NVIDIA expands Microsoft partnership with Blackwell GPUs for AI infrastructure

Introduction & Market Context

Scotts Miracle-Gro (NYSE:SMG) released its fourth quarter and full-year fiscal 2025 results on November 5, showcasing significant margin improvement despite modest revenue challenges. The company’s stock reacted with a slight 0.26% increase in pre-market trading, reaching $54.60, as investors weighed the mixed performance against forward-looking guidance.

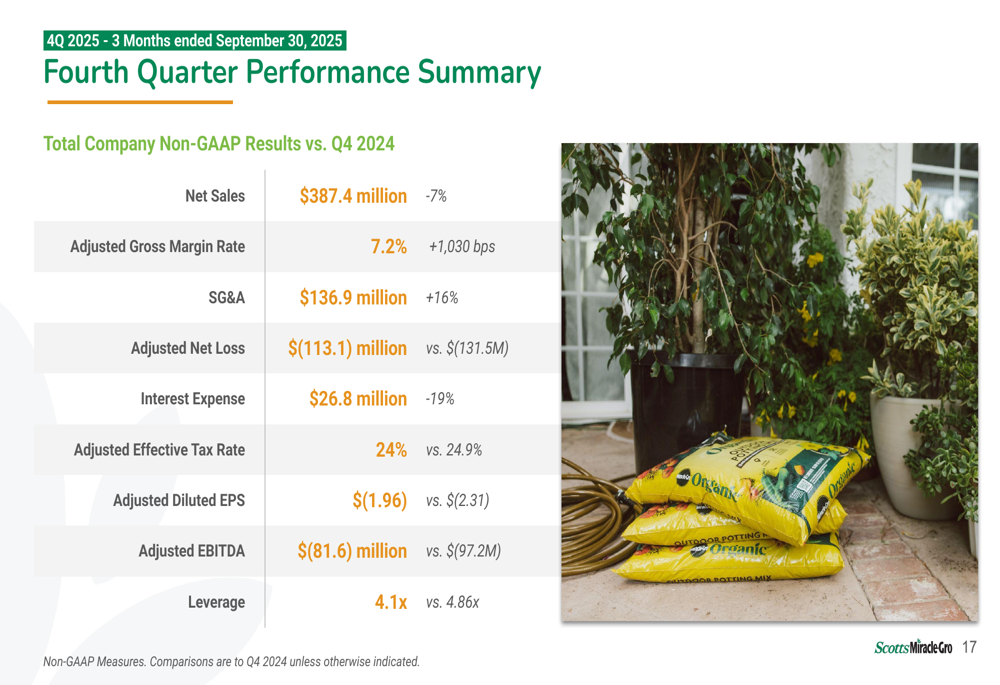

The lawn and garden products leader reported Q4 revenue of $387.4 million, missing analyst expectations of $396.2 million, but delivered a slight earnings beat with an adjusted EPS of -$1.96 compared to forecasts of -$1.97. For the full fiscal year, SMG achieved substantial margin expansion and EPS growth while implementing strategic initiatives across its business segments.

Quarterly Performance Highlights

Scotts Miracle-Gro’s fourth quarter showed a 7% year-over-year decline in net sales to $387.4 million, primarily driven by volume and mix challenges in the Hawthorne segment and other businesses. However, the U.S. Consumer segment demonstrated strength with a 4.4% volume/mix improvement during the quarter.

