InvestingPro’s Fair Value model captures 63% gain in Steelcase ahead of acquisition

Introduction & Market Context

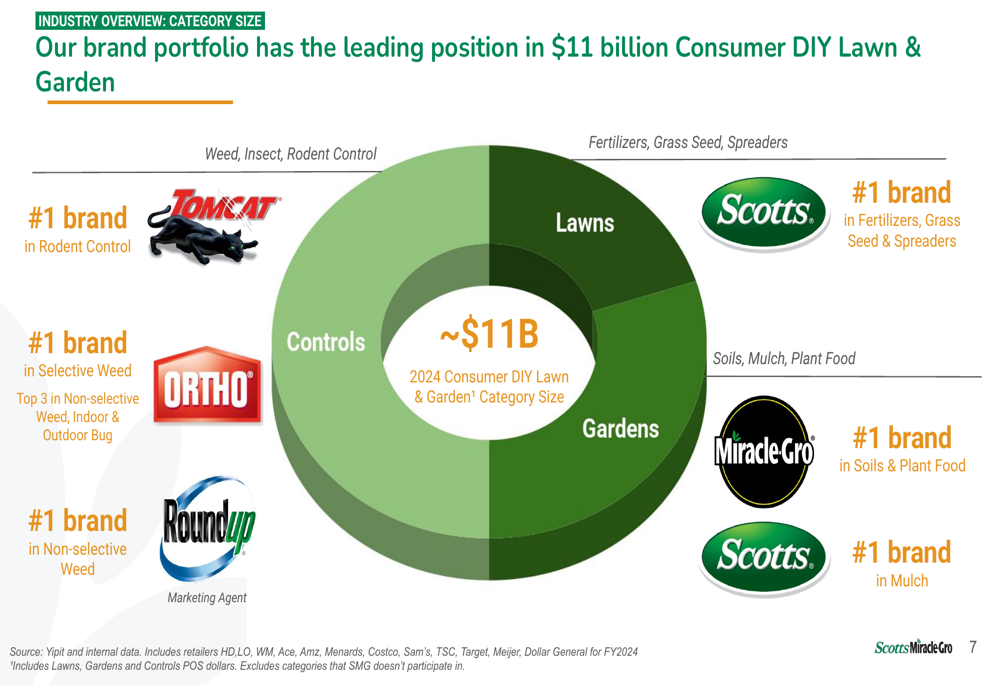

Scotts Miracle-Gro (NYSE:SMG) presented its third quarter 2025 earnings on July 30, showcasing improved profitability metrics despite a modest decline in overall sales. The company maintains a dominant position in the $11 billion Consumer DIY Lawn & Garden market with leading brands across multiple product categories, positioning itself for sustainable growth through strategic initiatives focused on margin expansion and digital transformation.

The presentation, delivered by CEO Jim Hagedorn and CFO Mark Scheiwer, highlighted the company's progress on its mid-range strategic goals while navigating a competitive retail landscape. SMG shares closed at $55.44 on October 14, 2025, up 1.39% and showing steady recovery from its 52-week low of $45.61, though still well below its 52-week high of $93.90.

