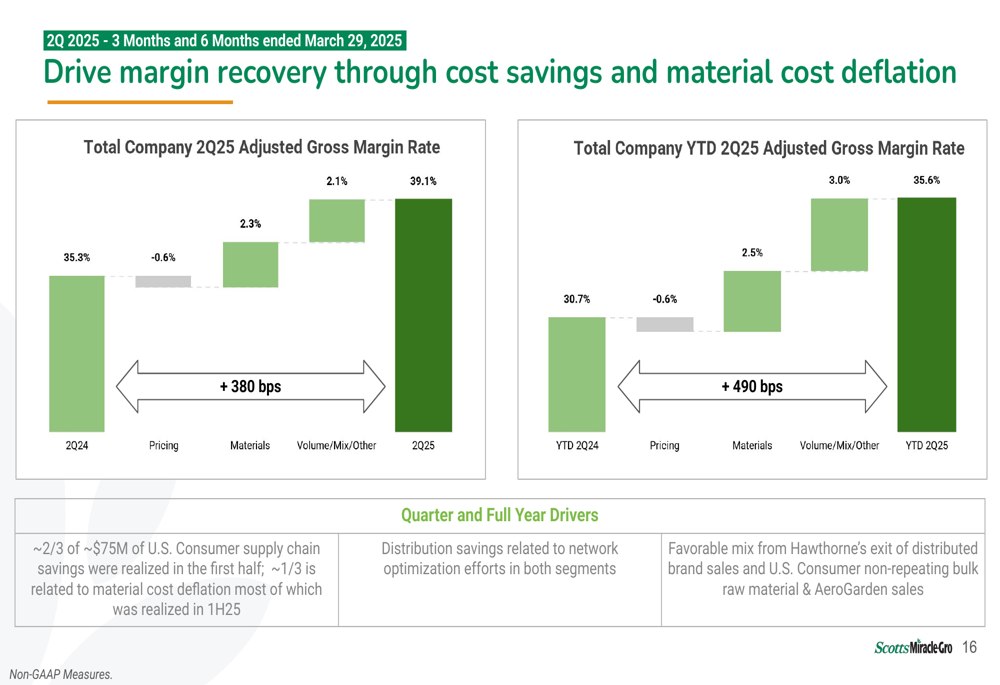

Scotts Miracle-Gro reported second quarter net sales of $1.42 billion, down 7% from $1.53 billion in Q2 2024. Despite the revenue decline, the company achieved significant margin improvement, with adjusted gross margin increasing 380 basis points to 39.1%.

As shown in the following performance summary:

The company’s adjusted earnings per share rose to $3.98 from $3.69 in the prior year, while adjusted EBITDA increased slightly to $402.8 million from $396.3 million. This improvement in profitability metrics came despite the sales decline, highlighting the company’s success in cost management and margin enhancement initiatives.

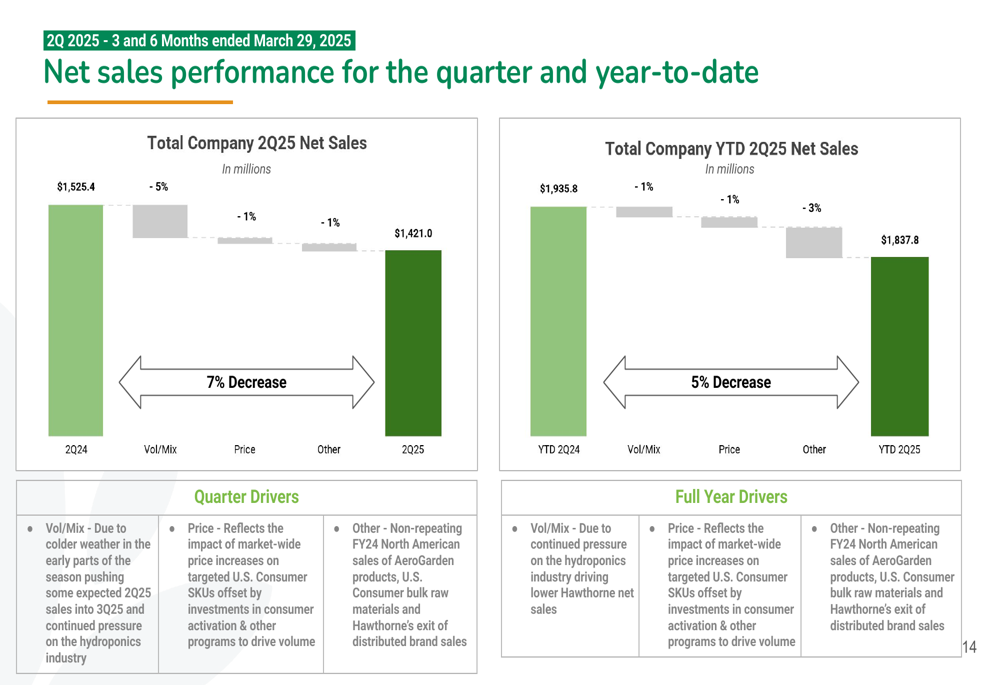

The sales performance breakdown revealed challenges across segments:

According to the presentation, the sales decline was driven by several factors, including colder weather, the company’s exit from certain business lines, and the timing of shipments. The U.S. Consumer segment, which represents the core of the business, saw a 3% decline in the quarter.