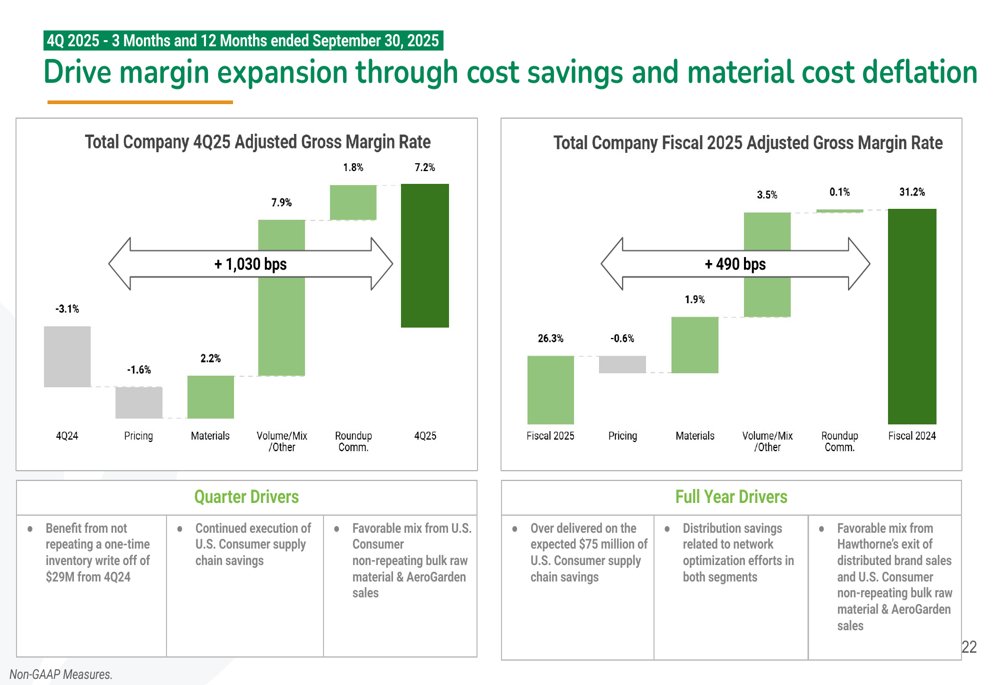

The most notable achievement was the dramatic improvement in adjusted gross margin rate, which increased by 1,030 basis points to 7.2% compared to -3.1% in Q4 2024. This improvement was driven by several factors, including material cost deflation, favorable volume/mix, and Roundup commission benefits.

As shown in the following performance summary from the company’s presentation:

Despite the seasonal net loss typical of the fourth quarter, SMG improved its adjusted net loss to $113.1 million from $131.5 million in the prior year. The company also reduced interest expense by 19% to $26.8 million, reflecting progress in debt reduction efforts.

Detailed Financial Analysis

For the full fiscal year 2025, Scotts Miracle-Gro reported net sales of $3.41 billion, representing a 4% decrease from fiscal 2024. However, the company achieved substantial improvements in profitability metrics, with adjusted gross margin expanding by 490 basis points to 31.2%.

The company’s fiscal 2025 performance summary highlights the significant earnings growth:

Adjusted EBITDA increased by $71 million or 14% to $581.1 million, while adjusted EPS grew by 63% to $3.74 per share compared to $2.29 in fiscal 2024. These improvements were driven by cost savings initiatives, with the company achieving approximately two-thirds of its targeted $150 million in supply chain cost savings.

Free cash flow reached $274 million, exceeding non-GAAP adjusted earnings, which enabled the company to pay down $120 million in debt. As a result, the leverage ratio improved to 4.1x from 4.86x in the prior year.

Competitive Industry Position

Scotts Miracle-Gro strengthened its leadership position in the $11 billion consumer DIY lawn and garden market during fiscal 2025, increasing its overall market share by 1%. The company maintains #1 brand positions across all key categories, including fertilizers, grass seed, weed control, soils, and mulch.

The presentation highlighted the company’s dominant market position and brand leadership:

An important competitive advantage for SMG is the limited threat from private label products. Private label unit share in the lawn and garden industry has decreased from 12.7% in 2019 to 9.7% in 2025, reflecting a decline of approximately 300 basis points. This trend supports the company’s brand-focused strategy and pricing power.

Strategic Initiatives

E-commerce expansion represents a significant growth opportunity for Scotts Miracle-Gro. In fiscal 2025, the company achieved 23% growth in e-commerce POS dollars and 51% growth in units. E-commerce penetration has increased dramatically from just 2% in 2019 to 10% in 2025.

The following slide illustrates this e-commerce growth trajectory:

Supply chain optimization and automation remain central to the company’s margin expansion strategy. As noted by CFO Mark Scheiwer, the company delivered $75 million in cost savings during fiscal 2025, with plans for an additional $75 million over fiscal years 2026 and 2027.

