How are energy investors positioned?

Introduction & Market Context

Scotts Miracle-Gro Company (NYSE:SMG) released its third-quarter 2025 earnings presentation on July 30, revealing improved profitability metrics despite a modest sales decline. The company’s shares rose 0.84% in premarket trading to $68.43, suggesting a positive reception following the previous quarter’s significant stock drop of 14.12% after a revenue miss.

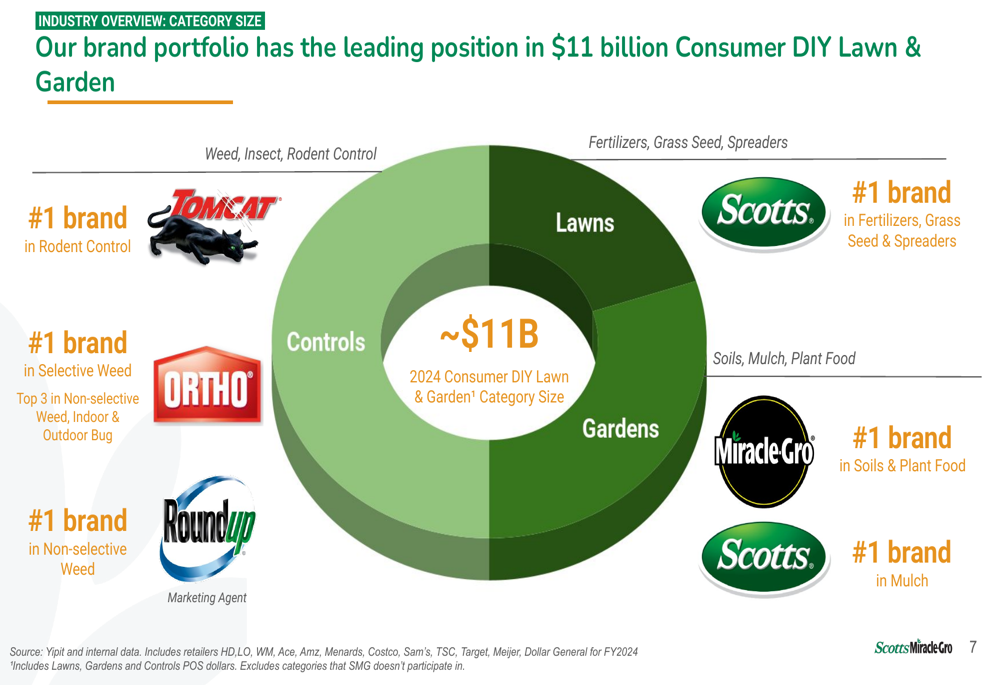

The presentation highlighted SMG’s dominant position in the $11 billion Consumer DIY Lawn & Garden market, where it maintains leading brands across key segments. This market strength provides a foundation for the company’s ongoing transformation initiatives focused on cost reduction, margin improvement, and strategic growth investments.

As shown in the following chart of the company’s brand portfolio and category positioning:

Quarterly Performance Highlights

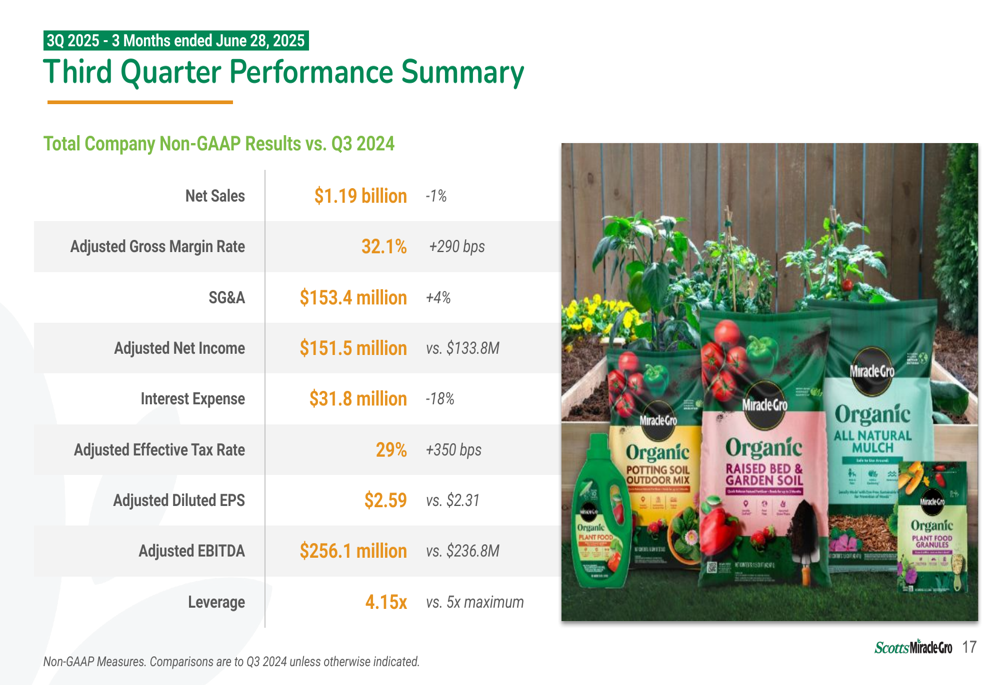

For the third quarter ended June 28, 2025, Scotts Miracle-Gro reported net sales of $1.19 billion, a 1% decrease compared to the same period last year. However, the company achieved significant profitability improvements, with adjusted gross margin expanding 290 basis points to 32.1% and adjusted EBITDA increasing to $256.1 million from $236.8 million in Q3 2024.

Adjusted diluted earnings per share rose to $2.59 from $2.31 in the prior year, representing a 12% increase. The company also reported a reduced leverage ratio of 4.15x, down from the maximum threshold of 5x, demonstrating progress in strengthening its balance sheet.

The quarterly performance summary is illustrated in the following slide:

By segment, U.S. Consumer sales increased 1% in the quarter, while Hawthorne (the company’s hydroponic and indoor growing business) continued to struggle with a 54% sales decline. The "Other" segment, which includes international operations, showed 8% growth. Year-to-date, U.S. Consumer sales were down 1%, Hawthorne declined 46%, and Other grew 3%, resulting in a total company year-to-date sales decline of 4%.

Strategic Initiatives

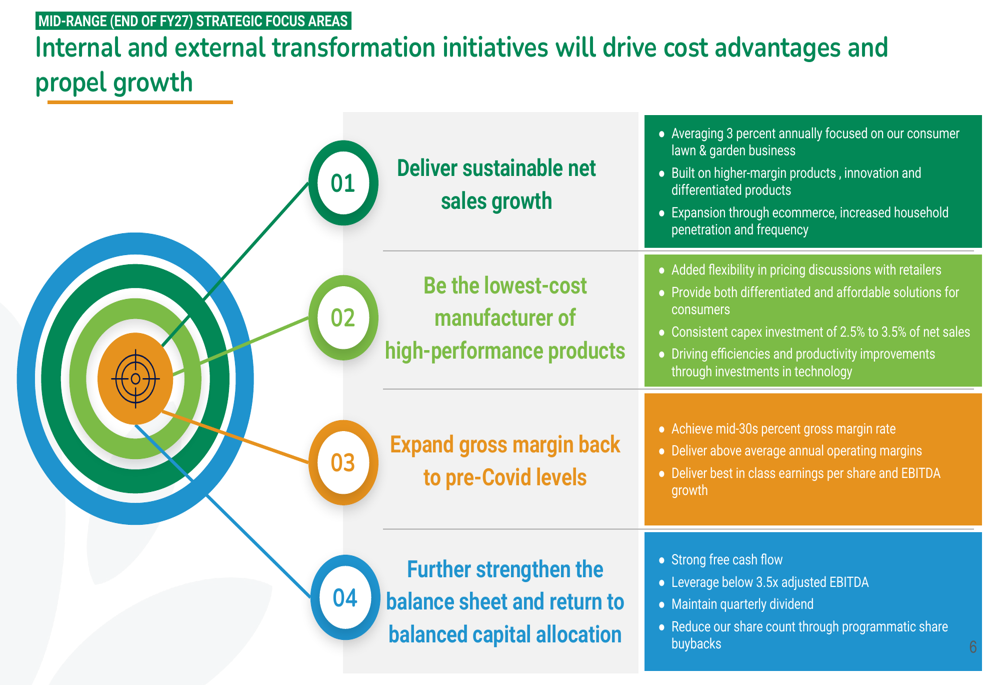

Scotts Miracle-Gro outlined four key strategic focus areas aimed at driving sustainable growth and profitability through fiscal 2027. These initiatives include delivering 3% annual sales growth in the consumer lawn and garden business, becoming the lowest-cost manufacturer, expanding gross margins to pre-Covid levels, and strengthening the balance sheet.