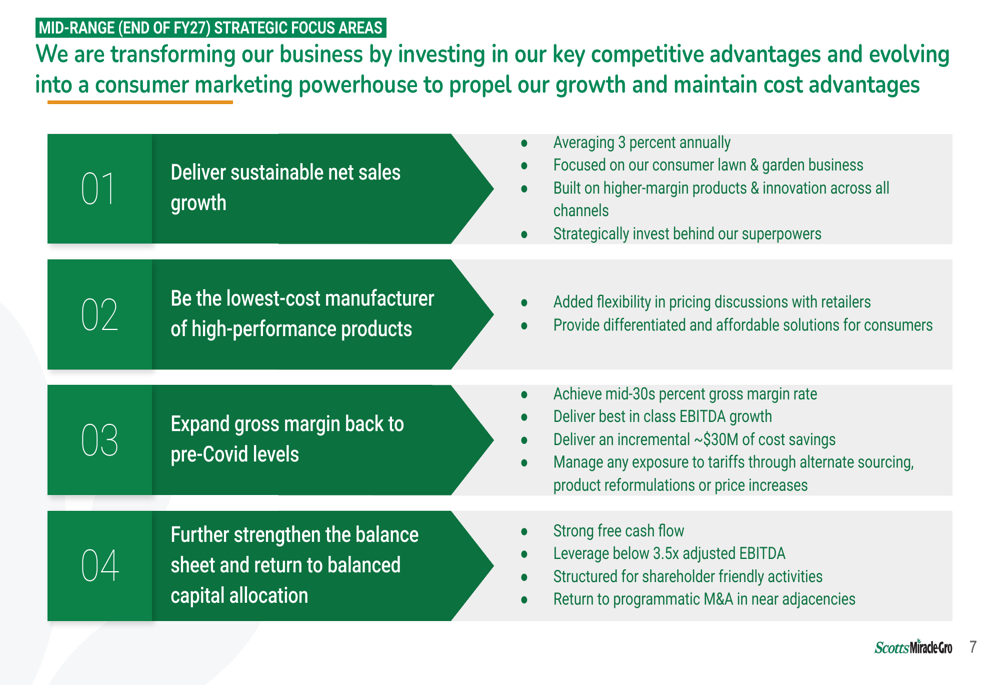

Strategic Initiatives

Scotts Miracle-Gro outlined four key mid-range strategic focus areas aimed at driving sustainable growth and improving financial performance through fiscal 2027:

A central element of the company’s strategy involves increased investment in advertising and brand development. The presentation detailed significant increases in media investments across its brand portfolio:

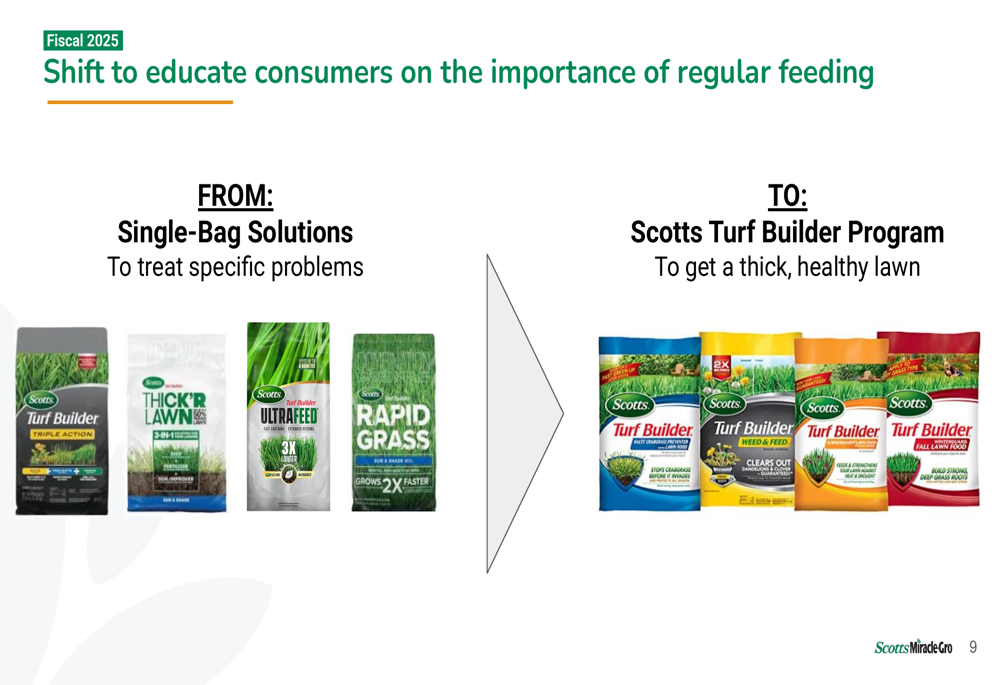

The company is also executing a strategic shift in its consumer education approach, moving from promoting single-bag solutions to encouraging regular lawn feeding through the Scotts Turf Builder Program:

Detailed Financial Analysis

Margin recovery remains a key focus for Scotts Miracle-Gro, with the company making substantial progress in the second quarter. The presentation highlighted the drivers behind the 380 basis point improvement in adjusted gross margin:

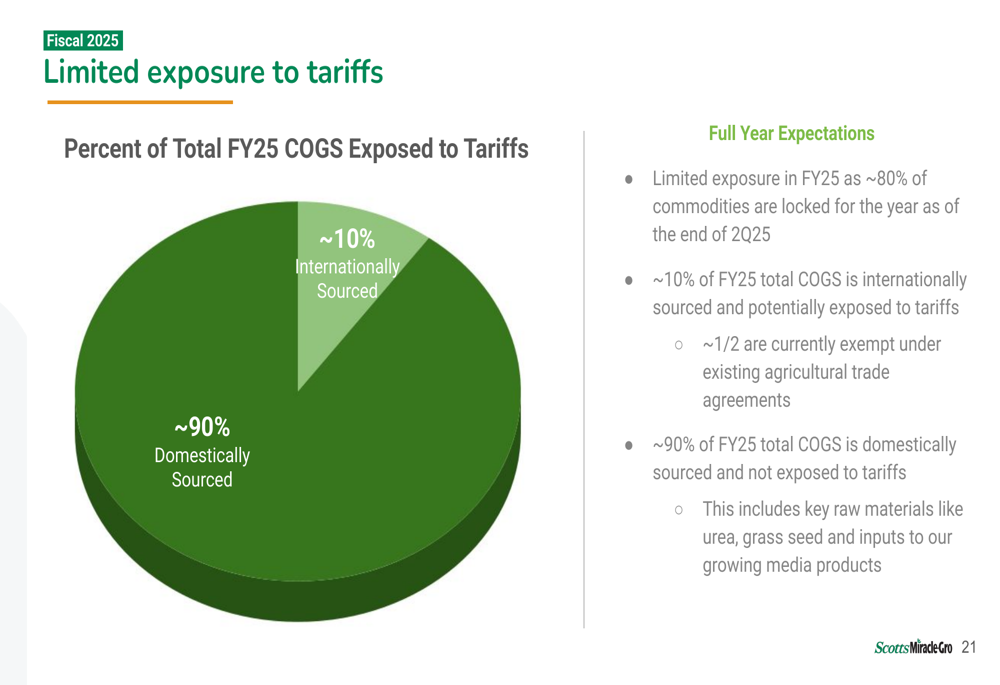

The company emphasized its limited exposure to potential tariff impacts, noting that approximately 90% of its cost of goods sold comes from domestically sourced materials:

Scotts Miracle-Gro also pointed to its historical resilience during economic downturns, presenting data showing the company’s point-of-sale unit growth trends over the past two decades:

The presentation noted that the lawn and garden industry has maintained relatively low exposure to private label competition, with private label unit share declining from approximately 14% in 2019 to around 10% in 2024.