President and COO Nate Baxter emphasized technology investments: "Over the past 18 months, we’ve harnessed the power of technology to optimize processes with IoT, advanced robotics, automation and real-time data analytics - including AI - for more informed decision-making and operational efficiency."

For fiscal 2026, the company outlined specific focus areas for each business segment:

- Lawns: Drive feeding frequency and target new DIY lawn care consumers, especially younger generations

- Gardens: Attract emerging consumers with accessible, modern solutions including indoor and organic products

- Controls: Launch 10 new innovative products under the Ortho brand and grow digital presence

Forward-Looking Statements

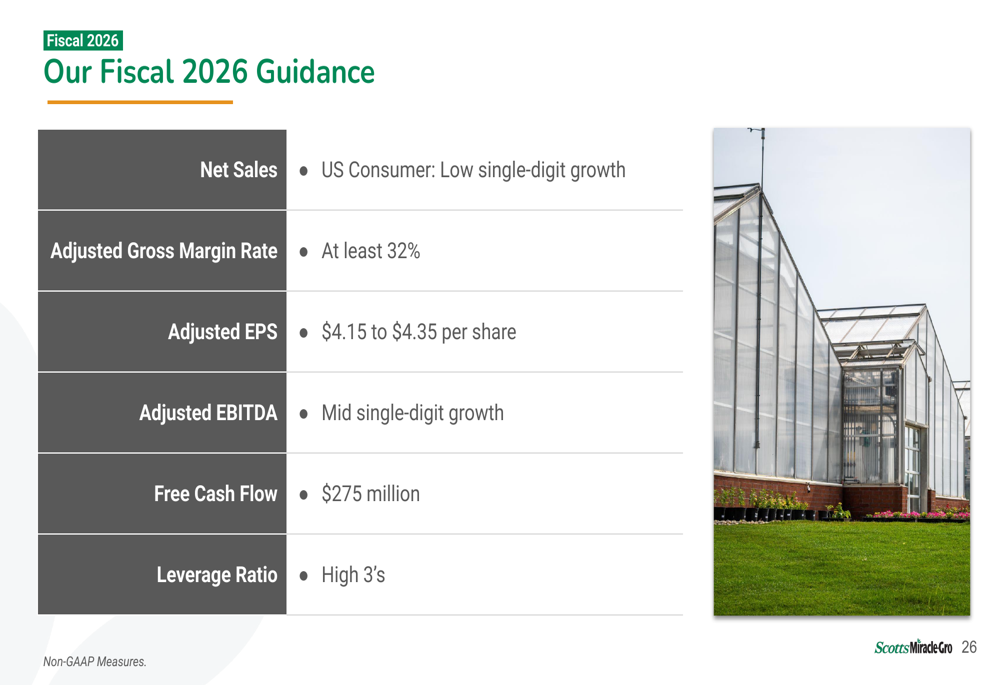

Looking ahead to fiscal 2026, Scotts Miracle-Gro provided optimistic guidance, expecting low single-digit growth in U.S. Consumer net sales and continued margin expansion:

The company projects adjusted EPS of $4.15 to $4.35 per share, representing growth from the $3.74 achieved in fiscal 2025. Adjusted EBITDA is expected to grow at a mid-single-digit rate, while free cash flow is targeted at $275 million.

A key financial objective is further strengthening the balance sheet, with plans to reduce the leverage ratio to the "high 3’s" by the end of fiscal 2026. This would represent continued improvement from the 4.1x ratio at the end of fiscal 2025.

The company’s margin expansion strategy is expected to continue delivering results, with a target of achieving at least a 32% adjusted gross margin rate in fiscal 2026:

CEO Jim Hagedorn emphasized the company’s return to its historical profile as a "safe harbor, high return equity," suggesting confidence in the strategic direction despite ongoing market challenges.

With strong brand leadership, e-commerce momentum, and significant cost savings initiatives underway, Scotts Miracle-Gro appears well-positioned to continue its profitability improvements in fiscal 2026, even as it navigates a competitive consumer landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.