Quarterly Performance Highlights

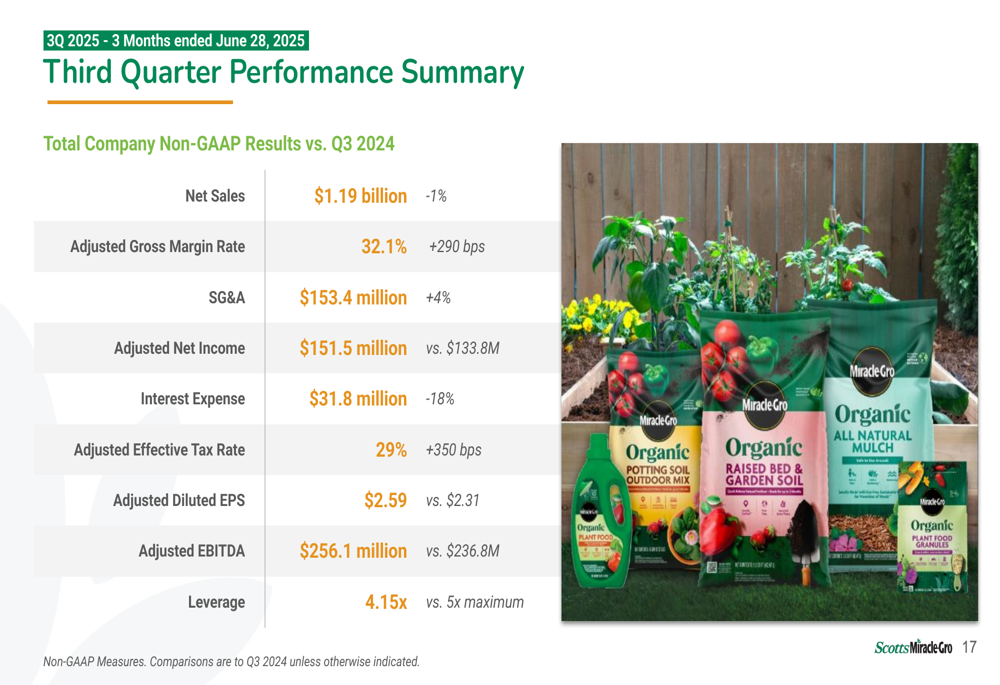

For the three months ended June 28, 2025, Scotts Miracle-Gro reported total net sales of $1.19 billion, representing a 1% year-over-year decline. However, the U.S. Consumer segment, which represents the company's core business, grew by 1% to $1.03 billion. More importantly, profitability metrics showed significant improvement across the board.

The company achieved an adjusted gross margin rate of 32.1%, an increase of 290 basis points compared to Q3 2024. This margin expansion contributed to adjusted net income of $151.5 million, up from $133.8 million in the prior year. Adjusted diluted earnings per share reached $2.59, compared to $2.31 in Q3 2024, while adjusted EBITDA improved to $256.1 million from $236.8 million.

As shown in the following comprehensive performance summary:

The company also reported an 18% reduction in interest expense to $31.8 million, reflecting progress in debt management. The leverage ratio improved to 4.15x, down from 5x, demonstrating the company's commitment to strengthening its balance sheet.

Consumer takeaway metrics were particularly strong, with year-to-date point-of-sale (POS) unit growth of 8%. Several product categories showed robust growth, including Soils (+12%), Grass Seed (+16%), and Controls (+3%), while Branded Fertilizer posted a modest 1% increase.

The following chart illustrates Scotts' leading position across key lawn and garden categories:

Strategic Initiatives

Scotts Miracle-Gro outlined four key strategic focus areas aimed at driving sustainable growth through fiscal year 2027:

1. Delivering sustainable net sales growth averaging 3% annually

2. Becoming the lowest-cost manufacturer of high-performance products

3. Expanding gross margins back to pre-COVID levels (mid-30s)

4. Further strengthening the balance sheet and returning to balanced capital allocation

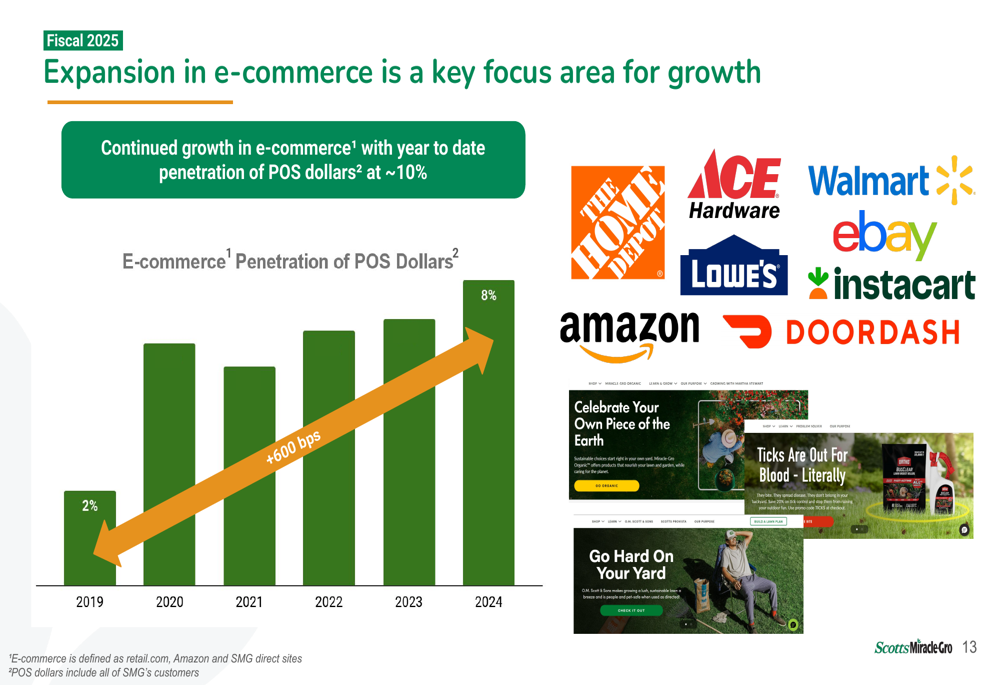

A significant component of this strategy involves the company's rapid expansion in e-commerce, which has grown from just 2% of POS dollars in 2019 to approximately 10% year-to-date in 2025. This digital transformation spans retail partner websites, Amazon, and Scotts' direct sites.