Forward-Looking Statements

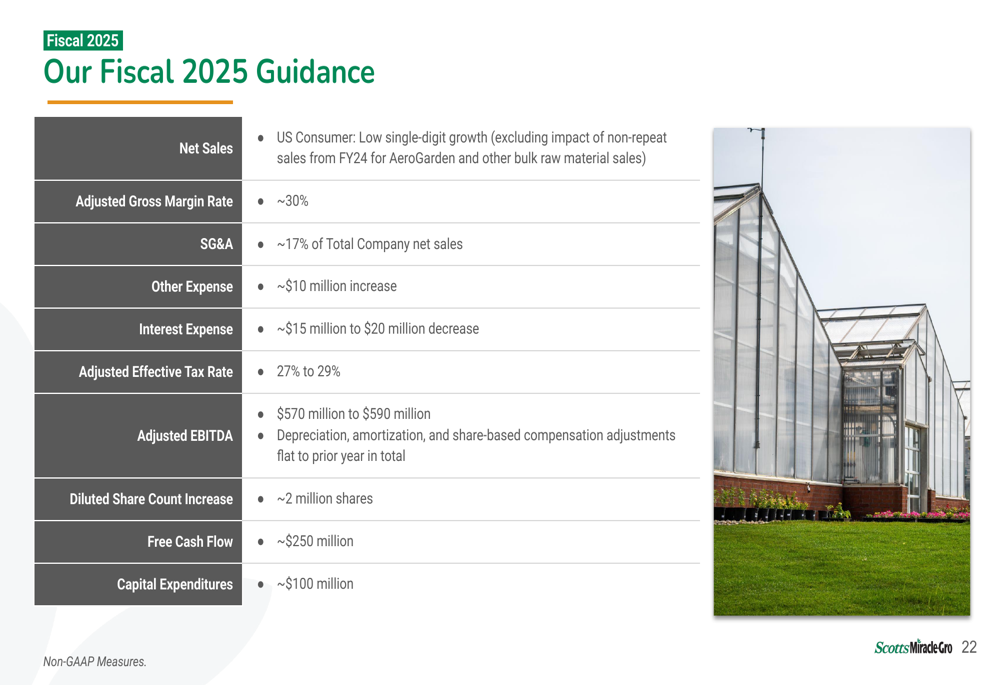

Looking ahead, Scotts Miracle-Gro provided guidance for fiscal 2025, projecting low single-digit growth for its U.S. Consumer segment (excluding non-repeating sales) and an adjusted gross margin of approximately 30%:

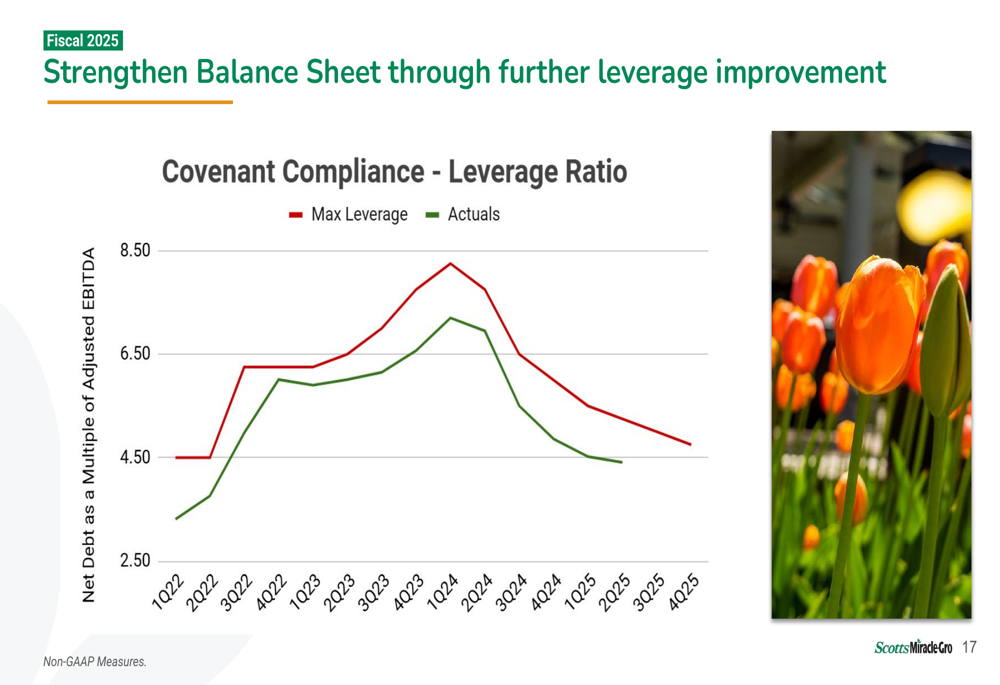

The company expects adjusted EBITDA of $570-590 million for the full year and anticipates generating approximately $250 million in free cash flow. Management also reiterated its commitment to strengthening the balance sheet, with a focus on reducing leverage below 3.5x adjusted EBITDA.

The guidance reflects management’s confidence in continued margin improvement, with expectations for adjusted gross margin to increase by approximately 370 basis points compared to fiscal 2024, driven by supply chain savings, material cost deflation, and distribution efficiencies.

Despite the optimistic outlook on profitability, investors appeared concerned about the sales decline and the company’s ability to return to sustainable growth, as reflected in the stock’s negative performance following the earnings presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.