The company’s mid-range strategic roadmap is visualized in this comprehensive slide:

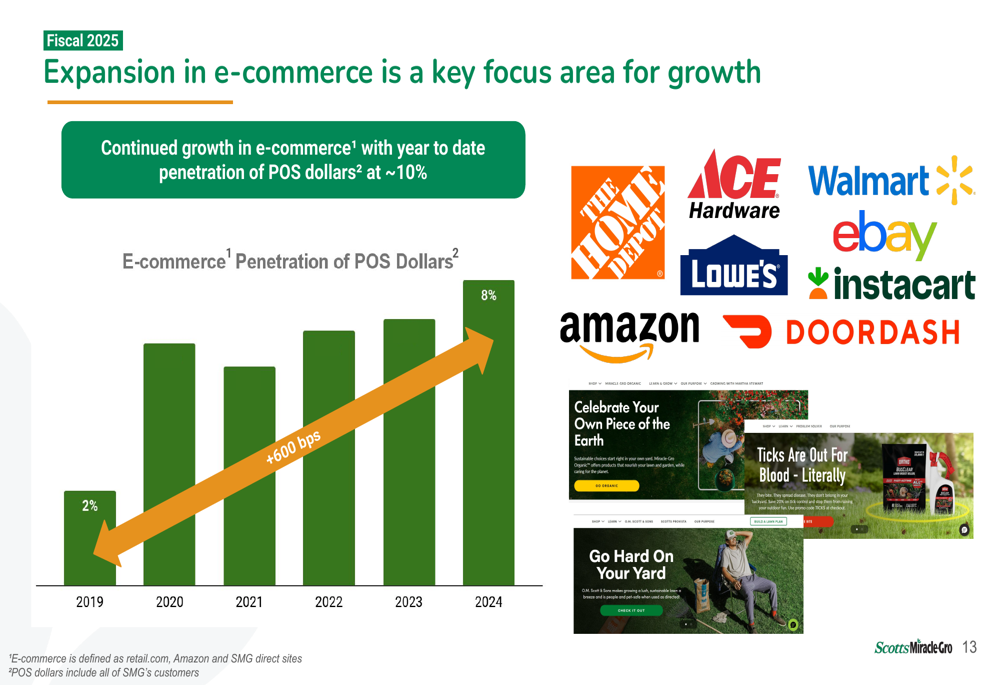

A significant component of SMG’s strategy involves expanding its e-commerce presence, which has grown from just 2% of POS dollars in 2019 to approximately 10% year-to-date in 2025. This channel expansion includes partnerships with major retailers like Home Depot (NYSE:HD), Walmart (NYSE:WMT), Lowe’s (NYSE:LOW), and Amazon (NASDAQ:AMZN), as well as delivery services like Instacart (NASDAQ:CART) and DoorDash (NASDAQ:DASH).

The e-commerce growth trajectory is illustrated in the following slide:

The company is also investing heavily in brand health, with increased media investments showing positive results for key brands including Miracle-Gro, Scotts, ORTHO, and Roundup. These investments appear to be paying off, as year-to-date POS unit growth reached 8%, with particularly strong performance in soils (+12%) and grass seed (+16%).

Detailed Financial Analysis

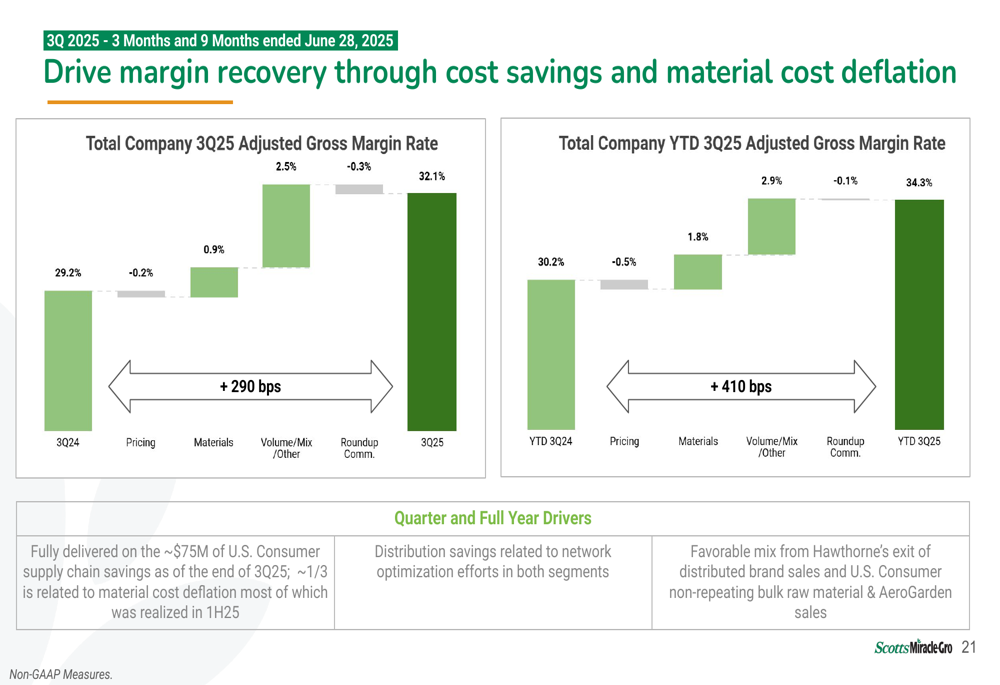

A key driver of SMG’s improved profitability is its supply chain transformation and cost savings initiatives. The company has fully delivered on approximately $75 million of U.S. Consumer supply chain savings as of the end of Q3 2025, with about one-third related to material cost deflation. Additional savings came from distribution network optimization and favorable product mix.