The company's e-commerce growth trajectory is illustrated below:

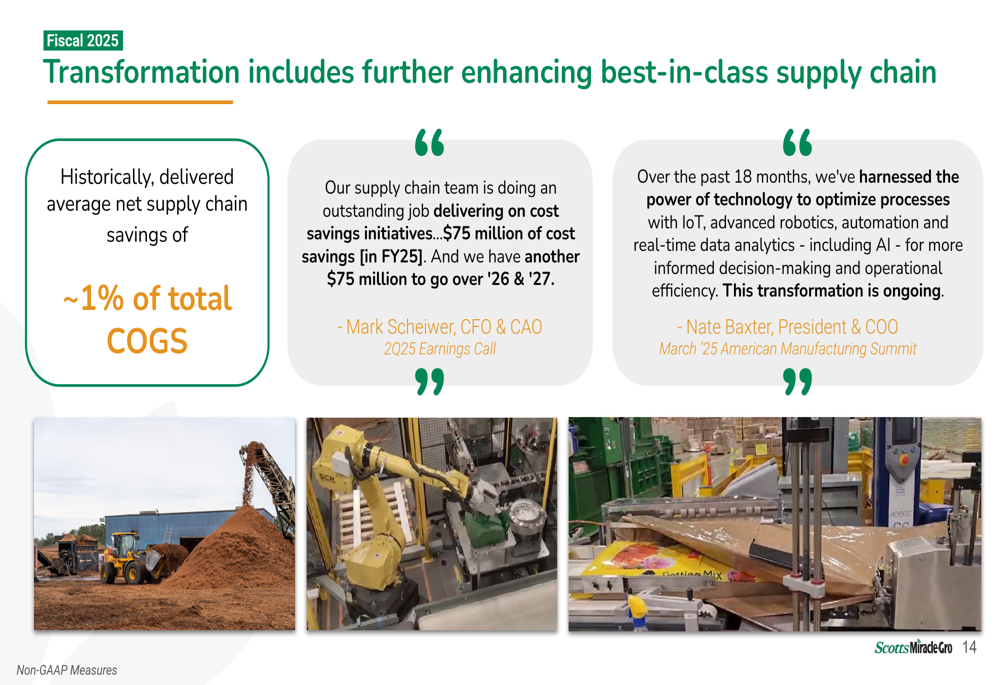

Supply chain transformation represents another critical strategic initiative. The company is implementing advanced robotics, automation, and AI-driven analytics to optimize processes and drive cost efficiencies. Management expects to deliver $150 million in supply chain cost savings over three years, with $75 million already achieved in FY25 and another $75 million targeted for FY26-27.

As shown in the following supply chain transformation overview:

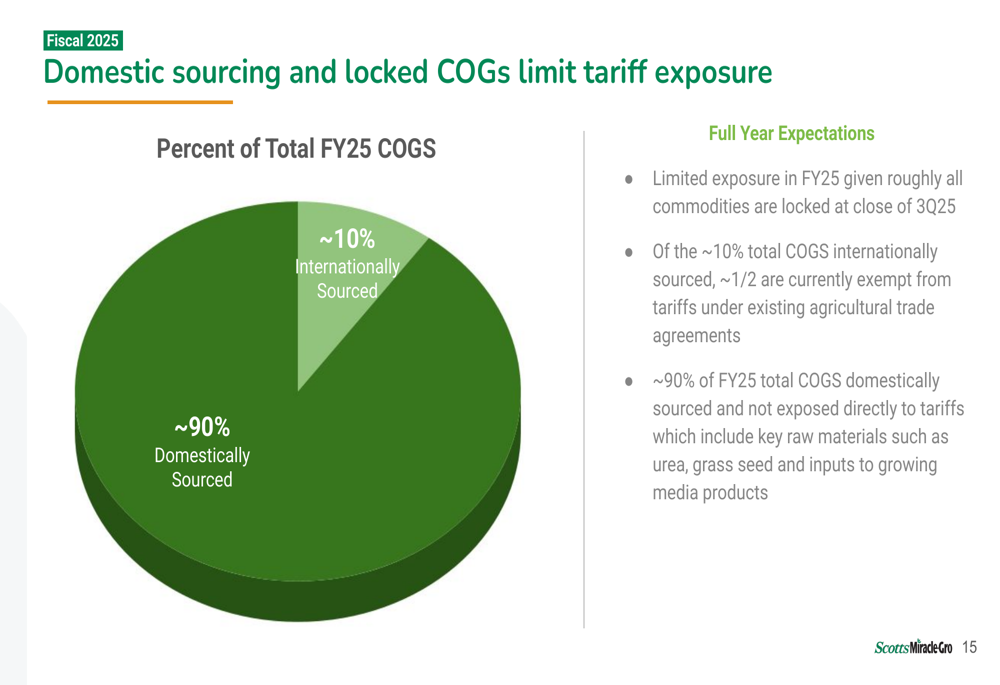

The company also highlighted its limited exposure to potential tariff increases, with approximately 90% of its cost of goods sold (COGS) being domestically sourced. Of the remaining 10% that is internationally sourced, roughly half is exempt from tariffs under existing agricultural trade agreements.

Forward-Looking Statements

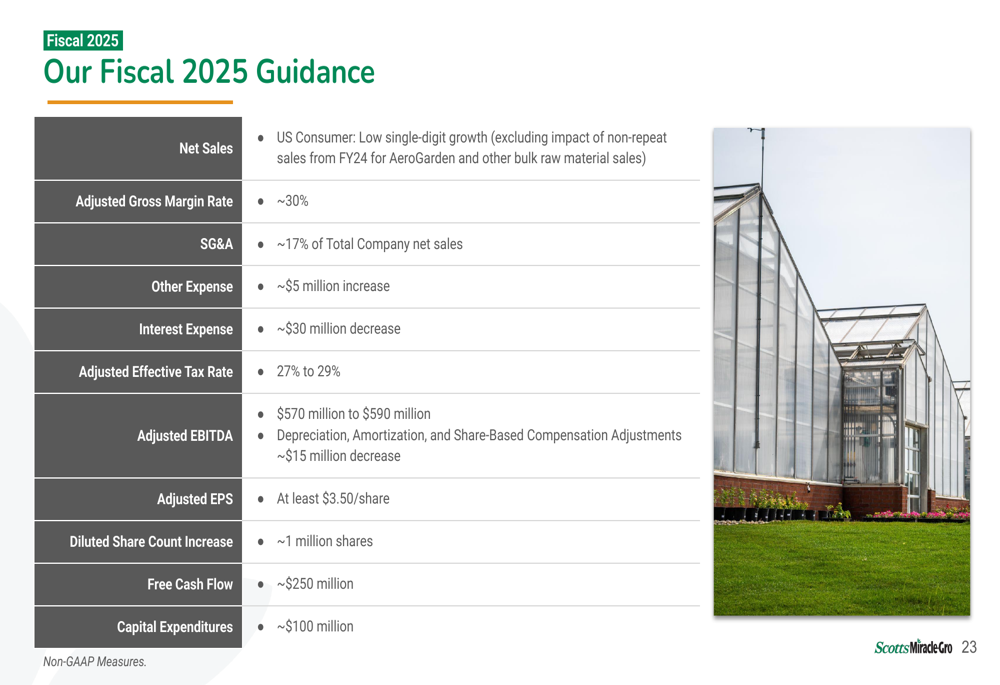

Scotts Miracle-Gro reaffirmed its fiscal 2025 guidance, projecting low single-digit growth for the U.S. Consumer segment and adjusted EBITDA of $570-590 million. The company expects to achieve a gross margin rate of approximately 30% for the full year, with continued improvement driven by cost savings initiatives and operational efficiencies.

Capital expenditures are projected at approximately $100 million, while interest expense is expected to decrease by around $30 million compared to the previous year, reflecting the company's progress in debt reduction.

The company's fiscal 2025 guidance is summarized below:

Looking beyond FY25, Scotts Miracle-Gro remains focused on its transformation initiatives to drive cost advantages and propel growth. The company aims to expand its gross margin back to pre-COVID levels in the mid-30s range, while maintaining leverage below 3.5x adjusted EBITDA.

Management emphasized the health of the lawn and garden consumer market and the company's commitment to investing in its brands, with over 10% of net sales dedicated to consumer activation and retail partner programs. These investments have led to positive gains in brand health metrics across the company's portfolio, including Miracle-Gro, Scotts, Ortho, Tomcat, and Roundup.

As Scotts Miracle-Gro continues to execute its strategic plan, the company appears well-positioned to leverage its market leadership and operational improvements to drive sustainable growth and enhanced shareholder value in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.