The margin recovery progress is visualized in this chart:

Notably, Scotts Miracle-Gro has limited exposure to potential tariff impacts, with approximately 90% of its FY25 COGS domestically sourced. Of the 10% that is internationally sourced, about half is currently exempt from tariffs under existing agricultural trade agreements. The company has also locked in commodity prices for the remainder of fiscal 2025, providing cost certainty.

The company’s SG&A expenses increased 4% to $153.4 million in the quarter, reflecting continued investments in brand support and consumer activation. Interest expense decreased 18% to $31.8 million, benefiting from debt reduction efforts. The adjusted effective tax rate increased 350 basis points to 29%.

Forward-Looking Statements

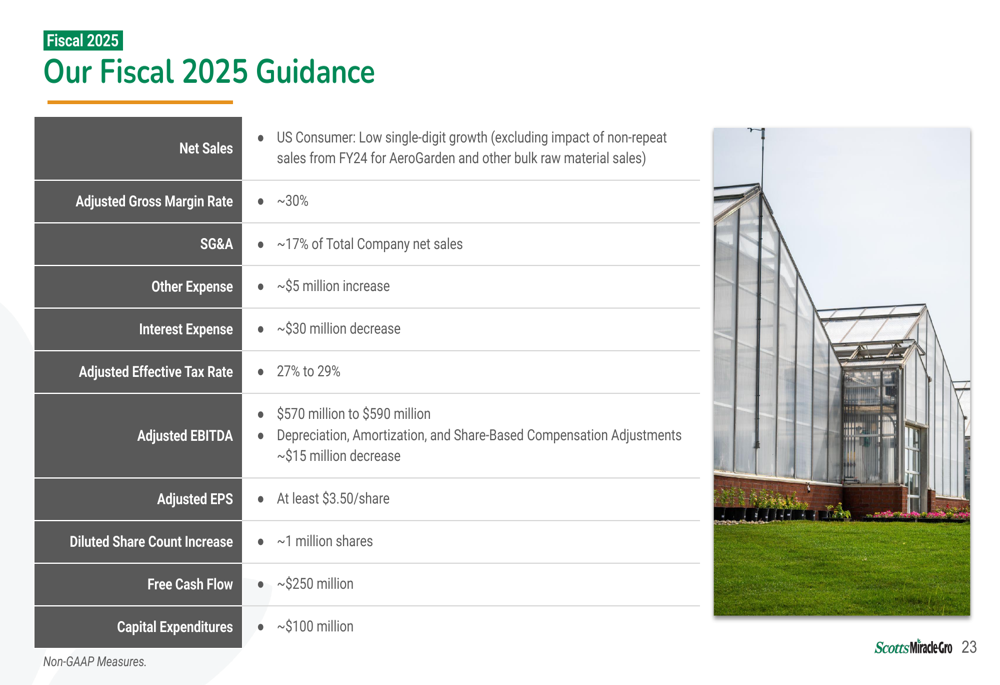

Looking ahead, Scotts Miracle-Gro reaffirmed its fiscal 2025 guidance, projecting adjusted EBITDA of $570-590 million and adjusted EPS of at least $3.50 per share. The company expects low single-digit growth in its U.S. Consumer segment (excluding non-repeat sales from FY24) and an adjusted gross margin rate of approximately 30% for the full year.

The detailed fiscal 2025 guidance is presented in this comprehensive slide:

Beyond the current fiscal year, SMG is targeting mid-30s percent gross margin by FY27 and aims to reduce its leverage ratio to below 3.5x by the end of FY27, which would position the company for more balanced capital allocation thereafter. The company expects to generate approximately $250 million in free cash flow in FY25, with the majority directed toward debt reduction while maintaining its quarterly dividend.

CFO Mark Scheiwer noted during the presentation that the company’s supply chain team is "doing an outstanding job delivering on cost savings initiatives" with $75 million of cost savings in FY25 and "another $75 million to go over ’26 & ’27." This ongoing transformation includes investments in technology, IoT, advanced robotics, automation, and real-time data analytics to drive operational efficiency.

As Scotts Miracle-Gro continues to execute its transformation strategy, investors will be watching closely to see if the margin improvements and cost savings can offset the challenging sales environment and drive sustainable long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.